Good morning. From one important speech last night to another this morning at 10a.

I’d like to start with a few A FEW WORDS FROM BLOOMBERGrelating specifically TO the Fed chair today and where the (front end of the) bond market is concerned,

…The bond market has seriously downgraded its expectations for global growth as Russia’s invasion of Ukraine escalates. The disruptions to supply chains and financial markets are getting broader and deeper as the U.S. and the European Union impose sanctions, prompting businesses to sever or suspend ties with Russia.

Commodity prices are also spiking -- WTI crude is up almost 40% this year -- but investors are more concerned about the hit to economic activity than that potential surging raw materials costs will accelerate already sizzling inflation. Two-year Treasuries are leading the charge as rates traders slash bets that the Federal Reserve will aggressively hike interest rates in the current, gloomier environment. Yields on the notes, among the most sensitive to the monetary policy outlook, are back below pre-pandemic highs just a few weeks after jumping back above those levels.

For the professionals out there, here’s what they (a large Canadian shop) says happened overnight

…Overnight Flows

Treasuries were under pressure overnight as investors await Powell’s testimony. The curve was decidedly flatter with 2s/10s dipping to 34.4 bp. Overnight volumes were elevated with cash trading at 107% of the 10-day moving-average. 5s were the most active issue, taking a 37% marketshare while 10s were a distant second at 28%. 2s and 3s combined to take 24% at 11% and 13%, respectively. 7s managed 7%, 20s 1%, and 30s 3%. We’ve seen selling in 2s, 5s, and 10s….

… and for some MORE of the news you can use » IGMs Press Picks for today (02 March) to help weed thru the noise (some of which can be found over here at Finviz).

With what happened overnight, here are some updated (technical) FI thoughts from 1stBOS just before mkts closed yest as some hay met the barn

10yr US Bond Yields have seen the warned of corrective move lower, but now face much more important resistance at 1.70/68%.

Outlook: US 10yr Bond Yields have seen the warned of correction lower following the cross in daily MACD momentum and bullish daily RSI momentum divergence. However, the market has now reached more important resistance at 1.70/68%, which is the 50% retracement of the upmove from November, the 38.2% retracement of the upmove from August and the series of yield highs and lows dating back to May 2021. Furthermore, the “neckline” to the major 3-year yield base is also just below at 1.65/635%, which we view as a similarly major resistance zone. With such important levels nearby, our base case is to watch for signs of a floor here and for a reversal back higher, before several weeks of sideways consolidation. With this in mind, first near-term support is seen at 1.865%, above which should confirm a floor. From a long-term perspective, we still see scope for an eventual move beyond here towards 2.34% by the end of 2022, but this is a distant prospect for now.

Short-term Strategy: We neutralise our successful tactical bullish bias from 1.99% after resistance at 1.74/73% was reached, however we would not reverse into a tactically bearish stance until we see signs of a base.

The firm prefers to STAY NEUTRAL on 5yy and 30yy, too. Well done with 10yr trade.

From everyone’s fav early morning read from a large German bank, relating TO the visual of 2yy above,

… This shift in central bank pricing was evident in the United States as well, where Fed funds futures not only moved to fully price out a 50bps hike at the next meeting, (only 96% probability of a 25bp hike now), but also priced out another -12.0bps worth of hikes from 2022 as a whole, having already taken out -21.5bps worth the previous day. This heightened uncertainty means that all eyes will be on Fed Chair Powell today, who’s testifying before the House Financial Services Committee, and his appearances today and tomorrow will be some of the last Fedspeak we get before the FOMC enters their pre-meeting blackout period this Saturday. In terms of the reaction from Treasuries, they had a more subdued move relative to their European counterparts, although yields on 10yr Treasuries were still down -9.8bps on the day to 1.73%, again entirely driven by lower real yields. There is not much change overnight. As I mentioned yesterday, real yields collapsing has probably helped cushion the blow for risk assets of the recent very negative events. US 10yr real yields are now -54.8bps lower from their post US CPI levels (Feb 10th), and -37.3bps over the last two days. At -0.97% they are below their levels from immediately before the December FOMC minutes released in early January that signalled the FOMC was more actively considering QT than the market was expecting, which kicked off the Fed’s hawkish turn that was the dominant market story for the first six to seven weeks of the year. How quickly things change. One other rates dynamic we were covering a lot before the geopolitical escalation was the flattening of the yield curve. The 2s10s curve has only flattened around -7bps since Biden’s speech noting an invasion was imminent back on February 11, so the rally has been a relatively parallel shock lower for the entire curve….

Also from this large German bank, comes an updated and INCREASED ‘Earl f’casst

Finally, from the same firm, a VISUAL which, in this specific strategist screams the market’s got it wrong (in the EZ anyways

The market, dear sir, is never wrong and the process getting HERE is what most missed. It started well in advance of the current war-time backdrop and telling us NOW the market is wrong, well, doesn’t forgive the error of all the ways which led here / now.

BUT, as the saying goes, haters gonna hate. Great Unwind next, right?

As far as STOCKS are concerned, a large British bank stock jockey note clarifies,

Who Owns What: Positioning a mixed bag, broad capitulation still a risk … Broad capitulation not seen yet, as 'TINA' still prevails. Despite the negative price action ytd, MFs have continued to add to equities at the expense of bonds, credit and cash. Retail remains active too, even though it has been slower at buying dips most recently, and sentiment is depressed. In a sense, rising inflation has reinforced the 'TINA' argument to own equities, although growth and earnings fundamentals have been supportive too. The V-shaped rebound post the COVID bear market in March 2020 was helped by very low MF/retail exposure. But this is not the case now, as both categories are near maximum OW. While a recession is not our base case, capitulation by LOs and retail is a key risk for equities if the geopolitical situation worsens…

… Over the last month, even as price action turned more negative and uncertainty increased, equities continued to receive steady inflows, while MFs cut exposure to credit and cash. As a result, the divergence between bond and equity flows has increased materially. In a sense, rising inflation seems to have reinforced the ‘TINA’ argument to own equities vs. fixed income.

All sounds very ‘NEXT GREAT UNWIND’ (ie haters gonna hate) to ME… See latest from money center bank (and same shop enlightening us as to what happened overnight) in latest POSITIONS REPORT,

Shorts and loss in Eurodollar - losses growing on extended shorts in whites and now squeezing legacy positions - ED Dec 22 offside above 99.32 with next level at 99.51 ( legacy squeeze)

Extended short in 10y (at $22m / 95th percentile) / max losses at 25bps… with short now offside above 127-00 and CTA trimming shorts at 127-30 / next stop at 129-00 (CTA long)

Mild shorts in 30y (at $7m / 70th percentile) => balanced risk with shorts onside below 186-16 and recent longs onside above 184-00

The war in Ukraine impacts the global economy through three channels: higher commodity prices; sanctions (government or private sector); and the collapse of the Russian economy. Russia is a relatively insignificant economy, but a significant producer of some commodities, so commodity prices are the most potent channel.

Commodities are not consumer prices—e.g. developed economy food prices are mainly labor costs. As commodity-intensive goods tend to be high frequency purchases, they drive consumer inflation expectations. Consumer inflation expectations only matter if consumer behaviour changes as a result (it rarely does).

If commodity prices are passed on to consumers, consumers have less money to spend on non-commodity goods and services. This matters as goods supply is at an all-time high. Confronted by an extreme shock (e.g. banning Russian energy imports), consumers will adapt behaviour more than markets think. Working from home cuts electricity consumption; food waste could be reduced, etc.

US Federal Reserve Chair Powell and ECB Chief Economist Lane speak. The US taxation system ties consumer energy prices more closely to commodity prices. Europe’s economy is more vulnerable to Russian supply. If commodities create a wage-price spiral, the narrative is a price inflation shock (stronger policy action). If there is no wage-price spiral, the narrative is a growth deflation shock (moderate policy action).

Finally, in closing, when JPOW meets lawmakers later on today, we’ll be watching 2yy, thinking of the Ukranian people and our own set of stagflationary realities

Sorry Paul, commod prices are an opportunity for large and small (visual above local bagel shop) and I don’t care WHAT you say … The current set of inputs seem to ME to be leading the Fed right in to a corner and I do not envy them with in the least.

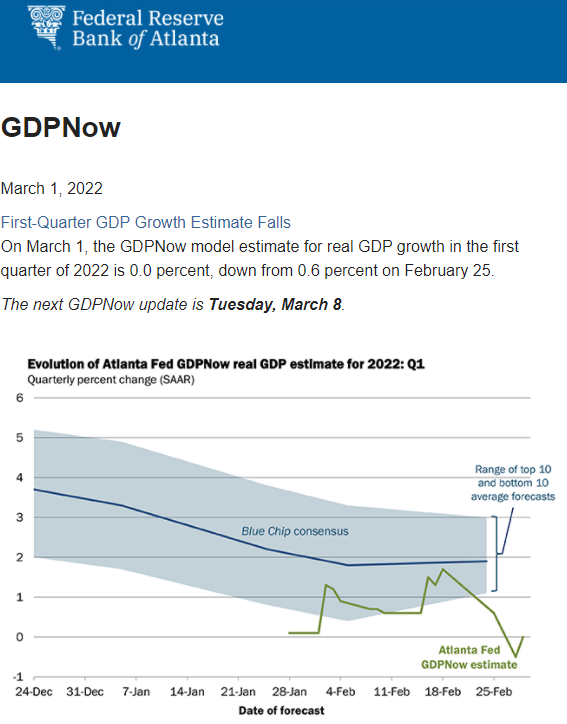

With a current read from Atlanta Fed falling TO ZERO-POINT-ZERO

Hard NOT to think STAG-flation (ZH did it so, must be legit, AmIRight) and also hard NOT to expect lawmakers TO JPOW to look / sound something like this a bit later on today,