(Good) morning. Stocks DROP, Ruble TANKS as Russia closed stock mkt and on a positive note (for Putin, nOPEC+), OIL SOARS … Going straight to a live look at Putin,

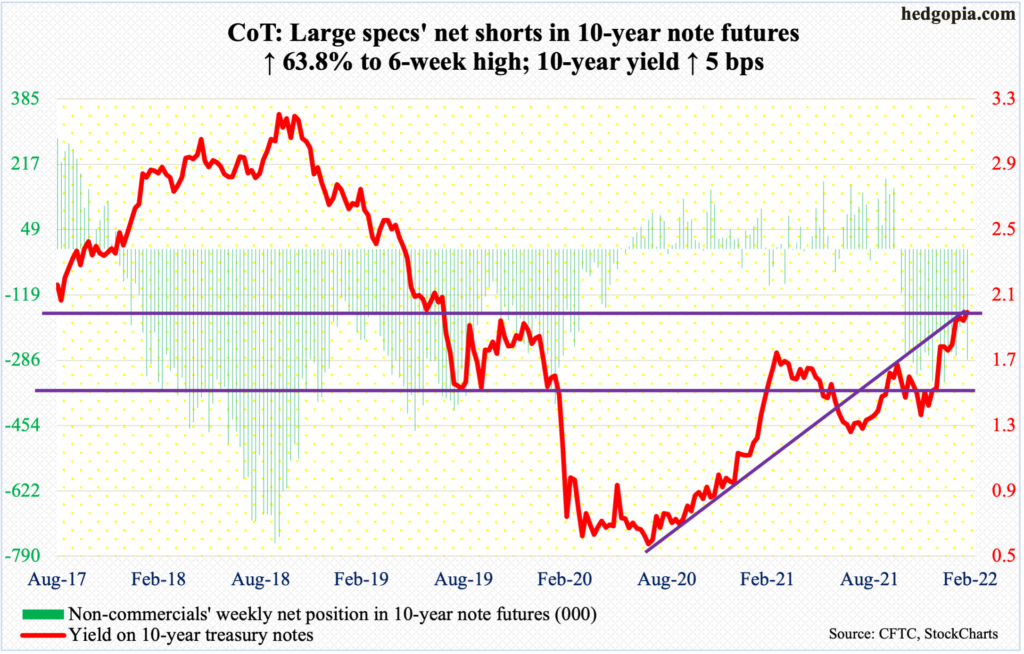

Treasuries are higher and the curve flatter as risk-off conditions dominate after the weekend Ukraine-Russia developments (see above). DXY is higher (+0.35%) while front WTI futures are too (+4.75%). Asian stocks were actually slightly higher on balance, EU and UK share markets are deep in the red though (SX5E -3.1%, SX7E - 7.1%) while ES futures are showing -1.4% here at 7am. Our overnight US rates flows actually saw real$ followed by fast$ selling during Asian hours as Treasury prices snapped higher to start the week. The desk noted a dearth of Treasury buyers this morning into the push higher. The desk also reported rising funding concerns as FRA-OIS widened notably along with cross-currency swap levels. Overnight Treasury volume was about 115% overall with relatively elevated turnover seen in 2yrs (156%)…

… Treasury 2s5s10s 'fly, weekly: Last week's confirmed breakdown below a year-long up-channel has us thinking that the medium-term prospects for belly outperformance have improved dramatically in recent days...

CNBC on USTs: Treasury yields slide as fresh sanctions are imposed on Russia

AND on STONKS: Dow futures fall 400 points as sanctions slam Russia and leaders meet for talks

… and for some MORE of the news you can use » IGMs Press Picks for today (28 FEB) to help weed thru the noise (some of which can be found over here at Finviz).

Moving along to a few more select items from Global Wall Street cognescenti who are never short of insight, offering some updated views as war drums beat.

Sanctions against Russia impact the global economy through three main transmission mechanisms. The risk premium on commodity prices slows the decline in inflation, unless countered by other producers. Sanctions directly disrupt trade. If Russia is plunged into economic recession (or worse), demand for imports falls. However, at 2% to 3% of global GDP, Russia is not a very large part of the global economy. Generally, risk aversion may encourage liquidity demand; the path of quantitative policy tightening is less certain…

ZH in case you missed latest Sunday evening 1stBOS Pozsar (aka the shock jock)

Finally, in the knowns and unknowns category is the latest Sunday Start by MSs stock jockey in chief, posting this graphic to help us all through the crisis (HERE for ZHs version)

Investing capital can be an exhilarating and humiliating experience. Anyone who has chosen this as a career has experienced both, sometimes in the same week, like the one just past. While the investment landscape is always filled with uncertainties, today’s backdrop seems dotted with more than normal. When faced with such an environment, it’s often helpful to lay out the big factors affecting asset prices and then try to determine what you think you know or can analyze, and what remains hard to determine so it can be properly handicapped – i.e., priced.

For this exercise one can use the Johari window, a tool originally developed by psychologists to help people better understand how they are perceived by others relative to how they perceive themselves. If done openly, it can facilitate better interactions, and communication in particular becomes more effective. This tool was later used by military strategists and became famous after former US Secretary of Defense Donald Rumsfeld’s famous speech about known unknowns…

Finally, the Russian invasion of Ukraine fits into the unknown unknown box, along with most geopolitics. While there are many people who know quite a bit about such matters, geopolitics are very difficult to analyze and therefore very difficult to price. Instead, this invasion simply adds another risk to the mix that’s unlikely to disappear quickly. In a world where valuations remain elevated and earnings risk is rising, last week’s tactical rally in equities will likely run out of momentum in March as the Fed begins to tighten in earnest and the earnings picture deteriorates.

Knowns and unknowns framework can be useful tool for investing

Under a framework of knowns and unknowns, the world is a confusing place right now with the Russian invasion taking center stage. Our attention remains focused on what we can analyze, especially earnings growth, as we try to identify companies that can deliver at a reasonable price.

… In last week's note, we presented a price analog comparing the S&P 500 today to what happened in 2018 as a guide for trading the near-term set-up. We suggested that the Russia/Ukraine conflict might provide a perfect reason for the S&P 500 to re-test its January lows, a re-test that investors should buy or at least cover up shorts. Indeed, Russia's full invasion on Wednesday night led to a very sharp sell-off on Thursday and led to the "textbook" re-test we were looking for. The positive divergence on lower volume provided the opportunity to cover shorts and even get long some of the most beaten up areas of the market for those nimble enough to do it (Exhibit 3).

While this technical set-up was/is bullish in the very near term, it does not look good for the intermediate term with all of the major averages below their respective 200-day moving averages and the 50-day moving average negatively sloped. The S&P 500 looks the strongest but it's severely damaged and it will take time to repair before it can make a real swing at new highs. This weak technical picture in the primary index now mirrors the technical damage that's been building for months under the surface. Most importantly, it reflects the challenging fundamental backdrop of tightening financial conditions colliding with slowing growth—the core message in our outlook for 2022 in mid November.

Going back to the price analog we showed last week, we have updated it to show that we're still very much on track for what looks like an extremely challenging March/April after this short-term rally exhausts itself (Exhibit 4). We think equity markets could rally / hold up for another week or two but we would be very careful if the S&P 500 approaches 4500 again. Bottom line, let the market work off its still oversold condition but use further strength to reduce risk in profitless growth stocks, low-quality cyclicals and stocks that are likely to be vulnerable to payback in demand from last year's binge and escalating costs that can no longer be passed along so easily. Conversely, and in line with our Year of the Stock Picker Outlook title, we are on the lookout for idiosyncratic stories centered on companies with superior operating efficiency—we analyze and discuss this later in this note.

And now you know.

One thing I know for sure is that I do NOT envy JPOW when he speaks this week in DC and I’d suspect it to go something like this,

{kind=link}

{kind=link}