Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note … Sending on heels of CPI and FOMC and because I will be outta pocket tomorrow and I neglected to mention in this mornings update …

30yy DAILY … noted over weekend this chart was the most interesting of the charts and looking at today’s DAILY, would you look at where yields stopped dropping …

… clearly in wake of the early DATA and FOMC announcement and presser, well, it may be too late (or early) and the turn lower in yields may have already started (again, or not) … On to a couple / few links / resources of interest as you get those bids in early and often for 30yy …

Reuters: US disinflation good, Chinese disinflation bad

… The Fed's revised outlook - fewer rate cuts this year, slightly higher unemployment, a higher long-term policy rate - cooled equity, FX and fixed incomemarkets late in the U.S. session on Wednesday. Quite significantly, in the end.

But it was not enough to puncture the U.S. 'soft landing' narrative and the market impact was clear - record highs for the S&P 500, Nasdaq and world stocks, and declines in U.S. bond yields, the dollar, and cross-asset volatility…

Here are some CP(H)I and FOMC resources / links for you to read with whatever bias and spin you wish …

Bonddad: May CPI continued to be all about shelter

CalculatedRISK: BLS: CPI Unchanged in May; Core CPI increased 0.2% CalculatedRISK: YoY Measures of Inflation: Services, Goods and Shelter CalculatedRISK: Cleveland Fed: Median CPI increased 0.2% and Trimmed-mean CPI increased 0.1% in May

ZH: Consumer Prices Hold At Record Highs - Up 20% Since Biden Elected ZH: Wall Street Reacts To Today's Dovish CPI Shocker: "Down And Out"

WolfST: Fed Sees Only 1 Rate Cut in 2024, Holds Rates at 5.50% Top of Range, QT Continues at Slower Pace as Announced in May

Higher for longer becomes formalized one meeting at a time, as projections for “longer-run” federal funds rate continue to be raised.

ZH: FOMC Holds Rates As Expected, Dot-Plot Shifts More Hawkish In 2024 ZH: Powell Admits The Biden Admin Is "Overstating" Jobs

AND some further sellside ‘recon’ and victory laps … here’s SOME of what Global Wall St is sayin’ …

May core CPI inflation printed 0.16% m/m (3.4% y/y), 13bp slower than in April. Disinflation in core services, led by transportation services, helped more than offset a modest firming in core goods driven by a rebound in used cars. The data translate to a 0.1% m/m core PCE inflation print for May.

… All told, we view this magnitude of slowing in the CPI (and the PCE) as unsustainable, and expect some payback next month. In the CPI, we view the slowing in categories such as airline fares and other services as unsustainable. We are interested to see how auto insurance inflation behaves in June, as the price decline in May was the first since October 2021. Within other services, we found that most of the deflation came from legal services (-2.3% m/m), a volatile category that could rebound in June, and carries slightly more than twice the weight in the PCE price index. In addition, we think financial services PCE, which we expect to slow in May, could rebound in June, based on improved stock market performance. Bottom line, it is plausible that we get a core PCE print that rounds to 0.2% m/m in June.

Bloomberg BNP US May CPI: A welcome (but noisy) downside surprise

KEY MESSAGES

Headline and core CPI delivered a sizable downside surprise in May, driven by the key non-shelter services category.

While encouraging, a few likely one-off factors exaggerated the degree of cooling.

With PPI still to come, we see May core PCE inflation at a soft 0.2% m/m with risks titled to the downside.

At the margin, the CPI print raises the risk of a September rate cut versus our December baseline. We continue to think that while the inflation outlook alone could justify a September move, the presidential election will keep the Fed sidelined until December.

By changing its dot plot projection for this year from three rate cuts to just one, the Fed is indicating a preference to wait longer before it can start easing, despite acknowledging “modest further progress” on inflation lately.

After all, having been surprised with disappointing inflation prints earlier this year, the Fed now wants to build sufficient confidence that inflation is on track to converge to the 2% target before embarking on a rate-cutting cycle.

We continue to expect the first cut in December. Even though progress on inflation could imply conditions for a first move in September, presidential election uncertainty would argue in favor of waiting until December, in our view.

The Fed held rates steady as expected and delivered a hawkish surprise with a dot plot that showed a median of only one rate cut this year. Although Chair Powell did not emphasize this hawkish signal, he did downplay this morning's softer CPI print as only one data point and stressed that the economy and labor market are solid. The meeting thus left open the door for a cut before the election, even if that may not have been the base case for a majority of officials in June.

Revisions to officials' forecasts were close to expectations outside of the 2024 dot. The median showed a 4.1% fed funds rate in 2025, up 25bps from March, and the long-run dot rose to 2.75%, its highest level since 2019. Growth and labor market forecasts were little revised, consistent with an economy that is expected to operate near its longer-run values over the coming years.

Our baseline remains that the Fed is likely to cut rates once this year in December (see "(Pushed) Back to December"). However, this morning's softer CPI print opens the door more widely to a September rate cut. That outcome requires the next few months show similarly tame inflation readings and, as Powell indicated, possibly some softening in the growth and labor market data.

… Bottom Line: Progress on inflation has improved slightly over April and May but not nearly enough to fully reverse the upward trend seen earlier in Q1. Amid those uncertainties, U.S. Fed again reiterated that interest rates will need to stay higher until greater confidence that inflation will return to the 2% target can be built. Separate dot plot correspondingly showed a move in the median fed funds projection higher in both 2024 and 2025. We see the outcome of today's meeting as broadly in line with our expectations, and maintain the view that ongoing easing in inflation and gradual cooling in labour markets will persist, prompting the Fed to make a first rate cut later this year in December.

Summary Today's CPI data were surprisingly soft and will be welcomed by the FOMC as it concludes its two-day meeting this afternoon. Headline CPI was unchanged in the month, the first flat reading since July 2022. Falling energy prices and a very modest increase in food prices helped to keep headline CPI in check. Core CPI increased by a "low" 0.2% (0.16% before rounding), the smallest increase since August 2021. Sticky services inflation finally showed signs of easing, registering 0.2% amid price declines for airfares (-3.6%), motor vehicle insurance (-0.1%) and lodging away from home (-0.1%).

On balance, the May CPI data were encouraging across the board. Tame inflation for food and energy bodes well for consumer spending power, while the deceleration in core CPI suggests that the underlying inflation trend remains firmly downward. The core CPI has risen 3.4% over the past year, the smallest 12 month change since April 2021. That said, inflation remains above the Fed's target, and there have been enough false starts in the past that the FOMC likely will need to see at least a couple more rosy inflation reports to gain the "greater confidence" needed to start reducing the federal funds rate. The materials and post-meeting press conference from the FOMC's meeting later today will shed more light on how the Committee sees inflation evolving alongside its employment mandate, and we expect the median participant on the Committee to project two 25 bps rate cuts by year-end.

As expected, the Federal Open Market Committee left the federal funds rate target range unchanged at 5.25-5.50% at the conclusion of its meeting today. Yet the latest Summary of Economic Projections showed most participants continue to expect at least some reduction in the fed funds rate before the year is out.

The median projection for the fed funds rate at year-end was raised to 5.125% from 4.625% in the March SEP, implying only one 25 bps cut before the year. However, the distribution of projections skewed toward more easing, with eight participants expecting two cuts and only four expecting rates to remain unchanged. Participants now see 100 bps of easing over 2025 compared to 75 bps in the prior SEP, which would leave the fed funds target at 4.125%.

The delayed start to rate cuts comes as inflation has been stickier this year while economic activity remains "solid." Participants now see core PCE inflation up 2.8% on a Q4/Q4 basis compared to 2.6% in the March SEP, but GDP growth unchanged at 2.1%—above the Committee's median estimate of potential—and the unemployment rate holding at its current rate of 4.0%.

Changes to the post-meeting statement were minimal. The Committee gave a nod to the somewhat better run of inflation data since its May 1 meeting by noting that there has been some "modest further progress" on the inflation front instead of a "lack of further progress." But, the statement reiterated that inflation remains "elevated" and the FOMC is "strongly committed" to its 2% inflation objective.

While the May CPI report released earlier today was encouraging for the inflation outlook, the FOMC clearly needs to see more benign prints before a consensus emerges that a reduction in the fed funds rate is warranted. With few signs of that consensus emerging yet, we continue to believe that the earliest the FOMC would reduce the fed funds rate would be at its September 18 meeting, when it will have three more months of inflation and employment data in hand.

It will be a close call between one or two 25 bps rate cuts, and the Committee seems evenly split between the two outcomes. Our base case forecast since early April has looked for a 25 bps rate cut at each of the September and December FOMC meetings. For now, our forecast remains two cuts this year and another 100 bps of easing in 2025. We will publish our standard monthly economic forecast update on Friday morning.

Both stock and bond market bulls are basking in the sun today as this morning's inflation data for May came in weaker than expected across the board. Headline CPI came in flat (0.0%) month-over-month (MoM) versus estimates for +0.1%, while core CPI came in at 0.2% MoM versus estimates for 0.3%.

Unfortunately for bulls, we still have the Fed to contend with this afternoon. At 2 PM ET, Fed Chair Powell and Co. will provide updates on interest rate policy and forecasts. Powell will then take the podium for a post-FOMC press conference around 2:30 PM ET.

Will the stock market manage to hang on to big intraday gains, or will we get another Fed-induced late-day sell-off?

As shown below, Powell (red line) has so far had the weakest Fed-Day gains of any Fed Chair for the S&P. The typical (or average) Powell Fed Day sees intraday gains mostly erased with a last-hour selloff into the close.

Of course, we don't ALWAYS see late-day selloffs on Powell Fed Days. As shown below, over the last five Fed Days, we've actually seen gains from 2 PM into the close three times and declines twice. The last meeting on May 1st was a doozy, though. Check out the intraday path for the S&P on May 1st in the chart (lighter blue line). Heading into the 5/1 FOMC announcement at 2 PM ET, the market was down slightly on the day. We then saw a big 1%+ rally from 2 PM to 3 PM, but then we fully reversed that rally in the final hour of trading to actually close down on the day.

Given today's better than expected news on the inflation front, Powell and the rest of the Fed have some ammo to take a more dovish tilt. Whether they want to actually do that or not, nobody yet knows.

After April’s allegedly soft report, the May CPI was truly weak and consistent with eventual Fed rate cuts. Both headline and core inflation surprised to the downsize, with a flat headline (compared to a 0.1% forecast) and a 0.2% increase in the core (0.3% consensus). As usual there was a lot of noise in both the headline and core measures, with big swings in gasoline, new and used car prices, vehicle insurance, airfares, tobacco and so on. As such, it is important to fade the core and focus on metrics that automatically strip out the noise. My favorite is the trimmed mean, which was even softer than the core, rising just 0.1%…

… This is exactly the kind of report the Fed is hoping for, cancelling out at least one and perhaps two bad reports. As I noted in my preview, after four months in a row of significantly-above target monthly readings, the Fed needs to see a similar number of on-target readings—that would be 0.20% for the core CPI and 0.17% for the core PCEs. Unlike the April report, the May data brings September into discussion. Similar 0.2% or so readings in the coming months (data for June, July and August) would likely trigger a September cut…

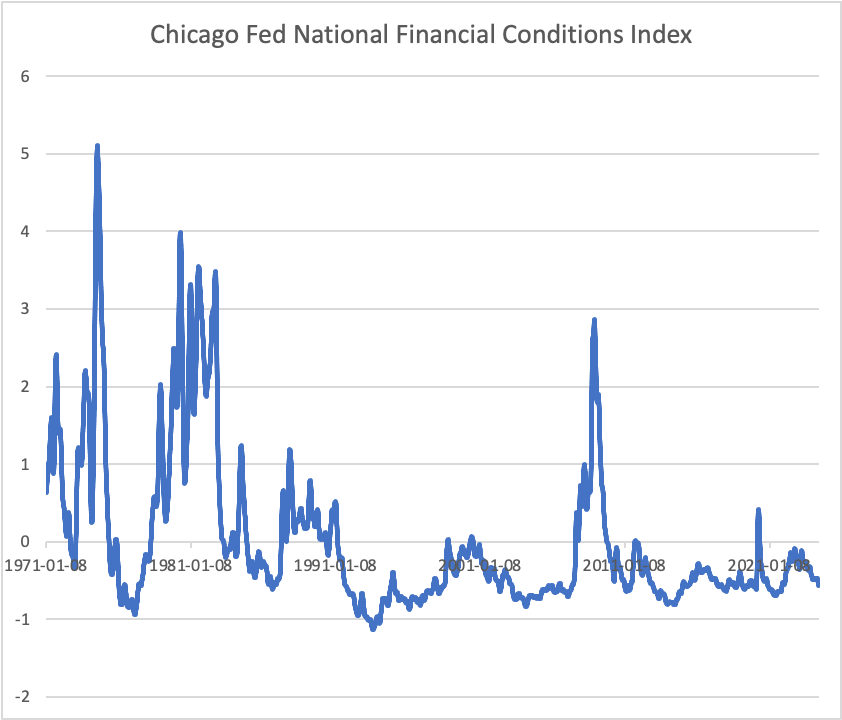

… In assessing whether policy is tight or not, we need to look at financial conditions, not the funds rate relative to last year’s inflation. Financial conditions have remained relatively easy in the despite the “surge” in the ex post real funds rate. Borrowing costs are high, but stable, asset prices are strong, credit spreads a tight and most financial conditions indexes are in easy territory, including the Chicago Fed’s metric (below).

FirstTrust: Data Watch - The Consumer Price Index (CPI) was Unchanged in May

… a subset category of prices the Fed has told investors to watch closely and is a useful gauge of inflation in the service sector – known as the “Supercore” – which excludes food, energy, other goods, and housing rents, was unchanged in May. That is the lowest reading since September 2021, a welcome sign for the Fed, as Supercore has showed no sign of abating since the Fed began hiking rates: up 4.8% in the last year and an even faster 5.5% annualized rate over the last six months. While the last two months of inflation data have been “good news” for the Fed, they have repeated they want full confidence that inflation is trending sustainably toward their 2.0% mandate. That likely means several months of cooler readings before they move toward the first rate cut. Moving too soon before the job is done could determine whether we repeat the inflationary 1970s.

ING: Federal Reserve keeps policy unchanged, signals just one rate cut before year-end

The Fed left interest rates unchanged at 5.25-5.5%. Their updated forecasts leave 2024 growth and unemployment unchanged, but inflation projections are higher than previously thought as they signal they are on track to cut the policy rate only once this year. We think they will start in September with a high chance they end up cutting rates by more

Bottom Line at the Top Line Markets reacted positively to this morning's Consumer Price Index (CPI) release. Softer inflation is good news for the Federal Reserve (Fed). Despite a good report this morning, the Fed will still likely communicate this afternoon their intentions to keep rates higher for longer in their updated Summary of Economic Projections. The updated dot plot will likely signal only two rate cuts this year, a change from the three cuts communicated back in March.

Key Points

Consumer prices were unchanged in May after rising 0.3% in April.

Bond yields dropped to their lowest levels this week (highlighted in the chart below) and stock futures rose after the release since it relieved some of the pressure the Fed had after the payroll report.

The headline energy component fell 2% from a month ago, driven by a 3.6% decline in gas prices.

Airfare, new car prices, and clothing were among the categories that decreased in May.

Grocery prices were unchanged in May after falling in April, giving some reprieve to consumers, although price levels are still extremely high.

Restaurant prices continue to rise as consumers have an insatiable appetite for going out to eat. Looking ahead, this category may be an important leading indicator for consumer sentiment amid a slowing economy.

Nautilus Research: Best Fitting 3-year Analogs for U.S. 30-year Treasury Yields Historical precedents suggest lower yields.

When we match the trajectory of U.S. 30-year Treasury yields with past periods, it indicates that the current three-year pattern resembles times when yields were at the final stages of a topping process and resolved significantly lower over the next 12-months.

Nautilus’ Analog

Function specializes in recognizing patterns. Using its unique algorithm, it compares present price movements with historical data to predict potential outcomes.

The chart highlights historical periods closely linked (minimum 50% correlation) to the current pattern. Additionally, the table summarizes the expected returns from these correlated periods.

The Composite Pane displays an evenly combined path of all historical analogs.

In conclusion, pure pattern recognition suggests a trend towards lower U.S. yields...

… Relative attractiveness: The decision to overweight equities cannot be made in isolation, as it can only be achieved by underweighting another asset class. We expect that we are in the early stages of a period of higher inflation and higher interest rates. Structurally, this argues for a lower weight in traditional fixed income compared to stocks and cash. But comparing valuations across asset classes suggests that some of this may already be reflected in markets. While some may take issue with comparing equity earnings yields to bond yields, the comparison gives you a sense for how the relative valuations have trended over time. Interestingly, the S&P 500® earnings yield is now lower than 10-year Treasury yields for the first time since the Financial Crisis and lower than cash yields for the first time since the Tech Bubble. Similarly, the S&P 500® dividend yield hasn’t lagged cash yields by this much since the 1980s!

We see enormous opportunities within the stock market despite some challenges for the asset class

Given the bifurcated equity market, equities as an asset class are not particularly attractive relative to bonds and cash. However, specific equity themes seem very appealing. Our portfolios currently reflect that dilemma, with a somewhat modest overweight in equities, but with sizeable exposures to the themes we believe are historically attractive.

WolfST: Beneath the Skin of CPI Inflation: A Stunning Outlier Services CPI Drove Down Everything Else

Services are big, and that one-month outlier was massive, and it drove down Core CPI and overall CPI.

Jeffrey Gundlach - Fed Day

https://youtu.be/1wRRR8NpDNc?si=baFN6ZGoXrEf2MKu

Rickards is guest posting on The Burning Platform?! That's as good a sign I've seen provided by the Heavens in ages!