Yields toying with breaking towards new YTD highs. Momentum oversold. This was MY interpretation of what to look for, here are some thoughts from a large German operation

Treasury will sell 3.375% of 8/42s $12bn 20yr bonds at 1pm today, $2bn less than the July reopening auction. The Fed will not buy any 20yr bonds as SOMA add-on at the upcoming auction.

Twenty-year bond yields have risen ~39bp since the last auction stop-out level and are currently trading at about 3.77%.

Direct bidders' participation increased to 18.3% in August from 14.1% in thew previous month but failed to make up for a weak indirect participation, which fell from its record high of 78.0% to 67.0%, and the end-user demand declined to 85.3%, the lowest level since February 2022.

The August auction tailed by 2.5bp and the bid-to-cover ratio weakened to 2.30 from 2.65 in the previous month.

Treasuries in 11yr+ maturities held by primary dealers as of September 7 was $44.3bn (36th percentile vs. last 3m history).

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have been led lower by the belly overnight as move highs in yields from mid-June are being threatened or taken out in longer duration benchmarks and in German bunds too. Sweden's Riksbank kicked off Hike Week with a bigger than expected hike of 100bp. DXY is little changed (+0.05%) while front WTI futures are close to UNCHD too. Asian stocks were all higher overnight while EU and UK share markets are all lower and ES futures are showing -0.5% here at 6:45am. Our overnight US rates flows saw a sleepy Asian session after a long weekend in Japan and the UK with no standout flow reported by our Tokyo colleagues. Overnight Treasury volume was still pretty decent at ~125% of average so there must have been some active turnover in London's AM hours- which we've missed a report on at press time.

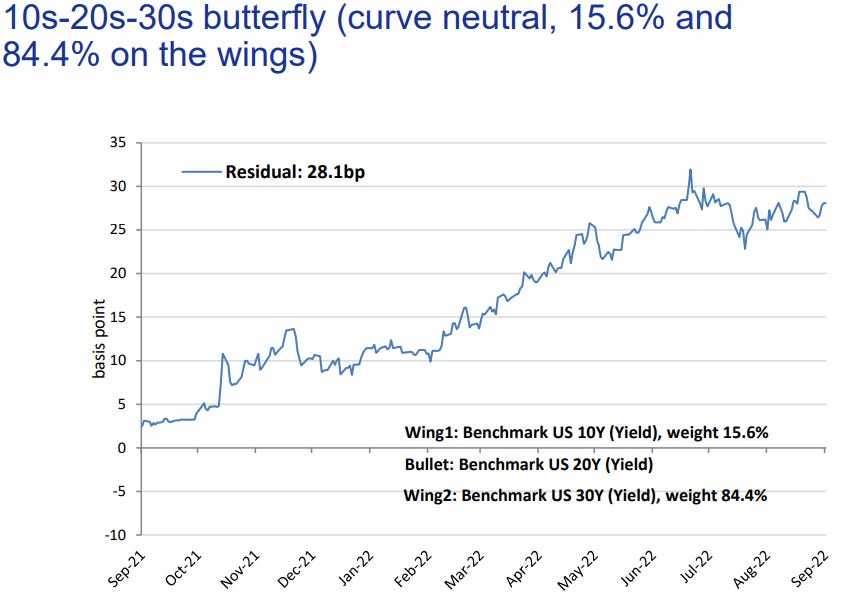

… The Tsy 10s20s30s 'fly hovers just above range support near 50bp so 20's going into this afternoon's auction looking slightly rich on curve. But as above, the halving in auction sizes since fall last year could/should sustain the richening trend in 20's on curve, in our view. Next stop 50bp in 10s20s30s after the supply clears?

… and for some MORE of the news you can use » IGMs Press Picks for today (20 Sep) to help weed thru the noise (some of which can be found over here at Finviz).

In my former life, this one from ZH (via BB) would have been something I could relate more directly to as yesterday was, ultimately, the calm before the storm

… On Tuesday we get the first of several monetary policy decisions in the developed markets with Sweden’s Riksbank’s review coming under scrutiny. The central bank is widely expected to raise rates by at least 75 basis points, which given how inflation and inflation expectations are evolving in the economy shouldn’t come as a surprise to anyone. In fact, considering that this will be the Riksbank’s penultimate review this year, it may not be a complete surprise if the monetary authority were to go jumbo and raise rates by a full percentage point, giving itself some head start over the European Central Bank.

A day later we get the Fed, and the markets are still torn between a 75-basis point increase and an even bigger move. That apart, it would be interesting to see how the members’ dot plot evolves, with current market pricing making the version we have from June pretty much moot. From near-zero interest rates just a couple of years ago, are we going to a 5% zip code as former Treasury Secretary Larry Summers reckons? …

… Phew, come Friday, we have the PMI numbers for September out of the euro area, but I am skeptical that a lackluster set of numbers will be a show-stopper for the ECB. And of course we have a mini budget from the UK’s new chancellor of the exchequer, and let’s see what magic rabbit Kwasi Kwarteng can pull out from his hat….

We’ve reached that part of the programming where I’ll bring forward a couple / few things — sellside or widely available on the intertubes (ZH, etc) which, in my former institutional FI role, might have some funTERtainment value.

ZH: "Who Wants To Hold Volatile Risk Assets When You Can Hold Cash?"

Hard to argue and I think ZH brought out that point yestwith note / visual from BBG re USTs yielding more than JUNK

Next up is THIS ONE from First Trust and Brian Wesbury asking,

… The Fed declares success when market rates move with its rates. But this is a test with a determined outcome. If the Fed grew five trillion bushels of corn, and corn was so plentiful that the price per bushel was essentially zero, then no private farm could sell corn for more. If the Fed then raised the price of its corn to $1/bushel, farmers could then sell theirs for 99 cents/bushel, but it’d be a completely manipulated market.

So, while raising interest rates may reduce economic growth and may throw the US into recession, there is no guarantee that this will fix inflation. Interest rates don’t determine inflation; the amount of money circulating in the economy determines inflation. And this is where the problem lies…

Thematically, Goldilocks has gotten the memo and seems to express a very similar sentiment … continued POSITIVE REAL INCOME GROWTH (so, money floating around the economy) creating more headache for the Fed (and heartache for restofus)

US Daily: More Money, More Problems for the Fed in 2023

… Real income growth has historically been the main driver of real spending growth, and we see several reasons—including positive real wage growth, continued job gains, cost of living adjustments to government transfer programs, and a normalization in the effective tax rate—why real income growth will likely be fairly strong through the end of next year. After incorporating these factors into our real income growth forecast, we expect roughly 3½% real income growth in 2023 on a Q4/Q4 basis, with positive real income growth for all income quintiles.

Strong real income growth suggests upside risk to real consumption growth in 2023, and raises the possibility that Fed will need to hike more than we are currently expecting to keep GDP growth below potential. This is one reason why we could imagine the hiking cycle extending into next year…

… Real spending growth is affected by a number of different factors—for example, our standard consumption model forecasts consumption growth based on real disposable personal income (DPI) growth, changes in financial and housing wealth, credit availability, and consumer sentiment—but is typically most sensitive to real income growth (Exhibit 1)

What this represents, then, is a means to an end. A defense OF higher terminal and nominal f’casts and along these lines, here’s what they suggest we DO with all this insight

… We think a peak in US 2-year rates will be a key signal for peak hawkishness and provide some relief across assets. Historically, 2-year yields have peaked at a higher level and beforethe Fed fund rate - in between a month and a month and half before - but we think we are not yet near such a turning point.

The road to peak hawkishness tends to be challenging for most assets: equities and 60/40 portfolios' performance tends to worsen 3-6 months before the end of the hiking cycle, and cyclical equities generally underperform vs. defensive. The US Dollar can remain strong until the peak in rates is reached.

We remain relatively defensive in our asset allocation for over the next 3 months (OW cash & N equities) and look for opportunities to add risk over the next 12 months. We continue to like collars on equities to take advantage of the very low skew and remain constructive on real assets for the new cycle. With TIPS yields approaching 1%, inflation-protected bonds will start to turn more attractive, in our view.

How LONG should one remain ‘defensive’ or asked another way, when will we know it’s time to become aggressive? What shall we watch? One thing to watch, potentially, noted HERE by a large German bank as they are,

… as we’ve previously pointed out, in over 70 years of data the Fed have never stopped hiking rates until Fed funds has moved ABOVE the rate of CPI inflation (Figure 2). More persistent inflation means that harsher rate hikes are going to be needed to bring real rates into restrictive territory.

Finally, in the WHO KNEW category, THIS SLIDESHOW from The Onion