Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

No football, pitchers and catchers report (not)soon(enough and here we are …

Sorry. NOT sorry … by now this is NOT news …

CNBC: Trump tariffs on Canada, Mexico and China begin Saturday, White House says

CNBC Live updates: Trump to impose tariffs on Canada, China and Mexico

… reminder (which you don’t need) why this matters …

CNBC: Dow closes 300 points lower Friday as White House says tariffs will start Saturday: Live updates

Moving on TO how the day / week and month ended and what, if any message can be gleened from RATES … In this case, I’ll look at 5s (as we already had a look at bonds thanks to Kimble HERE, earlier in the week AND there’s some interest — MS below — in the belly) …

5yy MONTHLY: support just above 4.65% while we’re retracing back down TO an uptrending line — a break lower from here would be bullish …

…momentum adjusted from overBOUGHT and now nearing overSOLD but not YET screamin’ BUY and so, caution warranted, awaiting further dipORtunities …

AND I couldn’t help but look at long bonds myself and so …

30yy MONTHLY: double toppy … and happening at / near levels Kimble noted back in 2007 — a good spot by him …

… momentum (stochastics, bottom) appear to have become less overBOUGHT but are by now means screaming BUY, at least not yet, to ME so … await further dipORtunities…?

NEXT up data …

ZH: Headline PCE Inflation Continues To Rise; Savings Rate Revised Down... Again

CalculatedRISK: Personal Income increased 0.4% in December; Spending increased 0.7%

… putting PAID to idea expressed in recent days that last weeks FOMC was, in fact, a hawkish pause and not a dovish one. AND as the day / week and month came to an end, a quick recap …

ZH: Trump 2.0 Sparks Best January For Gold In A Decade; Bonds, Bitcoin, & Big-Tech Bounce-Back

January looked like a goldilocks month for macro data with 'growth' data surprising to the upside, and 'inflation' data surprising to the downside (even though today's PCE was more 'sticky' than many hoped for). But, as Apollo Global’s Chief Economist Torsten Slok commented on inflation under the headline “The US Economy Is Strong” concluding that "the narrative that the economy is slowing and inflation is moving down to 2% is wrong.”

…All of the US majors ended higher in January with (unusually) The Dow leading the charge as Nasdaq lagged. This is the best start to a year for The Dow since 2019 …

… Bonds had a wild ride in January, starting the month with yields surging higher (Trump tariff fears), then as inflation data started to come in weaker than expected (and DeepSeek's gut-punch prompoted safe-haven flows), yields fell and ended the month lower...

Source: Bloomberg

On the week, yields were lower but only just, as today's Trump tariff headlines sent yields higher...

Source: Bloomberg

… Alrighty, then.

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

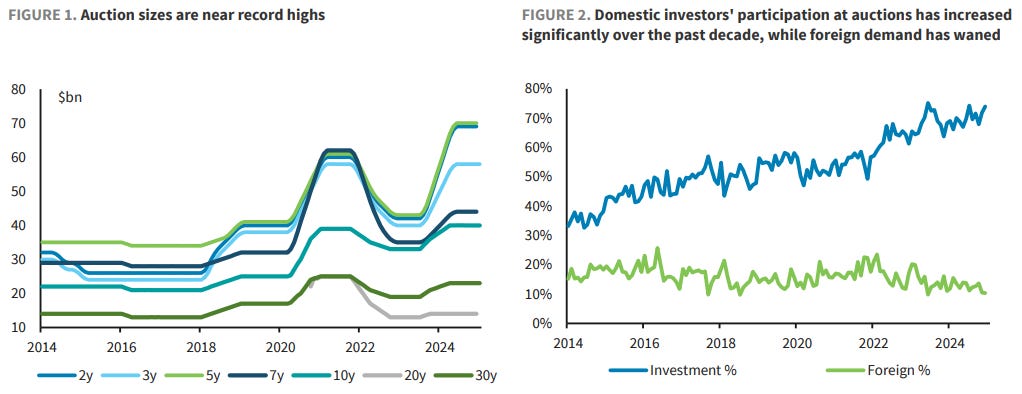

First up a global RATES weekly with excerpts on the US section given it’s dedication — albeit a look BACK — to investor demand for USTs in 2024 … hey, at least we are jumping into this weeks reFUNdingin on strong footing …

In the US, the Fed is in wait-and-see mode but has an easing bias. The Treasury could tweak guidance at the refunding meeting. In Europe, ECB steered clear of any hawkish messages, keeping its data-dependent approach. In Japan, we expect carry on FX-hedged foreign bonds to improve sharply in 2025…

…United States: Treasuries 2024 Treasury auctions: Domestic investor demand at new highs. . . . We review auction demand in 2024, with the Treasury keeping auction sizes of nominal notes/ bonds unchanged for much of the year. Demand was led by domestic funds, with their share increasing to 70%, the highest on record, while foreign demand moderated further. Long-end auctions tailed more in H2.

Here’s same shop w/a(nother) economically driven look at the week ahead …

DeepSeek news startled some tech stocks and intensified the US-China AI rivalry , but it could ultimately be positive for growth globally. Meanwhile, Fed and ECB rates diverged further, reflecting economic momentum. Focus now turns to Trump's tariffs, the BoE, US payrolls, and European inflation.

…US Outlook When will the hammer drop? A big week of data and news culminated with strong indications that the US could finally drop the hammer on tariffs, with levies on Mexico, Canada, and China. Powell's Q&A signaled that the FOMC feels no urgency to adjust rates as it awaits clarity about federal policy, implying an extended pause.

Private spending is carrying plenty of momentum, for now, with the advance GDP estimate placing Q4 growth at 2.3% q/q saar, led by a robust 4.2% rise in consumer spending. Strong PDFP and carryover effects from a strengthened monthly PCE trajectory bode well for solid spending to continue in Q1, though tariff front-running and a strong dollar may divert some to imports.

We think a 25% tariff on Mexico and China would likely blocked by a court injunction. But if the "hammer" is dropped, we estimate that it will boost CPI and PCE price inflation by about 10-15bp (%y/y), relative to our current placeholders, after various offsets (including dollar appreciation and trade diversion). It would also subtract about 25-50bp from GDP, in our view.

The main message from the FOMC was that the Committee feels no urgency to adjust rates with activity still on a solid trajectory and given elevated uncertainty about federal government policies (including trade and immigration) and their effects. Barring a significant weakening in the labor market, we see them delivering only one 25bp cut this year, in June.

In as far as THE bank of the land with a rates weekly winning catchy title of the weekend …

BofA Global Rates Weekly: DurationSeek 31 January 2025

The View: Confirmation bias Today’s EA inflation prints may already allow markets to regain confidence in the EUR disinflation story, especially after the ECB. In the UK, watch BoE forecasts for pushback against market pricing. In the US, all eyes on payrolls

Rates: US duration “DeepSeek” US: We expect rates to be range bound and hold a soft long duration bias. Focus less on term premium and more on asset swaps. UST refunding = hold, watch coupon guidance.

US duration “DeepSeek” …We hold our core rate views. We expect US rates to be relatively range bound; since the election US 10Y has traded between 4.2-4.8% & we expect this range to hold until US data meaningfully shifts. We keep our soft long duration bias, especially if rates shift back towards upper end of recent range. Logic for our soft duration long bias (1) high bar for Fed hikes (2) 10Y to struggle to breakout meaningfully above 4.8% unless Fed hikes priced (3) downside macro risks stemming from elevated economic policy uncertainty vs high US growth & risk asset optimism. We also continue to expect slow steepening of the 5s30s curve, flattening of the swap spread curve (wider front-end spreads with debt limit driven bill cuts & slow tightening of back-end spreads with elevated UST supply), & slightly elevated vol in short tenors / short expiries.

… Bottom line: We hold our core rate views. We expect US rates to be relatively range bound & hold a soft duration long bias. Treasury supply / demand dynamics are better proxied by the spread between UST yields and a similar tenor OIS rate, not term premium. We expect the February refunding announcement to be relatively uneventful; focus will be on coupon size forward guidance & UST cash balance outlook…

…Technicals

Short-term top formations in US yields have formed, such as a head and shoulder tops for US 5-, 10- and 30- year yields.

For 10Y yield, it suggests a February decline to +/- 4.30% while below the risk-off gap down in yield on Jan-26 at 4.60% and/or the right shoulder high at 4.66%

After the resolution of this pattern we can access whether US 10Y yield will still retest 5.00% by US Memorial Day, which has been a medium-term target.

Here I’d note / highlight best in biz booked profits in front-end long (FFF6 Monday) but remains stuck in 2s10s steepener (vs 35bps) and considering adding TO this (at 22bps which is 50dMA)

In the week ahead, Treasury investors will have an array of fundamental updates from which to derive trading direction. Friday’s combination of NFP/UNR and the benchmark revisions to the payrolls series is arguably the most relevant for the forward path of Treasury yields…

…As for Friday's BLS data, the consensus is for headline NFP to have increased by 150k jobs with an unchanged UNR at 4.1%. On the benchmark revisions, estimates are in the -650k to -700k range. An improvement from the initial projection of -818k, but still a downshift that will, at least partially, offset the resilient labor market narrative. That being said, as demonstrated by the pace of Personal Consumption during Q4 – US households continue to drive the real economy with no signs of waning in the near-term. In this context, it is worth highlighting that during December, the Savings Rate declined to just 3.8% from 4.1% in November – this marked the lowest since late-2022…

…Technical Analysis …10s – 10s are drifting toward the bottom of the recent yield range, and we’re encouraged by the drop below 4.50%. Daily and weekly stochastics are into overbought territory, although not dramatically so. This suggests that there is further room for the move to extend before requiring a period of consolidation or correction. The passage of monthend demand and the looming Refunding Announcement could prove triggers for a reversal. Initial resistance is the local low-yield print at 4.484%, followed by the Bollinger Band bottom of 4.463%. Through there isn't much before volumes near 4.40%, and then the 4.25% level. Initial resistance is the 9-day moving-average of 4.563% followed by an opening gap at 4.599% to 4.621%. 2s/10s flattening momentum remains intact, and we’ll target a drop below 25 bp as an opportunity to scale into steepeners.

A note from France on this upcoming weeks NFP data and revisions (which would appear to offer a more MIXED, neither bullish nor bearish readthru to USTs if) …

BNP: US January jobs preview: Eye on future as revisions reshape past

KEY MESSAGES

We look for a rise in nonfarm payroll employment of 170k in January and a steady jobless rate.

We expect the annual revision to pare back job growth over recent history, but the household survey should show a significantly higher level of employment on account of revised population estimates.

Looking ahead, restrictive immigration policy and potential changes to federal hiring practices suggest that while job growth may slow going forward, the labor market is unlikely to loosen materially.

…More detail on the annual revision Payroll growth to be revised lower: In August 2024, the BLS announced that the level of payroll employment as of last March might have been overstated by 818k. That is 0.5% of the roughly 157 million then employed. The administrative data on which that is based is not infallible as a guide to the true number of workers, as it assumes all paperwork is lined up in unemployment-insurance databases. That is unlikely to be the case universally, especially for undocumented immigrants who entered the workforce in 2022-2024.

The newer Q2 2024 Quarterly Census of Employment and Wages (QCEW) report suggested the preliminary estimate was roughly correct (subject to the caveat above). That implies an average reduction of 68k/month to job growth over the 12 months through March 2024.

That would mean a revised pace of about 175k versus the 240k that current BLS data show – still solid, but less stellar. We assume reductions to the pace of job growth extend through 2024, but to a lesser degree (about 35k). That would put the trailing 3m average at 135k, lower than the current 170k. We are skeptical that revisions will cut payroll growth much more over recent history. The recent pace of GDP growth (about 3%) is consistent with job gains of 175k-200k/month…

Now you may be asking what to do with the French NFP analysis … and they came out with this next note a little before hitting send on jobs report and so, maybe there’s a method to the madness …

BNP: New dynamics for the yield curve | US Rates Insights

Treasuries: We explore two emerging dynamics for the US Treasury yield curve: (1) the close link between Fed policy pricing and term premiums means bear-steepening and bull-flattening will be more dominant than before and, (2) the risk of less “regular and predictable” issuance may limit extreme moves in the yield curve.

The recent strong and unusual link between term premiums and Fed pricing suggests that calling the recent rise in yields as just a term premium story is an oversimplification. It also suggests yields might be capped as long as there is no discussion of rate hikes – also our view. We favor being long 10s in the TIPS space, given an asymmetric setup for real yields.

One risk from the heightened focus on term premiums is that the US Treasury’s coupon issuance policy may become less “regular and predictable”. 2023 already has such a precedent, and such an evolution might be in line with the new Treasury Secretary Scott Bessent’s preference to handle issuance “deftly”.

Trade idea: Given these dynamics, we favor selling 6m2s10s ATMF CMS curve straddles.

Short duration: Our analysis of short-end rates suggests QT can continue longer than we had expected. We now pencil QT to end in June 2025.

Volatility: We maintain short 1y1y swaption versus 3m1y A +/-25 strangles to fade rich volatility while protecting against abrupt macro moves.

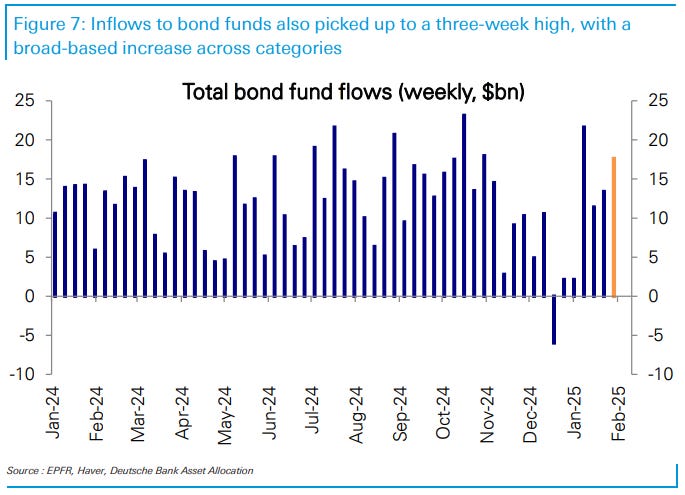

Pausing / interrupting Global Wall read on econ, rates and macro for a word on EQUITY FLOWS … with a visual of bond fund inflows — 3wk HIGH … hey now …

DB: Investor Positioning and Flows - Persistent Equity Inflows

Our measure of aggregate equity positioning continued to bounce in an elevated range with only a modest pullback this week (z score 0.78, 92nd percentile). Discretionary investor positioning fell but is still in the top decile (z score 0.85, 92nd percentile) while that for systematic strategies ground higher (z score 0.73, 83rd percentile)…

…Overall equity fund flows also jumped higher ($24bn) this week, with the bulk going to the US ($20.8bn). Beyond the strength in Tech fund flows ($6.5bn), those into Financials ($2.7bn) also surged notably to a 3-year high, helped by the strong earnings growth they have reported this season. Inflows to bond funds ($17.6bn) also picked up to a three-week high, with a broad-based increase across categories. As we have highlighted previously, we expect the ongoing cross asset inflows boom to continue through this year (What’s Driving The Inflows Boom? Nov 1 2024). This is largely as ample cash balances allow households to allocate their new savings disproportionately to other asset classes, but equity inflows are crucially boosted by risk appetite which remains strong along with a favorable macro and earnings backdrop..

Same shop and for even MORE on stonks …

DB: Asset Allocation - Q4 2024 Earnings Takes: Growth Edges Up To A Three-Year High

Coming into the earnings season, we looked for S&P 500 earnings to grow 12.8% in Q4, in line with the low-double-digit growth rates of recent quarters and that is typical outside of recessions (Q4 2024 Earnings: Looking For Steady Low Double-Digit Growth To Continue, Jan 9 2025). About halfway through the earnings season, with 177 companies (50% of market cap) having reported, we see …

…Earnings growth up to a three-year high. Earnings for companies that have reported are up 7.5% yoy. If companies yet to report beat at the current rate, Q4 earnings growth for the S&P 500 is on track to end at 12.4% yoy, rebounding from 8.7% in Q3. This would be the strongest rate of growth in three years. Earnings growth for the median company is also tracking a three-year high of 10.3%. Energy continues to be a large drag on headline earnings growth, excluding which growth is tracking a robust 15.8%. Following the strong Q4, EPS for full-year 2024 is on track to come in at $253, 10.6% growth over 2023.

This last note from German shop is one with CHARTS and I’ll note just one …

DB: US Economic Chartbook - Monthly charts: The waiting game

…Easier financial conditions provide a tailwind to nearterm private demand growth

Moving back onshore to one of the nations fan favorite domestic bank CEOs shop … Jamie Dimon’s FI group says … STAY NEUTRAL (see positions visual) and favor 5s10s FLATTENERS …

JPM: U.S. Fixed Income Markets Weekly 01 February 2025

…Governments We unwound front-end longs earlier in the week: the Fed’s easing bias should anchor the front end, but OIS forwards are priced to our Fed forecast. Further out, valuations remain somewhat attractive, but long investor positioning is a near term bearish signal, so we stay neutral duration. Maintain 5s/10s flatteners. We preview the February refunding announcement, where we expect Treasury to maintain its current forward guidance and keep nominal auction sizes stable. We look for early signs of debt ceiling risk pricing. Considerable uncertainty remains regarding a potential Feb 1 tariff announcement. Stay neutral on front-end inflation but maintain 5Yx5Y inflation swap shorts…

…Treasuries Welcome back my friend to the show that never ends

The FOMC maintains an easing bias, but we don’t forecast another cut until mid-year, OIS forwards are priced to our Fed forecast, and yields are near their local lows

Term premium concerns have faded somewhat and we expect next week’s refunding announcement to be relatively neutral, but our Treasury Client Survey has moved to its longest levels since October 2010

Hence, we unwound our front-end duration longs earlier this week and stay neutral on duration. Along the curve, we maintain 5s/10s flatteners …

… while rates investors have extended duration, perhaps supporting the retracement from this month’s yield highs, position technicals have become a headwind for a further decline in yields. Our latest Treasury Client Survey, released earlier this week, has moved to its longest levels since October 25th, 2010. We have historically viewed positioning indicators in a contrarian manner when they reach extreme levels. Specifically, we have found that the Treasury Client Survey Index can be used to trade duration in a contrarian nature, with sharp moves in the 1-year z-score of the 4 week moving average of this index providing a good signal for tactically taking the opposite position (Figure 15Our TeasyClint Surveyhas xtendirc weks,and owstand ilogest vlinceat-201, see Survey says: Using the Treasury Client Survey to predict rate moves, 7/21/23). Thus, with the survey flashing a bearish signal, this warrants caution, even with valuations flagging as somewhat cheap. On balance, we recommend maintaining a neutral stance on duration over the near term.

Turning to the curve, we continue to favor 5s/10s flatteners for two key reasons. First, the intermediate sector of the curve has tracked medium-term Fed expectations, steepening as front-end yields fall and vice versa. However, 5s/10s diverged sharply from the level of 2-year yields as the bearish steepening unfolded in early-January, and remains too steep on this basis (Figure 165s/10 remains toeprlaiv tohelfrnt-d yiels.). Second, 5s/10s has tended to be more volatile than 10s/30s over the last year, but appears steep on this basis as well...

These words, while NOT from the ‘best in the biz’ ARE from a group who I cannot stress enough, I find to continually offer amazing insights … so happens they are very bullish of bonds (and so too is HIMCO and if you read through BMO above …) and they remain long, lookin’ to BUY MORE (5s) and note they DIFFER in view on the curve in that they’d prefer to AVOID steepeners …

MS: Buy More Treasuries On Tariffs | US Rates Strategy

If the US implements broad-based tariffs on Canada, China, and Mexico this weekend, we expect the US Treasury market – the most deep, liquid, risk-free investment in the world – to act as a release valve for any tightening pressure that builds in other financial markets like the USD and equities.

Key takeaways

The White House press secretary said on Friday the president would implement a 25% tariff on Mexico and Canada, and a 10% tariff on China, on Saturday, Feb. 1.

We expect tighter financial conditions led by the USD strengthening and, initially, US Treasury yields rising as investors worry over the inflationary impact.

We think investors should use any rise in Treasury yields to add more high-quality duration to their portfolios at the 5-year key rate duration point.

Avoid yield curve steepeners because investors may see FOMC reaction function as less dovish than before. Tighter financial conditions raise flattening risk.

Details of exact tariff implementation should determine the extent of the opportunity to increase duration exposure. Broader tariffs = bigger opportunity.

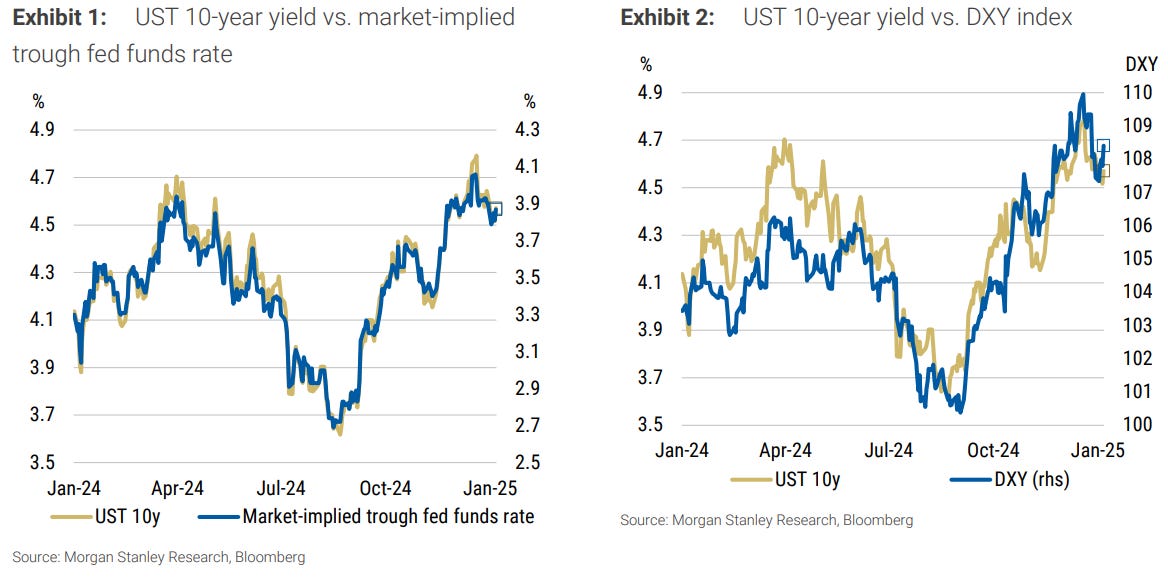

…You may think, if the Fed doesn't continue to lower rates, then the market won't be able to price in a lower trough rate for policy. And if the market-implied trough policy rate doesn't decline, then Treasury yields further out the curve won't decline either (see Exhibit 1 ).

You also may think that a stronger US dollar might align with higher Treasury yields. After all, the strong relationship between the two has lasted for over a year now (see Exhibit 2 )

In the end, though, your experience with macro markets affords you variant perception. You understand the interconnected nature of the world – functionally, economically, and financially. You also understand the nature of how financial conditions form…

…What do we think about the opportunity, you ask? We think investors should use any rise in Treasury yields to add more high-quality duration to their portfolios at the 5-year key rate duration point.

We also think investors should avoid yield curve steepeners because investors may see FOMC reaction function as less dovish than before. To us, tighter financial conditions – led by a stronger USD and lower equity prices – increase overall curve flattening risk…

Same shop offers robust discussion on SUPPLY as this is as important, near and dear to me as are positions and DEMAND … and so …

February Treasury refunding could ignite a sentiment sea change about Treasury supply. We expect no increases to coupon sizes at this refunding, nor over the remaining quarters in 2025, as we find reason for more, not less, T-bill issuance.

Key takeaways

We expect Treasury to maintain current coupon auction sizes over the February refunding quarter.

We address common counterpoints to our view that Treasury will not increase coupon sizes throughout 2025.

We examine coupon auction results over the previous quarter and find signs of stronger demand, but TIPS auctions have been meaningfully weaker.

Same shop with an NFP precap … more than just LA fires, too, mind you, we’ve got to be thinkin’ benchmark revisions (as BMO noted)

MS US Economics: Employment Report Preview: Wildfires likely slow January payrolls

Net headwinds to January payrolls should slow gains to 140k: wildfires (estimated -40k); a swing toward colder weather (-30k); a new strike (-5k). Wages probably continue to moderate, +0.3% m/m and slowing by 0.2pt to 3.7% y/y. The unemployment rate is probably unchanged at 4.1%.

… Benchmark revision to payrolls. In this year’s revision, March 2024 payrolls are likely to be revised down by about 818,000, or about 68k per month on average. Operationally, this means the level of payroll employment in March 2024 will be revised lower, and changes will be applied to monthly payrolls from April 2023 to March 2024 that sum to this amount. We expect minimal revisions to payrolls since last March…

Woah, big fella … slow down and DONT be in such a hurry (Fed TO markets this past week) and this next note made ME pause to read / investigate bit further …

…Interest Rate Watch: In Little Hurry to Cut Further As universally expected, the Federal Open Market Committee (FOMC) left its target range for the federal funds rate unchanged at 4.25%-4.50% on Wednesday. The post-meeting statement continued to note that "economic activity has continued to expand at a solid pace." Indeed, Thursday's GDP report showed the U.S. economy expanded at a 2.8% average annual rate in 2024, just below its 2023 pace and above the average pace that prevailed in the business cycle before the pandemic (2.4%).

In view of the Committee's dual mandate of maximum employment and price stability, the statement went on to characterize labor market conditions as "solid." The description represents an upgrade from the December statement, which said that "labor market conditions have generally eased." On the price side, the statement simply said that "inflation remains somewhat elevated." The year-over-year change in the core PCE deflator, which Federal Reserve officials believe is the best measure of the underlying rate of consumer price inflation, has trended sideways in a tight range of 2.6%-3.0% throughout 2024 —noticeably above the FOMC's 2% target.

In sum, there was little in Wednesday's statement to suggest the FOMC is contemplating another rate cut soon. The latest Summary of Economic Projections, released in December, showed the median Committee member thought an additional 50 bps of rate cuts would be appropriate by the end of 2025. If the FOMC views only 50 bps of rate cuts by December as appropriate, then it clearly does not need to be in a hurry to cut rates.

As highlighted in our latest U.S. Economic Outlook, we look for the FOMC to maintain its current target range for the federal funds rate until the second half of the year. Chair Powell noted in his post-meeting press conference that policy "is significantly less restrictive" today than it was before the FOMC started to cut rates, which "means we do not need to be in a hurry" to ease further.

With inflation remaining stubbornly above target and real economic activity holding up reasonably well, we see little reason for the FOMC to cut rates in the near term. Yet with the level of policy today still somewhat restrictive, albeit not as restrictive as a few months ago, we maintain our view that the FOMC will lower its target range by 50 bps this year (25 bps in September and another 25 bps in December). Thereafter, we look for the FOMC to maintain its target range at 3.75%-4.00% through the end of 2026.

… Moving along TO a few other curated links which maybe useful …

First up only for allstars of the charts and of course, for those believing only and forever in stocks for the long run …

AllStarCharts: Whenever they say "Tariffs" Buy More Stocks

Ok, so China stonks not for me but this next note’s auther remains consistent with regards to the US ECON and so, there’s likely a readthru to equities, I’d imagine …

On Monday, we will get manufacturing ISM for January, and it is likely to show a big jump higher, see charts below. Based on the historical relationship with the regional Fed ISM indicators, the nationwide ISM could increase to 54, a level which would be consistent with first-quarter GDP growth of 3.4%.

The strong momentum in the economy is driven by high stock prices, high home prices, and strong tailwinds to growth from tech capex spending, defense spending, and spending driven by the CHIPS Act, the IRA, and the Infrastructure Act.

Combined with low jobless claims and higher animal spirits since the election, the bottom line is that the US economy is entering 2025 with accelerating momentum.

The narrative that the economy is slowing and inflation is moving down to 2% is wrong, see again charts below.

Being a fan of super thoughtful charts and generally speaking, a visual learner, this next note / CHARTS are, in my view, worth our collective attention, agree (tariffs = inflation) or NOT …

…Interest Rates In the last Friday Speedrun, I made the argument for why bonds should rally on a tariff announcement. It’s an easy argument to make because that’s what happened in 2018 and 2019, and after Smoot-Hawley (of course!). The confidence shock of tariffs can easily outweigh the temporary change in the price level. In the interest of full disclosure: I changed my mind. One of the worst diseases you can get in financial markets is the inability to change your mind. If you commit to the belief that a recession is coming (or already here) and then refuse to acknowledge new information as it comes in… Guess what: You will keep seeing recession around every corner. You might even torture the current data to “prove” we just went through a recession, even as stocks and yields climbed the whole time. That’s bad.

There is a tension between flexibility and flipfloppiness and honestly I would rather flip flop a bit too much than be stuck in stale views with a rigid mind possessing no Bayesian plasticity. Better flip flops than confirmation bias, every time. Keep re-aiming the bow until you think you’re on target. That’s my philosophy. When the facts change, or when you come to some new realization… Change your mind! You can always change it back.

For an explanation of why I changed my mind on the inflationary impact of tariffs, let me post an excerpt from am/FX this week.

Maybe tariffs will be inflationary this time

Psychology now is not like it was in 201

I changed my mind

Nick Timiraos had a good article in the WSJ overnight and it has changed my mind on the bond market impact of tariffs. The article is here. There are two ways you can look at the bond market impact of tariffs.

One: Look at recent history. Almost every tariff announcement in 2018 and 2019 saw bonds rally. This is a pretty good starting point for what bonds might do now. The equity-negative fear factor was larger than any inflation worries on those announcements and you could argue that’s the case today, too. I have argued that in am/FX and on the podcast with Alf in recent weeks.

Tariffs create a one-time price change that could be viewed as similar to a tax hike. It’s a step higher in the price level, but not really “inflation” per se. It also creates a negative confidence shock as foreign retaliation and risk of escalation can freeze investment in export-focused industries. Obviously, Smoot-Hawley is the textbook manifestation of a confidence shock as tariff increases (and about 20 other factors) led to a collapse in confidence and a deflationary spiral.

So that was my view. Tariffs are bullish bonds because the Fed will look through them and the economic confidence damage is greater than any one-time price level change. Until I read the Timiraos article.It changed my mind to: Two: Psychology has changed and tariffs will be inflationary. I think the key point is that inflation is a psychological phenomenon. Companies didn’t even have “raise prices more than 2%” on their list of options between 2008 and 2020. Then, the restaurants in my town realized that they could raise the price of the salmon from $17 to $22 to $31 and people would just keep on buying. An extra $9 in Uber fees and such? No problem. I’ll take two and have one for lunch tomorrow.

Even if they lost the most price sensitive 15% of their customers, the 82% menu price increase more than made up for it. This is the concept of Price over Volume or PoV that Sam Rines made famous in 2023. Companies now understand that they increase profits by sacrificing some volume to juice margins. Here’s Timiraos:

The last time Trump was president and imposed tariffs on trading partners, expectations of future inflation were low and firmly anchored—or set in dry cement. The public had little experience with inflation, and that made businesses more hesitant to pass along price increases from tariffs.

“They didn’t know how much business they would be losing” if they raised prices, said Hammack.

But several years of high inflation triggered by the pandemic and a policy response that showered the economy with ultralow interest rates and fiscal stimulus have raised questions over whether the Fed could be as relaxed about an increase in prices. If the cement is wet, expectations of higher inflation in the future could sustain higher price growth.

Because corporate management teams have been passing through higher costs, they have the experience of raising prices that they lacked five years ago. Even domestic producers that aren’t hit by tariffs could use higher import prices as an excuse for raising their own prices.

Sure, the dollar can strengthen to partially offset the inflation, but the nefarious aspect of scaled tariffs could be that they stoke inflationary expectations by putting a floor under prices, changing corporate pricing psychology, and creating a world where consumers know prices are going to stair step up, up, up as the tariff vise tightens. This could lead to front-loading, panic buying of tariffed goods, and all the usual inflationary demons that run around in central bankers’ nightmares.

End of excerpt…

AND somewhat more on ‘flation, as it FESTERS … from Da WOLF …

WolfST: Inflation Festers in Core Services, No Progress in 12 Months. PCE Price Index Accelerates for 3rd Month: Justifies Fed’s Pivot to Wait-and-See

In a broader sense, there has been no progress at all on inflation in eight months.

…In a broader sense, there hasn’t been any progress on inflation since May (black box in the chart below), with the Fed’s favored inflation measures well above its 2% target, confirming the Fed’s pivot this week to a wait-and-see strategy.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

")