CSFB > svb … and so, another “ADULT SWIM!” sign posted as you walk in and flip on machines this morning. Here are some overnight thoughts / updates on moves from a friend,

Good morning. Asian equities are higher with the Hang Seng advancing 1.50%. European equity bourses, however, are off between 2-3% across the board. Chinese retail sales rose 3.5%YoY in February.

U.S. equity futures are are down about 1.50%.

Asian credit is tighter but European credit is meaningfully wider. EMEA Eurotrax IG is 7 bps wider and iTraxx Crossover is 27 bps wider.

European sovereign bonds are rallying with advances all over the map. Gilts are 10 bps richer but German bunds are 17 bps richer, Italian BTPs 9 bps etc. In Asia JGBs are off 13 bps demonstrating bifurcation in markets.

Eurodollar futures are also fractured with various moves. Late 2023 dates have rallied as much as 30 bps this morning but term markets are only 5 bps richer with almost all dates past Sept. 2024.

USD is three quarters of a percent stronger and emerging market and commodity based currencies are weakening. Norwegian Krona and Mexican peso as proxies are off 1.50%.

In commodities the base metals are lower with some bigger moves in palladium off almost 5%, copper off almost 2% etc. Crude and energy is also lower, crude by 1% and nat gas and regular gasoline off 3%. Heating oil is 2% lower.

Meanwhile, on heels of CPI, stocks remain overvalued, at least by one metric cited recently by Liz Ann Sonders

Rule of 20 (combines S&P 500’s P/E and CPI y/y) thru February continues to suggest stocks are overvalued

AND if stocks OVERVALUED then … TINA? Never mind … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have been all over the place this morning with 2yrs revisiting yesterday's highs ~4.40% just after 4am before plunging over roughly 40bp in the following 2 1/2 hours on amped-up fears over a bank across the pond MSN. DXY is higher (+0.8%) while front WTI futures are lower (-1.5%) after being higher earlier (see attachments). Asian stocks were mostly higher, EU and UK share markets are now deep in the red (SX5E -3.3%, SX7E -7.5%) while ES futures are showing -1.7% here at 7:11am. Our overnight US rates flows saw a 'welcome reprieve from mayhem' in Asian hours; a calm that lasted mere hours. Asian flows were muted with the front-end materially softer, and the curve flatter, during their hours. But London's AM hours saw an orderly start that turned to chaos with the desk seeing better selling from real$ accounts (intermediates). Colleagues also reported ongoing and strategic buying of off-the-run paper on ASW. Overnight Treasury volume was ~185% of average overall.

… It's therefore of little surprise that the MOVE index (index of 1mo Tsy vol, see first attachment) has passed its pandemic peak and now sits at the highest level seen since the GFC. The Minutes from the upcoming FOMC meeting should make a fascinating read, for sure. Bloomberg's connorsen this morning: "If you have a friend or loved one who knows what SOFR futures are they haven't slept since Saturday." lol

… Data dependency to banking conditions dependency?? We'll see... Our last attachment this morning looks at the yawning and expanding gap between money market yields and bank savings rates. The siren song that could lure cash out of deposits and into money funds/short Treasuries blares, it seems.

… and for some MORE of the news you can use » IGMs Press Picks for today (15 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

First, an appropriate sounding place to start from a large German bank,

Although investor concerns have eased overnight and banks have rebounded, several markets remain dislocated. Today, we are watching several signals for further signs of an easing or mismatch.

Signs of weakness in commercial real estate markets - listed real estate stocks underperformed yesterday despite the broader easing of risk constraints.

Private capital managers - yesterday's rebound in the share prices of large firms glosses over the risks in the much larger mid-tier segment.

Spreads on high-yield tech debt - these shrank yesterday but remain at elevated levels and proxy for some dislocation in private markets and the financing supply chain of the tech industry.

Haven assets - we watch for how any further falls match up with equivalent gains in risk assets or whether a mismatch indicates investors concerns.

The slope of the yield curve in treasury and bund markets ahead of upcoming Fed and ECB meetings.

From SVB and dust settling TO CPI — this from BBG … I mean a large French bank

Main takeaway: The Fed still has an inflation problem. Core inflation accelerated sequentially in February (0.5% m/m from 0.4% prior), driven by the strongest increase in the key non-housing services component since September 2022. Prices gains were again broad-based throughout both goods and services.

Inflation fight far from over amid financial stability concerns: While banking sector developments will factor prominently in policymakers’ calculus, those inclined to pause and assess did not receive any additional cover in the February CPI report.

Our bias is for the Fed to continue to lean against inflation: The hot February CPI report underscores how far the Fed remains from its price stability goals. Though financial stability considerations will likely preclude a 50bp move, we think the February CPI report should keep the Fed on track to deliver a 25bp hike. Of course, market functioning and financial stresses now play a larger role in the calculus—so the next several trading sessions will prove influential.

Overall business conditions continued to improve in March. Survey respondents reported better labor supply in select industries, such as construction and restaurants. Cost management initiatives such as layoffs and hiring freezes remain a key focus among companies in response to margin compression.

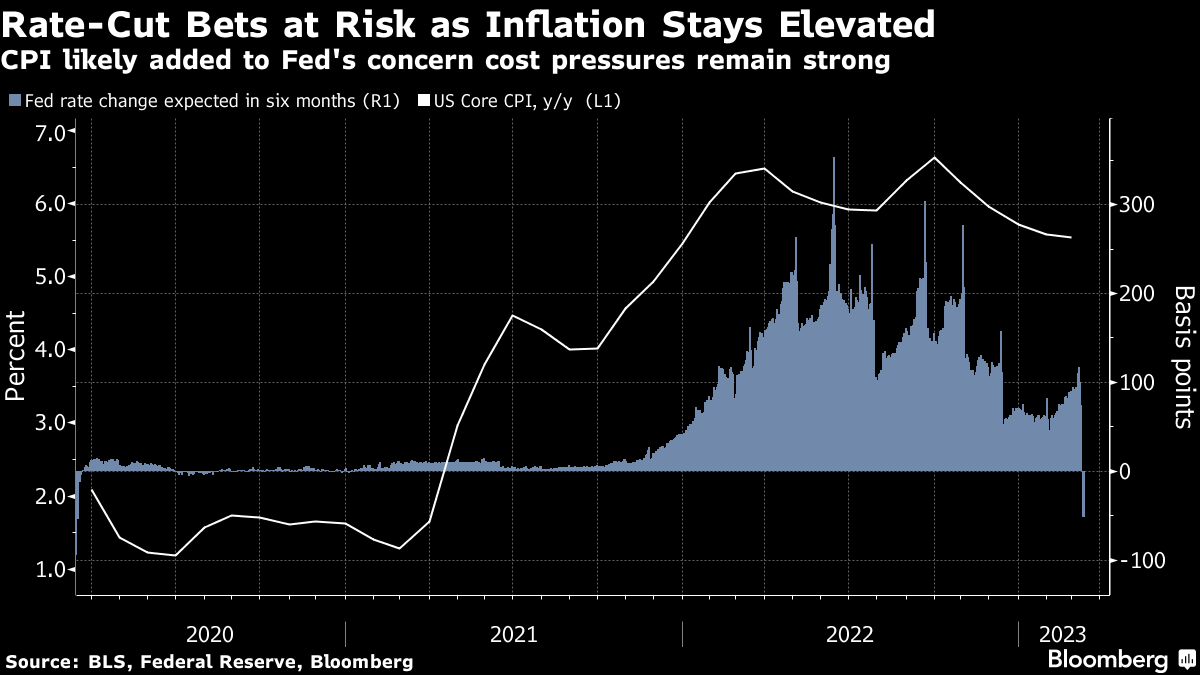

Finally, a couple for the visual learners out there like myself. BBG on rate CUT BETS

… US inflation data did the Federal Reserve, and rates markets, no favors. Monthly core inflation was stronger than expected in February while the annual pace on the same basis edged down to a still very elevated 5.5%. Given Fed Chair Jerome Powell’s comments just a week ago about the likely need for significantly higher rates to tame inflation, the latest economic data would indicate a chance for a half-point hike next week and further increases in the coming months.

Of course, the collapse of Silicon Valley Bank came after that data was gathered, but it remains to be seen whether the Fed regards the crisis as requiring the rapid shift in policy course now priced. Even after the CPI print led traders to push up the odds for a quarter-point increase, swaps markets continue to show expectations that there’s just one hike left in this cycle and it will still be more than reversed within six months. That means plenty of potential for more wild market moves during the lead-in to the Fed meeting and then after policymakers reveal what they think SVB means, if anything, for the tightening cycle.

And from the firm that is apparently the root of all (todays)evil,

… US 10yr Bond Yields fell sharply over the past week but are still for now holding their 200-day average, maintaining our expectation for further potentially lengthy ranging, before a deeper move lower towards our 3.00% objective in the 2nd half of the year…

…and we have a very similar outlook for the US 2yr Bond Yield, with a major potential top now threatening.