breathe; fact vs hyperbole; collapse in bank deposits; happy bazookA-versary; picked the wrong day to (stop sniffin' glue and / or turn clocks) AND ... its gone.

Janet was NEVER my favorite — neither as Fed Chair or at Treasury. When at FED she was given the keys TO the kingdom and a playbook authored by Bernanke & Co and told what to do and how NOT to muck it up.

She was … how to say this gently? Necessary and sufficient? Fine.

From a source I trust: @SVB_Financial depositors will get ~50% on Mon/Tues and the balance based on realized value over the next 3-6 months. If this proves true, I expect there will be bank runs beginning Monday am at a large number of non-SIB banks. No company will take even a tiny chance of losing a dollar of deposits as there is no reward for this risk. Absent a systemwide @FDICgov deposit guarantee, more bank runs begin Monday am.

Rumors and innuendo and hyperbole have persisted (and likely WILL throughout the remainder of the weekend) and we’re all to blame as we’ve helped create this idea a BAILOUTS COMING tonight.

I’ve heard of an FDIC meeting this evening (CANNOT CONFIRM or find anything solid) as well as an ‘emergency’ FED meeting tomorrow.

There IS a FED meeting tomorrow — an impromptu and CLOSED BOARD MEETING (see HERE) — but I’m not sure they’d be waiting IF it were as ‘emergency’ as we think we KNOW it is, as we’re all bank analysts and SPECULATORS now, right?

CASE IN POINT … Today in history — on this day in 2020, the Fed responded when fiscal authorities wouldn’t (think about that … 3yrs to the day), the Fed offered QE and REPO BY THE YARD … it was a proverbial BAZOOKA

THAT was then and this is now and NOW is NOT THEN again.

We’re likely going to need all the time they can muster (between now and markets opening — perhaps they should NOT have turned clocks AHEAD this weekend) to put humpty dumpty back together again…Sow where to next? Clearly to the main stream media they go.

Yellen earlier today has officially ruled out bailout for SVB:

There continues to be that vibe of 2008 and old folks (not unlike myself) feel like it is some sorta civic duty to share a ‘war story’ of how it was WE spent those moments.

I’ve gotta be honest with you. I’m over it and frankly, think it’s a bit condescending.

There’s this thing — its called the internet — and you — can use it — as well as whatever other resources you TRUST (ie pick up the phone and TALK with people), to become as informed about history as you might like.

I’m simply now more removed and an honest spectator and continue to be fascinated by it all.

Specifically by the way in which NARRATIVE normally FOLLOWS PRICE. That is a general enough statement and you can see it in official language. Reuters citing CBS

"Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out...and the reforms that have been put in place means we are not going to do that again," Yellen told the CBS News Sunday Morning show.

"But we are concerned about depositors and are focused on trying to meet their needs," Yellen said.

This may very well become the next subprime — CONTAINED (I did NOT fall for this one), or the next TRANSITORY (I DID fall for this one — sorry but then the current administration turned the stimmy dial to 11).

A couple things from the inbox AND intertubes to help distract (semi inform) and get you TO this evenings markets opening and whatever it is the authorities have decided and lined up.

Financial markets face a no-win situation, trapped between fears of regional bank runs and central banks worried about sticky inflation. With US retail sales and CPI to come, as well as the ECB meeting, we stay underweight risk assets for the second straight week.

… 3-, 6-, and 12-m average payroll growth is all near 350k; there has been no slowdown on that metric

… The Fed will have to consider both strong macro data and financial sector fears at its next meeting

With regards TO SVB, Barclays notes a valid question (thanks Bill Ackman?),

… If uninsured SVB depositors take a haircut, other regional banks may face runs as well

Wait, what? I thought the saying WAS / is — heads I WIN, tails YOU LOSE?

The note is worth a point and click as is this mornings global macro ‘Sunday Start’ from MS who states the obvious,

Chair Powell’s congressional testimony this week was consequential to markets. He reiterated his strong commitment to returning inflation to the 2%Y target, noting that while the Fed has made some progress, it has been "bumpy”. He indicated that the peak policy rate is likely higher than previously anticipated in the December SEP. Furthermore, he added that the Fed stands ready to increase the pace of monetary tightening again if the "totality of incoming data" warrants it…

… Market pricing of terminal rates illustrates how what drives markets has shifted dramatically this week. At the start of the week, the market-implied terminal rate was 5.45%, but this jumped to 5.69% after the Powell testimony, only to revert to 5.29%, and option-implied volatility for the front end of the rates curve jumped over 20 points as of this writing on Friday. As Guneet Dhingra, our US rates strategist, wrote last week, the market had been underestimating the probability of a 50bp hike – roughly a 20% chance of a 50bp hike in March, which jumped to nearly 75% following Powell's testimony. The 40bp rally in market pricing of terminal rates in the wake of this idiosyncratic bank failure shows that factors which drive market pricing can shift on a dime. We had anticipated higher volatility within a relatively narrow range of outcomes for rates, but what has now transpired is that the range of outcomes itself has widened meaningfully. Yes, it’s complicated.

Where do we go from here? As Betsy Graseck, our large-cap banks analyst and the global head of banks and diversified finance research, noted, “the current pressures facing SIVB are highly idiosyncratic and should not be viewed as a read-across to other banks we cover. Yes, funding is a headwind for the industry, but only to NIM and EPS”. She further noted that “we do not believe there is a liquidity crunch facing the banking industry, and most banks in our coverage have ample access to liquidity”. When combined with the view that Betsy does not expect that other banks in her coverage universe will need to raise capital, we think it is reasonable that market focus on the trajectory of interest rates will revert to the labor market and inflation…

… From a markets perspective, while it is yet unclear if a faster tightening cycle from here is upon us, the prospects for rates staying higher for longer have increased. The improved macro narrative notwithstanding, higher for longer poses challenges for companies with lower-quality balance sheets. In particular, the lower-rated, floating rate-oriented nature of the leveraged loan market makes it fundamentally more vulnerable to this rates environment, in our view.

… However, this week I’m going to spend time on the “most important story” (Silicon Valley Bank) with hopefully a somewhat different angle from most commentators…

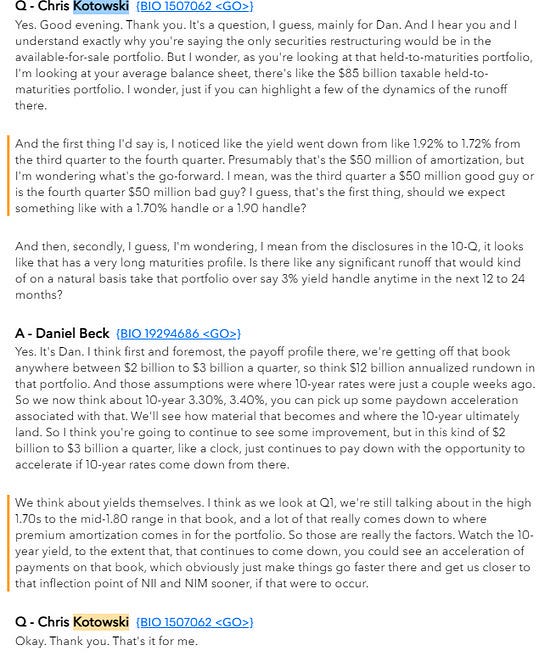

… For the first time in history, an analyst asked a question about the held-to-maturity portfolio on the Q4-2022 call that happened in January 2023.

“That’s it for me”… “Great quarter guys” …

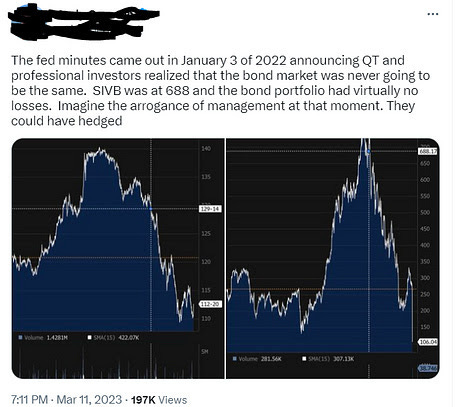

… You will read many stories about the “idiocy” of SVB management team in failing to hedge their interest rate exposure. It’s certainly true that they took a risk by moving too large of an asset pool to HTM and failing to consider the potential for the Federal Reserve to hike interest rates in a truly unprecedented manner. It was OBVIOUS after all:

These are bad takes. First, by this point, SVB management had already moved the assets to HTM and hedging was NO LONGER AN OPTION. Second, the expectation of rate hikes at the time was for something that looked like 2018 which had very little impact on mortgage rates. As the exact same account noted in the “not benefitting from hindsight” March 2022 period, mortgage rates up 120bps reflected “expectations of the full path of hikes already priced into markets.” In other words, mortgage rates above 5% were unthinkable.

Think again…

… So who really owns the failure of SVB? The Fed. By hiking rates in a totally unprecedented manner less than a year after assuring market participants that they were NOT going to hike rates until 2024, they created conditions that predictably led to the second-largest bank failure in US history. And managed to drive stimulus to the economy even as they claimed to be fighting inflation. Is SVB management blameless? Of course not. But unfortunately, they are far from the only bank management team that is seeing deposits collapse as banks struggle with rising competition from money market funds. In fact, the system-wide collapse in deposits is approaching unprecedented levels:

THISvisual is not offered constantly because it’s fun or by accident, rather to detail said ‘accidents’.

Whether or not whatever SVB did was wilful or malfeasance and is latest episode of moral hazard, well, may end up being decided by YOU (certainly not ME).

Regulators right now,

… As they attempt to distract the population from reliving this,