From yesterday’s post with a weekly look at 20s TO an updated look at DAILY

Momentum HERE is ‘middle of the road’ — neither a buyer NOR a seller has a (momentum) advantage so perhaps a continued peek above 5.25% (ie concession) will help …

‘nuff said? OR perhaps yer weary of MAGAzine covers as indicators (likely for good reasons) … but still, how could I ignore …

Missed weekend 2.0 (HERE) and link thru to Barrons …

Barrons: It’s Time to Stop Crying About Bonds and Buy Them Instead

… there you go. I ALSO noted and updated look at 20yy WEEKLY (bullish) and so perhaps a look at the DAILY worth a moment ….

And as the week gets underway with lots of formidable event risk (coupon supply, FOMC and NFP to name just a few), a quick look ahead by Bloomberg

Bloomberg- One Last Make-or-Break Week of 2023 Has Treasury Traders on Edge (I’m a visual learner and clearly the trend WAS our friend — defining my entire career in an institutional FI strat / sales / trading seat and so…TO those who write for a living …)

Traders wait on Treasury sales plans, central banks, jobs data

Events expected to shape sentiment in year’s last two months

It’s been a tempestuous year for US Treasuries. The coming week will set the stage for how it ends.

In the span of just a few days, investors will get updates on the major forces responsible for the unusually high volatility in the US bond market as it heads toward an unprecedented three-year loss. Saturday’s escalation of the Israel-Hamas conflict will also draw the attention of investors, though in recent weeks haven flows into Treasuries have been largely outweighed by concerns over the direction of monetary and fiscal policies.

The federal government will spell out how many new bonds it will sell to plug the budget deficit, which is testing the market’s capacity to absorb a seemingly endless supply of Treasuries. The Federal Reserve and the Bank of Japan will telegraph where monetary policy is heading, which may help shape demand from buyers overseas. And on Friday, the Labor Department will release its monthly employment report, a closely watched indicator of whether tighter monetary policy is cooling the economy as much as policymakers want…

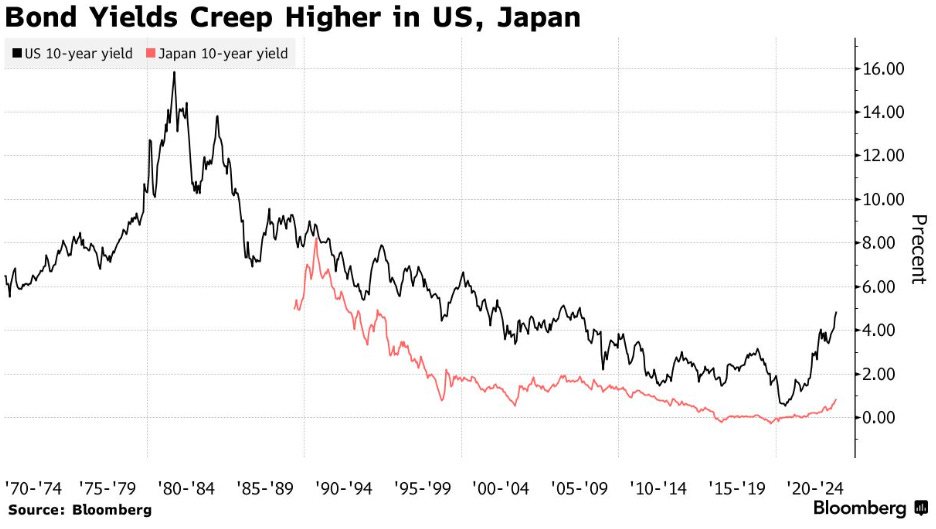

… Bank of Japan The BOJ’s surprise decision in late July to relax its grip on long-term yields, allowing them to rise a bit, helped trigger a global fixed-income selloff by removing an anchor that kept Japanese investors buying government bonds overseas, where rates are higher. That’s heightened interest in the Oct. 30-31 meeting.

“The more they do away with yield-curve control, that’s a bearish impulse on the back end of the Treasury curve,” said Stephen Bartolini, fixed income portfolio manager at T. Rowe Price. The BOJ is “on our checklist of things to mark a high in US yields. Getting off of yield-curve control could lead to the sort of the final impulse in this cycle.”

…FOMC Meeting

At 2 p.m. the same day, the Federal Open Market Committee, the Fed’s policy-setting arm, is expected to announce that it has decided to keep rates steady at a 22-year high of as much as 5.5%. Markets are betting that the Fed’s hikes are likely over, after Chair Jerome Powell said that rising long-term yields reduce the need for further tightening “at the margin.”

STOP … I’ll note this visual of importance and was somewhat more detailed over the weekend (HERE) and by others — SocGEN — who noted, “Historically the fed funds and 10yT yield end the cycle around the same level” …

Whatever the Fed says (and Mr. Market decides to hear and PRICE) this week (November PASS but then what of December), will be of YUUUUGE significance…

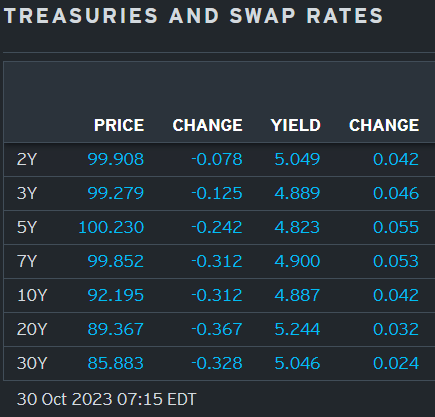

… here is a snapshot OF USTs as of 715a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower in a belly-led, risk-on move ahead of this week's big events. DXY is little changed while front WTI futures are lower (-1.25%). Asian stocks were mixed (Japan lower, China higher), EU and UK share markets are all in the green (SX5E +0.9%) while ES futures are showing +0.65% here at 6:55am. Our overnight US rates flows saw a 'quiet and orderly' leak lower in bond prices as Friday's safe-haven bid was unwound. Real$ has shown interest in flatterers (2s10s, see attachments) and outright demand for front-end paper from fast$. Overnight Treasury volume was again weak at 60% of average overall with 2yrs (90%) seeing the highest relative average turnover overnight, matching our flows.

… and for some MORE of the news you can use » The Morning Hark - 30 Oct 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in a similar sorta way you’ll find content if you pay for ZH PREMIUM … except different … I think, as they seem to be selling others research and I’ve never been quite sure how they can do that … anyways, another time …)

Apollo- The Costs of Capital Are Permanently Higher

The Fed has since the beginning of 2023 steadily increased its estimate of the long-run fed funds rate, see chart below. The implication for investors is that the Fed is beginning to see the costs of capital as permanently higher. A permanent increase in the risk-free rate has important implications for firms, households, and asset allocation across equities and fixed income.

BNP - Fear over fundamentals in oil and gas markets

Crude and gas markets are struggling to find direction as market fundamentals and sentiment fight for dominance.

We believe these dynamics lead us to a few conclusions:

1.Oil and gas markets are driven by sentiment rather than fundamentals;

2.TTF is overpriced versus fundamentals while Brent is underpriced;

3.Gas is more sensitive to conflict escalation; and

4.Recalibration to fundamentals-driven prices can be aggressive in gas particularly.

We expect crude to reconnect with fundamentals in November, while for gas we need to see an end to conflict escalation and milder-than-expected weather.

As suggested in active trade ideas, we believe shorting gas and buying crude is a strategy to monetize this, with the risk being a gas blow out in the heaviest conflict escalation.

… We start a busy week for markets after a few major landmarks were reached on Friday that are worth highlighting. The S&P 500 moved into "correction" territory, now down -10.27% from the July highs. Meanwhile the benchmark small-cap Russell 2000 index went through its June 2022 lows and back to levels last seen in November 2020, around the time that Pfizer announced the first successful Covid-19 vaccine trials. In fact, it's now back to levels it first breached in November 2018. When you factor in the huge inflation over this period, that's some serious real adjusted declines. So for all the optimism surrounding US equities this year it really is only a handful of huge companies that's skewing the positivity…

… In short, fiscal policy and FX interventions may aim to reduce inflation in the short term, but they increase the risks of higher inflation in the medium term, resulting in an increasingly unsustainable policy mix.

MS - The Weekly Worldview: The Downside to Higher for Longer

EM banks led the hiking cycle. What does "higher for longer" in the US mean for them now?

This entire hiking cycle, we have said the US economy would avoid recession, and the Fed would hold its policy rate in restrictive territory for years, the so-called “higher for longer” strategy. Anticipating the DM hiking cycle, EM central banks were early to start hiking this cycle. The logic was to try to insulate their domestic economies from higher rates elsewhere, and we anticipated a cycle of hikes and subsequent cuts for both EM and DM. Indeed, many EM central banks recently began to position to start cutting….

The word “recession” is a curse cast on the economics profession. There is no formal, universal definition. The media’s obsession with “two consecutive quarters of negative growth” is increasingly meaningless in the modern world. Output economic measures like GDP depend on how many people are working, and how hard those people are working. Thus, countries with declining populations are more likely to have falling GDP, but are not more likely to have falling living standards….

… And from Global Wall Street inbox TO the WWW,

Bloomberg - The Big Bond Market Event Wednesday Is at Treasury, Not the Fed

Dealers see the US Treasury lifting note and bond sales again

Meanwhile, Fed officials have prepped market for another skip

The Federal Reserve’s policy statement is setting up to be the No. 2 event on Wednesday, with investor focus instead likely to be on the Treasury Department’s new borrowing plan, due hours ahead of the interest-rate decision.

The so-called quarterly refunding announcement will reveal the extent to which the Treasury will ramp up sales of longer-term debt to fund a widening budget deficit. Those securities have been tumbling for weeks, even amid signals from Fed officials they’re “at or near” the end of rate hikes.

The selloff has sent yields to the highest levels since before the global financial crisis — making longer-term Treasuries more costly for the government. Investors are eager to see whether officials maintain the pace of increase in longer-term debt sales they announced in the August plan. Bumpy auctions of some securities in recent weeks have only increased that focus.

“Market participants are really hyper-focused on supply now and we kind of know the Fed is on hold,” Angelo Manolatos, a strategist at Wells Fargo Securities, said in a telephone interview. “So the refunding is a bigger event than the FOMC. It also has a lot to do with the moves we’ve seen in yields since the August refunding.”

Many bond dealers predict a refunding size of $114 billion, representing the same cadence of increases per each refunding security as laid out in the $103 billion August plan, which marked the first step up in issuance in more than two years.

An alternative view predicted by several large dealer firms would be a smaller bump in longer-term debt, given the surge in yields, and greater reliance on bills, which mature in a year or less. Some see this tweak potentially combined with a signal that a further increase of long-term sales isn’t certain for the next refunding, in February.

“Looking at the refunding, the composition of Treasury issuance might be very consequential and relevant” to the market, said Subadra Rajappa, head of US interest rates strategy at Societe Generale SA. As for the other Wednesday event, “this meeting is sort of a placeholder for the Fed,” she said.

Indeed, Fed Chair Jerome Powell — a former Treasury official himself — and his colleagues may take interest in investor reactions to the refunding. He and others, including Dallas Fed President Lorie Logan, who previously oversaw the Fed’s market operations, have said the surge in long-term yields may mean less need to raise the benchmark rate.

Yellen’s Rebuff

Ten-year yields were around 4.8% at the end of last week, well over three quarters of a percentage point higher than before the August refunding. Yields remained high even after the outbreak of the Israel-Hamas war three weeks ago – the kind of geopolitical flashpoint that can spur haven demand for Treasuries. Israel’s weekend invasion of Gaza will again test previous norms.

While Treasury Secretary Janet Yellen on Thursday rejected the idea yields were climbing due to swelling federal debt, Powell this month did list a focus on deficits as a potential contributing factor.

Earlier this month, Treasury data showed the federal deficit roughly doubled in the fiscal year through September compared with the year before, effectively reaching $2.02 trillion. The worsening trajectory helped prompt Fitch Ratings to strip the US of its top-tier AAA sovereign rating on the eve of the August refunding.

On Monday, the Treasury will set the stage for its issuance plans with an update of quarterly borrowing estimates, and for its cash balance. In August, officials penciled in net borrowing of $852 billion for October through December. Lou Crandall at Wrightson ICAP LLC says he’s not expecting any downward revision in Monday’s update.

US debt managers in August lifted the refunding issues, which include 3- and 10- and 30-year Treasuries, by $2 billion, $3 billion and $2 billion relative to each of those securities’ previous auctions of new debt. They also increased issuance of all other note and bond maturities, something dealers see happening again this time.

A $114 billion plan for Wednesday would mean the following upcoming quarterly refunding auction sizes:

The JPMorgan Chase & Co. rates team is looking for a “rinse, repeat” of August. That, they say, was also signaled by Josh Frost, the Treasury’s assistant secretary for financial markets, in a talk last month.

That’s not the universal view, however. Wells Fargo, Goldman Sachs Group Inc., Barclays Plc and Morgan Stanley are among those expecting the Treasury to tilt this time more toward short-term securities, in part given the rise in long-term rates.

Solid demand for Treasury bills, which yield well over 5%, means there would be ready buyers, but bills currently make up more than 20% of marketable Treasuries. That’s slightly above the recommended range of 15% to 20% laid out by the Treasury Borrowing Advisory Committee — a panel including dealers and investors. Even so, in August, TBAC said it’s comfortable with bills temporarily taking a larger share.

While the government has a longstanding pledge to be “regular and predictable” with its debt-issuance plans, the group of dealers forecasting a change in the pace of the expansion in note and bond auctions argues that the Treasury’s credibility would remain intact. That’s in the context of the August TBAC guidance on bills and an expected lift in auctions of all coupon-bearing maturities.

Besides issuance plans, investors will also be looking for an update from the Treasury of its progress in assembling a program of buybacks of existing securities. The department has said those will start in 2024.

The deficit isn’t the only dynamic forcing the government to borrow more from the public. The Fed is running off its holdings of Treasuries at a pace of up to $60 billion a month. Powell cited this process, known as quantitative tightening, as another potential contributor to the rise in long-term yields.

Next February

It all means the department may have little option over time.

“Treasury will have to again raise funds across the maturity spectrum” on Nov. 1 and again in February, said Praveen Korapaty, chief interest-rate strategist at Goldman Sachs. Goldman’s economists don’t see Fed QT ending completely until early 2025.

The backdrop is ripe for volatility after the 8:30 a.m. refunding details hit the wire.

“Treasury does make adjustments based on how markets are receiving supply,” Korapaty said. “Right now the market is telling you that if you are putting more duration supply in then the market clearing price is going to be higher.”

Hopefully something more of a complete update tomorrow but … THAT is all for now. Off to the day job…

So much like Covid Vaccine & Booster uptake, Pfizer shares, and the US stonk indexes, have taken the zero to infinite to zero round trip. Since that magical day, the Monday after Brandon had been declared the "winner". I'd like to GLOAT, but considering FDA doesn't track Covid 19 Vax injuries, I'm reminded of many memes. Such as "If I burn my published books first-they can't be banned!"

Very informative on the Quarterly Refunding announcement...

Barron's Cover: Hope those aren't "Magic Mushrooms"...... Hallucinogens ????

What a week comin up.....should be interesting, but probably more torture...

Thanks for your Expertise...

So much like Covid Vaccine & Booster uptake, Pfizer shares, and the US stonk indexes, have taken the zero to infinite to zero round trip. Since that magical day, the Monday after Brandon had been declared the "winner". I'd like to GLOAT, but considering FDA doesn't track Covid 19 Vax injuries, I'm reminded of many memes. Such as "If I burn my published books first-they can't be banned!"