Good morning / afternoon / evening (please choose … ah, forget it) … shortly AFTER hitting send earlier this morning — perhaps in some haste having to walk the dog, shovel, and feed some of the kiddos — I neglected to mention I will NOT be spamming the internet or your inbox tomorrow but rather, will resume regular spammation on Friday morning.

In any case, this was out on social media just ahead of the CPI data …

Donald J. Trump @realDonaldTrump

Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!! Lets Rock and Roll, America!!!

… this ‘truth’ released or ‘truthed’ (? strugglin’ here, help me out) a mere 32mins ahead of the CPI …

ZH: "Biden Inflation Up!" - Stocks Slump With Rate-Cut Hopes As CPI Soars In January

ZH: *TRADERS SHIFT NEXT FED RATE CUT TO DECEMBER FROM SEPTEMBER

ZH: "These Numbers Are Uncomfortable For The Fed": Wall Street Reacts To Today's Red Hot CPI

CalculatedRISK: BLS: CPI Increased 0.5% in January; Core CPI increased 0.4% CalculatedRISK: YoY Measures of Inflation: Services, Goods and Shelter CalculatedRISK: Cleveland Fed: Median CPI increased 0.3% and Trimmed-mean CPI increased 0.4% in January

… more from Global Wall below. Something you WONT see in Global Wall’s recaps is possibly THE worst news of all this … No, not price of oil, housing, apparel, travel or supercore but rather …

@M_McDonough

Wow! My Bacon, Egg & Cheese (With a Cup of Coffee) Price Index just saw its largest-ever monthly price jump in January, surging 6.1% (+18 cents)! Here are the details: (Chart from WSL POLITICS)

Dammit JOE!! Most expensive friggin bacon-ator ever!!?

On way in to NYC tomorrow gonna have to SKIP the bacon egg and cheese. I will NOT skip the morning coffee, though. Sorry. Not sorry. ‘Merica runs on Dunkin, they say …

Ok ok ok so the table then was set with a hot CPI for the afternoons 10yr auction … which will certainly go well with the early concession, right?

Will this roll to tomorrows 30yr auction? I’ve NO idea BUT a chart of my own (in addition TO the best in the techAmentalists biz noted HERE) …

30yy DAILY: back at 4.843 support (April ‘23 top and shoulders …) and IF a rally should materialize, 50dMA down near 4.73 would be an area of interest …

… and while momentum (stochastics, bottom panel) have adjusted and become far less overBOUGHT they are not yet overSOLD enough to be considered short term ‘rental’ … do what you want BUT keep your friends close and your stops closer?

I’ll move right along and again, outta pocket tomorrow so yer on yer own … get those 30yr auction bids in early and often …

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

All things CPI recapAthon related (where some nuance and shift of view is afoot)…

BARCAP: US CPI Inflation Monitor (January CPI): Not quite there yet

Core CPI inflation accelerated to 0.45% m/m SA in January, topping expectations amid increases across core goods and services categories. That said, we think the underlying details are not as bad as the aggregates suggest, and expect some relief in the February data.

BARCAP: US Economics Research: January CPI: Another upside surprise

Core CPI surprised to the upside yet again in the January print, rising 0.45% m/m, SA (3.3% y/y) amid an acceleration in both core goods and services prices. Headline inflation was also strong, at 0.47% m/m, SA (3.0% y/y). This translates to January core PCE inflation of 0.38% m/m (2.7% y/y).

…Putting this all in the context of monetary policy expectations, it delays our first cut assumption for 2025 until the September 17th meeting. We had been holding onto the potential for June, but this report has so many similarities to 1Q 2024 that assuming further reluctance to normalize will likely prove the more prudent approach. We’re viewing the futures market as underpricing the probability that the Fed resumes normalization in Q3 as the September meeting has just 17 bp of cuts priced in. To be fair, the Fed (and market) is going to require some time, and cooler inflation data, before ‘getting over’ today’s print. This dynamic is made all the more relevant in light of the fresh tariff regime that is currently being established and the inevitable flow-through to realized inflation…

Residual seasonality was likely at play in the January CPI report, but we think the data still showed underlying price pressures.

While the Fed is cognizant of the pattern of early-year inflation strength, the print will do little to ease policymakers’ inflation anxieties, particularly given the context of accelerating labor demand, increased inflation expectations, and incoming tariff effects.

We look for 0.39% m/m headline and 0.36% core PCE prints for January.

First Trust: The Consumer Price Index (CPI) Rose 0.5% in January

…No matter which way you cut it, inflation is still running above the Fed’s 2.0% target, and it is no longer improving. And yet, the Fed has cut rates a total of 100bps since September. Moving forward, we expect the Fed to remain on hold until inflation renews its long and winding march toward 2.0%, or the economy slows substantially.

US inflation came in well ahead of expectations, prompting the market to dramatically reprice the prospect of rate cuts. Potential tariffs add upside risk to inflation in coming quarters, but there are some encouraging signs that housing costs will slow meaningfully later in 2025 and keep the door open to the second half of the year cuts we are forecasting

It had been coming. A slow grind, but then a pop – US inflation is suddenly an issue again. Chair Powell says it's not. But it is, and Treasuries know it. Rate cut ambitions have been hit in consequence. Poor fiscal data for January doesn't help. In Europe, the spread between gilt and swap rates to see widening pressure under disappointing growth numbers

MS: US Inflation Monitor: January CPI: Temporary push confirmed

… As expected, the details of the report suggest acceleration due to wildfires (pushing used cars) and residual seasonality (pushing other goods and selected services). The CPI strength also implies a firm core PCE print, but less than the Jan-24 print. Consequently, we expect a step down in y/y core PCE rates in January and the rest of 1Q25 (see below for PCE details). This print is still consistent with our call of an extended Fed pause, with only one rate cut in 2025, happening in June…

…The main surprise was in core services, which came in above expectations at 0.51% m/m (vs 0.37% expected). Rents and OER came in consistent with our numbers, but car insurance and "other core services" including recreation services accelerated significantly. Overall, core services ex-housing came in significantly above our forecasts, at 0.77% (MS: 0.45%)..

RBC: Seasonality strikes again- January U.S. CPI moves up 0.5% month-over-month

The Bottom Line:

Core CPI’s upside surprise was another reflection of the “January effect”- seasonality strikes again! Even still, if the FOMC was not in a further easing mindset before, this morning’s data release will not incentivize them to move from the sidelines.

More importantly, today’s print was one of many upside surprises to the economic data in recent months- following two successive moves lower in the unemployment rate.

Our expectation is for the Fed to hold rates at 4.25% to 4.5% through the year, and January’s CPI numbers add to that conviction. At the January FOMC meeting, Chair Powell emphasized that the Fed remains data dependent. Still, he acknowledged we are in a “fatter tails” scenario where the odds of a shock to the economy are wider. It is still too premature for the impact of tariff announcements to show up in core goods, but we will be watching in the coming months. Over the longer-term, a structural shift will become more problematic- tighter labour market thanks to higher retirements and stringent immigration policies, which will exert upward pressure on wages.

While headline inflation is sitting at 3.0%, it still feels like 3.2% for lower income households. This disparity will continue to be an important story in a higher-rate environment, as lower-income earners become more dependent on debt to sustain spending. The $40.8 billion increase in consumer credit outstanding in December (the largest month-over-month increase in season history) could be a growing sign of higher prices weighing on lower-income consumers.

We expect next month’s February release to show a smaller increase for both headline and core CPI. Currently we project the headline CPI to increase around 15bp (seasonally adjusted; +37bp NSA) and the core CPI to increase also around 22bp (seasonally adjusted).

12-month headline CPI inflation is projected to slip to 2.8% next month and core CPI inflation is projected to edge down to 3.1% in February. Both headline and core CPI inflation are projected to slow further in March.

We will review these forecasts as we go through the details of today’s release and additional relevant data come in.

WELLS FARGO: Hot January CPI Sends a Chill Over the Inflation Outlook

Summary Expectations of seeing further modest improvement in inflation at the start of this year were dashed by the January Consumer Price Index. The headline CPI rose 0.5% last month, well ahead of consensus expectations for a 0.3% increase. The upside surprise to the core index was more modest (0.4% versus expectations for a 0.3% increase), but illustrated broad-based strength in pricing at the start of the year. Core goods prices rose 0.3% and are now little changed over the past year as the deflationary tailwinds of improving supply chains have petered out. Core services prices rose 0.5% amid a 0.4% rise in shelter costs and strength in non-housing services like transportation and recreation.

The upside surprise is reminiscent of last January's CPI report and suggests even the updated seasonal factors released in today's report are still struggling to capture early year price increases after the pandemic-period scrambled the typical calendar year pattern of price changes. That said, both the year-over-year rates of the headline and core CPI indices rose over the month. Therefore, setting aside any issues over residual seasonality, today's report offers more evidence of progress in lowering inflation stalling out.

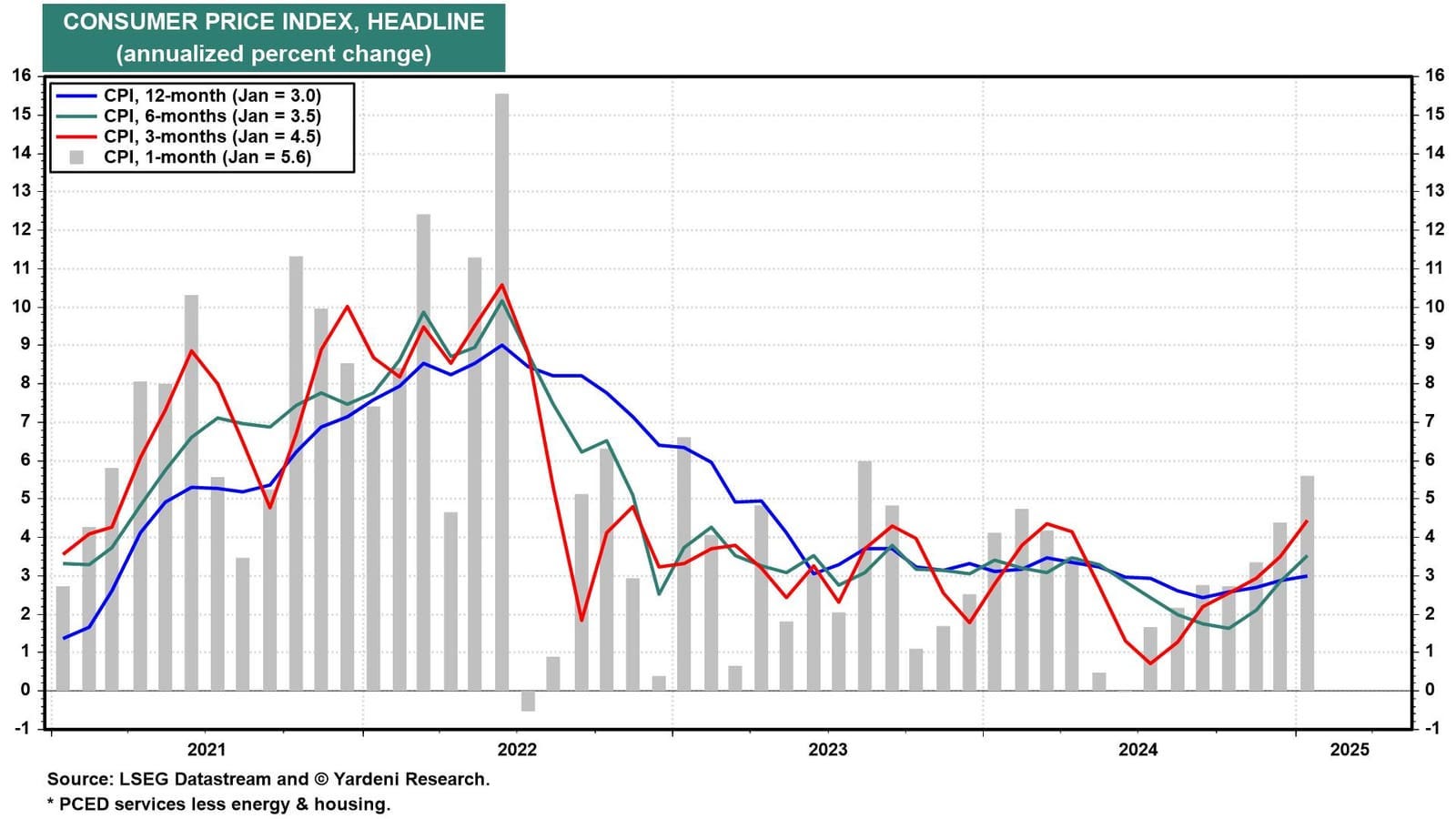

Yardeni: Fed Rate Cuts On Ice As Inflation Heats Up

Today's hotter-than-expected January CPI inflation did some damage to bonds, raising long-term Treasury yields roughly 10bps. Headline and core CPI rose 0.5% and 0.4% m/m, respectively, as many companies set their annual price increases. But this wasn't a start-of-the-year blip; inflation has been rising since last summer (chart). So after 100bps of federal funds rate (FFR) cuts from September 18 through December 18 last year, the Fed's easing cycle is on pause for the remainder of the year, as we've been predicting.

But a side effect of Trump 2.0 is that Fed-related economic data, like inflation and labor market news, are not the only headlines which move markets. President Trump said that Russia agreed to begin negotiations "immediately" to end the war in Ukraine, helping give stocks a lift and leaving them mostly unchanged on the day.

Crude oil prices fell around 2.5% today on that news…

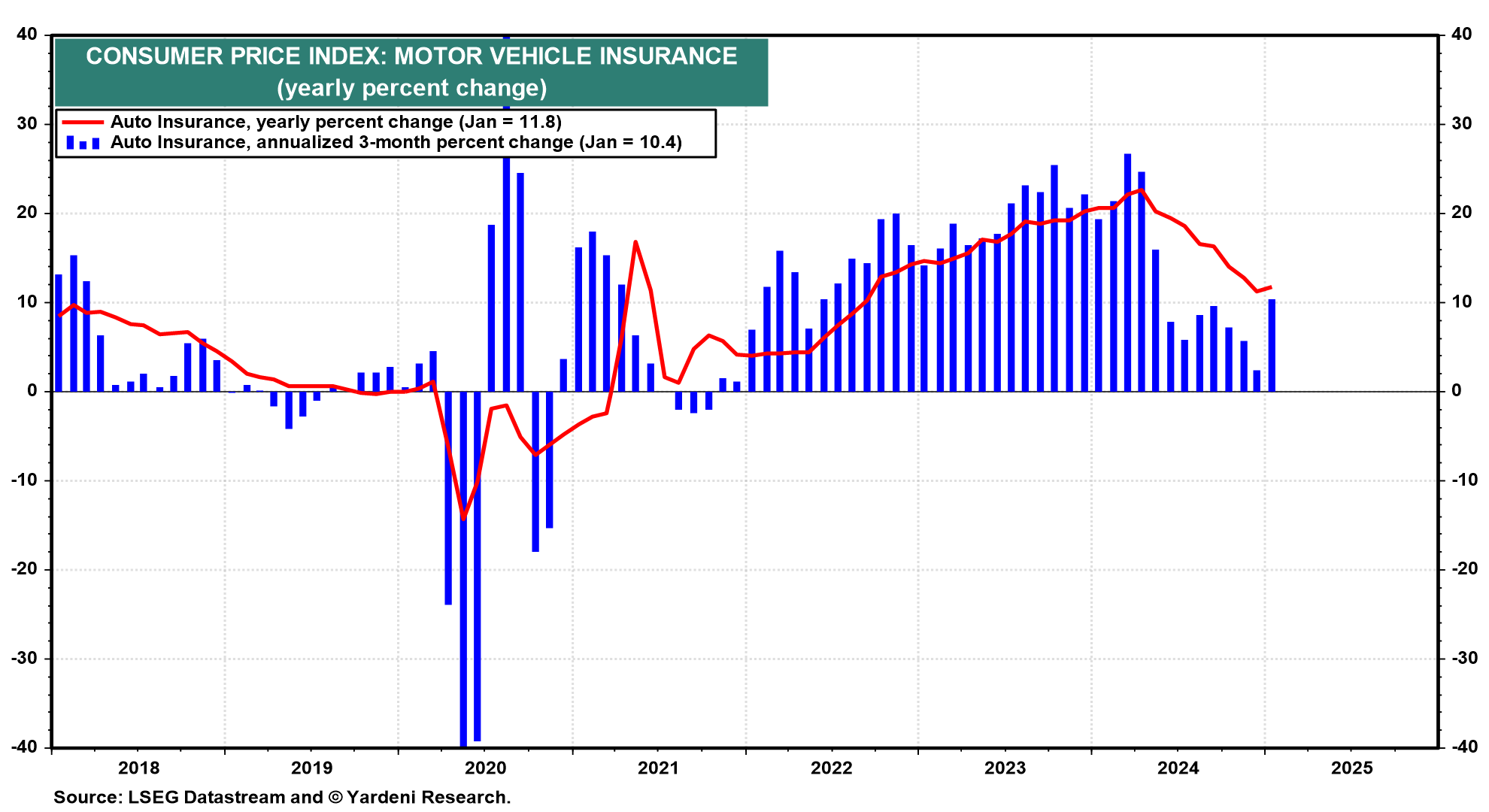

…One culprit of supercore's jump was auto insurance, which rose 2.2% m/m and 11.8% y/y (chart).

We expect disinflation to resume next month. But there are only so many categories that can be stripped out before one misses the forest for the trees. For instance, the rate-cut camp has pointed to expectations for shelter CPI inflation to fall. But shelter prices were up 0.4% m/m last month, accounting for nearly 30% of the total increase in headline CPI.

Another legitimate concern is that goods inflation is rebounding while progress on services inflation has stalled

AND a few other items of note (which ultimately all relate back TO CPI) … changing of calls (BMO above and UBS below) do catch ones attention …

DB: Fed Notes - Could the Fed's patience wear thin?

In our November 2025 outlook report (see “Trump II: Growth too fast, inflation too furious for Fed cuts”), we outlined a base case that the Fed would keep rates steady this year. Recent developments on the data and policy fronts have reinforced that view. We discuss the Fed outlook, including whether rate hikes could come into view, in the context of these developments.

Last week Treasury Secretary Bessent made waves as he declared that the Trump administration is focused on bringing down the 10y Treasury yield. In the days since, 10y UST is up nearly 10bps, making it clear that declarations about lower rates alone will not bring them down. In this note we discuss steps the administration could take to achieve their objective of lower long-term bond yields. There are two main messages: (1) lowering the fiscal deficit is the clearest and most impactful lever the administration has to lower yields, and (2) this and other measures that could be considered entail important trade-offs with other goals and policies.

Rebound in US CPI; USTs sell off as market-implied cuts recede; EUR outperforms as risk sentiment is boosted; Central Europe currencies gain amid Russia-Ukraine developments; JGBs bear-steepen; swap spreads widen after Powell's comments on SLR; DXY at 107.98 (0.0%); US 10y at 4.621% (+8.6bp)

Another rate call change: normalization stalling for longer The upside surprise in today's CPI should fuel the sticky inflation narrative, even if the impact on the PCE deflator turns out to be more modest than the CPI surprise might suggest. We will know more after the PPI release tomorrow, but fighting upstream, with rising tariff risks potentially hamstringing the central bank, we are going to change our baseline expectation for rate cuts this year. We now do not expect a rate cut until the September FOMC meeting. Normalization it seems, may be stalled for longer than we previously expected.

We still expect to make progress lower on the year-over-year rates of core PCE inflation. We also expect the current backdrop of over 4% annualized consumption growth and a 3-month moving average of gains in nonfarm payroll employment of 237K likely gives way to something slower as we move through the middle of the year, not unlike what unfolded last year. To be fair, in his testimony yesterday, Chair Powell skipped the typical 3-month moving average reference and cited the 4-month moving average of 189K per month, still brisk, and we would argue supported by some residual seasonality.

However, the rolling risk of tariffs, including the China tariffs now in place plus the steel, aluminum tariffs that are set to go into effect in March, and the results of the trade imbalance review, directionally will keep that risk in front of some FOMC participants, even if Chair Powell seems to argue for being cautious about making assumptions before seeing the impact of what trade policy looks like in the data.

What seems underappreciated is how much the growth and inflation trade-off may be worsening as rate calls change. Market attention appears to be focused on inflation with the backdrop of strong growth, and the combination of strong growth and sticky inflation keeping the FOMC on hold. Indeed,the FOMC seems to see it that way. The labor market looks strong, and consumption has been strong, so why not wait? The strength in the economy has afforded the FOMC the luxury of being able to wait. However, that growth and inflation trade-off may be worse than appears. In the calculations and simulations we run, tariffs come at a cost, and many of our estimates under many scenarios typically see a larger drag in domestic growth than there is an inflationary impact. An FOMC staying on pause while they wait to assess the impact of tariffs, or any knock on effect on inflation expectations, seems unlikely to be growth positive either. Right now staying on hold because the economy looks resilient may seem obvious, but the tariffs, high rate rates for longer, and potentially overestimating the current degree of strength in the expansion imply rising downside risks ahead that may be underappreciated.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

These from the Bloomberg Markets Live group (and Simon White) ahead of the CPI print, via …

Annual inflation accelerated up to 3.0% in January from 2.9% in the previous reading.

Shelter costs rose 0.4% in January, accounting for nearly a third of the headline increase.

Energy prices rose 1.1% over the month from the rise in gas prices.

Bird flu was a major factor in hotter food inflation, causing egg prices to rise 15.2%, the largest increase in roughly a decade and pushing annual prices up 53%.

Large numbers of underinsured and uninsured drivers have impacted the auto insurance market. The motor vehicle insurance index rose 2.0% in January with little signs of easing.

The demand for travel placed upside pressure on travel costs, including airfares, hotel prices, and rental vehicles. The number of travelers passing through TSA checkpoints in January was higher than January 2019 by about 200 million.

…Fed Will Likely Wait Until Summer to Cut Rates

WOLFST: Beneath the Skin of CPI Inflation: Worst Month-to-Month Acceleration of CPI since Aug 2023, on Spikes in Used Vehicles, Non-Housing Services, Food

Inflation has been going in the wrong direction relentlessly month-to-month since June.

AND … i’m done. Out for now back to spammation ahead of Friday’s ReSale TALES and … THAT is all for now. Off to the day job…