Good morning and happy Monday (said nobody ever)! In light of the lack of economic fundamentals today and the most important data point this week being CPI on Thursday(calendars HERE), well I’ve not much to add to what little was noted over the weekend.

Treasuries are mixed with the curve pivoting steeper around a little-changed belly. DXY is little changed (+0.05%) while front WTI futures are -0.9%. Asian stocks were mixed/lower except in China (SHCOMP +2%) which returned from holiday today. EU and UK share markets are all close to home (save for Italy's FTSE MIB at -1.5%) while ES futures are showing -0.15% here at 6:45am. Our overnight US rates flows saw better real$ buying (mostly long-end) out of Asia along with fast$ buying as the curve flattened further. After the London crossover, long-end Treasuries underperformed on Buxl weakness and ahead of long-end supply over there. Overnight Treasury volume was solid (~215% of average) with nations returning from Lunar New Year.

And from same shop, some news and a chart, of the belly,

US News: An oil trading exec calls out 'worrisome' levels of global oil stocks and an 'alarming' level of OPEC+ spare capacity SPG One of the Big 3 auto makers suspended or cut output at 8 of its factories due to chip shortage RTRS Worker absence pressures from Omicron still linger for some employers WSJ US lawmakers signal stopgap spending bill as government funding is set to run out Feb 18th WSJ US inflation is probably about to spike again BBG US stock market liquidity 'abysmal,' adding to volatility risk RTRS US calls for 'concrete action' from China for Phase 1 purchase commitments RTRS El-Erian: The Fed and the ECB are still behind the inflation curve FT Citi's (Jason Williams) latest Treasury supply projections Citi

… Our next attachment this morning takes an updated look at the Treasury 2s5s10s 'fly and how the 24bp area has emerged as a formidable downside support. So the local range for 2s5s10s appears to be 24bp below up to ~40bp above- where we're close to mid-range this morning.

And for some more of the news you can use » IGMs Press Picks for today (07 FEB) to help weed thru the noise (some of which can be found over here at Finviz).

… When the dust settles we will soon move on to US CPI on Thursday. In terms of what to look out for, note that 8 of the last 10 CPI releases have seen the monthly headline figure come in above the consensus estimate on Bloomberg. Our US economists are projecting that monthly headline CPI growth will slow to +0.36% in January, with core inflation also slowing to +0.36%. However, this would still push YoY readings to 7.2% and 5.8% (consensus at 7.3% and 5.9%) respectively the highest since 1982 for both. There are plenty of wildcards in the release but we'll be watching rents/OER most as this makes up around 40% of core and around a third of the headline number. Since last summer it's been clear from our models that this was going to continue going up and up and given its weight it's very difficult for inflation to mean revert without it also doing so. It's showing no sign of this at the moment and likely won't for several months at least…

Since we’re on the topic of the ‘flation, here’s a hit from Pragmatic Capitalism bringing forward recent NYT story on MMT and what a glowing review it is(nt)

MMT Failed Its First Big Inflation Test Here’s a NY Times piece calling for a MMT “victory lap”, with an asterisk. It’s an interesting article, but the asterisk seems to be doing an awful lot of heavy lifting here. The basic gist of the article is that the government spent a lot of money and the government didn’t go broke. And sure, on the one hand, the economy is robust. On the other hand, inflation is worrisomely high. Depending on how you pick your narrative you can frame this as either very good or very bad. But does MMT deserve a “victory lap” or is the current economic experience a worrisome sign of how they’d handle a truly scary inflation? My view is the latter. I’ll explain why…

I’m with Cullen on this one — MMT no bueno — and this is why I am bringing this forward. To be fair, not ALL I see around the intertubes, are only things I agree with. I do respect them and to whit, this from Wolf Richter

… But for future bond buyers and for savers, a whole new world opens up: a world with more income. And this higher income will throw off more tax revenues for governments. So how much money are we talking about here? $67 trillion in assets that will generate higher incomes…

When you have a government who is unable to spend what it was on social services BECAUSE it’s spending MORE ON SERVICING DEBT, well, it’s terrific SAVERS can bank a few more shekels BUT … $30 TRILLION?

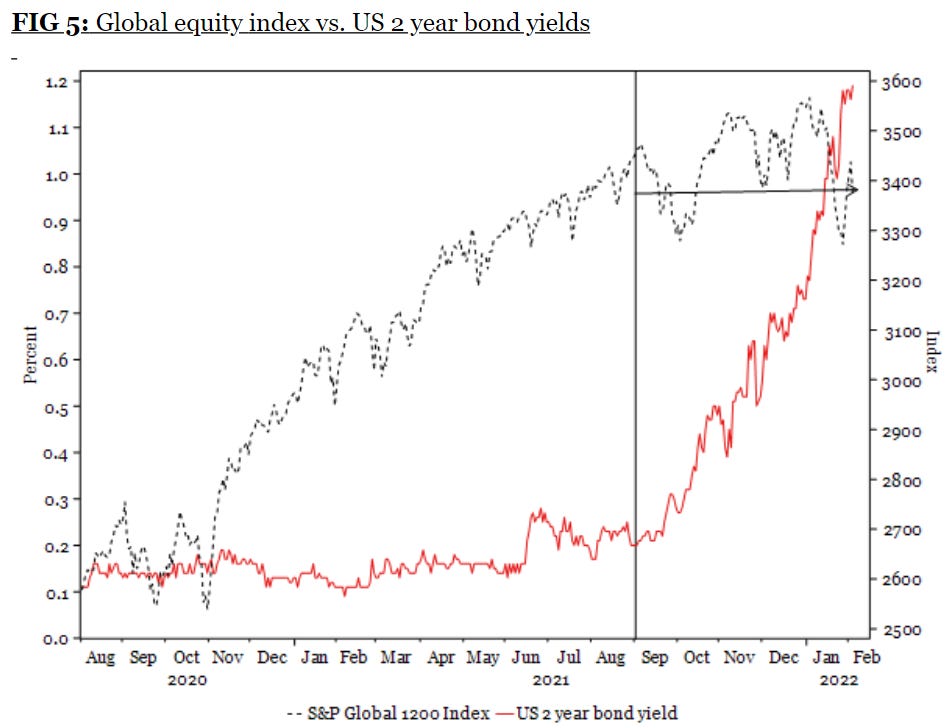

… For the visual learners out there like me, Authers latest (neg yielding debt, bunds, stocks and 2s and more)

Every Picture Is Telling a Story of Markets Regime Change … Many care about short-term bond yields because of their effect on equity prices. Over history, a rise in two-year yields as tightening by central banks grows likely is associated with a halt in gains for the stock market. That’s happening now, as this chart from London's Longview Economics makes clear:

Speaking of 2s, in the case you missed YESTERDAYwhen I noted specs RAISED 2yr UST BULLISH BETS …

In OTHER news, a couple things from the inbox and which some may find funtertaining … you’ll likely find this one on ZH at some point sooner or later,

MS: Punxsutawney Phil Says 6 more Weeks of Winter. Stay Defensive We continue to be more focused on what growth is going to do rather than rates and believe investors are still too optimistic, particularly as it relates to consumption. Exacerbating that risk is the fact that inventories are now rising rapidly. Maintain a Defensive Posture…

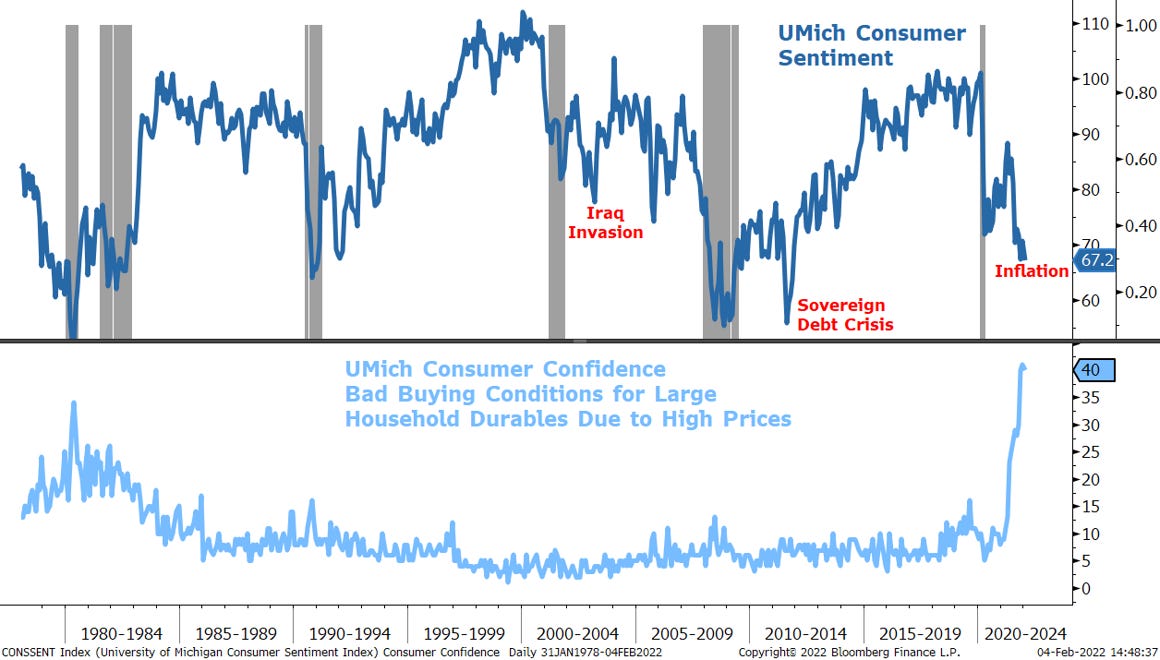

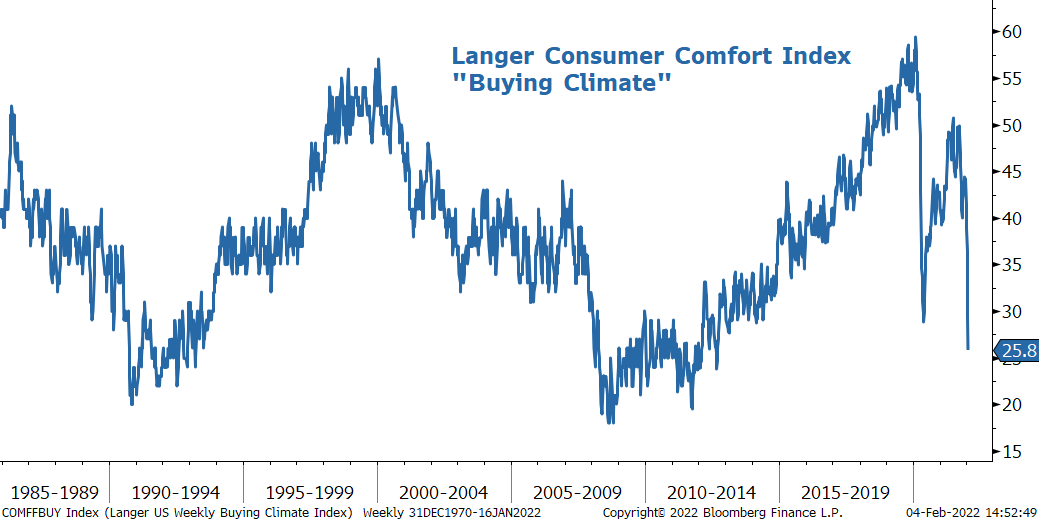

…In addition to the payback for last year's over consumption, there is growing evidence that the consumer may be in a weaker position to spend even if she wants to. Consumer confidence measures continue to remain in recession territory, mostly due to inflation that could start to be demand destructive, particularly for discretionary items (Exhibits 1 and 2). This is risk is acute for the lower income cohorts where inflation in necessities is eating into disposable income. Bottom line, we think the consumer spending is at risk and and it's not all due to Omicron. Instead, it is more a combination of government transfers running as prices rise to levels of demand destruction.

Exhibit 1: Consumer Confidence Remains Soft

Exhibit 2: Leaving Buying Appetite Very Low

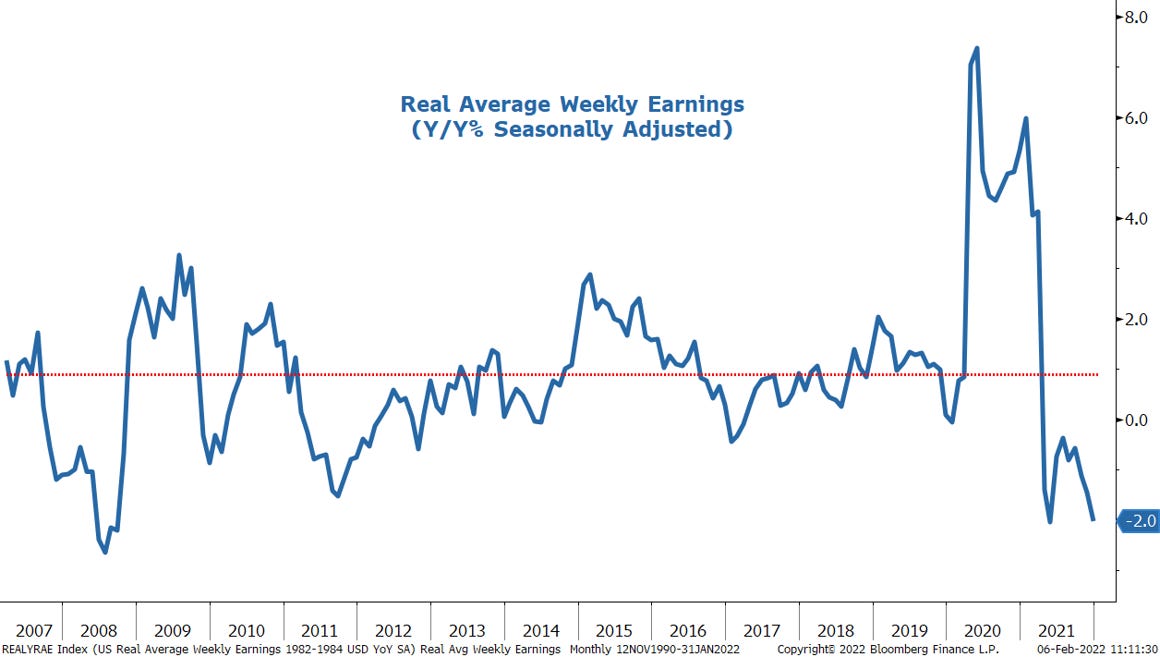

… While those increases can help to offset inflation for the consumer, they haven't been keeping up. Real wage growth is deep in negative territory (Exhibit 6). Not only is this the most negative real wages have been since the Great Financial Crisis but it's also in sharp contrast to where we were a year ago. In our view this simply increases the odds of consumption disappointing in the first half of the year even if Omicron proves to be the last major wave of this pandemic. In other words, we don't expect better supply of labor to alleviate the wage pressures on overall inflation metrics in the near term. Furthermore, these wage increases are unlikely to be big enough to alleviate consumers' concern about rising prices.

Exhibit 6: Wages are up nicely but it's not enough to keep the consumer ahead of inflation

… Perhaps most troubling and supportive of the narrative above is that expectations for rails were particularly bearish with the sharpest decline in volumes expectations in the 20+ year history of the survey (Exhibit 12). Bottom line, Winter is here and Punxsutawney Phil says we got at least 6 more weeks. We agree and think it could even bleed well into spring. Earnings risk is increasing for a wider swath of the market than most investors expect as rising inventories meet waning demand.

Exhibit 12: Morgan Stanley Freight Pulse Survey Expected Rail Volume Change Index

Having just returned from MA to drop some things for Thing 1’s travels abroad, this morning waking up to text that he’s just tested positive, well, now puts his travels and my health at risk.

Such is life in a panic-demic. OR as they say, another day in paradise! Just livin’ the dream, ‘Mater boy, livin’ the dream!! Hope y’all stayin safe!