sellside observations for the week ahead (03/13th); SVB is / is NOT 2008 (please choose); it is / is NOT different this time (please choose); 2yy (and THE bible) weigh in

Good morning/noon/night (please choose one depending upon where you reside and whenever it is you maybe stumbling across this and THEN add one hour and, well you get it…).

I’ll apologize upfront as

I’m not a bank analyst and I’m NOT a HTM or AFS or deposit ratio expert.

I’ll refrain from offering, ‘but its different this time’ — NOT 2008 … or suggesting that we’re doomed to repeat history as we’ve not yet learned anything.

I’ll leave all this TO the smart folks — bank analysts I know reading as well as institutions and individuals whom I’ve great deal of respect for.

Folks, I’m just an old bond dawg who had (mis / good)fortune of having front row seat in the bond market dating back TO Orange Cty crisis. And it wasn’t an issue until it became one REAL QUICK then, as now.

That said, a couple things before I jump TO global wall street … Jim Bianco on Friday afternoon as fallout from SVB was still, well, falling out and frankly is still becoming known …

With bond yields (and interest rates) rising sharply, it’s understandable that most of the world is hoping for lower rates.

Lower interest rates allow for more flexible lending to both businesses and consumers… BUT…

As the “weekly” chart (below) shows, the last time 2-Year bond yields were this high and interest rates turned lower, it was the start of challenges for stocks (i.e. The Financial Crisis).

And currently, 2-Year treasury bond yields are testing that very same level! And the 150-week change is up 2,127% Yikes!

Will they turn lower here? Will it be different this time? Stay tuned!

…The Biggest Picture: 1 year ago Fed funds was 0%...since then 290 global rate hikes (425 past 2 years)…not a prelude to “Goldilocks”, prelude to hard landing & credit events (Chart 2); bad “crashy vibes of March” set to worsen absent a soft Feb payroll number.

AND … we’re just waiting for that day when they etch in a red circle … perhaps we’ve witnessed the day — lived / traded / invested through it and NOW the worst of it is to be viewed in rear-view mirror. HOPE, they say, does SPRING eternal!

Finally in effort to help in YOUR own process of determining whether or not this is / isn’t 2008 all over again, a few things / links from the interweb to browse ahead of Sunday evenings futures market opening.

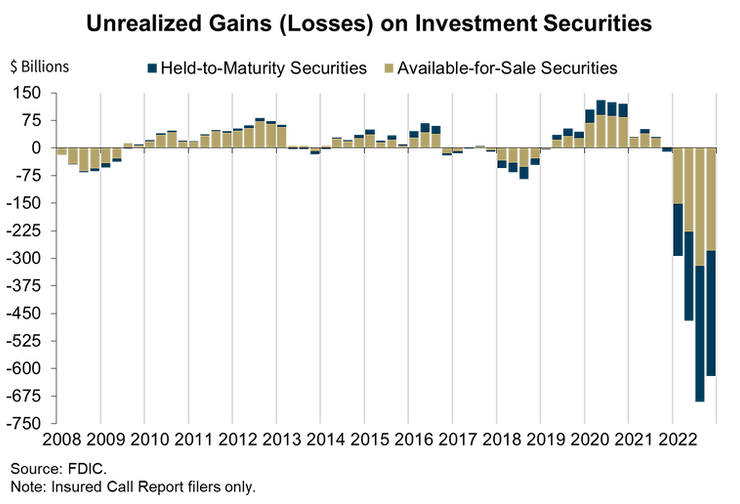

I’ll start with Chris Whalen IRA blog post as he’s got a very popular visual (found in MIKE CEMBALEST note, too so it MUST be important) from the FDIC … HTM and AFS, where he attempts to help us figure out,

… When the Fed began to tighten policy and end asset purchases in 2021, much of the COVID era debt was quickly left underwater. As we noted in an earlier post (“QT & Powell's Liquidity Trap”), as the Fed pushed up short-term interest rates, the effective duration of the Fed’s $3 trillion in agency and government MBS ballooned to over $10 trillion today, which a commensurate reduction in price. The MBS owned by SIVB and other banks went from a three-year average life to in excess of 15 years today. The change in duration of MBS is responsible for the huge unrealized losses on the books of US banks.

By the time that SIVB collapsed in March of 2023, the FOMC had moved short-term interest rates nearly six percent. Any first year associate at a bank knows that if you issue a security at 3% and then the Fed raises interest rates by 500bp, the value of that security is going to fall by about 20 points from its original value. SIVB had half its balance sheet in “low-risk” government and mortgage backed securities (MBS), but the market risk overwhelmed the bank and caused a deposit run. Now you know why the short-sellers focused on SIVB.

As Q1 2023 comes to a close, the US banking industry is on a knife’s edge…

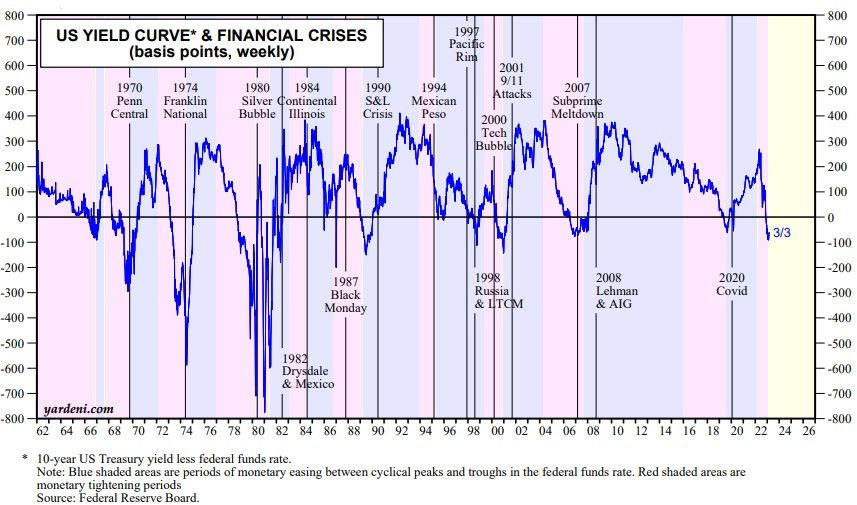

This seems as good a time as any to offer a visual of the YIELD CURVE AND FINANCIAL CRISIS from Dr. Ed BOND VIGILANTE Yardeni — which was offered out to inboxes Friday MORNING before FDIC seized SVB and Ed details briefly,

… As it has done often in the past, the inverted yield curve has been signaling since last summer that something could break in the financial system if the Fed continues to tighten monetary policy (chart).

The meltdown in SVB may be the beginning of a credit crunch for tech startups since the bank has been a major lender in that space. However, we doubt that it is the canary in the coal mine for the overall credit system…

Right. Okie dokie. THE BEGINNING. Back TO some further graphical insights,

Tooze: Chartbook #200 Something Broke! The Silicon Valley Bank Failure - How tech hubris and low interest rates combined …

… So SVB was a big accident waiting to happen. What pushed it over the edge?

Did SVB make speculative loans? Yes, some. But not enough by itself to blow it up. Did it engage in adventurous financial engineering? No! A large part of its depositors’ money was invested in what is supposed to be the safest part of the financial system, Treasuries and government-backed bonds like agency-backed Mortgage Backed Securities.

A portfolio of government backed bonds will be something you can sell. The question is what price do you sell it at and will you suffer a loss?

That saying — there’s no such thing as a bad bond, just a bad price…Tooze includes tidbit for those thinking there maybe something to the idea of where there’s smoke there just may be a fire,

… For years big US banks have been piling excess cash into bonds. Following the pandemic there was a 44 per cent surge in their bond holdings, to $5.5 trillion.

In 2022 the Fed began a tightening cycle and those bonds took a serious beating, inflicting HUGE paper losses on the bank holdings.

Unrealized Losses on Securities Increased: Unrealized losses on securities totaled $689.9 billion in the third quarter, up from $469.7 billion in the second quarter. Unrealized losses on held-to-maturity securities totaled $368.5 billion in the third quarter, up from $241.8 billion in the second quarter. Unrealized losses on available-for-sale securities totaled $321.5 billion in the third quarter, up from $227.9 billion in the second quarter.

The distinction between HTM and AFS is all-important because as FT’s Lex explains

Banks can classify their security holdings as “held-to-maturity” (HTM) or “available-for-sale” (AFS). Those that are labelled HTM cannot be sold. But that means any changes in market value will not count in the formulas regulators use for calculating capital requirements. By contrast, any losses in the AFS basket have to be marked to market and deducted from the bank’s capital base.

The upshot. Even allowing for accounting help, there is a huge paper loss sitting on the balance sheet of America’s banks. Were there to be a liquidity squeeze, then a large part of the banks’ portfolios - the HTM part - could not easily be sold.

Lex finishes the year by warning …

Moving along and perhaps equally important as knowing WHO to trust as you attempt to make it through the weekend separating fear mongers from those with facts, it might be good to know at least what ARE the ‘right’ questions to ask.

… The value of loans taken when rates were low have plunged, and depositors are expecting higher rates. Financial institutions and firms which borrowed from them amid two decades at lower-than-normal rates are already experiencing the effects of simple normalization. The combination of the SVB development on top of yesterday’s disclosure by Silvergate Capital Corp that it would cease operation amid the wreckage of the cryptocurrency industry, couldn’t come at a much worse time. Estimates for the Fed’s terminal policy rate are creeping toward 6 percent amid persistent inflation in services and too-strong-for-comfort employment data. If history and market-implied policy rates are any guide, it won’t take much more pain in the financial sector for the Fed to begin easing rates again.

We won’t know for another twelve or fourteen months whether Silicon Valley Bank (or any of the other banks being thrown overboard today) were the ones borrowing at the Fed’s discount window. But it is increasingly likely that whatever firm(s) it was, exigency was the driver.

Another question I’m thinking about and not sure if relevant or a ‘good’ question but … Would Fed open Discount Window for banks in trouble with regards to ‘stablecoins’?

ZeroHedge: USDC 'Stablecoin' Breaks Peg As Circle Admits Billions Stuck With SVB

… Yesterday afternoon, after the equity market close, USD Coin (USDC) issuer Circle revealed that $3.3 billion of its $40 billion reserves were tied up in now-failed Silicon Valley Bank (SVB).

Another QUESTION asked by Rajan via OpEd in FT (again via ZH)

… The temptation then is for the Fed to be more ambiguous, keep a soft landing on the menu and pray for an immaculate disinflation.

If so, the Cecchetti study warns that the eventual unemployment needed to rein in inflation could be much higher.

The Fed’s only realistic options may be a hard landing and a harder landing. It may be time for it to choose.

So many questions so little time. I’ll continue thinking UP questions and trying to connect some dots (for myself) and cannot help but think about situation - WSJ,

… The bank is the 16th largest in the U.S., with some $209 billion in assets as of Dec. 31, according to the Federal Reserve. It is by far the biggest bank to fail since the near collapse of the financial system in 2008, second only to the crisis-era collapse of Washington Mutual Inc….

Not in terms of 2008 or NOT but how it’s likely never different this time.

The bank (debate if you wish (it’s NO Jimmy Stewart bank to be sure) funding the smartest in the room — the sharpest tools in the shed — you know, PE guys.

The very same who continue to sell us the idea of an alternate reality (have you purchased any lakefront retirement home in the METAVERSE? me either and certainly not thinkin’ bout it when so called STABLEcoin is anything BUT stable).

It’s never different this time means all sorts of different things to different folks. To each your own!

I’m going to move on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Treasure trove of pertinent links once again. Subscribe to Tooze so I'll get to that one soon. I was enjoying the AIER link till it ended like a JPOW pressor. There is going to be a political limit among the Public for how much longer these rates of inflation will be tolerated. After the GFC there wasn't much sympathy for the Banks among the Public and it didn't take long for a fair number of the Pols to get in line. Whether it is fair to the Regionals or not, doubt this time will be different on that score. He can't have it both ways. Suggesting 6% rates, but then saying rates will get cut because some regional banks feel the strain is getting annoying to read/hear. This notion America is so fastidious about the 'pain' banks are feeling just doesn't square with the Financial and Banking Crises and subsequent carnage I've witnessed repeatedly at this point. Remember the carnage among Banks in Texas, or Arizona, or New Mexico, or California, or pick the state or region of your choice? Most anyone will probably ask, if they probe their memories about it a minute, which among the episodes of Banking carnage in Texas would Mr Wriggles be referring to as there are so many? This link covers a little more than a decade in a long history of banking carnage just in the SW: https://www.fdic.gov/bank/historical/history/291_336.pdf It would be nothing short of miraculous if SIVB is the only casualty after inflation hit ~10%. As you point out this isn't anything you haven't witnessed, so my apologies, I'm just venting.

Treasure trove of pertinent links once again. Subscribe to Tooze so I'll get to that one soon. I was enjoying the AIER link till it ended like a JPOW pressor. There is going to be a political limit among the Public for how much longer these rates of inflation will be tolerated. After the GFC there wasn't much sympathy for the Banks among the Public and it didn't take long for a fair number of the Pols to get in line. Whether it is fair to the Regionals or not, doubt this time will be different on that score. He can't have it both ways. Suggesting 6% rates, but then saying rates will get cut because some regional banks feel the strain is getting annoying to read/hear. This notion America is so fastidious about the 'pain' banks are feeling just doesn't square with the Financial and Banking Crises and subsequent carnage I've witnessed repeatedly at this point. Remember the carnage among Banks in Texas, or Arizona, or New Mexico, or California, or pick the state or region of your choice? Most anyone will probably ask, if they probe their memories about it a minute, which among the episodes of Banking carnage in Texas would Mr Wriggles be referring to as there are so many? This link covers a little more than a decade in a long history of banking carnage just in the SW: https://www.fdic.gov/bank/historical/history/291_336.pdf It would be nothing short of miraculous if SIVB is the only casualty after inflation hit ~10%. As you point out this isn't anything you haven't witnessed, so my apologies, I'm just venting.