Good morning … ahead of today’s CPI and tomorrow’s ReSale Tales, I thought I’d take a moment to look at 20yy ahead of tomorrow afternoons liquidity event …

Daily momentum oversold while weekly appears overbought … pick your time frame and how YOU intend to approach next 24, 72hrs (or several days/weeks/months) and place your bets … something for everyone as you attempt to plan your trades and trade your plans. In the meanwhile, here is a snapshot OF USTs as of 709a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher and the curve a hair steeper ahead of CPI and today's raft of Fed speakers (3 voters). DXY is lower (-0.35%) while front WTI futures are lower too (-1.85%). Asian stocks were mostly higher, EU and UK share markets are all roughly +0.5% while ES futures are showing +0.25% here at 6:45am. Our overnight US rates flows saw light trading conditions during Asian hours with better buying in the long-end noted by our Tokyo colleagues. Overnight Treasury volume was ~80% of average overall with only 30yrs (103%) seeing above-average turnover, matching our Asian activity…

… The Treasury 2s5s curve is interesting because it continues to show a rounding bottom-like vibe. Since late last year, each push to a new low has been more feeble than the prior one, as illustrated. And what's quite clear looking at the daily closes is that the -66bp to -68bp zone is your major support for this curve.For now investors appear distinctly unwilling to press the 2s5s flatteners below -65bp. So there's that.

… and for some MORE of the news you can use » IGMs Press Picks for today (14 FEB— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

US January consumer price inflation is likely to produce a frenzy of media excitement. Technical factors mean that while inflation is slowing, it will slow more slowly. Many companies traditionally increase prices at the start of the year, and with profit expansion behind much of current inflation, that may be more relevant than normal. Reweighting the different components of inflation also (temporarily) slows disinflationary pressures. However the lived experience of US consumers is likely to be more disinflationary than the headline data.

Markets also care how the Federal Reserve interprets the data. Here, the news that Fed vice chair Brainard is to move to the White House is a bit of a blow. Brainard was one of the economic adults on the Fed’s leadership team…

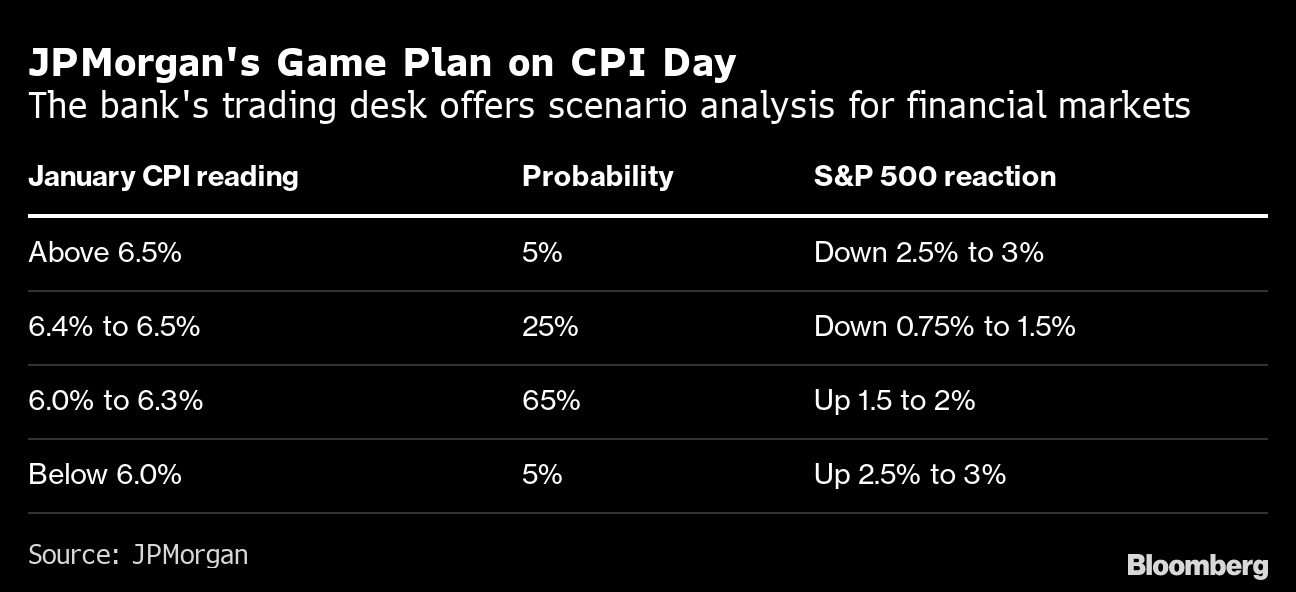

And John Authers / BBG offers some thoughts and JPM game planning,

… At JPMorgan Chase & Co., a team has gamed the way the figures on the yearly change in the CPI could be received by the market. Bloomberg colleague Lu Wang reported the scenarios the firm has for various outcomes and how these would impact the S&P 500. Data close to estimates would be treated as confirming a continued cooling in inflation, which would imply falls for bond yields and the dollar, while tech shares would lead an advance for US stocks. But any equity gains are likely to fade, they warned, “once investors shift attention to a relatively slower pace of disinflation than the previous two months, where each CPI print saw a decrease of 60 basis points.” The firm is betting on a print for year-on-year inflation that comes between 6.0% to 6.3% (which is bang in line with the consensus Bloomberg survey estimate of 6.2%):

Market moves over the last few weeks suggest a hurry to get away from bets that inflation will come down fast, especially since the jobs data. Two-year Treasury yields rose to a high for 2023 in the wake of the employment report, climbing 23 basis points last week as warnings from Fed officials that further interest-rate hikes suddenly seemed more believable. Traders are now reevaluating how high they will rise this year, fueling bets for the Fed to peak at 5.2% in July, up from less than 5% a month ago.

More importantly, confidence in swift easing later this year has evaporated. Looking at the Bloomberg WIRP (World Interest Rate Probabilities) function, which derives probabilities from the fed funds futures market, the implicit rate for the December Federal Open Market Committee meeting has never been higher since the start of the contract. Nearly at 5%, it suggests that there will be no rate cuts this year:

For those attempting to TRADE CPI, a large German shop offers,

Beyond today’s CPI is tomorrow’s ReSale TALES … and this from a large British operation,

US Retail Sales: Risks of another disappointing retail report Our credit cards data suggest a contraction in headline retail sales of 0.5%, accompanied by a similarly weak control group print. This would be another negative surprise relative to consensus forecasts, which look for robust gains in both categories.

Hawkish drift in central banks’ rhetoric last week has put the focus again on economic data.

US CPI report on Tuesday is the next key data on the agenda. We expect a solid print to highlight risks of inflation staying persistent.

An upward surprise would add momentum to the repricing in the short end of the yield curve, contributing to a further inversion of the 2y10y segment, in our view.

We see a scope for higher implied volatility in both the FX and the rate space.

With all the data / inputs ahead, question IS what will the Fed make of it all and FRBSF attempts to ask / ANSWER an important question being asked when thinking of OER,

Can Monetary Policy Tame Rent Inflation? Rent inflation has surged since early 2021. Because the cost of housing is an important component of total U.S. consumer spending, high rent inflation has contributed to elevated levels of overall inflation. Evidence suggests that, as monetary policy tightening cools housing markets, it can also reduce rent inflation, although this tends to adjust relatively slowly. A policy tightening equivalent to a 1 percentage point increase in the federal funds rate could reduce rent inflation as much as 3.2 percentage points over 2½ years.

Perhaps the Fed won’t HAVE to and perhaps we’re in a golden age of TRANSITORY GOLDILOCKS? 1stBOS latest,

The Goldilocks-like mix of industrial production (IP) recovery and falling inflation we expect this quarter has helped boost risk appetite and equities. Chinese reopening, one of the warmest winters on record, and improving global real incomes should support a recovery in industrial activity through May after a period of contraction that likely ended last month.

Risk appetite has rallied ahead of the IP bounce – as it frequently does. This quarter is likely to deliver one of the best mixes of lower inflation and rising IP in the last 50 years. Equities typically perform well during these ‘goldilocks’ periods.

However, this windfall is unlikely to persist into the summer and may stall even earlier. We expect IP momentum to drop back to below trend rates from June. The lagged impact of central bank tightening should keep global demand too weak to support a sustained upturn in activity, and a slowdown in inventory building is likely to drag.

Falling IP momentum and disinflation from Q2 should skew markets away from equities and in favor of bonds. Bonds reliably outperform when growth and inflation slow together.

From TRANSITORY to actual Goldilocks who opines on growth drag from SLOOS,

The Senior Loan Officer Opinion Survey (SLOOS) indicated that bank lending standards tightened further in 2022Q4. We have previously found that the SLOOS is an early indicator of investment growth, so the recent tightening to levels unseen outside of recessions could signal weaker growth later this year…

From transitory goldilocks back TO the writings from an ‘official’ account of sorts. FRB Chicago offering a warning on … MUNIS and (lack of) liquidity

Finally from BAML and is for those who follow CHARTS … Ciana asks,

US yields double bottomed, now what? Key takeaways > The market's reaction to strong US labor data, an ISM bounce back and a variety of Fed speak last week was net bearish USTs. > This reaction caused US yields to form double bottom patterns and to break above downward sloping trend lines beginning 4Q22. > We discuss tactically higher yield targets, weekly charts that lack big yield tops and a speculative triangle base in 5s30s.

… History says: Still no big top in 10Y yield. Snap back or retest common.

Today (at best) we see a two peaked yield / RSI divergence. History shows a three peaked divergence or a top pattern with a two peaked divergence is how yield tended to top. MACD did not confirm the current RSI divergence as it made a new high 4Q22. We continue to think yield can have a significant bounce back and then potential to form a big top pattern. In this scenario, a move back to or possibly above 4% would help to form a more typical technical top in line with history. A modest new high in 10Y yield can’t be ruled out either and would contribute to an RSI and MACD oscillator divergence formation.

Chart of the Day: Going into the key CPI report on Tuesday, US 10yr Bond Yields rebounded further towards the end of last week, in line with our view over the past two weeks (see here and here). The market is now very close to key support at the potential downtrend from the October 2022 high and 50% retracement of the October/January fall at 3.81/82%. Absent a big upside surprise in CPI tomorrow, we would look to increase duration exposure further around this level, in line with our structurally bullish view on US Fixed Income, with our core objective still at 3.00%. Failure to hold below 3.81/82% on an upside surprise would in contrast open up next support at 3.91%.

The firm reiterates staying tactically neutral prior to CPI BUT would turn bullish again on break back below 3.85% and also has gotten tactically bullish long bonds @ 3.85% support and above here, will be watching 4.00% (above and back TO the fence).

And there are many more charts which may be of some value … have at em and … THAT is all for now. Off to the day job…