10yy DAILY: 4.55% is a point of interest, to me … rising TLINE …

… momentum on daily basis remains BEARISH, a concession for today’s auction would be welcomed but a break back above TLINE today on into the weekend would be more concerning … 50dMA (blue) just north of … you guessed it … 4.50% … I remain concerned on the shorter-term DAILY basis but being short entirely different proposition so continue to WATCH in / around 4.50% …

That said, one can only HOPE today’s 10yr auction goes as well as yesterdays “stellar” 3yr did …

ZH: Stellar 3Y Auction Sees Bid To Cover Spike, Record Low Dealers, First Stop Through Since Sept

… This ‘stellar’ auction a result of the message JPOW delivered in the morning (?) …

CNBC: Fed Chair Powell says central bank doesn’t ‘need to be in a hurry’ to lower interest rates further

…“With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance,” Powell said. “We know that reducing policy restraint too fast or too much could hinder progress on inflation. At the same time, reducing policy restraint too slowly or too little could unduly weaken economic activity and employment.” …

AND then as day ended and ALL this was priced in …

As everyone and their pet rabbit hold their breath for tomorrow's CPI print, today saw small business optimism droop from multi-year highs, economic uncertainty jump, and CapEx expectations tumble.

Add to that Fed Chair Powell offering little new information during his 'Humphrey-Hawkins' testimony - reafffirming that the fed funds rate was "significantly less restrictive than it had been" and reiterated that the FOMC did "not need to be in a hurry to adjust our policy stance."

Additionally, Chair Powell tamped down Democrats' "tariff-tax threat" fearmongering, reiterating that “it would be unwise to speculate” on the economic impact of the new administration’s trade policies. Powell noted that it “remains to be seen what tariff policies are implemented,” and later stressed that their impact on the economy would “depend very much on specific facts about what’s being tariffed, for how long, etc.” He also reminded the Senate Committee that the FOMC “wound up cutting rates” in 2019.

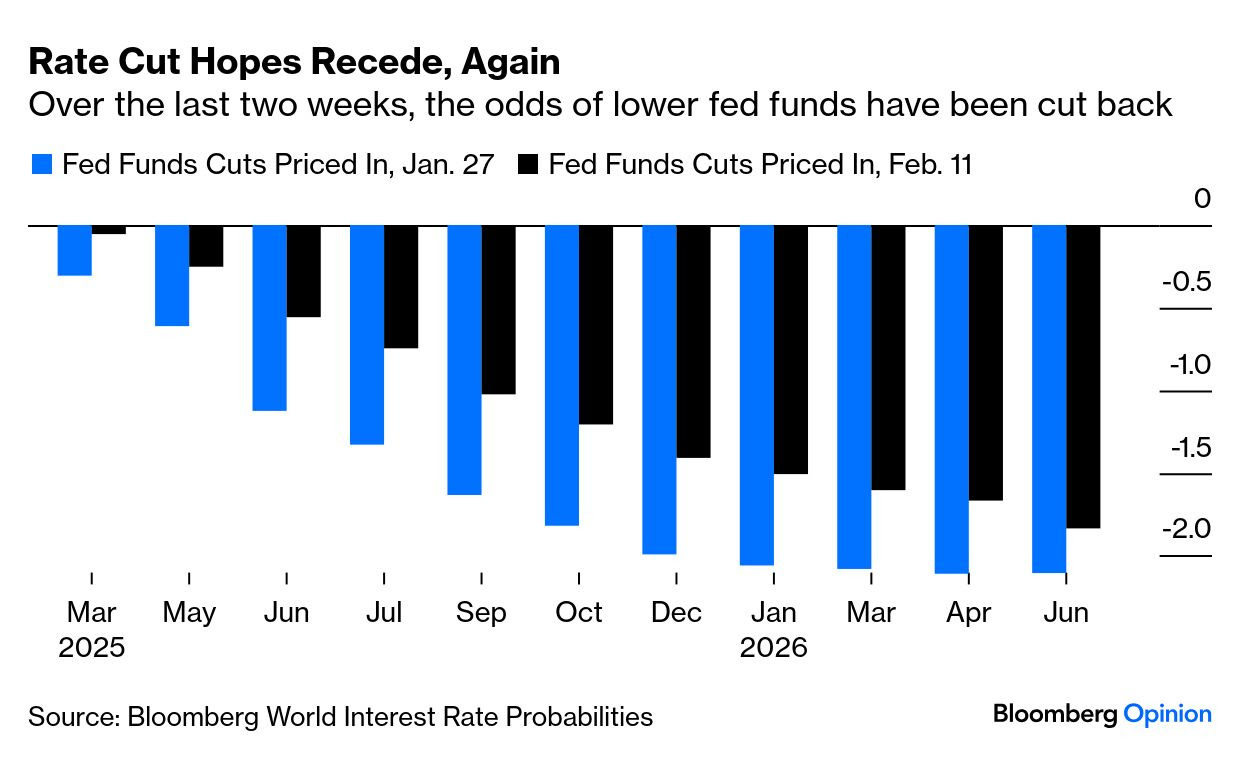

On the day, rate-cut odds fell once again, back to their lowest in almost a month (36bps price in by year-end, so one cut plus a 50-50 chance of a second cut)...

Source: Bloomberg

And thanks to relatively low liquidity in stonks, the chaos monkeys were back again today as stocks ramped higher at the US cash open from accelerating overnight weakness, managed to get green right before the European close and then puked back down, only for all the majors except Small Caps to ramp back up to the highs of the day…

I’ve nothing to add AND I gotta go shovel, walk dog and make sure everyone fed ahead of school so … here is a snapshot OF USTs as of 625a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

Yield HuntingDaily Note | February 11, 2025 | JFR Rights, Investment Grade CEFs, JHS A Buy

PiQ Overnight News Roundup

Opening Bell Daily: Inflation isn't budging. Fed Powell doesn't have much to say because inflation won't budge. January CPI is seen holding steady as the central bank chief testifies before lawmakers…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … lots of FOMC recaps and victory laps …

Here are some updated thoughts / visuals from the very best techAmentalists out there … They offer more but I’ll limit my attention TO today’s and tomorrows issues up for auction … interesting to note a definite change of tone (from bullish to bearish)…

CitiFX Techs: US rates: Daily indicators don't change the broader picture

Following NFP, some daily indicators in US rates suggested we could be in for higher yields in the short term. In the medium term, however, the picture remains largely unchanged. A break of support in 2s10s suggest that we are still likely to see a flattening bias…

…US 10y yields A number of notable updates. We posted a morning star formation in the daily chart last week. However, we still closed below the 4.50% level on a weekly basis.

Overall, we think the picture is slightly different now for 10y yields. Short term, we would not be surprised to see yields higher towards 4.60% (Feb 4 high).

In the longer term, the head and shoulders formation we flagged last week is in play. This is an indicator of lower yields and would suggest a target of ~4.24%. That would be very near the next layer of support at 4.25%-4.27% (55w MA, 200d MA). Weekly slow stochastics, which is crossing lower from 'overbought' territory, also supports the case for lower yields in the longer term.

Source: Citi, Bloomberg

US 30y yields We did not close below the 4.68-4.70% (55d MA, November high) on a weekly basis last week. Instead, we posted a daily morning star formation suggesting a short term bias for higher yields. We see resistance at 4.83% (Jan 31 high).

Longer term, however, we keep an eye out for a weekly break below 4.68-4.70%. If seen, this would suggest room for a move lower towards 4.46-4.47% (55w MA, 200d MA), alongside with weekly momentum crossing from 'overbought' territory.

From rates techAmentals back TO the comments by JPOW …

…Talking of 2026, markets have been getting slightly more concerned in recent days as to where inflation will be next year. We'll know a little more about the near term direction of travel today with US CPI out later. Ahead of that bonds have continued to sell off from their 2025 yield lows seen last week. There were a few catalysts yesterday but comments from Fed Chair Powell, who said that “we do not need to be in a hurry to adjust our policy stance” were a factor even if that's what we expected him to say. But on top of that, a fresh rise in energy prices and the prospect of retaliatory tariffs from the EU led to anxiety that inflation would keep lingering above target for some time. Indeed, the US 2yr inflation swap (+4.2bps) closed at its highest in nearly two years, at 2.796%.

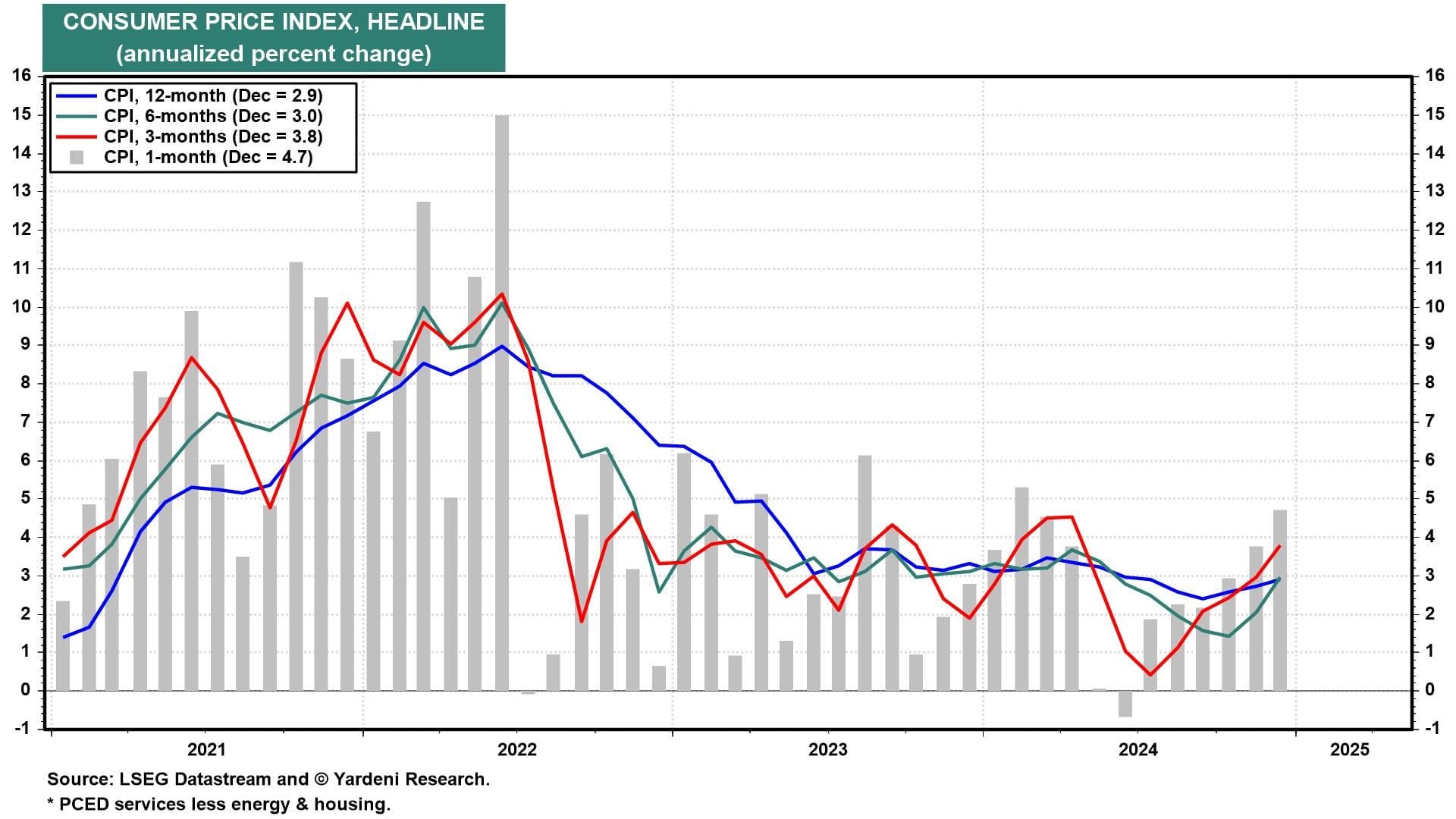

This backdrop makes it an interesting day to get the US CPI print for January, which will offer the first big clue on inflation in 2025. Today’s report is getting a decent amount of attention, in part because last January’s report saw a strong upside surprise, so the fear is we could get another new year uptick that upsets market expectations for the Fed to still cut this year. That’s particularly the case because recent data has leant in a more hawkish direction, with the 3m annualised rate of CPI already running at +3.9% in December, whilst the 6m rate was at +3.0%.

In terms of what to expect, our US economists are looking for monthly headline CPI at +0.31%, which would keep the year-on-year rate at +2.9%. Then for core CPI, they’re looking for a monthly +0.28% print, with the year-on-year rate ticking down a tenth to +3.1%. The other key thing to look out for will be the annual revisions to the seasonal adjustment factors, which could affect the last 5 years of data. Last year the revisions didn’t change the picture much at all, but two years ago they showed that inflation wasn’t slowing as rapidly as we thought, so that shifted attitudes in a more hawkish direction. For more details, see our US economists’ full preview here and how to sign up for their immediate reaction webinar.

Ahead of that, the main story yesterday came from Fed Chair Powell, who was delivering his semiannual testimony before the Senate Banking Committee. As discussed above, his main comment was that the Fed didn’t need to be in a hurry, and he also said that if “ the economy remains strong and inflation does not continue to move sustainably toward 2 percent, we can maintain policy restraint for longer.” Otherwise, there wasn’t too much in the way of headlines. Note that Powell speaks before the House Financial Services Commitee today in the second of his semi-annual double bill in Congress. Normally the second act doesn't get as many headlines but there's a chance today's CPI may solicit a slightly different tone or encourage different questions. All depends on where the release is relative to expectations…

AND then there’s this somewhat more bearish view … or is a bullish one?

ING Rates Spark: Chair Powell's juggle smells like higher yields

Chair Powell is minded to cut rates, but not yet. He was balanced, but markets continue to shave the extent of expected cuts. Significant supply pressures are also pushing Euro rates up. Meanwhile, Dutch pension reforms are awaiting clarity about potential legal changes from politicians, which could have a material swap market impact

ING: US Fed remains inclined to cut rates, but is in no hurry

After 100bp of rate cuts, Fed Chair Powell suggests policy remains restrictive – even if inflation remains elevated they will merely “maintain” policy restraint for longer. This indicates an inclination to cut rates closer to neutral, but no change is likely before June

Chair Powell's testimony offers little new information; USTs bear-steepen after strong 3y auction; EUR strengthens alongside local equity outperformance; large beat in Hungary CPI; BoE's Mann explains her vote for a 50bp cut; India rates outperform; DXY at 107.91 (-0.4%); US 10y at 4.535% (+3.8bp)

Chair Powell stayed on message in the first round of the February semi-annual monetary policy testimony hearings, and, assuming the January CPI report comes close to expectations on Wednesday (see our preview here), we don’t expect he will break new ground in his follow-up House appearance on Wednesday morning. Today’s testimony was thoroughly consistent with the January FOMC meeting, so it did not change the policy outlook at all in our view. Our base case continues to be that the Fed will take a "long" pause (with just two quarter-point rate cuts in June and September), but the risks around that baseline (in light of the January jobs report, see link), could be for an even longer delay.

The key points that he reiterated include and were virtually identical to his prepared remarks he discussed at his January 29th FOMC presser (see link):

"[E]conomic activity has continued to expand at a solid pace."

"[L]abor market conditions remain solid and appear to have stabilized. Payroll job gains averaged 189,000 per month over the past four months. Following earlier increases, the unemployment rate has been steady since the middle of last year and, at 4 percent in January, remains low."

"Inflation has eased significantly over the past two years but remains somewhat elevated relative to our 2 percent longer-run goal."

"With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance [our emphasis added.]. We know that reducing policy restraint too fast or too much could hinder progress on inflation. At the same time, reducing policy restraint too slowly or too little could unduly weaken economic activity and employment. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the FOMC will assess incoming data, the evolving outlook, and the balance of risks."

"As the economy evolves, we will adjust our policy stance in a manner that best promotes our maximum-employment and price-stability goals. If the economy remains strong and inflation does not continue to move sustainably toward 2 percent, we can maintain policy restraint for longer. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we can ease policy accordingly. We are attentive to the risks to both sides of our dual mandate, and policy is well positioned to deal with the risks."

In Q&A, Chair Powell dodged several questions from various senators eager to elicit Powell's views about the Presidents recent actions on tariffs.

A couple notes from Switzerland … on CPI, JPOW and 3% spending growth forever …

US January consumer price inflation will be largely unaffected by US President Trump’s trade taxes (though prices are occasionally raised in anticipation of tariffs). Unless tax increases are very aggressive, nothing Trump does will have a bearing on first quarter inflation. However, the composition of consumer prices is politically important.

Food prices merit attention. They are not just egg prices—neither Trump nor Federal Reserve Chair Powell can influence those. Food prices are, however, a very visible form of inflation. If food prices move higher, this may restrain trade taxes on imports from Canada and Mexico (which export food to the US). Taxing Mexican imports directly raises the US price of avocado on toast, which would agitate Gen Z. The composition of inflation may influence which areas of the US incur the burden of trade taxes.

Powell testified to the Senate yesterday, and speaks to the House today. Their remarks stressed no urgency in cutting rates—market expectations are being buffeted by volatile trade tax expectations anyway. Powell did take questions on Fed independence—an important condition for the US dollar’s reserve role, which depends on rule of law being observed…

His prepared remarks reproduced language from the December and January FOMC meetings. The Chair noted that concern about the labor market has diminished significantly since late summer and in Q&A said "the labor market is very strong."He similarly repeated the prior observation about inflation, "inflation has moved much closer to our two percent goal though it remains somewhat elevated." And, as we expected, with the economic wind in their sails, he said "we do not need to be in a hurry to adjust our policy stance."

"If the economy remains strong and inflation does not continue to move sustainably toward 2 percent, we can maintain policy restraint for longer. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we can ease policy accordingly. We are attentive to the risks to both sides of our dual mandate, and policy is well positioned to deal with the risks and uncertainties that we face." -Chair Powell

With the GDP release in hand, real personal consumption expenditures expanded 3.2% over the four quarters of 2024, after 3.0% growth in 2023. We were above consensus in our expectations for Q4 spending and still the 4.2% (saar) increase outpaced us and every other forecaster on Bloomberg. Can this pace be sustained?

Softer Q1s typically follow strong Q4s..

Strong incomes, dis-saving and stronger credit growth supported spending…

Some of these tides may turn though Still elevated interest rates, slowing wage growth, and less boost to real income from disinflation, imply to us that real spending should slow from the brisk pace of late. Rising delinquency rates on auto and credit card balances suggest rising shares of households under pressure. While in the aggregate, household balance sheets look good, that masks an unequal distribution, suggesting an increasing share of households should be fitting their spending within their incomes. Then, the headwind of tariffs on China and potentially other countries and sectors could restrain consumption growth too. While our real consumption growth estimate of 2.0% in 2025 is not all that bad, slowing reflects loss of support and still restrictive interest rates.

US consumers continue to confound expectations. Real consumer spending rose 4.2% (saar) in Q4 supported by strong goods spending, 6.6% (saar), and an acceleration in services spending too, 3.1% (saar) from the 2.8% (saar) pace in Q3. Can this pace be sustained? We think not, but our expectations for real consumption growth of 2.0% in 2025 is also not suggesting significant weakness to come.

Interrupting JPOW and HH testimony and recapAthon for a read of small biz…

WELLS FARGO: Small Business Optimism Falls Back Slightly in January Labor Demand Stable Amid Brighter Economic Outlooks

Summary Small Business Sentiment Weakens, but Still Improved Post Election The NFIB Small Business Optimism Index dipped 2.3 points in January following surges in November and December. Despite the setback, the index remains far above its prevailing level over the past three years. Most of the recent improvement, which coincided with the 2024 election outcome, was driven by the “softer” index components surrounding economic expectations and credit conditions. The “hard” components of the index, e.g. job creation plans, job openings and capex plans, remain muted compared to pre-pandemic norms. On the upside, labor market deterioration appears to have stalled amid a sideways movement in job openings and slight improvement in hiring plans. On the downside, small businesses are experiencing little relief on the inflation front. Owners also expressed a pickup in general uncertainty, possibly driven by recent volatility in tariff announcements.

Federal Reserve Chair Jerome Powell's congressional testimony today confirmed that the Fed remains in a dovish pause mode. The FOMC is in no hurry to lower the federal funds rate (FFR). That's even though many of the committee's participants believe that the FFR remains relatively restrictive. So when they finally move again, it will most likely be to lower rather than to raise the FFR. That's the Fed's current message. Tomorrow's January CPI isn't likely to change it anytime soon.

The possibility that annual price resets might boost monthly consumer inflation is widely known. So a cooler headline CPI—something below 0.3% and closer to 0.2% m/m—could boost stock and bond prices. But that doesn't mean it would change the FOMC's posture, especially with so much uncertainty regarding the eventual impact of tariffs on inflation.

Headline CPI has been warming up since mid-2024 (chart). That's in part due to rising energy prices, which have recently stopped climbing. However, it's also notable that inflation tended to pick up in Q1 of each of the last two years. So even a cooler-than-expected January number does not mean CPI inflation will remain cool in February as well.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Starting off with a look at POSITIONS via EBB ..

BLOOMBERG: Traders Betting Big on Higher US Yields Face Crucial CPI Data

Jobs data spurs gains in open interest, signaling new shorts

CPI will provide first test for newly established positions

…In the cash market, Tuesday’s release of JPMorgan’s Treasury client survey showed a move closer to neutral in the week leading up to Feb. 10, with reductions seen in both long and short positions.

Here’s a rundown of the latest positioning indicators across the rates market:

JPMorgan Treasury Client Survey In the week up to Feb. 10, the largest shift was seen in short positions, where a 6 percentage-point drop was seen as invested turned more neutral. Long positions also declined on the week by 1 percentage point.

…Powell Plays a Straight Bat The biannual joust between congressional committees and the chair of the Federal Reserve is a time-honored US tradition. For the latest one, a cricketing analogy is in order. Jerome Powell played a straight bat, and he was not out at the end. For aficionados of other sports, he played ultra-conservatively, giving up any chance of hitting the ball out of the park, but making his defenses close to impregnable.

While senators made political points, Powell did nothing to conflict with the new administration, and said very little about future monetary policy. The consumer price inflation data for January, due shortly after this newsletter is published, will cast rather more light. His most newsworthy utterance was that “we do not need to be in a hurry to adjust our policy stance.” That brought 10-year Treasury yields back above 4.5%.

The last two weeks have seen a sharp retreat in expectations for rate cuts, after fed funds futures briefly priced in more monetary easing in response to the DeepSeek shock. The market still believes there will be one rate cut of 25 basis points this year, now most likely in September. A second cut at some point is also probable, but no longer a given:

Ahead of inflation, the only significant new economic data for Tuesday came from the National Federation of Independent Business’ regular survey of small companies. The proportion of respondents finding it hard to fill vacancies, a sign of a potentially inflationary tight labor market, has stabilized below the extreme reached in 2022 but remains elevated by historical standards. That would appear to mean rates will have to stay where they are:

Now to see what curveballs (or googlies or leg-breaks, to return to the cricketing analogy) the inflation numbers will have for Powell.

Jimmy P weighs on on valuations (not good trading tool but certainly good at helping sniff out inflection points) …

Paulsen Perspective: Valuation Concentration? The transformational upward shift in U.S. stock market valuations appears to be broad-based across nearly “all” parts of the stock market.

Valuation metrics for the stock market have been a conundrum for the last several decades. As demonstrated in chart 1, the valuation range of the U.S. stock market has gone through a considerable transformation since the middle-1990s, leaving a number of critical questions in its wake.

Chart 1 shows the famed Shiller CAPE Price-Earnings (PE) multiple for the U.S. stock market since 1900. Between 1900 to about 1994, PE valuations exhibited a very consistent range between about 7 to 21 times earnings. For nearly 100 years, it was possible to judge how cheap or expensive the stock market was by comparing its current valuation to this tried-and-true persistent range. Generations of investors learned that single-digit PE markets were a bargain and any market PE approaching 20 warranted caution.

A few words (and visuals) from the Wolf …

WOLFST: Treasury Market’s Inflation Expectations Become “Unanchored”

Why the Fed vigorously backpedaled on further rate cuts and pivoted to wait-and-see: Long-term interest rates matter.

…It’s the bond market talking here, and the bond market is getting worried again about inflation.

The 5-year breakeven inflation rate rose to 2.64% today, the highest since March 2023, having shot up by 78 basis points since just before the Fed’s September rate cut. This measure (5-year Treasury yield minus the 5-year Treasury Inflation Indexed Real Yield) shows what the bond market saw today as the average inflation rate over the next five years.

The Fed has cut by 100 basis points, while this measure of market-based inflation expectations for average inflation over the next five years has shot up by 78 basis points. It has become “unanchored,” as one might say to needle Powell during the FOMC press conference:

Finally, a couple from ZH …

ZH: Small Business Optimism Slides In Jan As 'Uncertainty' Surges

Having surged (by the most on record) to its highest level since 2018 after Trump's election victory, Small Business Optimism faded in January as 'uncertainty' soared higher (by the most on record, data back to 1986)...

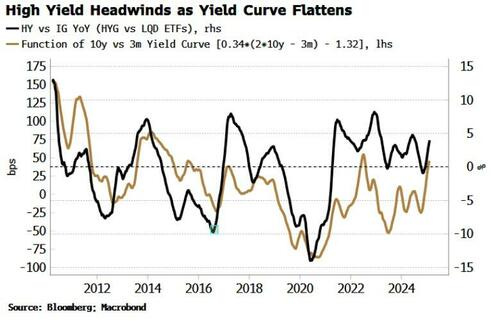

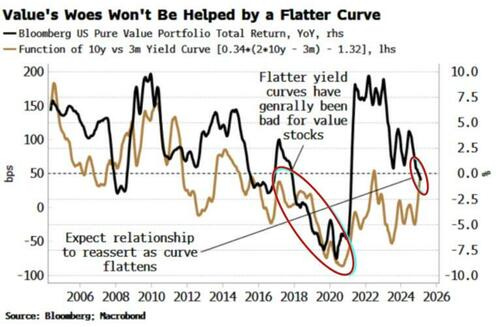

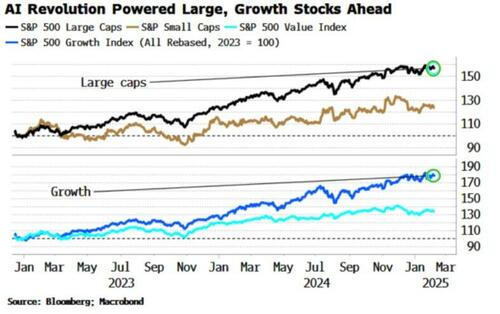

ZH: Who Benefits Most From The 'Bessent Curve Trade'

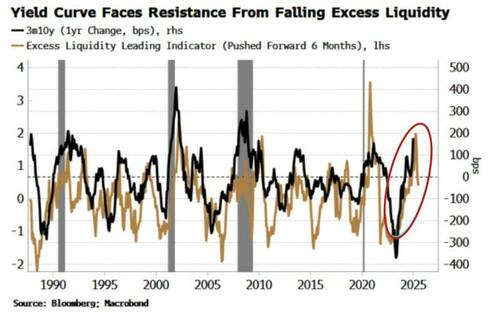

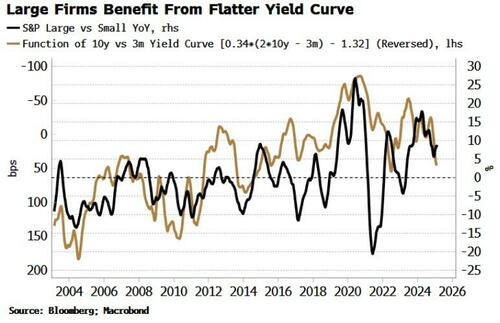

Larger, growth-like stocks are set to outperform smaller, value firms as the yield curve faces flattening pressure from falling liquidity. That trend will be underwritten by policy if Treasury Secretary Scott Bessent’s desire for lower longer-term yields is realized.

As a former hedge-fund manager, the Treasury Secretary is probably more intimately familiar with the yield curve than most of his predecessors. But now rather than directly trading it, he is hoping to influence it. Bending the bond market to his will might prove tricky, but the ultimate winners are likely to be larger, higher-rated growth stocks, leaving those of smaller, value firms to lag further behind.

Bessent has attempted to shift the attention of President Trump’s administration away from the Federal Reserve and instead bring focus to lowering longer-term yields, a de facto curve flattener as long as the US avoids a recession. Fortunately for Bessent, excess liquidity is pointing in that direction in the coming months.

The Treasury Secretary’s comments have been interpreted as being consistent with a reduction in the term premium.

But we can dispense with the unnecessary complications of an unobservable quantity and focus on the yield curve. As argued in a recent column, the two are functionally the same, and we can easily reconstruct the term premium from yield-curve inputs, as I do in the charts below.

A flatter yield curve is not necessarily a good thing electorally for President Trump.

The administration’s agenda is pro-business, yet like any political movement, it will struggle to survive if wealth does not trickle down. Larger stocks have been strongly outperforming their smaller counterparts over the last two years, and growth stocks are outpacing value stocks. A flatter yield curve will only widen these divergences.

That comes as smaller, unlisted businesses are also underperforming. Whether that becomes a political problem or not, the market conclusion is clear: a flatter yield curve should benefit larger over smaller firms. The chart below shows a close correspondence between the S&P’s large versus small-cap index and the reverse of the yield curve.

The same pattern can be seen in high-yield versus investment-grade debt, with the latter expected to outperform as the yield curve flattens.

A flatter yield curve has also historically held back value firms.

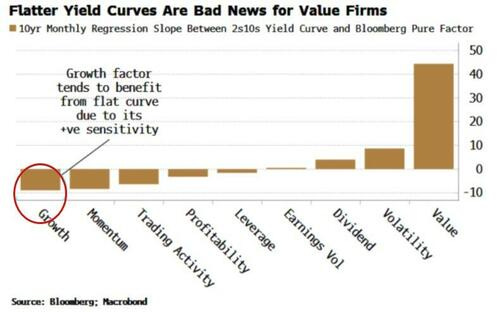

The same conclusion is arrived at by looking at factors’ sensitivities to the yield curve. The market-neutral value factor is the most positively sensitive to the yield curve, while the growth factor is the most negatively sensitive. In other words, growth versus value generally does well when the curve flattens.

There is a fundamental basis for the above relationships.

When the yield curve is flat, larger companies that tend to have a better credit rating are able to term out their debt for cheaper. Smaller firms in general aren’t able to get longer-term financing, and so tend to underperform. The same applies to value companies, which are typically smaller than growth ones. The flipside is true too, with a steeper yield curve favoring value versus growth.

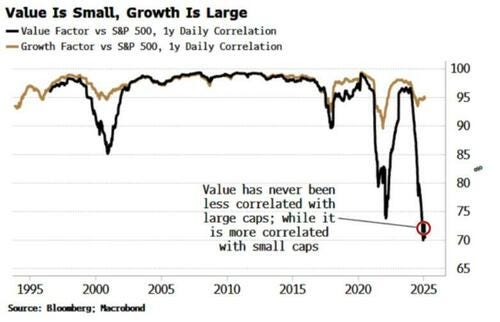

Value has become ever more synonymous with size in recent years. The rise of passive investing has meant that smaller, often more value-like firms have become orphaned, as they are not part of larger-cap indexes. Index funds can’t buy them, and so the big get bigger, the small stay small, and value firms look perennially cheap.

The change has become particularly notable over the last five to seven years. The value and growth factors were both highly correlated to the S&P for most of the 2000s, but since the late 2010s the value factor has become much less so, while its correlation to small-cap indexes has remained high. At the same time, growth stocks have become less related to small caps.

The real drag for small and value stocks began in the wake of the AI revolution, after OpenAI released ChatGPT 3.5 in late 2022. The biggest, growth-like firms, powered by tech, surged ahead and haven’t looked back.

The yield curve was very flat and inverted for most of that period. It’s only since the second half of last year that a steady steepening trend developed, taking the curve back into the positive zone.

Since then value firms and small-caps have caught up a little, but they still hugely lag their more dominant cousins.

Whether the Treasury will be able guide longer-term yields lower without directly interfering in monetary policy (something Bessent said he won’t do) is a moot question. The decision, so far, not to increase the issuance of longer-term debt will help, and so will DOGE if it manages to make significant savings, but the desire to bring in the trade deficit is a structural set-up for higher yields as there will be less global demand for dollar reserve assets. Perhaps it’s no accident that Bessent does not have the trade deficit as part of his 3-3-3 goal for 3% real GDP, a 3% fiscal deficit and 3 million extra barrels of oil production a day.

Either way, leading indicators show the curve should soon cyclically start flattening again. Music to the Treasury’s ears most probably, but an outcome that may have likely unintended, and politically unwelcome, consequences.

Our Biden Inflation Hangover continues....

J.Powell was the Bartender and bears some responsibility, for that misadventure...

Along Comrade Janet Yellen.....