On December 2, 2001, the Enron Corporation files for Chapter 11 bankruptcy protection in a New York court, sparking one of the largest corporate scandals in U.S. history…

… AND away we go! This weeks closing price action likely to be more meaningful than anything I might conjure up here and now and so here’s a weekly look at 30s highlighting bullish momentum in some context:

Make as much or as LITTLE of this as you’d like and as you do (or don’t) … here is a snapshot OF USTs as of 658a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are weaker led by the belly after opening lower in Tokyo (10y JGB +3bps) and gradually cheapening into London hours. Bund’s remain a strong outperformer with semi-core widening notable (FR-GMY 10y +4bps), which sees some EURUSD weakness (-0.5%). UST desk flows have concerned selling from CBs in intermediates and slight steepening bias from fast$ in recent hours. Overall volumes are ~55% the 10d average, with crude oil +1.1%, DAX +0.8%, and S&P futures -8pts here at 6:45am…

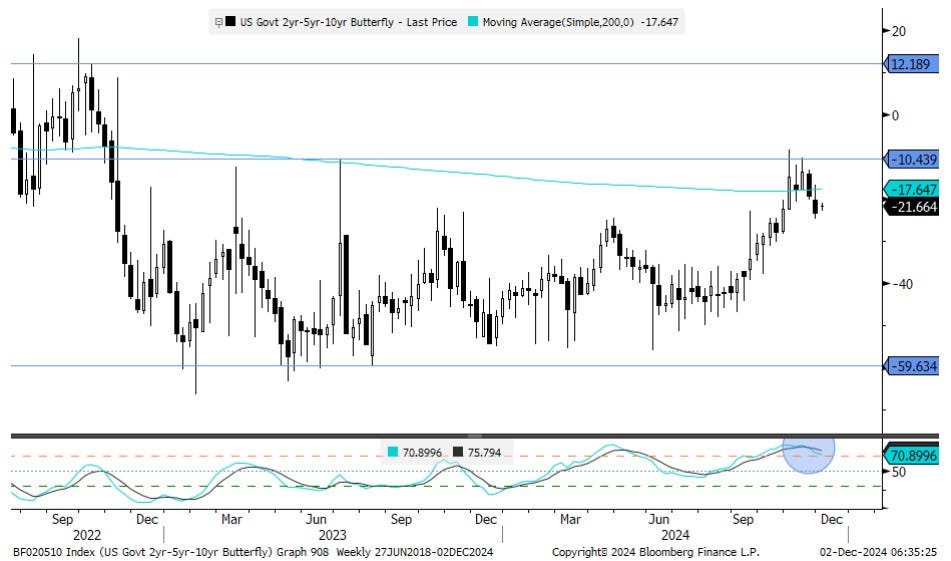

…Lastly, from a technical perspective after the November monthly closes, the clearest signs of durable outperformance remain in the belly-intermediate flys. The 2s510s fly is negotiating local resistance (-23.75bp area) in the near-term, but both daily and weekly momentum are now in unison in suggesting a potential breakthrough (towards further richening over the coming weeks). A similar dynamic is in play for the 2s10s30s fly as well, as our chart attachment illustrates, with weekly momentum rolling over in favor of intermediate-sector out-performance in the weeks ahead, with next resistance at -28.75bp (OCT ’23 highs) and then -39.25bp (April highs).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: USD bid amid further tariff threats ahead of ISM Manufacturing, OATs in focus as the French gov't awaits Le Pen's decision … OATs in focus as the French gov't awaits Le Pen's decision; USTs are slightly lower ahead of US ISM Manufacturing PMIs … Focus for USTs ahead, aside from France, is firmly on ISM Manufacturing PMI ahead of the services release later in the week and then most pertinently the NFP report. Currently trading at the lower end of a 110-31+ to 111-06+ band.

Opening Bell Daily: Traders see no risk … Investors are acting like there are no risks in the stock market … Traders are shrugging off macro and geopolitical concerns as bullish enthusiasm picks up.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up, a British operation on China developments over weekend …

BARCAP China: Better manufacturing, weaker construction

The NBS manufacturing PMI improved, with new orders expanding the first time since May. The services PMI expanded, while the construction PMI contracted. Overall, we see positive growth momentum lasting into Q4. We think Trump tariff threats could mark the start of a stream of new tariffs.

BARCAP China Stimulus: Tariff threats taking shape

Trump's threat to impose additional 10% tariffs is likely a negotiating tactic, but could mark the start of a stream of tariffs ahead. We expect China to respond with more fiscal support, though there could be a lag before the next policy announcements.

fresh from the French as they breakfast’d with all things macro …

Tariff threats triggered a stronger USD before a position squeeze weighed on the greenback last week. We remain fundamentally bullish USD and stay positioned short EURUSD but there is a chance the USD squeeze in FX could continue given upcoming risk events.

French budget risks will come to the fore at the start of this week, with the risk of a no-confidence vote on Wednesday. We think the government would survive this, which could lead to OAT-Bund spread compression and support the EUR on the crosses.

We expect a gain of 225k in Friday’s US employment report, a level which is likely to keep a December 25bp FOMC rate cut on the table. Considering both ECB and FOMC expectations, the risk of rate spreads narrowing presents a risk to our EURUSD short.

Markets saw a decent overall performance in November, with US equities bouncing back from their October losses as the S&P 500 hit another all-time high. Moreover, European sovereign bonds advanced as investors priced in faster rate cuts from the ECB. But there were a few weaker spots, with French assets underperforming given the country’s budget situation, whilst the Euro itself posted its biggest decline against the US Dollar in 18 months as investors contemplated the prospect of further tariffs. And given the dollar’s strength in November, it meant many of the returns were even worse in USD terms…

…Which assets saw the biggest gains in November? US equities: After losing ground in October, the S&P 500 (+5.9%) posted its strongest monthly performance so far this year. That was supported by a strong performance for the Magnificent 7 (+9.4%), and the small-cap Russell 2000 (+11.0%) also posted a strong gain.

Sovereign bonds: November was a strong month for sovereign bonds, particularly in Europe. For instance, Euro sovereigns were up +2.3% as investors priced in faster ECB rate cuts. But French OATs (+1.8%) were a relative underperformer given the budget issues there…

… and from month passed TO the year ahead, same firm …

DB: Mapping Markets: Why the bar is high for an outperformance in 2025

Both 2023 and 2024 surpassed expectations from a macro point of view. After all, a hard economic landing never materialised. Both the US and the Euro Area saw growth beat consensus expectations at the start of each year. And markets performed very strongly as a result, with equities up, credit spreads tightening, and broader volatility subdued.

But an important consequence is it’s raised the bar for another outperformance in 2025. After all, fears of a hard landing have now receded, and consensus growth expectations for the US and the Euro Area are stronger than they were at this point before 2023 or 2024. In addition, markets are already pricing some pretty benign outcomes, including further rate cuts from the Fed and the ECB, alongside subdued inflation. So that’s already priced in, making the bar for a 2025 outperformance much harder on paper than it was going into the last two years.

…Let’s look at the factors that are making another outperformance more difficult:

1. Growth expectations for 2025 are stronger than they were going into 2023 and 2024…

2. More rate cuts from the Fed and ECB are already priced in, and we’re now getting closer to neutral policy anyway…

3. Long-term inflation expectations (including market-based measures) are already well anchored around target…

4. The relentless rally of the last two years means valuations are much more stretched now…

… finally an economic week ahead which includes a look at economic surprises on top of 2yy …

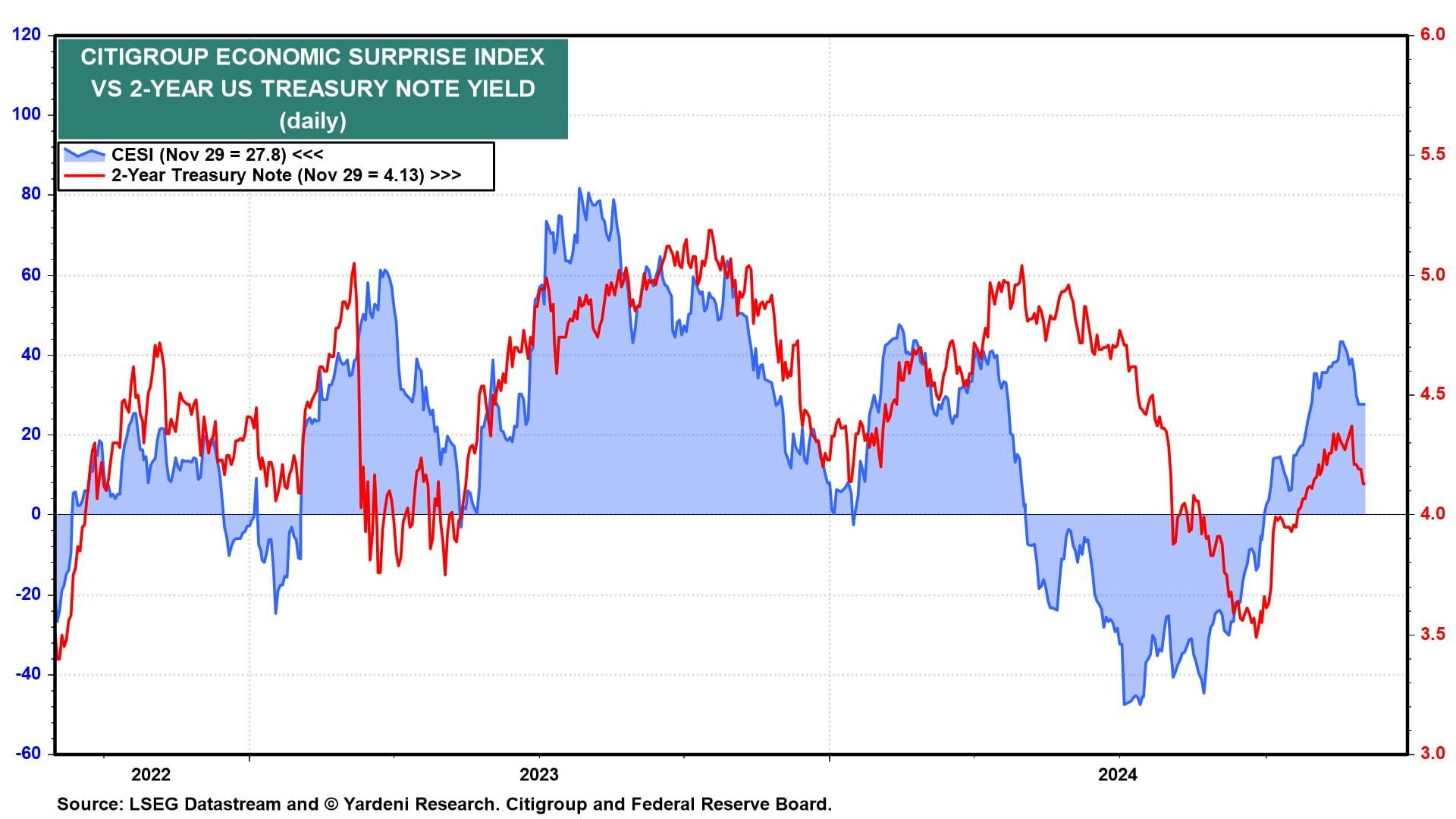

We expect to see more animal spirits during the economic week ahead. It is chock-full of updates of labor market indicators, as well as soft data (i.e., surveys) on business in the manufacturing and services sectors. The grand finale will be November's employment report on Friday. We are expecting this week's indicators to beat expectations, boosting the Citigroup Economic Surprise Index and sending yields a bit higher (chart). While hurricanes and union strikes depressed October's readings, we believe analysts are underestimating the economy's positive reaction to Trump 2.0 and easier Fed policy.

Here's what we're watching:

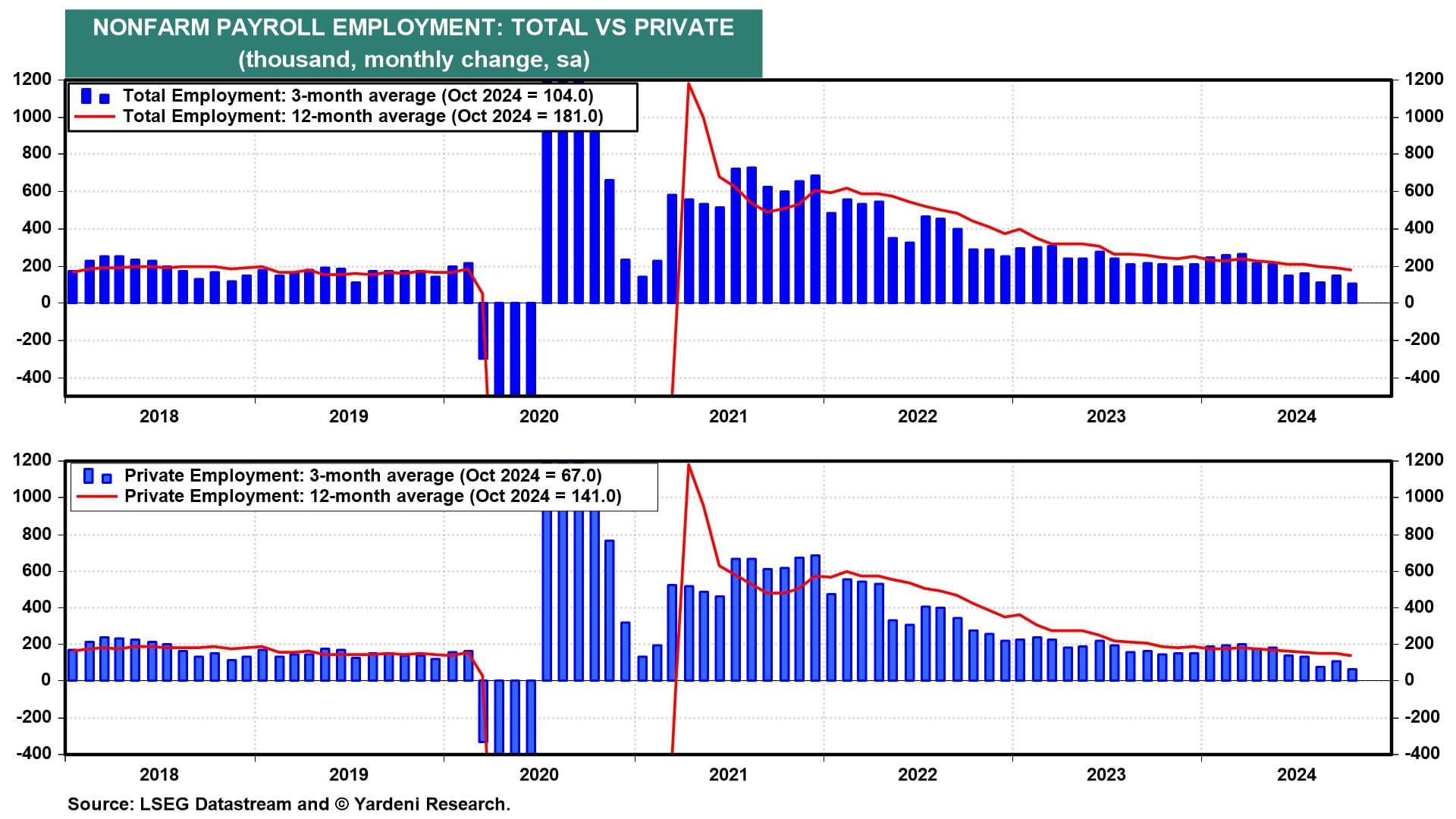

(1) Employment. We expect November's employment report (Fri) will show payrolls rose by more than 250,000. There were 33,000 Boeing workers returning from strikes, and coming back to work at Boeing's suppliers and after Hurricane Milton. We are expecting additional hiring attributable to the revival of animal spirits following Trump's big win and his promises to cut the corporate tax rate and implement deregulation. This should lead to better payroll gains into year-end. In fact, we think the 3-month gain in payroll employment could increase from 104,000 through October to 200,000 by January's employment report (chart).

… And from Global Wall Street inbox TO the WWW … first up a sanguine view …

Sometimes, FOMC members think the risk to their inflation forecast is to the upside, and sometimes, they think the risk to their inflation forecast is to the downside, see the first chart below.

This is in sharp contrast to their views on the risks to the unemployment rate.

The number of FOMC members who think the risk to their forecast for the unemployment rate is weighted to the upside is always much higher than the number of FOMC members who think the risk to their unemployment rate forecast is to the downside, see the second chart.

In other words, the Fed has a very asymmetric view on its dual mandate, putting much more weight on low unemployment than on getting inflation to stay at 2%.

… next is an OpED with a few words / visuals on vigilantes (who are not yet making presence felt) …

Bloomberg: Is Le Pen for turning? France can't bank on it

…No Sign of Bond Vigilantes

Abead of the election, the overwhelming consensus was that Trump 2.0 would be stocks-positive and bonds-negative, as logical effects of a policy of aggressively pursuing growth.But the bond part hasn’t come true. Instead, yields are lower than on Election Day (following a menacing buildup). The long search for a Treasury secretary assuaged the vigilantes in two ways. First, it showed that the Trump team understood that this was a crucial pick. Second, the vigilantes believe that appointing a macro hedge fund manager who learned his trade attacking currencies for George Soros shows that Trump 2.0 won’t do anything too stupid. Much weight is now on Bessent’s shoulders:

Inflation

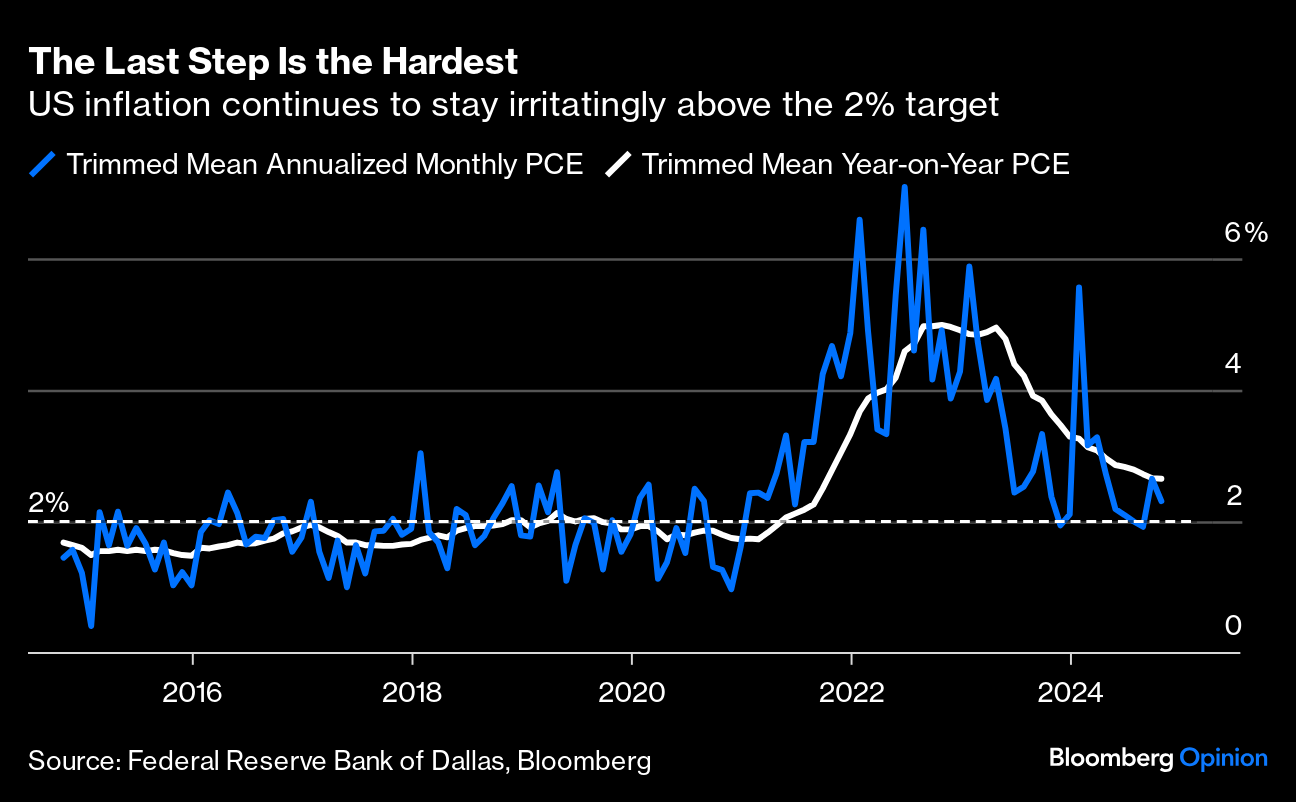

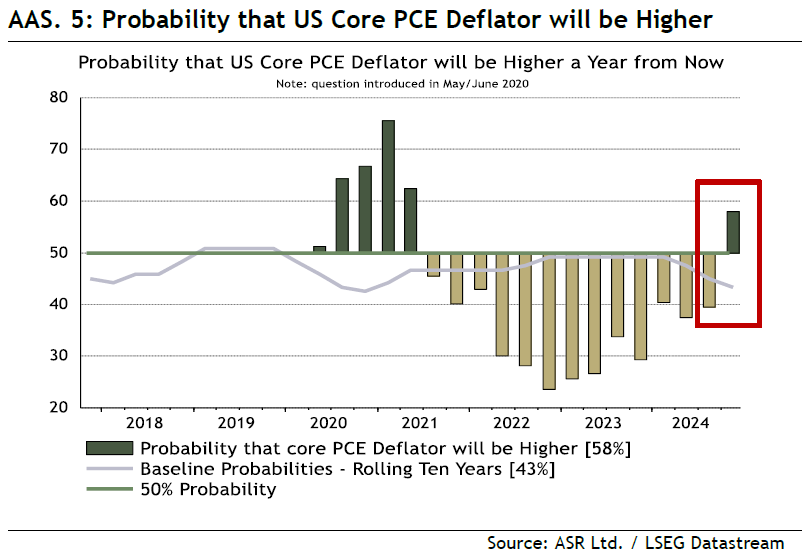

There are plenty of risks, of course. The biggest remains inflation. The latest edition of the Personal Consumption Expenditure (PCE) deflator, the Fed’s official target, gives further evidence that inflation is down but not out. Using the statistical purists’ favored trimmed mean version, produced by the Dallas Fed, in which outliers are excluded, the pattern is of disinflation tailing off stubbornly above the 2% target:

This doesn’t oblige the Fed to start hiking, although the expectation is now for a maximum of one more cut to the fed funds rate in the next two Federal Open Market Committee meetings. Investors are now very much alive to the disquieting risk that inflation still hasn’t been beaten, just as a new government prepares a barrage of policies that should at the margin be inflationary. Absolute Strategy Research’s latest quarterly survey of asset allocators shows that a majority of global money managers now expect US inflation to rise over the next 12 months, not fall:

Trump has a mandate for tariffs, corporate tax cuts, and an immigration crackdown; but everyone knows that the electorate will not tolerate a fresh wave of inflation. It’s not yet clear how severe the trade-off between policy aims and inflation will be, nor how the administration will deal with it, but it’s by far the greatest “known unknown” risk. Until it arrives, the trade is to keep buying American assets. That’s certainly what the money managers interviewed by Absolute Strategy seem intent on doing:

…Rates Positioning has been and will continue to be a factor. I’ve been pointed to the “Commitment of Traders” report: there is a lot of short interest by speculators, especially in the 10-year part of the curve. It apparently has been coming down, but if traders remain short, it will continue to help support bond prices. TLT, a 20+ year ETF, has been seeing outflows even as yields went higher – another potential indicator that positioning remains “underweight” bonds.

The negative buzz around the deficit and bond yields seems to have dissipated. In a quick note on Friday to our capital markets team and via Bloomberg to the clients I’m in IB chats with, we reduced our bullish outlook on bonds at 4.19% on 10s. We actually saw buying right up to the last minute on Friday’s trading, but I think with the “index extension” trade over and back to full days to trade bonds, it will be difficult for the rally to continue Our target was 4.1% to 4.2%, and while we are at the high end of our range, the rally has been almost too ferocious of late to be truly believable. The fears around tariffs, immigration, and the deficit (which were overdone), have now been replaced with a degree of complacency that doesn’t seem deserved.

China TIC data showed China holding $772 billion of Treasuries at the end of September. That number has been between $780 billion and $767 billion (a very narrow range) since February. There is no obvious reason for China to grow their holdings, and if anything, as they continue their efforts to stimulate their economy and gird for potential tough negotiations with Trump, we could see them lowering the amount held in the coming months. Not a big problem for markets, but not helpful as we have a lot of bonds to auction in the coming months…

…Bond Yields:

Expect the 10-year to inch a touch higher, pushing back towards 4.3%, with a lot of difficulty getting back to 4%.

Should be a good “range trading” environment, with a much greater risk of 50 bps higher than 50 bps lower from here, for the long end…

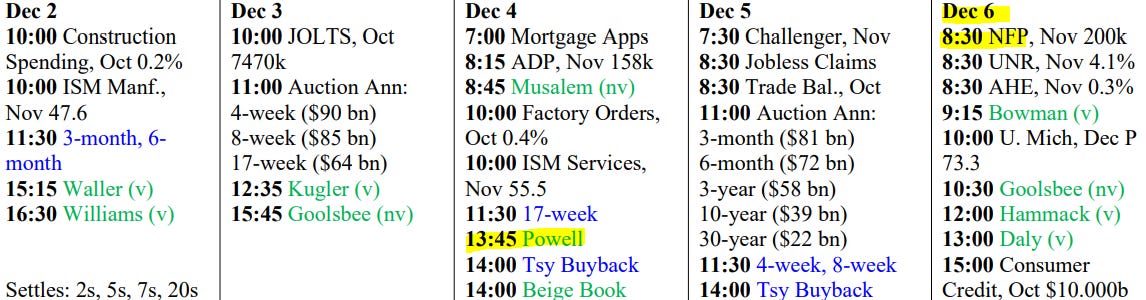

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here is an economic calendar I used when I was closer to and still IN ‘the game’ … from the best in the strategy biz is a LINKthru TO this calendar …

Really sad to learn Art Cashin has passed, a true legend and statesman. Was it he who said the problem w/betting on the END is you're only right once? Was about 30 yrs ago when I was 1st learning about investing watching CNBC before it became BubbleVision I noted when he said "where do I park my money during recessions? T-Bills!"

Really sad to learn Art Cashin has passed, a true legend and statesman. Was it he who said the problem w/betting on the END is you're only right once? Was about 30 yrs ago when I was 1st learning about investing watching CNBC before it became BubbleVision I noted when he said "where do I park my money during recessions? T-Bills!"