Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP on Friday BEFORE JPOW …

ZH: US Manufacturing Surveys Signal Stagflation: Prices Paid Up As Jobs Drop

… and on that — JPOW went on to apparently WIN the internet as …

ZH: Powell Comments Send Everything Soaring, Gold Hits All Time High As Dollar Plummets As Market Prices In Rate Cuts

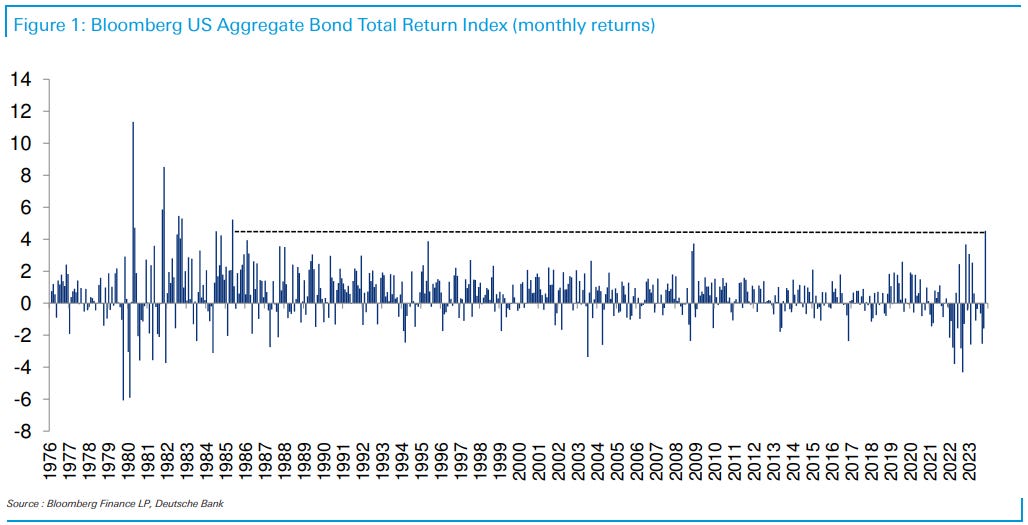

… AND as the week finished UP it looks to ME like long bond yields testing ‘resistance’ from back in October of LAST year (4.423) …

… and forgive me for ‘markin’ this one up more than normal BUT you can see that momentum can and will remain overbought for longer than some shorts might be willing to keep capital committed. Have a look at the last time … in fact it was this time last year when rates dropped from about where they are now down TO 3.40% (so, a 100bps) and THEN …

Barclays rates weekly, “The last mile” (10yy look too low)

… If we assume that the Fed will over time lower the policy rate from 5.3% to 3-3.25%, reflecting rstar of 1% and inflation of 2-2.25%, the 10y average of the policy rate would be 3.5% at YE23. If we instead assume an r-star of 1.5% and a steady state rate of 3.5-3.75%, the 10y average of the policy rate would be 3.9% at YE23. We believe long run r-star has meaningfully shifted higher from pre-COVID levels, reflecting structurally wider budget deficits, the increase in the dependency ratio and the greater investment needs related to green energy. These should shift the saving/investment balance away from excess savings, which plagued the pre-COVID era of low and potentially negative real neutral rate, despite only a modest drop in trend growth expectations. We would put the point estimate closer to 1.5%, which would still be somewhat below trend growth estimate of 1.8%, and would be between the 0.5% pre-COVID and 2.5% preGFC estimates.

Hence, at 4.35%, the implied term premium in 10y yields is about 45bp ( = 4.35% - 3.9%). After accounting for a 35bp swap spread, that leaves just 10bp for rate term premium. We find that too low in an environment of historically elevated macro uncertainty (Figure 9), which should be exacerbated by duration supply-demand mismatches…

… we maintain that summer is the earliest potential timeline on which the Fed will commence what we expect will be framed as "fine tuning" the stance of policy.

… In Summary Bond market volatility remains high. In the last six months, the iShares Treasury fund (TLT) has moved between $82 and $104 or a 26% range. The S&P 500 range has been around 11%. But as the Fed’s intentions clarify and if inflation and the employment numbers come in at the expected levels in the next few weeks, we’d expect bond volatility to settle down. It’s been a rough 22-months but the end seems in sight.

… Fade front-loading of cuts in US front end. With roughly 135bp of easing priced by December 2024 (and nearly 60bp of cuts to the Fed funds rate by next June), we think markets are approaching the limits of what can plausibly be priced without attaching material odds of a recession in the near term … It appears to us that markets are overinterpreting Fed governor Chris Waller’s comments. In our view, the Fed will likely have some inflation risk management considerations in mind that should limit how aggressively it might ease. If it were to ease in line with current market pricing in the absence of clear recessionary signals, and solely because of inflation normalization, there would likely be further significant easing of financial conditions, increasing the risk of a reacceleration of the economy. Given that the current growth slowdown will still leave it at roughly around trend next year, a reacceleration would likely be inflationary and therefore perceived as unwelcome by the Fed. We therefore recommend taking profits on our received 1y OIS position, and instead recommend fading some of the front-loaded cut pricing by selling June 2024 SOFR (SFRM4 95.25) calls.

… best be summarized as a steep deceleration in growth from Q3 2023 into a recession by Q1 2024, and a strong recovery at the end of the year and into 2025; a "ski jump" when plotted on a chart

After having tried twice to get long duration this year and failing, we tried again and the third time was a charm. We suggest staying long and buying any dips that arise … We switch long 30y exposure in US rates, to long UST 10y …

Retain a long duration bias until mid-year. Go long the belly in UST 2s5s10s or 2s10s30s fly … Hold curve 2s10s curve flatteners in 1Q as the curve will likely bull flatten first before a Fed policy pivot leads to a bull steepening of the curve. Go long 5y TIPS….

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Bloomberg: When Bond Market Shifts From Optimism to Worry (Ed Harrison OpED with a single CHART which I hope you’ll find thought provoking)

… But in the past, the recession hasn’t actually materialized until we got the bull steepening we now see. And to be clear, the bull denotes Treasury market bull market gains as yields drop, while the steepening connotes a curve with shorter maturity yields dropping the fastest. That’s the sign the data have started to worry the bond market enough that many are predicting rate cuts in the near term, just as we see today. Since the Volcker onslaught, which was too aggressive for the bond market to fully react to before recession came, 10-year yields have always ended up higher than 2-year ones before the recession actually materialized. We are now less than 40 basis points away from that — a ways to go, to be sure, but maddeningly close given the economy’s resilience.

Bloomberg: Bill Gross’s Recession Bet Has Minted Millions From Bond Rally

Former ‘bond king’ nailed wager on short-dated rate futures

Securities have rallied as traders pile into rate-cut wagers

… Gross, via a spokesperson, confirmed he bought 3,000 three-month March 2025 contracts tied to the Secured Overnight Financing Rate. Based on Friday’s price, the wager, which is still active, has likely netted a more than $4 million profit, according to Bloomberg calculations.

Bloomberg: Surprise Call Shocks Staid Corner of Bond Market: Credit Weekly

Arch Capital called $1.7 billion of credit risk transfer bonds

The move comes as banks look to shift more risks to investors

Hedgopia: CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (shorts in 10s building once again…)

at RENMAC (Dutta moving to a rate cut coming and markets are pricing it and so he’s throwing those rocks in to the wettest paper bag…we’d call that financial bobblehead populism?)

Powell notes that it is premature to talk about a rate cut, but doing a rug pull would not be new for him.

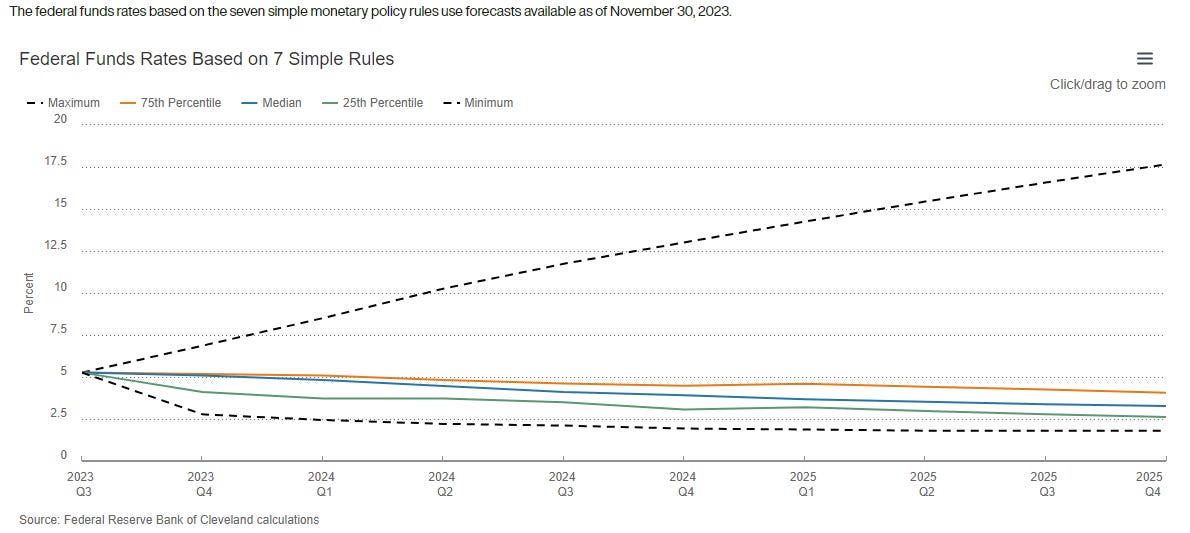

FRBCleveland: Fed funds rates based on 7 simple monetary policy rules 12.1.2023

As of November 30, 2023, the median federal funds rate across seven policy rules and three economic forecasts falls from 5.08 percent in 2023:Q4 to 3.28 percent in 2025:Q4.

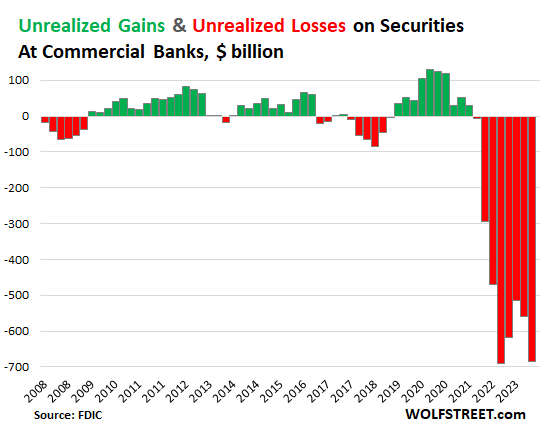

WolfST: “Unrealized Losses” on Securities Held by Banks Jump by 22% to $684 Billion in Q3, Oh Lordy

… These paper losses occur predictably when interest rates rise. As yields rose in Q3, the market prices of those bonds fell, and the unrealized losses stacked up. For example, the 10-year Treasury yield jumped from 3.81% at the beginning of Q3 to 4.59% at the end of Q3. In periods when yields fell and bond prices rose, banks had “unrealized gains” (green).

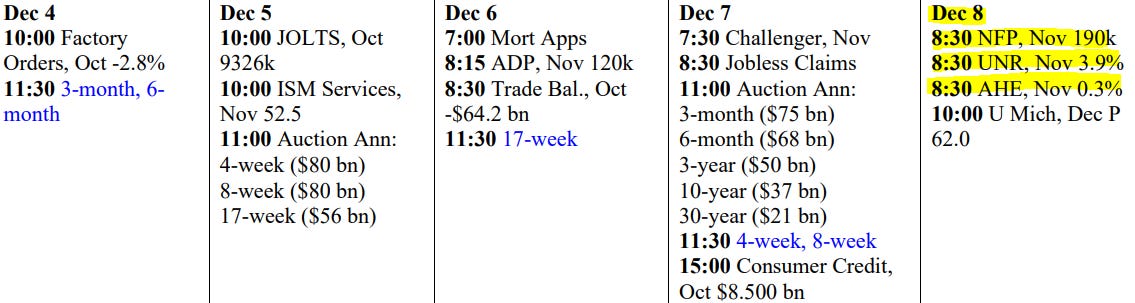

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Excellent Content !!!

"Ski Jump" Economy....incredible, if it happens, to see a 25T+ economy bounce around....

I'm probably looking for a more "dampened" next couple quarters...some of which could

be negative....but who's to say....

The two Bills have been right....so far.....wish I could trade like that....

The Rate Cut Bandwagon is filling up......

I can see a future headline: "Why does Fed Unch.....feel like a Rate Hike???"

"Steady as she goes" will now start to annoy the Hedge Funds.

Powell must maintain the Feds control as opposed to the large Market Participants

that want to usurp that control.

Thank you for all your work !!!!