Good morning. Overnight flows clearly all done with the more hawkishly perceived FOMC meeting (statement / opening comment / principles forQT HERE and press conference HERE) in mind. I’ll attempt to offer a couple other items which may be of interest but FIRST,

BMO: Flattening Follow-Through … … Overnight Flows Treasuries were modestly bid overnight with 5s/30s flattening to 43.8 bp. Overnight volumes were elevated with cash trading at 152% of the 10-day moving-average. 5s were the most active issue, taking a 31% marketshare. 10s managed 22%, while 7s took 10% and 20s 1%. 2s were particularly active at 19%, while 3s took 13% and 30s garnered 4%. We’ve seen buying in 2s and 10s.

(refresh / check this post later for any input from other shops reporting what happened while we slept)

AND away from US markets, Goldilocks on some China data overnight,

China: Both industrial profits and revenue fell sequentially in December Bottom line: China's industrial profit growth moderated to +4.2% yoy in December. In sequential terms, industrial profits contracted further by 4.2% mom non-annualized sa in December following a decline of 16.8% mom in November. Industrial revenue fell 9.4% mom sa in December.

Other news you can use » IGMs Press Picks for today (27th Jan) to help weed thru the noise (some of which can be found over here at Finviz).

CNBC: U.S. futures trim losses as investors assess Fed update

A fan-fav recap from the sellside comes via this early morning Reid,

… So what did the FOMC actually say? Well they did leave policy unchanged as expected, while the statement signalled it would soon be appropriate to raise the federal funds rate, in line with market expectations. The FOMC also released principles for reducing the balance sheet, which were more or less identical to the last round of QT. That is, the Fed will gradually decrease the size of its balance sheet by letting securities mature uninvested, not through sales, in line with our house view.

The press conference proved much more interesting though. Our US econ team has their full review here, where they have added a hike for 2022, with the base case now five. The biggest takeaway was the Chair’s emphasis that this cycle was different from the last round of tightening, in that inflation is well-above target, the labour market is historically tight, and growth projections remain above long-run potential. While the Chair demurred when asked what that specially meant for parameters of monetary policy, he did not rule out a faster pace of rate hikes or larger increments, adding that the Fed had plenty of room to tighten given the state of the labour market. This was the catalyst that sent shorter-dated yields higher, driven by real yields, as markets priced in a higher probability of an earlier and steeper policy path. Underscoring the shift towards tighter policy, he noted the Committee still viewed the balance of risk tilted towards higher inflation, and that the inflation picture had probably gotten worse since the Committee last submitted projections for the dot plot, which only contained three hikes this year. Presumably more hikes will be incorporated in the March dots.

Speaking of March, the Chair confirmed liftoff was likely to take place at the March FOMC, flagging the risks that would prevent that from happening including a worse-than-expected impact from Omicron (which he noted should not be persistent), and intimated geopolitical risks could pose an issue. So March, and every subsequent meeting should be treated as live with a 50bp hike at some point an increasing possibility.

On balance sheet policy, the Chair noted no decisions were made, and that conversations would continue at upcoming meetings (plural), implicitly matching our US econ team’s timeline that QT will begin after multiple rate hikes. He re-emphasized the message laid out in the balance sheet principles document that the Fed will set caps and let securities mature at a predictable pace, adjusting parameters as needed, but the Committee would rely on rate policy to control monetary policy…

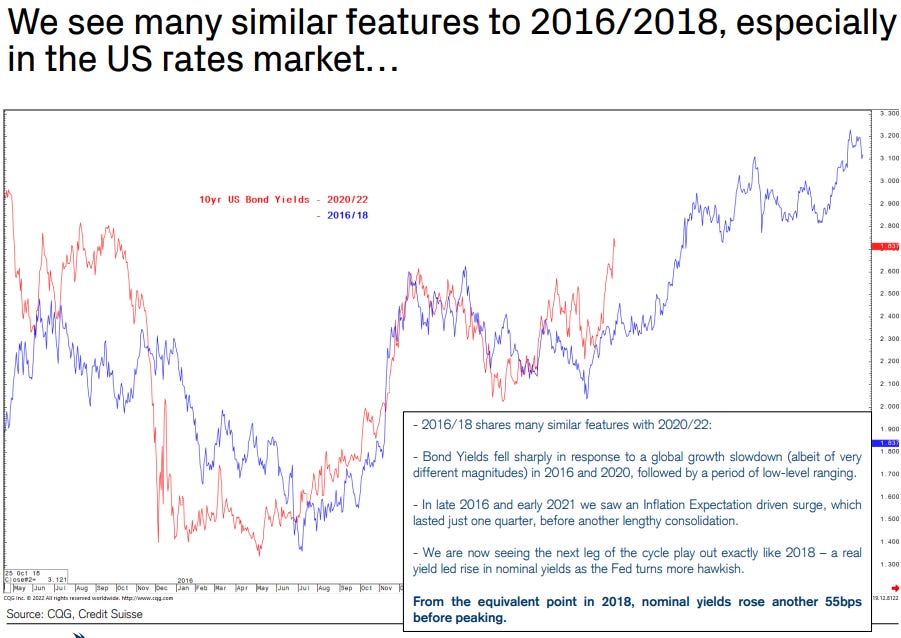

Also from large German bank comes a trade idea from Reids colleague,

Fed packs a punch: buy the FFJ2-FFF3 spread for quick and nimble hikes …Post Fed, our economists revised their baseline view to the Fed raising rates at every meeting from March through June, then at a quarterly pace for the rest of the way. Importantly, this amounts to five total hikes for this year, or four additional hikes after the anticipated March liftoff. If this expectation is realized, it would suggest a fair value for the FFJ2-FFF3 spread of around 100bp. However, we see scope for the market to overshoot as risks continue to tilt toward the Fed needing to hurry to get itself to a restrictive policy stance. We recommend buying the FFJ2-FFF3 spread at 90bp, target 105bp, and stop 82bp.

And in simple titles format from John Authers of BVIEW with some attention to the detail of what happened in front-end

… The rise in short-term expectations was spectacular. The two-year Treasury yield was flat for the day as Powell rose to speak. By the end of the sessionit had risen 13 basis points. Aside from one moment of terror during the bond market meltdown caused by the initial Covid shutdown in 2020, this was its biggest one-day rise since the Great Financial Crisis:

Looking specifically at FOMC days, this chart from Mitsubishi UFJ Financial Group Inc. shows that it was the greatest rise for both the two-year and 10-year yield since the GFC: