(belly leading selloff on 'statistically weak' volumes) while WE slept; bad news IS good; DFS chargeoffs; COLAs good (but not good 'nuff); yields 'bout to DROP (RoC...)

Good morning … HIMCOs quarterly updated was posted and I’ve mentioned it HERE, in the case you’ve not seen or heard. I’d ALSO note with BoJ and YCC remaining top of mind, Japan inflation hit fresh 41 year high of 4.0% and then this morning, completely UNRELATED to YCC,

ZH: "I Have Difficult News To Share": Google CEO Tells Employees 12,000 Jobs Will Be Cut

… Following the news, Alphabet's shares are up nearly 2% in premarket trading.

The cuts mark the latest high-profile layoffs from some of the biggest tech names. Days ago, rival Microsoft Corp said it would slash its headcount by 10,000 workers. Amazon, Meta, and others have also announced job cuts as macroeconomic headwinds continue to mount…

Bad news really IS good (save for those 12k families)! I KNEW it!

Livin’ in interesting times, indeed…here is a snapshot OF USTs as of 706a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have been led lower by the belly and peer markets overseas (Bund and Gilt 10's ~3bp cheaper to UST 10's) amid locally 'overbought' conditions here. DXY is modestly higher (+0.15%) while front WTI futures are higher too (+0.9%). Asian stocks were generally higher (Hang Seng +1.8%), EU and UK share markets are all modestly higher (SX5E +0.5%) while ES futures are showing +0.1% here at 6:45am. Our overnight US rates flows saw relatively muted activity with a 'soft tone' to the price action with fast$ front-end selling a noted feature. Going into the London crossover some real$ buying in 10's helped to claw back some earlier losses while our London desk said that there was very little activity to report during their AM hours. Overnight Treasury volume was indeed statistically weak at ~55% of average overall with 3's and 5's each seeing the highest relative average turnover at ~85% each.

… our first attachment this morning again shows the deep, short-term 'overbought' conditions in Treasury 5-year notes. We used 5yrs as just one example where similar-looking, tactically 'overdone' set-ups are now evident in all other Tsy benchmarks as well... Moreover, recall that it was the Q4 2021 ECI print a year ago that bubbled brains at the FOMC and sent the Fed's 'transitory inflation' narrative into the dustbin... Will lightning strike twice?

… and for some MORE of the news you can use » IGMs Press Picks for today (5 JAN — and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

First, from the intertubes as the dust from yesterday continues to settle … it would appear consumers are NOT in good shape … surprising nobody?

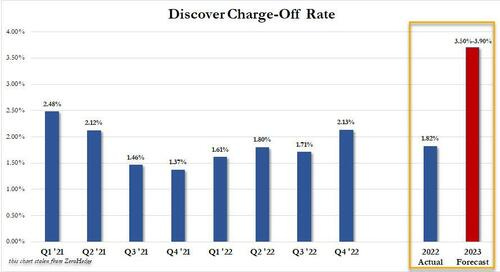

ZH: The US Consumer Has Cracked: Discover Plunges After "Shocking" Charge-Off Forecast

… Presenting Exhibit A: Discover Financial Services (DFS), a credit card issuer which traditionally targets to low to middle-income households, and which yesterday reported earnings that were so scary, Wall Street has uniformly dubbed them "shocking." But while the bulk of the company's historical results were actually not all that bad, it was its forecast that a stunner: in a presentation on its website, DFS forecast that its charge offs would climb as high as 3.9% this year (it gave a range of 3.50% to 3.90%) which is more than double the 1.82% net charge off rate it booked for all of 2022 and was about 100bps higher than the 2.8% consensus estimate.

Cutting to the chase, this is what the company's historical and projected charge offs look like:

And since this is a net number, the gross number will likely hit 5% or more, a level not seen outside of painful recessions.

As Bloomberg explains, credit cards typically reach their peak loss rates about 18 months after origination. That means that Discover is expecting losses to tick up this year on accounts it started in 2021, which was a much bigger year for credit-card growth than 2020, when the pandemic forced the company to curtail new business. Starting last year, Discover began gradually tightening underwriting standards by offering smaller lines of credit to new customers, although the combination of a recession plus tapped out consumers will ensure a surge in charge offs for that and any one vintage.

… AND moving along right back TO Global Wall Street inbox where today we’ll find some great news and discussion of the UPSIDE to inflation — COLA increases — and so, this one from a rather large French bank

Recent pronounced weakness in in retail sales points to rapid cooling of consumer demand going into 2023. While, in our opinion, a hefty cost-of-living adjustment for social security recipients at the beginning of the year may provide a temporary reprieve, the resulting increase in income will not be enough to avert a broader slowdown in spending later this year.

Annual cost-of-living adjustments to US government transfer payments (mainly Social Security) are set to increase by about USD100bn on the back of the fastest inflation in 40 years. While this will not prevent the economy from falling into recession later this year, it will provide some offset to slowing wage growth, particularly in Q1 2023. However, we expect much of the benefit to erode by Q2.

Around 70 million Social Security and Supplemental Security Income (SSI) recipients will see their monthly payments rise by 8.7% in January. This COLA top-up should appear in the US personal income and spending data for January, which will be released on 24 February.

The increase will take effect as consumer prices decelerate, making it particularly beneficial for lower-income consumers, who have a much higher propensity to consume. Higher-income individuals have largely supported growth in consumer spending more recently (see US: Twilight of the post-pandemic consumer, dated 1 December 2022).

This one-time bump in income will give some additional spending power to households that have been burning through savings, but will not be a game-changer in aggregate. Other negative offsets will moderate the income boost, which we discuss below.

Oh … never mind … I thought there was a bright side to inflation. Guess not. Moving right along then from a large French bank to a popular kid from a large German bank,

After a few ruckus days when global markets were roiled by both the BOJ and weaker US data, it seems a brave call to suggest that bond vol will be a restraining force on FX vol going forward. Nonetheless, it appears likely that we are in for a quieter picture for asset market vol, most specifically driven by US Treasuries.

Risks are that US bond ranges tend to get squashed, as better-behaved US inflation constrains the top side in yields, as does evident strong foreign and domestic demand when 10s are near 4% - in no small part because 4% is in the 98.7% percent rank of the yield range over the last 15 years.

Meanwhile, contrary to many bullish expectations, the downside in yields is protected by two historical relationships: Firstly, since the early 1980s, the 10y minus fed funds spread has spent close to no time with a negative carry of more than 150bps. By this relationship, IF effective fed funds stay near 4.88% then 10s will struggle below 3.38%. If the Fed is correct, and the fed funds peak is going above 5% as the last median Fed dots indicate, then 10s are not going to spend much time below 3.5% easily.

Secondly, over the last 5+ decades of interest rate cycles, the 10y has (since 1971) averaged 116bps above fed funds. IF the funds rate were to settle at a 2.5% equilibrium rate in the medium term, then - again - a 10y much below 3.5% would start to look out of step, without special factors reducing the term premia. Currently the Eurodollar strip indicates a low point in fed funds near 2.75%. The most obvious way for 10s to go lower is, of course, when/if the funds rate dips below perceived equilibrium in the next Fed easing cycle, but for now the market is reluctant to entertain a quick dip in the funds rate despite the zero nadir in rates from the last two cutting cycles.

The message is that: i) the terminal rate peak must drop, and/or ii) the subsequent expectations on the speed and extent of the next rate-cutting cycle must extend further, to generate much bond bullish momentum. For now, the market does not seem willing to price in less than another 50bps of additional hikes, and equally is not ready to more aggressively price in cuts below neutral, at least while rates are still being hiked. These are already some of the features behind bond vol’s moderate slippage this year, with metrics like the MOVE index down significantly from the start of the year, even with what has been a sharp 48bp slide in 10y yields over this period.

The point is that US bonds will very likely provide less leadership in terms of absolute moves than they have over the last year …

Okie dokie … good piece and worth a look. NOW continuing to span the GLOBE right from comfort of the inbox we move from France to Germany and now over TO the UK

Barcap Global Rates Weekly: Too fast, too furious In the US, recent negative data surprises might not be a reliable gauge for the outlook ahead, and we recommend a tactical short position in the front end…

… As we approach the February FOMC meeting, the general consensus among members seems to be for a 25bp hike but to keep policy restrictive for longer (Figure 5). Dallas Fed President Logan noted that “A slower pace is just a way to ensure we make the best possible decisions” and added that “We can and, if necessary, should adjust our overall policy strategy to keep financial conditions restrictive even as the pace slows.” Philadelphia President Fed President Harker reiterated his call for 25bp and added that “I think we get north of 5 — again, we can argue whether it’s 5.25% or 5.5% — but we sit there for a while”. St Louis Fed President Bullard seems to favor a larger hike but added that “We are almost into a zone that we could call restrictive — we’re not quite there yet” and also added that “Policy has to stay on the tighter side during 2023” …

… Heading into the data releases over the coming weeks (PCE inflation and payroll) and the upcoming FOMC meeting, we recommend a tactical short position in the front end (using SFRU3, entry 4.68%). As discussed above, we believe some of the pessimism with respect to the economy, which is based on data releases for the month of December, is not justified. The upcoming inflation prints are likely to be robust and with initial claims trending lower, the upcoming payroll print should also be relatively strong. Further, given the easing in financial conditions, Chair Powell is likely to stress the need for higher policy rates for longer. Should upcoming data suggest that the pessimism is not justified, markets are likely to pay more attention to such Fedspeak. We therefore see attractive risk-reward in being short the front end in the very near term.

What does this all add up to and MEAN?

… Heading into the data releases over the coming weeks (PCE inflation and payroll) and the upcoming FOMC meeting, we recommend a tactical short position in the front end (using SFRU3, entry 4.68%). As discussed above, we believe some of the pessimism with respect to the economy, which is based on data releases for the month of December, is not justified

This front end short is NOT on a deserted island … there are SOME positives ‘out there’ and they note,

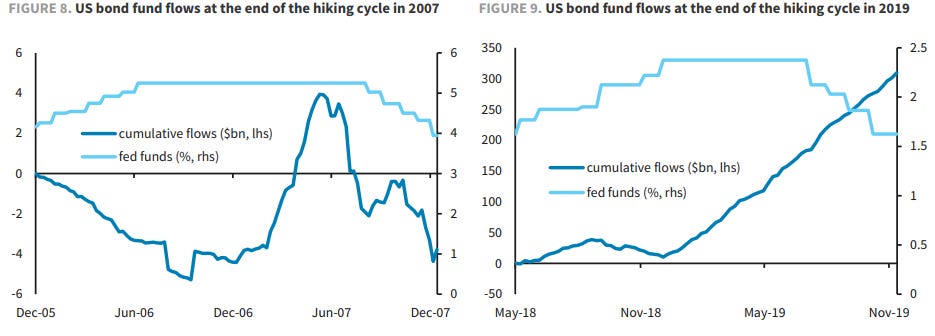

… one tailwind for bonds is the shift in mutual fund inflows. Last year, US bond mutual funds and ETFs recorded a staggering level of outflows, eclipsing the amount in 2013 during the taper tantrum and was one of just three years in which net flows were negative since the data series began in 2003. On the other hand, the most recent two weeks of data show funds had net inflows raising the possibility that the worse may be behind us.

Looking back to when the Fed neared the end of its hiking cycles in 2007 and 2019, we find that such inflows might indeed be sustained (Figures 8 and 9). In both cases, as the the Fed raised rates, bond funds had outflows, which continued even as the Fed paused hikes in 2006. Flows did not turn positive until the Fed neared the start of rate cuts — six to eight months before actually doing so — during both of these cycles. Using this as a guide suggests that bond fund flows may be positive in the months ahead, and that term premium may remain contained for now.

Case of RETAIL buyin’ at the ‘highs’? Struggling, personally, with this one as well as some other risks — investors flowing themselves into the front-end (talked with friends / family lately about how ‘cheap’ 3mo, 6mo and 1yr TBILLS are lately?? CDs anyone??) and while it seems to make an enormous amount of sense on the one hand … The Fed not about to CUT, are they?

Dunno — if something seems to good to be true, it likely isn’t.

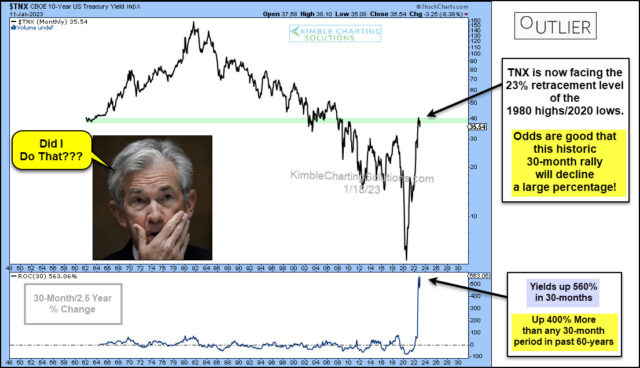

Finally, for those inner chartists as well as any / all academics and FUND MANAGERS (like was noted HERE yesterday …) who are long bonds

… As you can see, the 10-year bond yield rallied up to the 23% Fibonacci retracement level of the 1980s high/2020s low (green line). And, while doing so, it recorded a Rate-Of-Change (ROC) that we haven’t seen before: yields are up 560% in 30 months!

That is up 400% more than any 30-month period in the past 60 years. Looks like it’s time for a breather…

Time will tell if the Federal Reserve rose interest rates too fast…

Equities and bonds are both faltering after 2023’s opening rallies, though the former is noticeably gloomier. Still, the bugbear for both can be boiled down to concerns the Federal Reserve is going to end up engineering a hard landing for the US economy. True, rates traders are boosting bets the US central bank will stop short of a 5% target rate — and then cut it by at least half a point over the second half of the year. But the nagging worry is that Fed officials are insistent a higher level is expected and that wherever they stop they will hold borrowing costs at restrictive levels for a significant time.

Even if the economic damage that would do might lead to longer-term bond gains, the short term looks full of risks, and for equities the potential of a second year of Fed hawkishness looms as a severe challenge. Given the way assets rebounded since tightening expectations peaked in the fourth quarter of last year, any reversal of that trend in rates pricing would signal plenty more pain for investors.