Good morning … Not much change with regards TO 20yy ahead of this afternoons liquidity eventso how ‘bout a look at 1yr TBILLS having a peak up OVER 5%

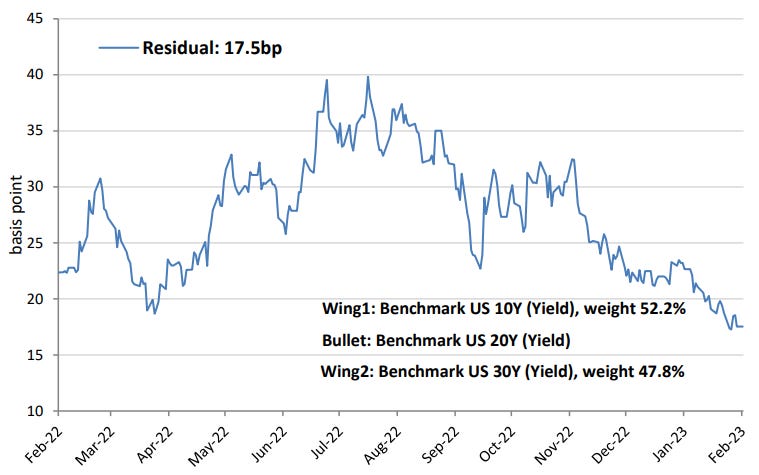

For somewhat MORE on 20yr, a visual from a large German bank on how it’s set up on 10s30s curve,

… 10s-20s-30s butterfly (curve neutral, 52.2% and 47.8% on the wings)

Get those bids in early and often and meanwhile — OVERNIGHT the UKs headline inflation slows to 10.1% from 10.5%, below 10.3% expected.

The Feds Williams said in a speech entitled “Our Work Is Not Yet Done” that “We need all the gears turning at the right pace to restore balance between demand and supply in the entire economy. We still have some way to go to achieve that goal.”

There was other important fedspeak and to be sure, markets are, on the one hand, losing (democratic leaning) DOVE, but on the other hand, gaining, well, just that … another democratic leaning DOVE as White House announces Brainard nomination to the National Economic Council.

… here is a snapshot OF USTs as of 705a:

… HERE is what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are slightly higher and off earlier highs with the curve little-changed ahead of today's data slate and Treasury 20yr auction. DXY is higher (+0.25%) while front WTI futures are lower (-0.75%) after yesterday's afternoon's big crude oil inventory build (link above). Asian stocks were mostly lower, EU and UK share markets are mostly higher while ES futures are showing -0.35% here at 6:40am. Our overnight US rates flows saw Treasuries in a holding pattern during Asian hours with our activity seeing better buying in intermediates and 2-way action in the long-end. Overnight Treasury volume was about 70% of average overall with shockingly little turnover (33% of ave) seen in 20yrs ahead of their afternoon auction...

… Treasury 5yr yields probed their range support level near 4.026% yesterday, holding serve/support there amid a locally deep 'oversold' condition (lower panel). So 5's could be an important 'tell' whether 10's have a clear path to 3.885%, or not.

… we show the 2s3s5s Treasury 'fly and how the -10bp area has been the graveyard of 3yr outperformance on curve over the past year- with 2s3s5s testing that level early yesterday, resoundingly rejecting it again. Daily and now weekly momentum studies aim higher and hint of further underperformance on curve by 3's, for what it's worth...

… and for some MORE of the news you can use » IGMs Press Picks for today (15 FEB— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

After yesterday's US inflation numbers DB have increased our US terminal rate forecast from 5.1% to 5.6% with two extra 25bps hikes in June and July. From what I can see we are the highest on the street again as we have been for most of the last year…It was only 2 weeks ago that terminal was being priced at around 4.80% and December 2023 contracts at 4.30%. Last night we closed at 5.27% for the July contract and 5.07% for December, both fresh highs for the cycle and up +7.3bps and +14.9bps on the day. On top of that, 10yr Treasury yields closed at a new high for 2023 of 3.74%, which brings their gain to c.+41bps since an intraday low of 3.33% less than two weeks ago. Whichever way you want to cut it, it’s clear that the jobs report and the latest CPI print have painted a much more robust picture for the US economy than the consensus expected at the start of the year…

For the large German banks full CPI post op, click HERE and from Germany to France where a former German bank economist has landed (after several yrs at BBG)

Broad-based pressures in January CPI to keep Fed on its toes

KEY MESSAGES

Main takeaway: Resilience and breadth were the two key themes of the January CPI report. Non-housing service inflation barely budged at a nearly 6% m/m annualized pace, while a bounce in non-vehicle goods prices suggests that goods disinflation may prove bumpy and prone to upside surprises. Price gains were broad-based amongst both goods and services.

Backdrop of near-term strength: While January CPI printed in line with both our and consensus expectations, it showed inflation remaining well above target against a backdrop of an excessively strong labor market and a pick-up in activity data.

Fed on track for further hikes: This combination should keep the Fed on track to deliver 25bp hikes in both March and May, in our view. With just three FOMC participants needed to shift the median 2023 dot, we flag risks that it shifts up to 5.5% at the March FOMC meeting.

Setting CPI aside and rummaging around the room for instructions on how to play DEBT CEILING CHICKEN, a large French bank

The US debt limit standoff has always been resolved in the past, but the current political environment could induce a similar showdown to the 2011 debt ceiling crisis, in our view. Meanwhile, a lengthy US default could devastate the US economy and cause significant repricing in financial markets.

The debt ceiling was established in the early 1900s so that Congress no longer needed to approve each issuance of debt and to grant more borrowing authority and flexibility to the Treasury department.

However, the US debt ceiling has become a stressful issue nearly each year, raising concerns about when the US government could default on its debt obligations if Congress failed to raise or suspend the debt ceiling.

After each time the debt ceiling is either reached or reinstated, the Treasury resorts to extraordinary accounting measures and its available cash to avoid defaulting on its debt. This is accompanied by volatile T-bill issuance and liquidity conditions, along with dislocations in money markets.

We anticipate future publications to be released as new developments on this topic arise, assuming the debt ceiling standoff lasts the next several months.

From Germany to France and from Global Wall St TO quasi OFFICIAL site — FRBNYs Liberty Street econ department,

What types of foreign firms are most affected when the Federal Reserve raises its policy rate? Using cross-country firm level data and information on input-output linkages, recent empirical research finds that the impact on sales and investment spending is largest in sectors with exposure to trade in intermediate goods. The research also finds that financial factors drive differences, with U.S. monetary policy spillovers having a much smaller impact on firms that are less financially constrained.

For MORE from quasi official accounts, the KC FED IN PRINT (dated Feb 3)

The Federal Open Market Committee has been quickly raising the federal funds rate to lower inflation. However, services inflation remains high, supported by a tight labor market with high wage growth. Recent readings in the LMCI momentum indicator suggest monetary policy tightening is beginning to weigh on labor markets, which may eventually lead to lower services inflation and lower inflation overall.

In other words, don’t worry and it is NOT different this time?

Dunno ‘bout you but seems to ME there’s now a concerted effort to make us all feel absolutely fine … nothing to see here … move along, back to our cars, shows over

And with that visual in mind … Palestine, OH by way of Chinese news — Global Times, as much as it pains me … I believe this goes beyond whatever Fox / Tucker Carlson may / may not think …

The line between Entertainment and US News Media is probably even blurrier than you fear? If it is already in the Public's zeitgeist why beat a dead horse? Or maybe it is a simple calculation: which could bleed more? WWIII or some spillage of paint-thinner that has already evaporated, talk about 'move on nothing to see here', in a forgotten speck of the vast Rust Belt America?

![This is Fine. - 3D model by msanjurj (@msanjurj) [49efaa2]](https://substackcdn.com/image/fetch/$s_!YQbH!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fee6645a9-9a60-4535-ab01-a2eaa40c4cd1_1920x1080.jpeg "This is Fine. - 3D model by msanjurj (@msanjurj) [49efaa2]")

US Media and the train derailment? Finally a softball question! Easy answer is we just saw that movie!

https://www.polygon.com/reviews/23522513/white-noise-review-netflix

The line between Entertainment and US News Media is probably even blurrier than you fear? If it is already in the Public's zeitgeist why beat a dead horse? Or maybe it is a simple calculation: which could bleed more? WWIII or some spillage of paint-thinner that has already evaporated, talk about 'move on nothing to see here', in a forgotten speck of the vast Rust Belt America?