(strong volumes)while WE slept; UST mkt illiquidity; less than 1/2 'manhattanites' back IN office; Americans drowin' in credit (i'm sure rate hikes gonna help...)

20-Year Bond Reopening Results: 1.5bp Short Stop, Second Smallest Dealer Takedown on Record …

… the 20-year has cheapened 44 bps since last month's auction, the last 5 or 6 of which came this morning, so it is hard to characterize these auction results as particularly strong (that being said, 20s have richened on the curve vs 10s and US contracts since the last auction, so take the outright move with a grain of salt). It isn't often that Treasury reopens a bond within a month of the original issue date, and it stops with a 93 dollar price.

… Dealers took down 8.1%, which is the second smallest takedown on record behind the 7.9% takedown in July 2022. Note, this is 8.1% of a $12 bln auction, so Dealers ended up with just $966.5 bln.

With the FOMC meeting coming up tomorrow, it is hard to put together a constructive case for 20s. There are clearly some wildcards at play in the market right now, with tensions increasing in Russia against the backdrop of the FOMC, but even if there is a big flight-to-quality, we doubt that 20-year bonds will be at the top of anyone's shopping list. The WI has traded poorly in the immediate aftermath of the auction, and we expect that this will continue.

With the FOMC coming tomorrow, it’s hard to put together a bullish / constructive case for, well, anything.

A brief respite better than NO respite at all? (Got20s?) … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher and most curves are modestly flatter ahead of the FOMC outcome and after Putin called up 300k in military reserves for Ukraine. DXY is higher (+0.35%) while front WTI futures are too (+2.4%). Asian stocks were lower, following NY yesterday, while EU and UK share markets are mixed and ES futures are up modestly (+0.2%) here at 6:45am. Our overnight US rates flows saw Asian real$ buying in the long-end during the Tokyo session, before the Russia headlines hit. We're publishing too early to get a bead on London flows and what investor activity was like after the ~2AM (NY time) russian headlines hit. Overnight Treasury volume was ~120% of average overall with relative high turnover seen in 7's (169%), 10's (144%) and 20's (228%) and very little in 3yrs (54%)…

… Our next attachment looks at Bloomberg's Treasury liquidity index where market illiquidity is grinding toward the poor levels seen at the start of the pandemic, by this measure. This is one of red flags cited by Bloomberg (top bullet link) that think could slow the pace of Fed rate increases. Right or wrong, the Tsy liquidity situation appears to be trending bad still with year-end/GSIB/QT reserve impacts, etc still ahead of us.

… and for some MORE of the news you can use » IGMs Press Picks for today (21 Sep) to help weed thru the noise (some of which can be found over here at Finviz).

We’ve reached that part of the programming where I’ll bring forward a couple / few things — sellside or widely available on the intertubes (ZH, etc) which, in my former institutional FI role, might have some funTERtainment value…

Less Than Half Of Manhattanites Are Back In The Office Despite 'Pandemic Being Over'

… Another metric, and perhaps the gold-standard measure of office-occupancy trends, is the card-swipe data provided by Kastle Systems. The NYC office occupancy rate is only 38% and has bounced between 30-40% for much of this year.

The slow return to the office where levels are barely over occupancy rates seen right before the start of the omicron wave last November comes as a slew of companies from Better.com to Ford to Peloton to Carvana to Zillow to Coinbase, among many others, have laid off workers because of the incoming Fed-induced economic downturn. A declining workforce will mean smaller corporate footprints…

Americans Drowning In Long-Term Credit Card Debt: Survey

… And so it comes as no surprise from Bloomberg that more US consumers are saddled with credit card debt for longer periods of time. According to a survey by CreditCards.com released on Monday, 60% of credit card debtors have been holding this type of debt for at least a year, up 50% from a year ago, while those holding debt for over two years is up 40%, from 32%, according to the online credit card marketplace.

This one hit YESTERDAY morning (so, before the selloff)

Global Macro Thoughts: Time for a short bounce While our quarterly outlook remains negative, and we do not expect central banks to ease up anytime soon, we think risk assets are due for a short-term tactical bounce coming out of the FOMC meeting.

Sooner or later, they (risk assets) will have been down long enough, they’ll look UP?

And speaking of looking UP, Goldilocks on yields which are said to be,

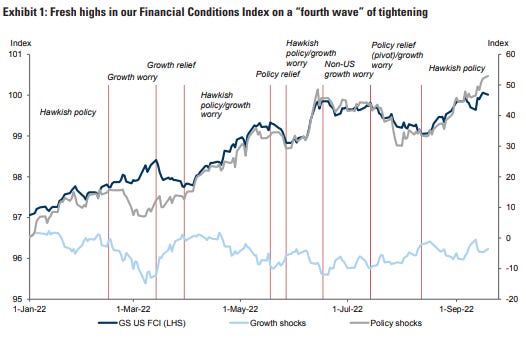

Back at the top of the FCI loop. If Chair Powell’s Jackson Hole speech dashed hopes of a Fed pivot to a slower pace of hikes, last week’s August CPI confirmed that the FOMC will struggle to credibly signal anything other than a 'stay the hawkish course' message. Our central market view has been that until the economy either enters a clear recession or shows sustained signs of progress on inflation, the pressure for tighter financial conditions is unlikely to abate and periods of relief are unlikely to be sustained. Those still look like the right conditions to wait for, and it is still the case that neither has yet been met. So we remain very much in the FCI loop.

It is true that a number of US inflation-related indicators (producer prices, import prices and inflation expectations have evolved in a more favourable direction. August’s CPI reading – like July’s - is only one data point and is only a “game-changer” when compared to hopes of more rapid progress towards lower inflation that the July print had fuelled. In many ways, the news is really that the macro “game” remains the same. With inflation still broad-based and in the high range that has dominated for the last few months, the market has again firmed up the near-term path, taking both 2022 and peak Fed funds rate pricing to fresh highs. Our US Financial Conditions Index had already reversed the entire 80bp of easing from the June/July peaks to the August lows in the wake of Jackson Hole and has now surpassed those peaks clearly again. Given that even under the best circumstances where the upcoming inflation news is more benign, the market will need at least a couple more months to be comfortable in any improvement in the inflation trajectory, those shifts make sense.

As shorter-dated real yields "reconnect" with longer-dated ones, policy moves likely to reverberate across the curve

Moving along to this mornings conclusion — ahead of the FED — this one from Paul Donovan of UBS asking,

The US Federal Reserve is expected to increase rates by 0.75%. The June policy errors trashed forward guidance and elevated the (unworthy) consumer price inflation measure as a policy objective. This has left markets skittish and inclined to overemphasize poor quality data.

The Fed’s challenge is the same as other central banks—to create disinflation where it has control to offset inflation, where it has no control. Much of current US inflation today is created by sectors that are less rate sensitive. The Fed also faces very unusual inflation divergence—between home owners and renters, high and low income groups, and across different geographies. Today’s hike has less power to lower inflation, but does raise risks to growth for specific groups…