(PBoC cuts RRR as Beijing battles COVID and USTs 'modestly' lower, belly weakest on about AVG volumes)while WE slept; pivot "SOON" -FOMC mins; "The Bullwhip Effect"; 10yy headed for BIG (monthly) fall

Good morning … the BOND and stock markets are going to close EARLY today in the USA and I’d be shocked if there is ANY noticeable volume. A couple things worth noting as we start today’s non-event … First, over in CHINA,

SCMP: China releasing US$70 billion to boost economy with cut to banks’ reserve ratio GS: PBOC delivers a 25bp RRR cut. Bottom Line: After Premier Li's comment on lowering RRR to support the real economy, PBOC followed up on Friday (Nov 25th) and announced a 25bp broad RRR cut (applicable to all financial institutions except those that already face a RRR of 5%, mainly small banks), effective December 5th. According to the statement following the announcement, PBOC described this cut as part of the policy package to support economic growth, aiming to maintain liquidity at reasonable levels and to keep broad credit growth largely in line with nominal GDP growth. DB: RRR cut signals PBOC's dovish stance is intact

Here’s a chart (from BBG via PBoC, h/t Chris Barraud — @C_Barraud)

And lest we forget, it would now appear the FOMC — based on THESE RECENT MEETING MINUTES — are putting paid to those who are thinking (trading, investing and positioning) OF A PIVOT. A reminder in case you were traveling Wed and MISSED THE MINUTES, specifically p9 into 10

Participants mentioned a number of considerations that would likely influence the pace of future increases in the target range for the federal funds rate. These considerations included the cumulative tightening of monetary policy to date, the lags between monetary policy actions and the behavior of economic activity and inflation, and economic and financial developments. A number of participants observed that, as monetary policy approached a stance that was sufficiently restrictive to achieve the Committee’s goals, it would become appropriate to slow the pace of increase in the target range for the federal funds rate. In addition, a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate. A slower pace in these circumstances would better allow the Committee to assess progress toward its goals of maximum employment and price stability. The uncertain lags and magnitudes associated with the effects of monetary policy actions on economic activity and inflation were among the reasons cited regarding why such an assessment was important. A few participants commented that slowing the pace of increase could reduce the risk of instability in the financial system. A few other participants noted that, before slowing the pace of policy rate increases, it could be advantageous to wait until the stance of policy was more clearly in restrictive territory and there were more concrete signs that inflation pressures were receding significantly.

It is with that in mind, here are a couple levels to keep in mind as central banks SLOW RATE OF INCREASES and as the Fed has yet to OFFICIALLY PIVOT (to cutting). June HIGHS in yield may be RESISTANCE. Look at 10yy vs approx 3.50% while keeping mind what looks to be bearish (daily) momentum …

… AND perhaps MORE importantly, the 2yy which may ALSO be defined by bearish (daily)momentum and kindly note the 50dMA (4.386%) which is acting as RESISTANCE,

I will have a look at WEEKLY charts before hitting send over weekend but for now, am thinking MORE about a PIVOT and IF front end does start to respond (break below 50dMA, work OFF it’s DAILY overBOUGHT conditions) there are likely to be several TRADE ideas — longs, steepeners — to discuss.

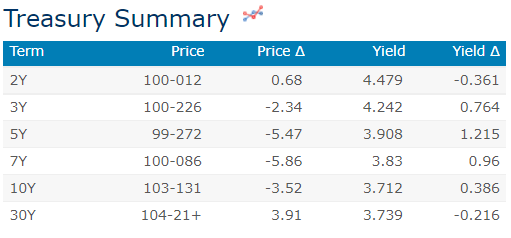

For now, though … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the belly under-performing this morning following a belly-led sell-of in german binds after a hawkish speech from Schnabel yesterday and better than expected German GDP and sentiment data today (see above). Tokyo's inflation just rose to a 4-decade high. DXY is little changed while front WTI futures are higher (+2.25%). Asian stocks were mixed/lower overnight, EU and UK share markets are modestly higher while ES futures are showing +0.13% here at 7:10am. Our overnight US rates flows were unavailable again with all eyes apparently on an exciting Wales-Iran World Cup game. Overnight Treasury volume was surprisingly decent overall (maybe ~ average) with the turnover appearing concentrated in the front end (2's at 128% and 3's at 139%) and in futures generally.

… Our first attachment shows that on Wednesday TLT's broke out above and closed through a bear trendline in place for nearly the past year. The breakout is kind of hard to see when showing the entirety of the bear move since late last year... so we've cut in a zoomed-in picture of the bullish breakout in the lower left. We view this trend break as yet another in an increasing series of feathers in the cap of the bond market since it's a pretty strong hint that the worst of the bond sell-off may be over, for now at least.

FOR NOW … we’ll see

… and for some MORE of the news you can use » IGMs Press Picks for today (25 NOV) to help weed thru the noise (some of which can be found over here at Finviz).

Moving right along in TO and through this holiday shortened week, here are a few things from the Global Wall Street narrative creation machine as well as random links from the intertubes

Bonds are bouncing off key levels of potential support.

For some, it’s a former low. And for others, it’s a downside extension level. Regardless, we can all rejoice that bonds have stopped falling.

That doesn’t mean we’re rushing out to buy treasuries. Instead, it signals a constructive start to a potential bottoming process for the bond market and relief from downside volatility.

Let’s check out the charts!

… ZROZ rebounds above its former 2014 lows, posting a potential failed breakdown. Risks are to the upside above 82 with potential resistance at the shelf of former lows ~100.

It’s a similar story for the T-Bond ETF $TLT:

T-bonds reclaimed their former 2014 lows yesterday. As long as TLT holds above 101.50, our tactical outlook is higher.

After trending downward since the summer of 2020, T-Bond prices have seen a small upturn here in November 2022. That price rise for T-Bonds had coattails, helping to boost the prices of investment grade corporate bonds. One effect of those corporate bonds moving higher is that the Advance-Decline (A-D) data for them has also seen a sharp upturn, which has resulted in a really high reading for the McClellan Oscillator in this week’s chart….

…Very high readings in this particular RAMO are associated with topping events for T-Bond prices. That may not mean they top on the exact same day, but the point is that these are markers of price exhaustion.

Why the bond market works differently from the stock market in this respect is an interesting question, but not an essential one. Different markets do have different personalities in how their price movements happen. Just ask any commodities trader. We do not have to know why those differences occur in order to acknowledge that they are real.

The point we should take from this chart is that the slight upturn in bond prices has exhausted itself, and we are more likely to see the downtrend in bond prices resume, rather than this being the start of a new price uptrend for bonds.

Thanks to today's release of the November 2nd FOMC meeting minutes, we know that the Fed has "pivoted" as expected; they are backing off of their aggressive tightening agenda. Instead of hiking rates another 75 bps at their December 14th meeting, we are likely to see only a 50 bps hike, to 4.5%, and that could well be the last hike of this tightening cycle—which would make it the shortest tightening cycle on record (less than one year). And they might not even raise rates at all in December—that would be my preference.

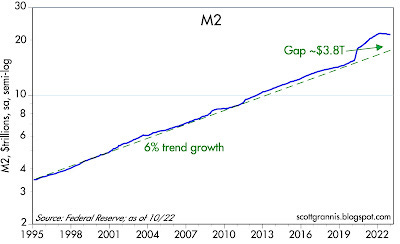

For more than two years I have been one of a handful of economists keeping an eye on the rapid growth of the M2 money supply. Initially I warned that it portended much higher inflation than the market was expecting. But since May of this year I have argued that inflation pressures have peaked: "Many factors have contributed to this: growth in the M2 money supply has been essentially zero since late last year; the stimulus checks have ceased; the dollar has been very strong; commodity prices have been very weak; and soaring interest rates have brought the housing market to its knees. All of these developments mean that the supply of money and the demand to hold it have come back to some semblance of balance." To sum it up, I think the Fed has gotten policy back on track, so there's no need to do more. In fact, the October M2 release showed even more of a slowdown than previously, thus underscoring the need to avoid further tightening.

… THAT is all for now. Off to the day job…

… I'm still firmly in the inflation-is-falling camp, and it's because of the unprecedented decline in the M2 money supply, coupled with forceful actions on the part of the Fed to bolster money demand with sharply higher interest rates. As a result, I believe we are going to see a gradual decline in inflation over the next year or so.

The following charts round out the story: Chart #1

Chart #1 has got to be the most significant monetary development that almost no one is paying attention to. It shows how M2 surged above its long-term trend growth rate beginning in April 2020, and then stopped growing about one year ago. It is still quite elevated (i.e., there is a lot of "excess" money sloshing around), but the growth rate of M2 is now negative: over the past six months M2 is down at an annualized rate of -2%, and over the past 3 months it is down at a -4% annualized rate. This adds up to the weakest growth of M2 since at least 1960—and possibly the weakest growth ever. M2 today is about 22% above its long-term trend, whereas it was almost 30% above trend earlier this year. The amount of "excess" money is declining rapidly, and that is a good thing…

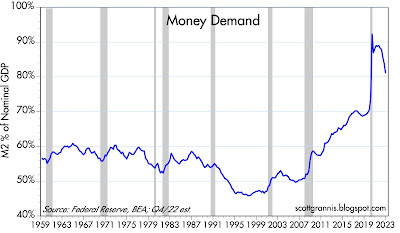

Chart #3

Chart #3 tracks the demand for money as defined by the ratio of M2 to nominal GDP. Let me explain: M2 is a proxy for the amount of money the average person holds in currency and bank deposits. Nominal GDP is a proxy for average annual incomes. The ratio of the two therefore tells us what percent of one's annual salary is held in the form of readily-spendable money. When the ratio is higher than people feel comfortable with (i.e., when there is no longer a need to stockpile funds for a rainy day), people attempt to spend down their money balances, and that fuels a surge in demand. Money balances decline, and nominal GDP surges. I estimate that the ratio of M2 to GDP will fall to almost 80% by the end of this year, down from just over 90% at its peak in Q2/20. Today there is simply no need for people to hold so much of their income in the form of cash. Indeed, I don't see why this ratio can't fall back to 70%, where it was before the pandemic hit. For that to happen, nominal GDP (mostly inflation) is almost certainly going to continue to grow, albeit at a slower pace, and M2 balances are likely to decline some more.

(Note: for those who prefer to think in terms of the velocity of money, just invert Chart #3. Velocity is simply the inverse of money demand, and vice versa. Today velocity is definitely picking up. For a longer explanation of this see this post.)..

Moving right along and from the intertubes back TO Global Wall Street for a moment

The US Black Friday celebrations begin. US consumers have just spent the past 18 months indulging in hedonistic excess by buying enormous amounts of durable goods. This may slow demand now. If you bought a washing machine in 2021, you do not rush to buy a new washing machine in 2022— these things are not iPhones…

(personal note — MOST of my home team will be WORKING — Thing 1s picked up hours at Under Armor and Thing 2 will be at Target — which leaves the Missus and Thing 3 unaccounted for — this could be an issue! :) )

One (maybe the only one) concept I remember from the logistics class I took at business school 20 years ago is the bullwhip effect. It essentially means that small disturbances in supply chains can lead to severe supply shortages and due to overordering these shortages are often followed by excessive inventories. Many indicators suggest that we have entered the last stage of the bullwhip cycle which coincides with weakening consumer demand. This has good as well as bad implications for markets.

The inventory-to-sales ratio for STOXX Europe 600 companies is at an all-time high and many supply chain issues have normalized. For example, container freight rates have come down 75% from their peak. With increased supply and lower demand, some industries will be facing shrinking pricing power. In aggregate, we expect profit margins in Europe to decline and to drive down earnings by at least 10% in Europe for 2023. On the bright side, we might see prices for goods come down quicker than expected. This week, the producer price index for Germany showed a first crack in European inflation data and decreased by an astonishing 4.2% in October (vs +0.6% exp.). PPIs for most other EU countries will be published in early December and typically point in the same direction. This could alleviate fears of rising rates and further drive the positive market momentum.

Moreover, the strong growth in European natural gas inventories over the past weeks has significantly reduced the tail risk of forced production curtailments. In combination with substantial government support programs for companies and consumers, the negative impact of the European energy crisis could be less severe than previously thought. We turn more optimistic short term and will revise our equity index targets in our 2023 outlook.

Average Inventory-to-Sales Ratio for STOXX 600 Companies

Good AND BAD implications and BOTH are going to be considered by global policy makers (monetary more than fiscal) as we put 2022 in the rear view mirror.

… The single biggest impact came from the Federal Reserve talking about its latest decision to boost borrowing costs — and how it may soon be time to slow down. Bond investors welcomed the news with open arms — Treasury 10-year yields are down more than 35 basis points in November to well below 3.7% in the steepest monthly rally since 2020.

As JPMorgan Chase & Co.’s Bob Michele put it — “bonds are back” as higher yields make them attractive on that basis for the first time in a decade.

Yet while the Fed is talking about slowing down, it hasn’t done so yet, meaning it’s not clear at what level yields will stabilize. Goldman Sachs Group Inc. is forecasting 10-year yields at 4% or higher through 2024 as the Fed faces a long inflation fight.

That fits with warnings from Kansas City Federal Reserve Bank President Esther George, who said ample US savings could mean higher interest rates are needed to cool spending.