Good morning and welcome to the beginning of the end of the week. A few things to consider as the week comes to a close AFTER digesting this mornings set of data (including ECI, PCE and UoMISSagain confidence all noted HERE as well as earnings and the FOMC). As far as TODAY IS CONCERNED, from sellside,

… US News: In US stocks, Energy is winning at the expense of every other sector (see chart) WSJ 'Window stickers' for mobile internet pricing is on the way says the FCC WSJ "It's all out of whack:" Snack inflation to persist according to a food giant WSJ The latest from JD Power on the near-term prospects for auto sales and pricing ("February will likely be another month of suppressed sales volume offset by near record level pricing and profitability") JD Power Name and shame? Just about every NYC employer will soon (May 15th) have to disclose pay secrets WSJ

Treasuries are lower and the curve steeper out to 20yrs this morning ahead of this morning's key US inflation prints and after UK 2yrs (see attachments) printed 1.00% for the first time in over a decade. DXY is modestly higher (+0.13%) while front WTI are too (+0.75%) a day after a wild expiration in NG1 which saw a ~73% up-spike at one point yesterday. Asian stocks were mixed, EU and UK share markets are all in the red (SX5E -2.1%, FTSE 100 -1.2%) while ES futures are showing -0.3% here at 7am. Our overnight US rates flows saw 'peaceful' trading with my Asian colleagues noting on-balance buying (fast$ in front end, real$ in long-end) amid light turnover. Overnight Treasury volume was ~80% of average all across the curve save for the newly-minted 7y note (113%).

… 2s5s30s Tsy 'fly, monthly: A close at spot levels on Monday would mark the highest monthly close (cheapest belly) in roughly two decades according the BBG data.

… What a week we’ve had. Yesterday saw another market whipsaw as markets continued to try to digest the aftermath of Chair Powell’s press conference. In particular, there was growing speculation that the Fed would embark on back-to-back hikes in order to get inflation under control, with Fed funds futures now pricing 2 full hikes over the next two meetings in March and May, in line with our US econ team’s updated call. Assuming this is realised, then this would be a much faster pace of hikes than anything seen over the last cycle, when the initial hike in December 2015 wasn’t followed by another for an entire year, and the fastest things got was a consistent quarterly pace when the Fed hiked 4 times in 2018. This time, we almost have 4 hikes priced between March and September alone. Of course however, it’s worth noting that today they face a very different set of circumstances, since the last hiking cycle actually began with inflation beneath the Fed’s target, and was a pre-emptive one given their belief that inflation would rise from that point. By contrast, this cycle of rate hikes is set to begin with inflation at levels not seen since the early 1980s, with the Fed seeking to regain credibility after consistently underestimating inflation over the last year. As we’ve highlighted in our work over the last 6-9 months this is a very, very, very different cycle to the last one and we should therefore expect different inflation and Fed outcomes. We repeat a few slides on this in the chart book so feel free to dip in.

These growing expectations of near-term hikes supported the more policy-sensitive 2yr Treasury yield, which rose a further +3.8bps to a fresh post-pandemic high after the previous day’s massive +13.3bps advance. And the number of hikes priced for 2022 as a whole actually rose to a new high of its own at 4.8 hikes. However, a -6.4bps decline in the 10yr yield to 1.80% meant that there was a further flattening of the yield curve, with the 2s10s down to its flattest level in over a year, at just 60.9bps. This is only adding to the late-cycle signals we’ve been discussing of late, particularly when you consider that the yield curve historically tends to flatten in the year after the Fed begins hiking rates, so an inversion over the next 12 months would be no surprise on a historic basis followed perhaps by a 2024 recession? See the chart book for more on this. Indeed, some parts of the curve are even closer to inverting than the 2s10s, with the 5s10s slope at just 14.1bps yesterday, which is the flattest it’s been since the initial market panic about Covid back in March 2020…

And as an AAPL fanboy,

Apple reported fourth quarter earnings after the close. Like other goods manufactures, they continued to be besot by supply chain issues, but that did not stop them from beating sales and earnings estimates, posting their best quarter of revenues ever. The stock was more than +5% higher in after-hours trading following the release. Prior to this they were down around -10% YTD. This has helped the S&P 500 (+0.7%) and Nasdaq (+1.1%) futures rebound as we hit the last day of a tough and very volatile week.

With some overnight flare, too,

Overnight in Asia, equity markets are also recovering some of their recent losses with the Nikkei rebounding (+2.17%), after falling nearly -3% in the previous session, followed by the Kospi (+1.44%). Meanwhile, the Shanghai Composite (+0.05%) and CSI (0.08%) are trading flattish as we type. On the other hand, the Hang Seng (-0.94%) is extending its recent losses this morning ahead of the release of Hong Kong’s Q4 GDP report scheduled in a few hours.

Early morning data showed consumer prices in Tokyo fell to +0.5% y/y in January from +0.8% in December while the core CPI inflation (+0.2% y/y) in January failed to exceed market expectations (+0.3%) after increasing +0.5% last month. Elsewhere, South Korea’s industrial output surprisingly advanced +4.3% m/m in December against economist expectations of -0.3%. It follows November’s upwardly revised +5.3% increase.

Back in Europe, sovereign bond yields rose for the most part, having been closed at the time of Chair Powell’s press conference the previous day. Those on 10yr bunds (+1.6bps), OATs (+0.7bps) and gilts (+3.1bps) all moved higher, and that rise in gilt yields comes ahead of next week’s Bank of England decision, where overnight index swaps are now pricing in a 94% chance of another rate hike, which is also our UK economist’s expectation.

One factor supporting sentiment yesterday was a decent set of economic data, with the US economy growing by an annualised rate of +6.9% in Q4 2021 (vs. +5.5% expected). That’s the fastest quarterly pace since Q3 2020 when the economy rebounded sharply from the various lockdowns, and left growth for the full year 2021 at +5.7%, the fastest since 1984. Meanwhile, the weekly initial jobless claims for the week through January 22 subsided to 260k (vs. 265k expected), ending a run of 3 consecutive weekly increases.

Now in as far as the Fed’s hawkish shift goes, the latest Global Market Views,

FCI tightening finally begins. 2022 so far is not like 2021. The last few weeks have been dominated by tightening US financial conditions, as the Fed’s policy shift has finally pushed real yields higher and equities lower (Exhibit 1). The Fed’s pivot over the last two months has been large and fast. In late November, as it began, the Fed’s latest projections showed a median forecast of one hike for 2022. At yesterday’s FOMC, Chair Powell opened the door to the prospect of more than four hikes this year. The price action in January is largely a belated recognition of that hawkish shock. We have expected the interplay between Fed tightening, financial conditions and growth to dominate the 2022 picture. The core of our US forecast is both that the tightening cycle has more room to extend than the market is pricing and that the economy will prove resilient enough to that tightening to keep the recovery going. With nearly five hikes priced for 2022 and a message that more might come, the distribution of risks is more symmetric than it was—a better place for both the Fed and ultimately for markets. After the sharp sell-off in equities, we think we may now begin to find our footing, particularly in more cyclical areas of the market as the pace of hawkish innovations slows and the omicron’s impact on activity fades. But we expect to revisit this dynamic through the course of the year. Paid rates positions in the US and some other DMs and long positions in back-end oil and copper are still our highest-conviction views and the areas where our forecasts stand out. And while we could see short-term relief, we remain wary of areas that are most vulnerable to a faster pace of Fed tightening and real yields, like the frothy parts of the tech sector and crypto. Despite ongoing Fed risk, we have become more willing to consider risk in parts of the EM complex, as China easing and fatter risk premia provide cushions that are harder to find in the DM world.

AND they continue along with several more talking points,

Pricing a more hawkish Fed. Waking up slowly to the Fed. Still most likely the growth-rates tango. China: a better vibe apart from Omicron. Commodities: long-dated upside a core view for the year. Valuation and carry buffers lead to tentative EM resilience. Overvalued Dollar likely to remain at lofty levels for now. Crypto at ground zero of macro rotations. Constructive but more selective

… Global trade volumes registered a strong growth of 2% in November over the previous month, as indicated by the latest figures from the CPB Netherlands Bureau of Economic Policy. With November’s data release, the global trade momentum turned positive after four months and trade volume isnow 7.5% above the pre-Covid level. Global growth was primarily driven by advanced economies, where import growth outperformed export growth. We revisit the transportation and logistics bottlenecks to gauge the current situation. While there are some indications of easing of supply constraints, shipping prices still remain elevated. The situation might get affected by the upcoming Lunar New Year and the associated factory closures and port delays. Moreover, the spread of the Omicron variant and renewed restrictions in Asia remains a key downside risk well into the first half of 2022.

Now another large British (and American) bank also on trade — offering a somewhat more muted view,

Barclays: Global supply chains: Still far from business as usual China's COVID outbreak has raised concerns over another round of supply shocks, but we believe the country’s domestic policy imperatives will aim to minimise disruptions. Globally, supply bottlenecks eased over the past few weeks, but price pressures may not decline amid renewed uncertainty.

… The flattening of the U.S. yield curve has been relentless and that suggests inversion will soon become a hotly-debated topic in markets -- and then, dare I say it, recession. That seems like crazy talk when fourth-quarter GDP smashed expectations but in the bond market at least there are worries the Fed will blow up the economy with rate hikes. The spread between 5-year and 30-year bonds has narrowed over 20 basis points this month to just over 40 basis points, and is close to its flattest since December 2018. With odds slowly building on a 50 basis point rate increase in March and almost five hikes for the year, you can understand the nervousness in markets. Inflation has yet to buckle, wage pressures are building and there is the risk of a disorderly hiking cycle in a world laden down with debt. On the plus side, at least the omicron impact looks like a short one. Still, the more the yield curve flattens, the more the talk of inversion will grow. And remember, it's an event with a reliable track record of presaging a recession within roughly the following 18 months.

This visual complimented by Authers LATESTwho notes curve relationship

…What is startling about this yield curve flattening is that it’s come so soon before the Fed has even started raising rates. If the curve swiftly moves to inversion, it grows far harder for the Fed to carry on with its hiking program:

Now we KNOW what the government bond curve ‘chatter’ has been and that it is likely to grow given the flattening but what then about CREDIT SPREADS, you ask?

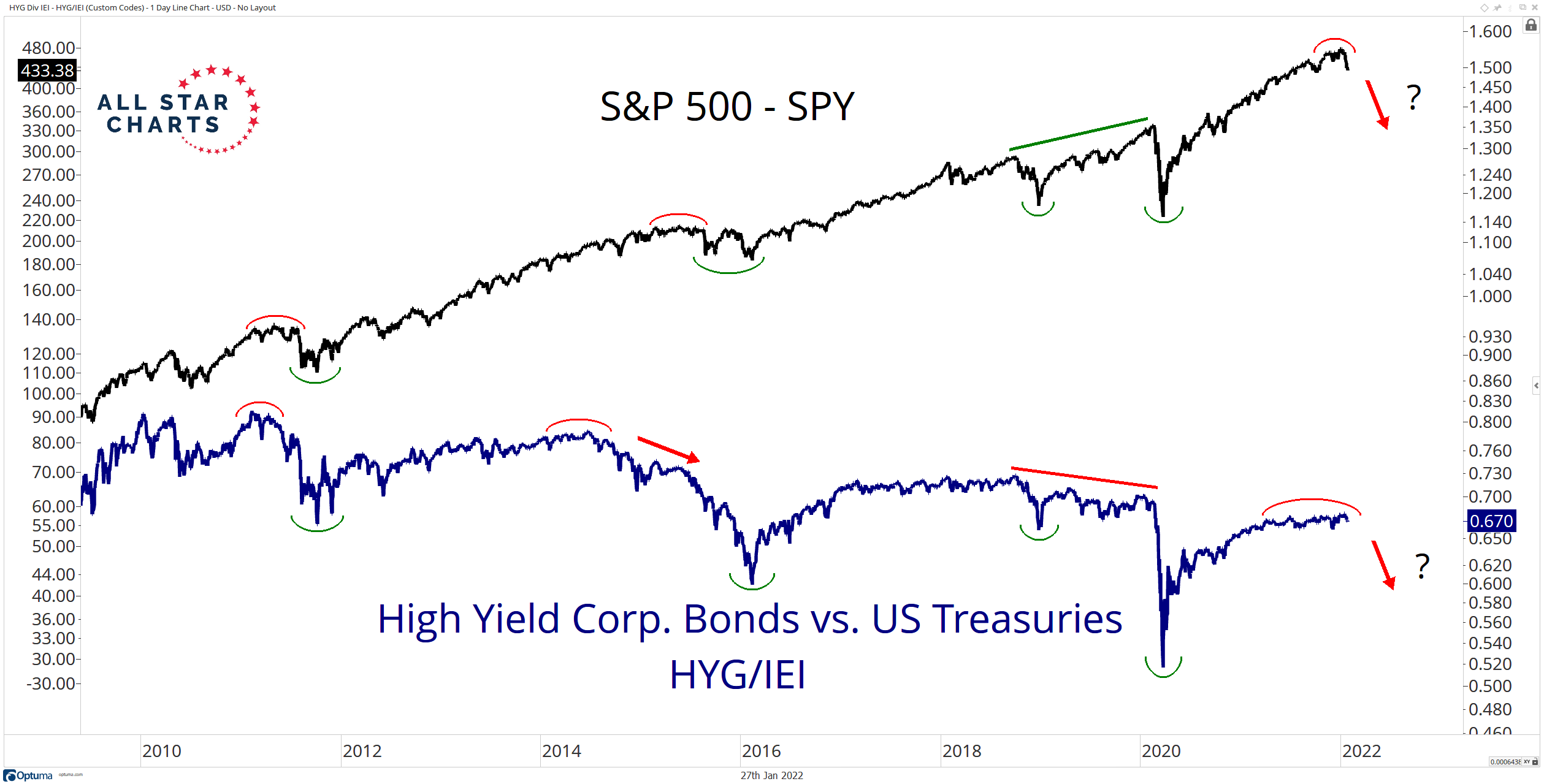

AllStarCharts: Breaking Down Credit Spreads … We can also study these relationships by comparing the bond prices themselves, instead of their yields. One of our favorite ways to do this is by charting the High-Yield Bond ETF $HYG relative to the Treasury Bond ETF $IEI.

We’ll dive into this ratio in today’s post and discuss where it’s likely headed from here, and more importantly, what it all means for risk assets.

First up, we have a chart of the HYG/IEI ratio overlaid with the S&P 500 $SPY:

When HYG/IEI is trending lower, it means credit spreads are moving higher, or widening. Remember, yields are simply a function of bond prices.

When we look at these two charts together, it’s clear that they tend to top and bottom around the same time. This makes sense. When times are good and investors are embracing risk, stocks tend to rally and high-yield bonds tend to outperform.

Now, let’s talk about what’s happening today. HYG/IEI has built a topping formation and is beginning to turn lower as credit spreads widen. This is not a good look for equities.

The HYG/IEI ratio is largely driven by the rate of change in the numerator, which is high-yield bonds. This is simply because it’s the higher-beta component.

To illustrate this point, here’s an overlay chart of HYG and the HYG/IEI ratio:

As you can see, the ratio essentially follows high-yield bonds on an absolute basis.

… The bottom line is bulls want to see high-yield bonds recover ASAP. If they don’t, then we have to expect lower prices for high-yield will lead to widening credit spreads. And this is definitely not something the bulls want to see.

It hasn’t happened yet. But with HYG at fresh 52-week lows, the writing is on the wall. With rates on the rise and the US stock market under pressure, it’s time to watch these developments closely and heed the message of the bond market.

Ok so we’ve got a bit of curve callin’, credit spreadin’ talk and all this matters in as far stocks and sectors and the like. How do I know? Because head stock picker and former ML strat says so,

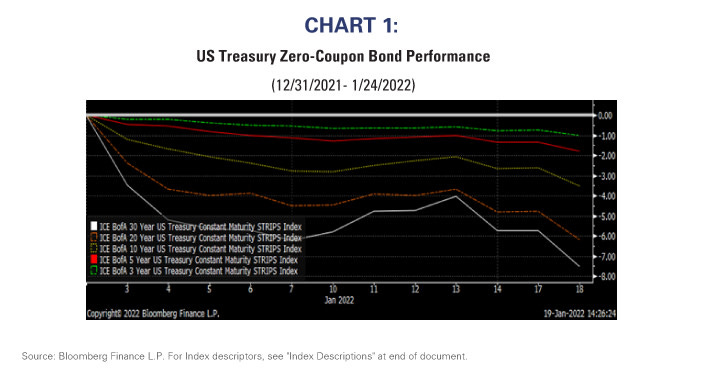

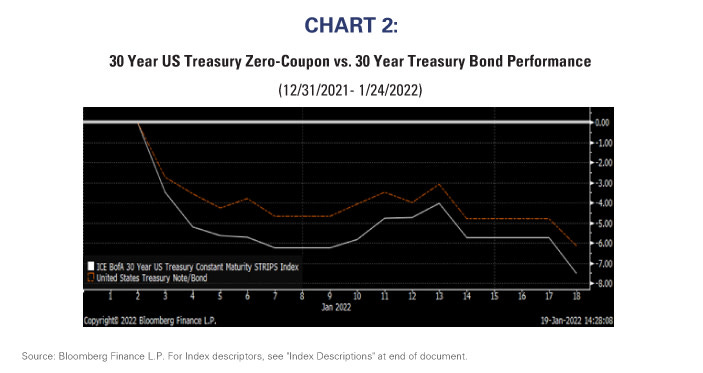

…Chart 1 shows the duration effect on performance so far during 2022 of zero coupon bonds of varying maturities. Chart 2 shows a similar comparison between the 30-year zero coupon bonds and current 30-year coupon bond.

How does duration apply to equities?

Our research during the 1990s highlighted a way to theoretically measure the interest rate sensitivity within equities. Unlike fixed-income, which as the name implies pays fixed rates of interest, equity cash flows can vary immensely and must be estimated. Analysts’ estimates for near-term and longer-term growth rates can be used to sketch expected future cash flows.

Such analyses suggest higher dividend paying stocks (like Utilities) have shorter durations because of their higher near-term dividend payments, whereas growth stocks (like Technology) have longer durations because of the lack of dividends but an anticipated long-term return.

However, investors must account for the correlation between interest rates and earnings. The earnings and cash flows of cyclical stocks are often positively correlated with interest rates because their earnings are economically sensitive. Interest rates tend to rise as the economy strengthens, but so do the earnings of cyclical stocks. Interest rates generally fall as the economy weakens, but so do the earnings of cyclical stocks.

Thus, the durations of cyclical stocks will change, sometimes significantly, as interest rates increase or decrease. Because earnings and cash flow estimates for cyclical industries tend to increase as interest rates increase, cyclical stocks’ durations will incrementally shorten as rates increase. On the other hand, cyclical earnings and cash flow estimates decrease as rates decrease. However, the earnings and cash flow estimates for stable or long-term growth companies don’t tend to change as much when interest rates change because their cash flows are relatively unaffected by the overall economy.

A simple measure of equity duration

A simple measure of equity duration is a PE ratio. A PE ratio of 5, within this simple model, suggests today’s price equates to 5 years of earnings, whereas a PE ratio of 30 suggests today’s price equates to 30 years of earnings.

A standard axiom of investing is PE ratios expand as interest rates fall and, ignoring cyclical earnings growth, a stock with a PE of 30 will tend to outperform a stock with a PE of 5 when interest rates fall just as a 30-year zero-coupon bond will outperform a 5-year zero. The reverse tends to be true when interest rates increase.

Charts 3 and 4 show the relationship between the 10-year T-bond yield and the S&P 500® Technology and S&P 500® Energy Indices over the past 5 years. Certainly interest rates are not the only variable effecting the pricing and the valuation of either sector, but the charts indicate that the longer-duration Technology sector has greater interest-rate sensitivity than does the shorter-duration Energy sector.

… Interest rates do matter

The concept of equity duration helps to explain why certain sectors outperform or underperform during periods of rising or falling interest rates.

Investors have been spoiled by decades of falling interest rates. If that trend ends, then it seems unlikely that the long-term growth leadership will continue. Investors might consider looking at shorter-duration equity strategies to help buffer any trend in rising rates.