Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this <UNSCHEDULED> note… … markets are closed tomorrow and I’ve got a couple / few things on MY mind so this note will NOT have much of the usual content / format.

In fact, I would like to lead with a visual spotted on the intertubes ‘bout a week ago and which I finally found the source (for linking / credit purposes) and as you know, I’m a BIG fan of visuals and context and so here’s some long-term history of rates (via Goldilocks) …

GS Top of Mind: HIGH BOND YIELDS: HERE TO STAY? ISSUE 135 | February 5, 2025

Despite the start of long-awaited central bank easing cycles, G10 bond yields have reset higher in recent months, led by the US. What accounts for this unusual behavior, and will yields remain elevated amid tariff and broader economic developments? PGIM Fixed Income’s Gregory Peters, MIT’s Ricardo Caballero, and GS’ David Mericle and William Marshall express varying levels of sympathy for the drivers of this reset: a reassessment of the inflation/Fed outlook, the neutral rate, and the term premium. While Peters argues that persistently above-target inflation should help support 10y Treasury yields closer to the top end of their recent 3.5-5% range, Marshall believes the further underlying disinflation Mericle expects should help yields end the year around—or modestly below—current levels. Looking further ahead, Caballero argues that 10y rates could settle well below current levels as he believes the future neutral rate could prove lower than many think. But with the risks skewed toward higher rates, we explore the implications for risky assets and portfolios if bond yields surge again.

Read the entire 25p note if you hadn’t stumbled on this Feb 5th note until now.

If you don’t, thats fine too, but do take away one thing … no matter what you see and gravitate to on the annotated chart chart above.

10yr yields AVERAGED 4.40% since 1790 (so, 235yrs) and we closed the week just past at 4.478% …

That’s not even a rounding error…and at same time very interesting we’re ‘holding’ and once again offers context to how very important 4.50% is for 10yy … not only to me, but all of us (see MSs stock jockey below, for current example).

And it is with this visual context in mind, everything else then is part of the pricing mechanism creating the next 100s of years on the chart …

With the week just past, lots of debate about residual seasonality (strong CPI) but very little about same ‘seasonality’ issue with regards TO ReSale Tales.

To ME that is evidence of bias — folks seeing what they wanna see.

Maybe I’m wrong and clearly don’t have more letters after my name than IN it, as many of my former colleagues and clients, but it just strikes me as interesting.

Bonds remain IN a range and over the holiday long weekend, i’ve spent time listening to a couple things which I’d highly recommend.

First, from the best in the biz, BMOs weekly podcast which puts voice and some puns to their weekly note … This weeks as good as any and highly recommend …

As the market continues debating how to translate CPI, PPI, and Import Prices into core-PCE and supercore, we’re reminded that once the Fed excludes all of the components of inflation that are particularly volatile – things don’t look that bad. Well, not unless one eats, lives in a home, or needs to fill up the tank. We're looking forward to the inevitable attempts to view inflation in ex-tariffs (or Trump) terms.

Episode 311: "Short Week, Long Bonds" is now available. This week, the team discusses the conflicting messages from CPI and PPI, as well as Powell's Congressional testimony. In addition, we ponder what is on the near-term horizon for Trump's trade agenda…

… As good as they are for the here and now, I’d also then add to the mix latest MacroVoices as this past weekly guest was none other than Jim Bianco. Lots of talk about gold and reserves (there or not?) and if monetized, would provide USAs sov wealth fund (?) something of some seed money (just south of a trillion). Not chump change and again, have a point / click and listen to all this in HIS own words …

MACROVoices #467 Jim Bianco: The Mar-a-Lago Accord

These can be found on iTunes and whatever / however else one ‘subscribes’ to them.

I hope you find something (above / below)of use and I’ll move right along …

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

We see the Fed as comfortably sitting back and waiting for conviction on its next policy move.

The flow of tariff news, and the administration’s expansive definition of “reciprocity,” suggest upside risk to our tariff expectations.

2s10s flatteners and long 10y TIPS seem like appropriate expressions for greater confidence in federal spending cuts, lower long coupon supply and a “stagflationary” risk narrative.

… Improved sentiment around longer-term spending cuts is among factors that support our suggestion for 2s10s flatteners and long 10y TIPS. The recent downward surprise in coupon supply from TBAC and word of a possible SLR exemption for Treasuries suggest that the administration is delivering on Secretary Bessent’s emphasis on reducing long rates via term premia. In other words, a vigilant administration could keep bond vigilantes at bay. More generally, mixed evidence last week on growth and inflation has bolstered a stagflation narrative, which in turn has supported a flattening move.

Bond vigilantes drove higher term premiums, but face resistance from a bond-vigilant administration

… and another of Sunday’s best is this one for ‘the <equity> Greeks’ with a hat tip towards … RATES …

MS: Sunday Start | What's Next in Global Macro: Alpha Over Beta

Since mid-December, the S&P 500 has made little headway. The impressive run that started in the summer came to a halt for a number of reasons, but none as important as the backup in 10-year UST yields, in my opinion. In December, we cited 4-4.5% on the 10-year as the sweet spot for equity multiples, assuming growth and earnings remained on track. We viewed 4.5% as a key level for equity valuations. Sure enough, when the Fed became less dovish at its December meeting, yields crossed that 4.5% threshold and correlations between stocks and yields settled firmly in negative territory, where they remain. In other words, yields are no longer supportive of higher valuations – a key driver of returns over the past few years.

Instead, earnings are now the primary driver of returns, and that is likely to remain the case for the foreseeable future. While the Fed was already increasingly less dovish, the uncertainty on tariffs and last week’s CPI data could reinforce that shift, with the bond market moving to just over one cut for the rest of the year. Our official call largely aligns with that view, as our economists took the March cut out of their forecast recently. June is now the earliest they expect to see the next cut. It depends on how the inflation data play out.

Our strategy has shifted, too. With the S&P 500 facing headwinds from rates and earnings revisions breadth now rolling over for the index, we have been more focused on sectors and factors. In particular, we’ve favored areas of the market showing strong earnings revisions on an absolute and/or relative basis – Financials, Media/Entertainment, Software over Semis, and Consumer Services over Goods. Within Defensives, we have favored Utilities over Staples, REITs, and Healthcare. While we’ve seen outperformance in these trades, we are sticking with them for now. We also maintain an overriding preference for large-cap quality unless back-end rates fall sustainably below 4.5% without a meaningful deterioration in growth. For equity valuations, the key component of 10-year yields to watch remains the term premium, which has come down but is still elevated compared to the past few years. In contrast, last week's decline in yields was more a function of weak retail sales data, which is not helpful for equity valuations.

Other macro developments driving stock prices include the numerous policy announcements from the White House involving tariffs, immigration enforcement, and cost-cutting efforts by DOGE. On tariffs, we think they will be more of an idiosyncratic development for equity markets. However, if tariffs were to be imposed on China, Mexico, and Canada through 2026, we estimate that the impact on consensus forward EPS would be around 5-7% for the S&P 500 – not insignificant. Industries facing greater headwinds from China tariffs include Consumer Discretionary Goods and Electronics. Lower immigration flow (and stock) seems more likely to affect aggregate demand than to become a wage cost headwind for public companies. Finally, skepticism remains high regarding DOGE’s ability to cut federal spending meaningfully. I am more optimistic on that front, but realize greater success also creates a headwind to growth before providing a tailwind via lower fiscal deficits and less crowding out of the private economy – factors that could lead to more Fed cuts and lower back-end rates as term premium falls.

Bottom line, higher back-end rates and growth headwinds from the stronger dollar and the initial policy changes suggest that equity multiples are capped for now. This means stock, factor, and sector selection remain critical to performance rather than simply adding beta to one’s portfolio. On that score, we continue to favor earnings revisions breadth, quality, and size factors alongside Financials, Software, Media/Entertainment, and Consumer Services at the industry level…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Here’s a question from a technical ‘guru’ and self-proclaimed / named all star of charting … things like this are written and offered on the intertubes NOT to answer questions but rather to do ONE thing. Sell subscriptions. Read on …

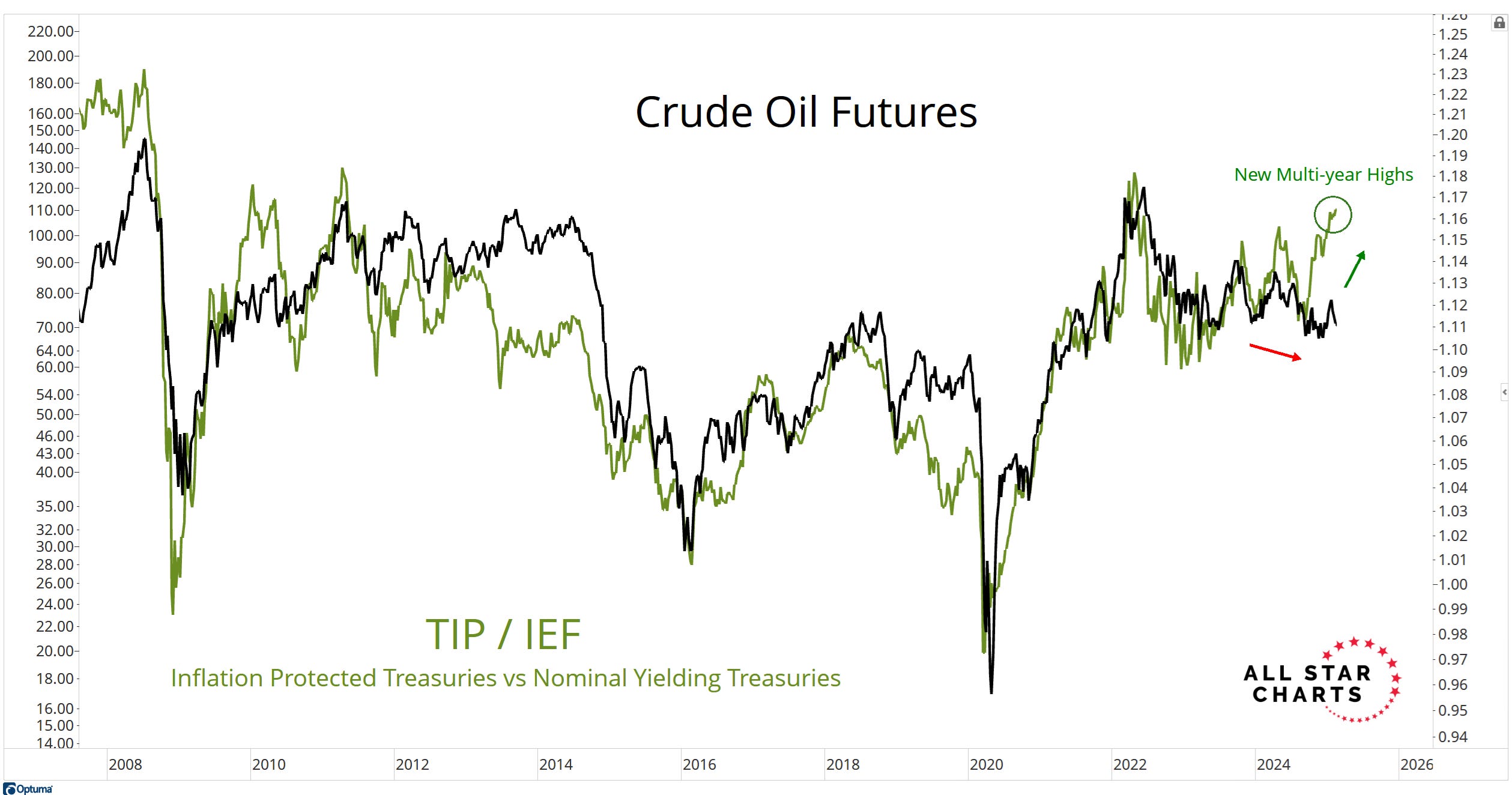

ALLSTARCHARTS: What Do Bonds Know?

f the bond market is like Shaquille O'Neal, the stock market would be like White Chocolate trying to find his spot all around the court.

That would make the Crude Oil Market like Mark Price or Ray Allen, over there in the corner waiting for their shot.

If you understand those references then this all makes a lot more sense.

For those who don't, the point here is that Shaq (bond market) is the big bully, pushing around all the others. So whatever the bond market is doing, we want to pay attention.

On Friday, we saw the Bond Market's inflation expectations hit new multi-year highs. In green, you'll notice the Inflation-protected Treasury Securities (TIPS) relative to regular nominal yielding Treasuries (IEF) going out at new highs:

Crude Oil has yet to get going. But these two dance together.

So what does the bond market know, that hasn't yet been priced into the Crude Oil market yet?

As you guys know, I don't really trust humans. They're wrong a lot, and also make things up that simply aren't true. But I do trust dogs and I do trust the bond market.

So I'm listening.

All this is happening while the US Dollar just closed the week at the lowest levels since early December.

The bond market is pricing in higher inflation, suggesting that Crude Oil could take off next.

With Gold hitting all-time highs, Silver ripping and Copper dominating the returns this year, how far can Crude Oil be from a breakout of its own?

If this is indeed a commodities supercycle, I don't think it's going to be one without Crude Oil participating.

The question is, when and how do we play it?

That's where Breakout Multiplier comes in.

The Breakout Multiplier System was specifically designed to maximize the returns whenever opportunities like this present themselves.

Our China Trades are working, and I think both Energy and the weaker Dollar are all part of the story.

Of the 8 China-related trades that we've put out since the Election, ALL 8 TRADES HAVE AT LEAST DOUBLED IN VALUE!

Yes you read that right…

AND here’s a note from our modern-day Lacy Hunt …

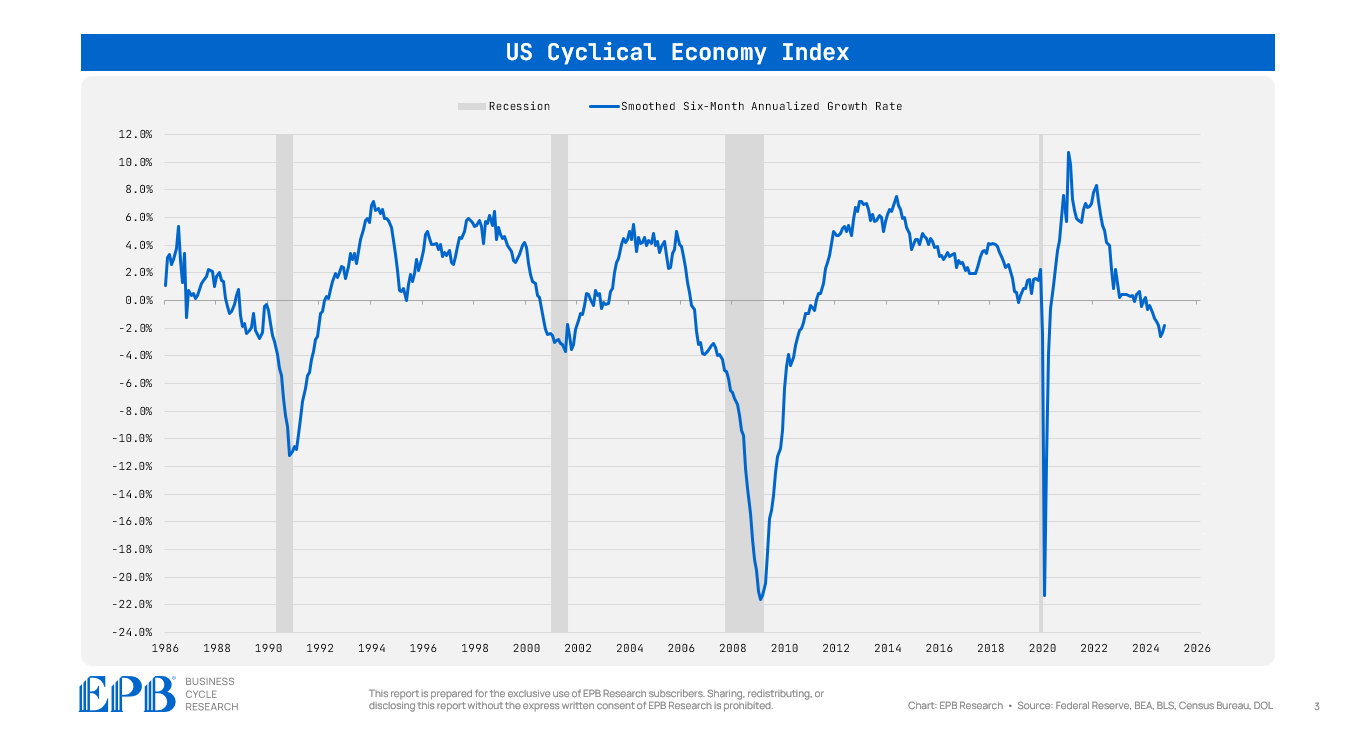

EPB RESEARCH: The Cyclical Economy: The Driver of Booms & Busts

… It’s often said that the Cyclical Economy sectors of construction and manufacturing don’t matter as much anymore as they are becoming a smaller and smaller share of growth and employment.

While it’s true that these sectors have become a smaller share of the economy over time, these sectors have extreme cycles, often declining 10%, 20%, or even 30% in a recessionary period.

The amplitude or swings in annual growth rates have ranged from +10% to -22% over the last several decades.

One of the biggest misconceptions in the post-2008 period is that the economy has avoided recession because it has been able to withstand declines in the Cyclical sectors.

This statement is empirically false and stems from a mismeasurement of the Cyclical Economy.

As the chart clearly shows, since the recovery after 2008, the Cyclical Economy has never declined, aside from the brief COVID lockdowns.

So it’s not that the economy avoided recession in spite of a downturn in construction and manufacturing; it’s very specifically because there was no downturn in construction and manufacturing.

The Leading Economy measures things like sales volume and new orders, and in that bucket, there were downturns and soft patches. However this bucket does not measure actual production or actual employment of these sectors…

POSITIONS. Lives. Matter. Specifically, those with positions in bonds and this weekend brought an update which caught MY eyes — large spec longs of duration JUMPED TO NET LONG …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

Finally, RIP, Rafterman …

… THAT is all for now. Off to the day job … enjoy what’s left of holiday LONG weekend!!

Rafterman has passed? At least he attended Charlie's last bday party 🤣! Funny thing been thinking I need to watch Full Metal Jacket again. Seriously great post & 10 yr hx chart. The basketball bond analogies cause me to remember James Carville's quote that he'd like to be reincarnated as the bond market to better Rule the World. Spoken like a true psychopath. Thanks for the Bianco tip that'll provide good listening while driving to the ski resort today 👌

Rafterman has passed? At least he attended Charlie's last bday party 🤣! Funny thing been thinking I need to watch Full Metal Jacket again. Seriously great post & 10 yr hx chart. The basketball bond analogies cause me to remember James Carville's quote that he'd like to be reincarnated as the bond market to better Rule the World. Spoken like a true psychopath. Thanks for the Bianco tip that'll provide good listening while driving to the ski resort today 👌