June rate PEAKS coming (back) into focus as RESISTANCE as PBoC continues to CUT (RRR) and the Fed minutes put some wind in the sails of the S.S. Pivot (although slower pace of HIKES are still HIKES but who am I to offer common sense and logic).

Here are 30yy WEEKLY with some fibo retracement levels highlighted along with June (weekly)PEAK (~3.50%) … Note momentum (slow stochastics, bottom panel) are STILL SUPPORTIVE OF BONDS (ie lower rates, see TLT signals noted HERE)

It is that time of year where Global Wall Street is compelled to recalibrate it’s narrative generation machine and essentially hit RESET.

Putting aside the daily grind of views for a somewhat longer-term rocket-propelled dart throwing contest — 2023, the year ahead — HERE is what we think we think.

Perhaps not a good analogy but it is, unfortunately, all I got. There’s little accounting of ‘closest to the pin’ for 2022 and there will likely be even LESS accounting for 2023 BUT there will ALWAYS and forever be plenty of victory lapping as we enter / and next year.

I’ve left some up and added a few for your dining and dancing pleasure … feel free to pass this out at the table or in between games this weekend in lieu of talking politics.

THIS PDF combined with some leftover TurDUCKENwill most certainly have EVERYONE snoozin’ quickly!!

US consumers are indulging their hedonistic tendencies in the most important celebration of the economic year—Black Friday. However, real spending on durable goods fell in the third quarter across several major economies.

Over the course of this year people have switched from spending on goods to having fun, which involves spending on services. The share of spending allocated to durable goods has fallen as a result. Catastrophically negative real wage growth in the industrial economies has meant consumers have been using savings and credit to pay for food and fuel, not furniture and other fripperies. Some of the past surge in durable goods demand will have cannibalised current spending—the consumer who bought a washing machine in 2021 will not rush to buy another in 2022.

This slowdown in demand produced an astonishingly sharp reversal of durable goods price inflation. US durable goods price inflation has fallen from almost 19% y/y to below 5% y/y in just eight months.

Does this rapid disinflation of durable goods prices signal anything about other inflation drivers? Durable goods prices do demonstrate that inflation rates can reverse extremely quickly. However, today’s inflation is more about profit margin expansion than a transitory surge in demand. Different factors will reverse the 2022 inflation wave.

Other side of the DISINFLATION coin may be … and this depends on your positions,

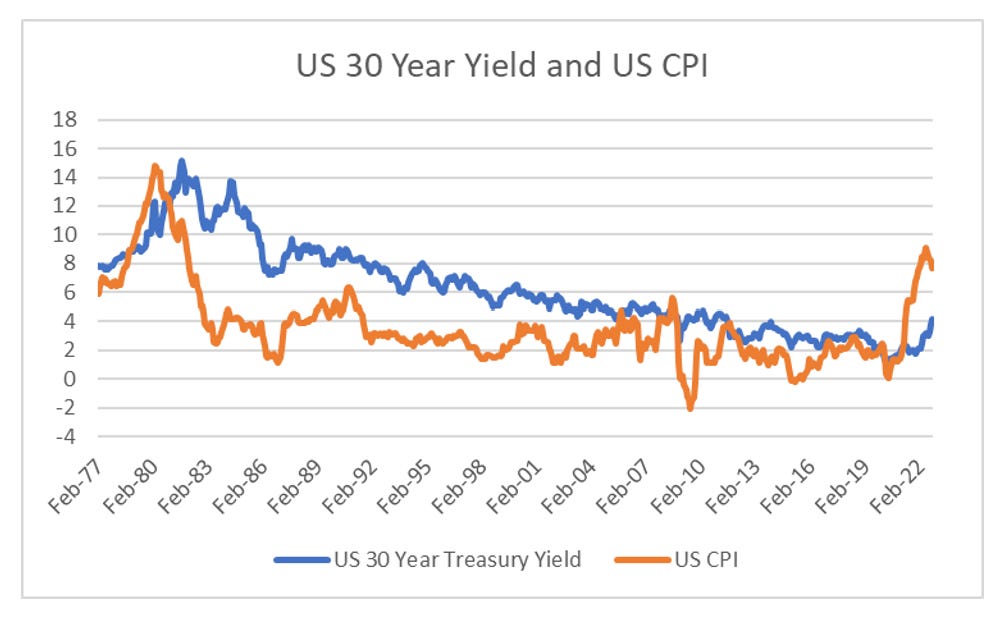

… US CPI is back at levels last seen in the 1970s, when the US 30-year treasury yielded north of 8%.

The reason that people are getting bullish bonds I believe is that the yield curve has inverted. And every time that has happened, you have a recession, and you want to get out of equities and into bonds.

Very oddly, Japanese long dated bond yields continue to trade poorly. For as long as I have been in markets, the JGB market has acted as a very good lead on US bond markets. Not only has it been prescient in leading the US bond yields lower from 1999 onwards, in 2020 the JGB market was also prescient in signalling the future US treasury sell off.

What does the JGB market see that the US doesn’t?

Read on for more of HIS view and in light of recent Japanese ‘flation news …

… Jeff Hirsch at The Stock Trader's Almanac has been writing about these trends for decades. (His father, Yale Hirsch, first discovered and wrote about the Santa Claus Rally in 1972.)

Hirsch has found that November to January is "the year's best consecutive three-month span." This year, this period also falls within what Hirsch dubs the "sweet spot" of the four-year presidential cycle — from the fourth quarter of the midterm year through the second quarter of the pre-election year.

Putting it all together, here are the stats for a long trade spanning from the Tuesday just prior to Thanksgiving through the second trading day of the new year, which encompasses the narrowly-defined Santa Claus Rally.

Since 1950, the S&P 500 has posted an average gain of 2.65% over this period, with a median increase of 2.40%. During the average winning period, the index is up 3.78% and down 2.01%, on average, when the market drops…

… Hirsch notes this is an unusual year given the the 15.5% drawdown seen for the S&P 500 so far this year. And while the major indices are unlikely to claw back the losses so far this year, the bullish seasonality still exists.

As Hirsch writes: "The fact that November 2022 is up so far is supportive for continued upside."

Game ON, then…? Checking in with ‘EARL to see what, if ANY messages might be heading our way — this via Chris Kimble,

This week brought a slew of interest-rate increases from jumbo to regular in size. The single biggest impact came from the Federal Reserve talking about its latest decision to boost borrowing costs — and how it may soon be time to slow down. Bond investors welcomed the news with open arms — Treasury 10-year yields are down more than 35 basis points in November to well below 3.7% in the steepest monthly rally since 2020.

As JPMorgan Chase & Co.’s Bob Michele put it — “bonds are back” as higher yields make them attractive on that basis for the first time in a decade.

Yet while the Fed is talking about slowing down, it hasn’t done so yet, meaning it’s not clear at what level yields will stabilize. Goldman Sachs Group Inc. is forecasting 10-year yields at 4% or higher through 2024 as the Fed faces a long inflation fight.

That fits with warnings from Kansas City Federal Reserve Bank President Esther George, who said ample US savings could mean higher interest rates are needed to cool spending.

Despite the risk that yields might keep rising, bonds were in vogue even as central banks across the globe delivered a range of tightening moves. South Africa and New Zealand each delivered three-quarter point moves, with the latter in particular sticking with strongly hawkish rhetoric. South Korea’s central bank on the other hand, fretting about signs of strain in its credit markets, hiked by just a quarter point and signaled a bias to stay gradual from here on in. Iceland was reading from the same page even as it raised borrowing costs to the highest since 2010…

… Recession Redux

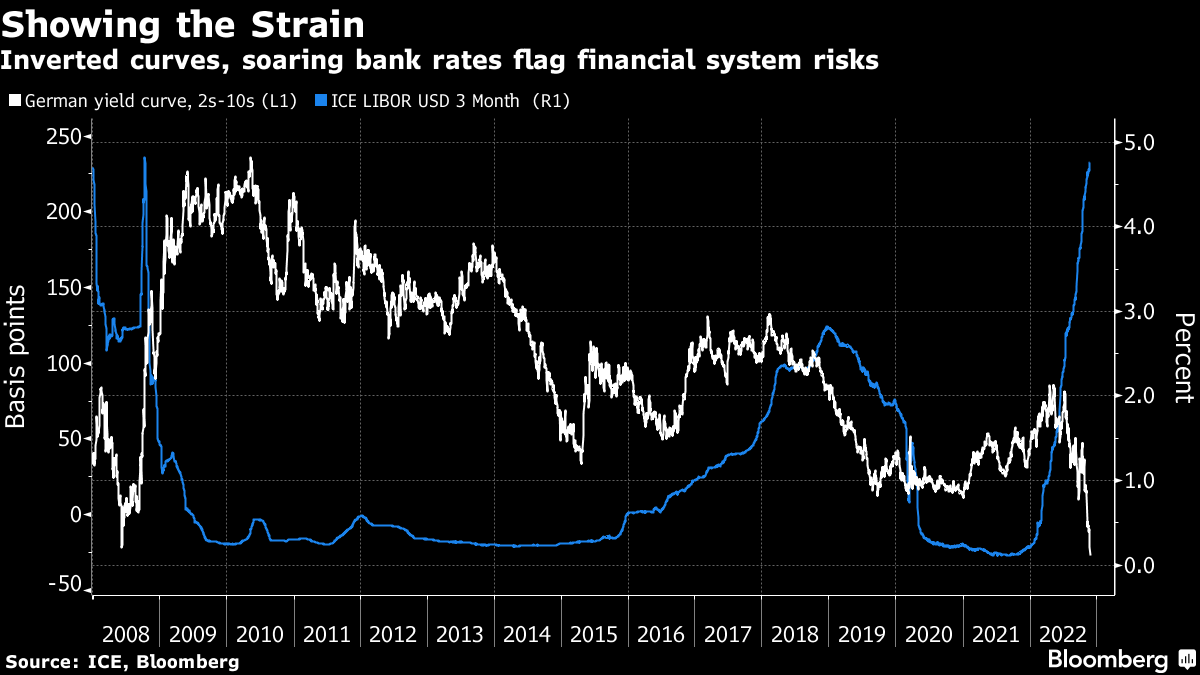

Why then are bonds traveling so well in the face of a mostly still rather hawkish barrage? Investors are growing more certain that any short-term pain from fresh central bank moves will only make for larger future gains because they expect economies to buckle under the strain. Germany’s yield curve inverted by the most in 30 years to join the growing chorus of growth warnings echoing across bond markets. Even the Fed’s own economists are estimating odds are nearly even of a US recession next year.

Little wonder then there’s a growing constituency betting on substantial declines in yields in the coming year or two — traders are piling into wagers on 10-year US yields tumbling to 2%.

There is something of a sting in the tail for bonds from all this pain, however. The Bundesbank warned financial stability in Germany, Europe’s largest economy, has taken a substantial turn for the worse this year. And the three-month London interbank offered rate for dollars climbed to the highest level since 2008…

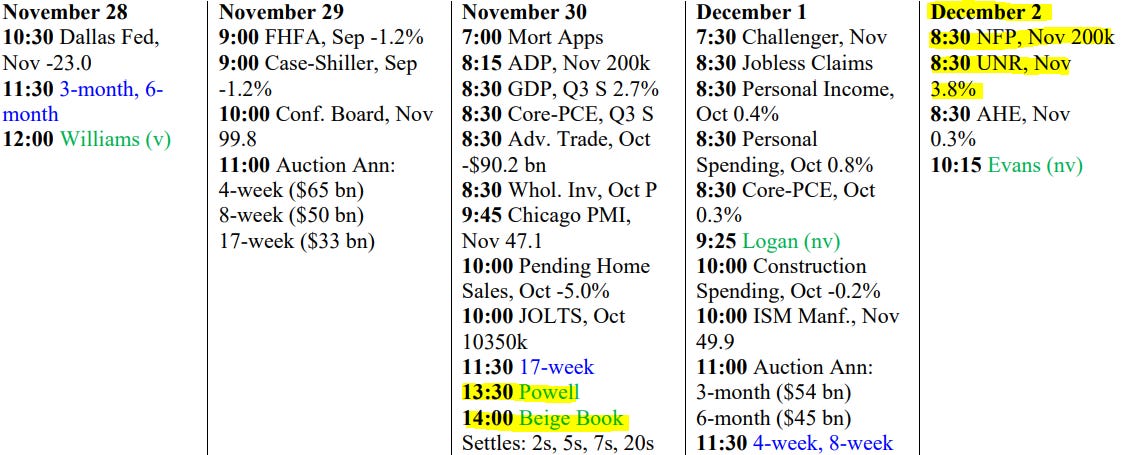

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,