while WE slept: USTs watching equities, 'Earl; 'The Art of Warsh' (and more...); BLK, Beachboys see 'flation RISKS;

Feb 02, 2026

Good morning …

Equity futures fall (silver, BITC, AI questions, CSCO) and bonds are BID …

… and a few thoughts …

GOOD NEWS (kinda sorta) …

Bloomberg: Oil Plunges as Iran Risks Ease and Commodities Selloff Deepens

(Bloomberg) — Oil plunged as geopolitical risk premiums faded after US President Donald Trump said Washington is talking with Iran, while a broader commodities selloff exacerbated the slide…

… and this is helping bolster bond prices and keeping them MIDDLE RANGE BOUND …

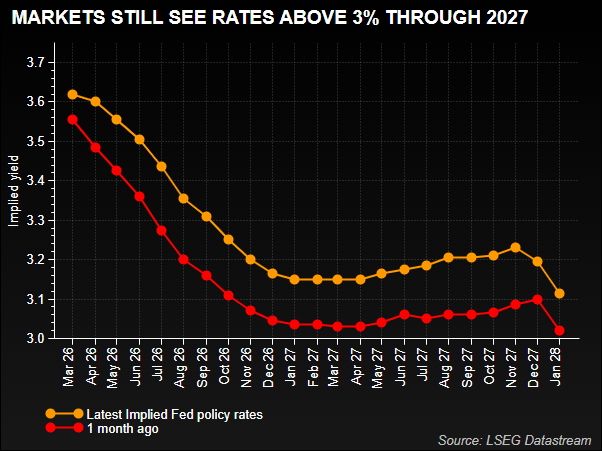

10yy DAILY bars: watching 200dsMA (4.233%) … within 4.58 / 3.98 RANGE (so 4.28 would be the middle)

… as IT remains FLAT and momentum (stochastics) offering little to NO signal

… make of that what ever you can — much ado about nuthin’, still, though … a calm before the storm?

AND … on storms, I’m NOT a BITC fanboy, much to my own demise … still, the move over the weekend does make one pause …

February 1, 2026 Bloomberg: Bitcoin’s break below $80,000 signals new crisis of confidence

… something more along the lines of the old-school assets which are leaned on as confidence in CBs fade …

February 1, 2026 Bloomberg: Chinese Speculators Set the Stage for Gold and Silver Crash

… and so here we are. Silver, gold and the bitcoin’s world and USTs just livin’ in it. I hope y’all had a nice weekend and hoping for a bit of a warm up here as this cold certainly gettin’ me down. That’s all for now …

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 650a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US stocks lower, NQ underperforming due to NVIDIA and Oracle updates; Metals continues Friday’s slump … Fixed initially bid given the risk tone, but pulling back as sentiment turns mixed in Europe … USTs are being dictated by the risk tone. Just off a 112-02 peak, firmer by c. five ticks as things stand. The tone is driven by the continued pullback in metals, weak Chinese PMIs, NVIDIA reporting, the likely temporary US government shutdown and as we await the first remarks from Trump’s Fed Chair pick and any potential SCOTUS update re. tariffs. While there is no schedule for the latter two points, today’s docket does have the S&P Final Manufacturing PMI and then the ISM figure …

…How soon before Trump dubs Kevin Warsh ‘clueless’?: Mike Dolan … But the initial market reaction to the decision, which still needs congressional confirmation, was modest. With a blizzard of other domestic and global influences swirling, it was hard to detect any sudden or pointed shift in the dollar, Treasury bonds or stocks that indicated fresh anxiety.

A basic test of that was that futures still pointed to roughly two Fed rate cuts in 2026 — about where they’ve been since last year. The shaky dollar firmed a bit on the news, and the Treasury yield curve steepened slightly.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS of Global Wall you might be able to use …

It would appear a memo circulated to see who on Global Wall could come up with the catchiest WARSH related research note … at end of the day, still thinkin NO rate cuts this year…

We see the Fed on hold for all of 2026, even if Kevin Warsh is confirmed as Chair Powell’s successor.

There is risk that the Treasury hints at coupon cuts this week. We are long 30y spreads into the refunding announcement.

We expect a hold with dovish risks from the BoE and therefore go into the event received March MPC and long EURGBP.

We revised our Fed outlook last week and no longer expect any rate cuts this year. This is for four reasons: 1) we expect the data to bear out Chair Powell’s optimism on growth and employment over the year; 2) we see inflation proving stickier than the FOMC now expects; 3) we believe the FOMC will increasingly assess its policy stance as non-restrictive or stimulative; and 4) regardless of who succeeds Powell, policy will probably follow a traditional reaction function…

…That said, the probability that the data is released on schedule has diminished, given that the federal government is partially shut down over disagreement on funding for the Department of Homeland Security. This episode is expected to be much shorter than the shutdown late last year. And data collection for the January jobs report is complete. But if the reopening does not occur early this week, we doubt that enough time will remain to put the final touches on the report for on-time delivery…

A large German bank remains BEARISH duration (and yes, short 10s vs 4.11 lookin for 4.45%) … and also some metals context as well as monthly asset performance review …

The first FOMC meeting of the year played out broadly in-line with expectations. The nomination on Friday of Kevin Warsh to be the next Fed chair led to modestly steeper curves, higher term premia, and narrower swaps spreads, which we view as warranted given his opposition to active use of the Fed’s balance sheet and the implications for the mix of policy tools going forward. Although it seems unlikely Warsh will have an immediate impact on balance sheet policy, his views present risks to the market’s long-held expectation that the Fed will readily act as a backstop in times of market dysfunction. One channel to a smaller Fed balance sheet over time would be regulatory changes that reduce bank demand for reserves, in-line with comments over recent months from Governors Bowman and Miran that the balance sheet is “downstream of regulations.”

The only change to the views and trades below is that we decided to take profits on our 30y SOFR swap spread long and turn neutral on spreads more generally given stretched positioning in recent weeks and Warsh’s nomination…

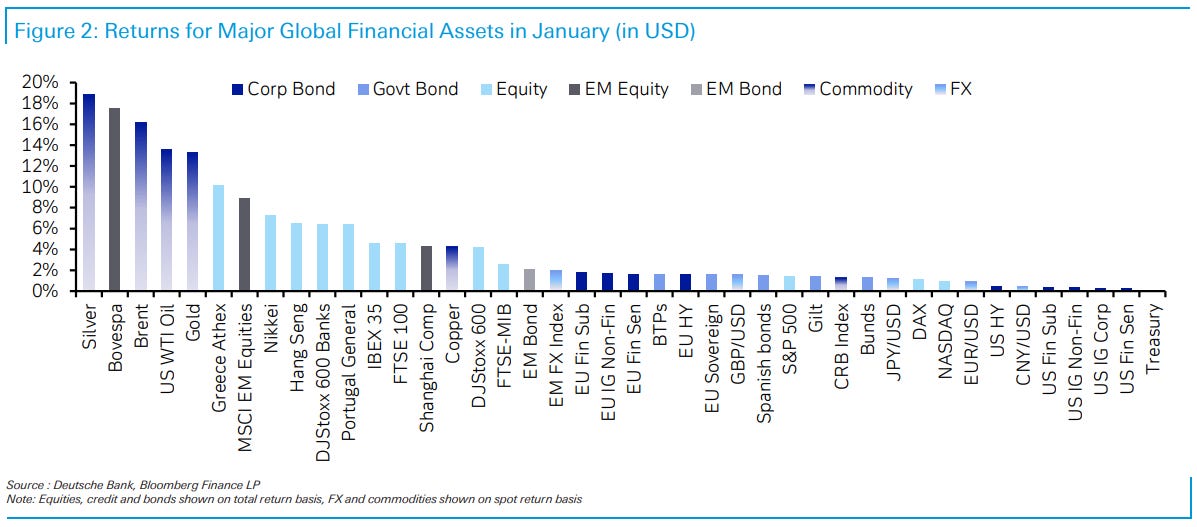

…Welcome to February with another big sell-off in Gold (-5%) and Silver (-10%) overnight, and a partial US government shutdown that isn’t as severe as the record one before Xmas, and is expected to get resolved soon. Nevertheless it’s typical of the 2026 constant stream of complicated news flow. This follows a January that managed to both shock and awe in various ways, yet still delivered broad based gains across all global assets in our monthly performance review when measured in USD terms—a genuinely rare occurrence. It was perhaps fitting then, that the month ended with extraordinary volatility: Silver saw its largest daily fall since 1980 (36% at the intraday lows, 26.3% at the close), while Gold recorded its biggest one day decline since 2013 ( 8.95%). With the overnight moves, Silver is now around $5 below its real adjusted level from 1790—something we explored in last Monday’s CoTDhere. As we noted, even incorporating the dramatic 1980 boom and bust and the recent surge, Silver has failed to outperform inflation over more than 230 years of data. So while I’ve long been a bit of a gold bug given my strong views on the inflationary consequences of fiat money, the recent run up in precious metals feels to have an enormous speculative element. Friday’s moves, almost certainly driven by positioning and margin dynamics, only reinforced that impression…

… just published his usual performance review here, and despite the late month turbulence it was still a very strong January for global assets. Silver (+18.9%) and Gold (+13%) topped the performance tables, joined by oil (+16.2%), which posted its biggest monthly gain in four years. Outside our formal performance review, it’s also worth noting that Bitcoin is currently down about -14% year to date after a difficult few days. It now sits around -40% below its October 2025 peak and back at levels first breached in November 2024. Over that same period, Gold has doubled…

02 February 2026 DB January 2026 Performance Review

Markets put in a strong performance in January, as positive data surprises continued to power risk assets, with the S&P 500 briefly poking above 7,000 for the first time. But just as we saw in 2025, those headline gains masked significant volatility under the surface, as geopolitical risk rose significantly, including over Venezuela, Iran and Greenland. So that meant Brent crude oil (+16.2%) saw its biggest monthly jump in 4 years, particularly after Trump warned that a “massive Armada” was heading to Iran, which raised speculation about a US strike. Moreover, precious metals had their biggest surge in decades, with gold prices (+13.3%) seeing their biggest monthly jump since September 1999, despite the sharp pullback at the end of the month. All that came amidst growing pressure on the US Dollar, which saw its biggest 4-day decline since the Liberation Day turmoil last year, weakening against every other G10 currency in January…

…the Federal Reserve were in the spotlight in January, particularly after the Department of Justice began a criminal investigation that revived questions around central bank independence. That also added to the upward pressure on precious metals, with gold prices moving higher throughout the month, ultimately closing up +13.3% in its best monthly performance since September 1999. If anything, that underplays the volatility, as gold prices hit an all-time intraday record of $5,595/oz on Jan 29, before pulling back sharply to close the month at $4,894/oz, including its biggest daily decline on Jan 30 (-8.95%) since April 2013. That surge in gold prices also occurred alongside a fresh move lower for the US Dollar, with the dollar index down -1.4% in January, which included the biggest 4-day slide since the Liberation Day turmoil last April. That accelerated after Trump himself was asked about the decline, and he said “No, I think it’s great”. However, the moves stabilised after Treasury Secretary Bessent reiterated the “strong dollar policy” the next day in a CNBC appearance. Finally on Jan 30, it was also announced that Kevin Warsh had been nominated by Trump to become the next Chair of the Federal Reserve…

Here’s an excellent EQUITY primer for the week ahead …

The Warsh nomination should be viewed as a market stabilizing event with the recent parabolic rise in precious metals raising questions about the "run it hot" strategy. Friday’s price action signals it was the right move as the S&P 500/Gold ratio had one of its best days in history.

The Warsh Nomination...In our view, President Trump’s nomination of Kevin Warsh as Fed Chair is aimed at restoring market confidence following a parabolic rise in precious metals and a rapid weakening in the US dollar. While the administration favors a weaker dollar to support competitiveness and reduce trade imbalances, the pace of the recent move was likely undesirable. Warsh’s reputation as a balance sheet hawk is seen as a credibility anchor, helping to cool gold prices and modestly support the dollar—buying time for broader policy objectives to play out as designed. From our perspective, the administration’s policy mix is aimed at driving a more sustained balance of real growth (through productivity) and inflation.

Remember, “Run It Hot” Is a Debt-Management Strategy...With debt-to-GDP levels resembling the post-WWII era, the administration is pursuing higher nominal and real GDP growth as the only viable path to managing the debt and deficits. Unlike prior approaches centered on government spending, population growth, and subsidies, the current strategy emphasizes private-sector capital allocation, productivity gains, and wage growth, particularly for lower and middle income Americans. This reflects a continuation of fiscal dominance, where the Fed tolerates above-target inflation in favor of growth and financial stability, though the focus of policy is directed more at main street…

…It appears that the current administration is focused on driving a more sustained mix of real growth and inflation by rebalancing the economy on three different planes, simultaneously:

Current/trade accounts: the “international” imbalance

Policy: tariffs/weaker USD

Over-consumption vs. under-investment: the “domestic” imbalance

Policy: tariffs/weaker USD and OBBBA tax incentives for capex

The k-economy: the “inequality” imbalance for corporates and consumers

Policy: immigration enforcement and de-regulation

The end goal of these policies is the same—to grow out of the debt problem. However, the approach is focused on having companies, rather than government, make the capital allocation decisions, while increasing income through the wage channel rather than entitlements. The result should be higher nominal GDP growth with a greater emphasis on real growth via higher productivity and wages…

Read this and instantly thoughts turned TO … the video (after the note) …

February 1, 2026 MS Sunday Start | What’s Next in Global Macro: The Final Countdown

Jerome Powell’s term as Chair is drawing to a close. Last week’s FOMC meeting brought no change in policy, but the two dissents in favor of a cut demonstrate the division within the FOMC. Reports indicate that Kevin Warsh will be the nominee for the Chair to replace Powell. A natural question is what the Fed’s reaction function will be in the future…

…But inflation is still rising and the overall tone of last week’s Fed meeting conveyed a view that economic activity is solid. With inflation above target for the past five years and a labor market that could start to improve, our baseline call for additional cuts is not guaranteed. Current market pricing is consistent with our baseline, but investors should contemplate the path to no further rate cuts in this cycle. If the unemployment rate falls further, business and consumer spending remain as strong as they have been, and inflation fails to inflect lower beyond the current quarter, the Powell Fed would certainly question the merits of easier policy. That constellation of data would call into question the level of the neutral policy rate and whether we are not already there. Even with the turnover in leadership, strong spending with sustained inflation and low unemployment could stay the Committee’s hand for the rest of the year.

AND …

… Moving ON and back TO … tariffs as well as another couple NFP precaps …

Markets have largely looked past tariff announcements in 2026, but the narrative around supply chain and investment flows could evolve this year, while tariff risks linger…

…Markets have largely moved past the US headlines on tariffs, but we think the story will continue to evolve. Countries are becoming proactive in their trade policies, and a new multipolar order continues to take shape. The recent EU-India deal is one example, which is concluding now after nearly two decades of negotiation. India also recently signed a trade deal with the UAE, and the UAE signed a similar deal with Turkey. A new trade route has effectively been created. We expect more bilateral deals to be negotiated that create even more new trade routes. It is in the details of these negotiations that a new trade paradigm will start to be realized.

The labor market appears to have stabilized, and we forecast another solid month. Payrolls rise 55k. Private payrolls (+90k) are biased up temporarily, but federal resignations hold back gov't payrolls. The UE rate is unchanged (4.4%). AHE +0.3% (-0.2pp to 3.6%y/y) and the workweek is unchanged.

The net birth-death adjustment improves payrolls estimates through an analysis of the effects of business openings/closings in recent years. It's effective, lessening benchmark revisions. The Jan jobs report will alter the method and may amplify payroll swings but we do not expect large effects.

Key takeaways

The net birth-death adjustment estimates employment from business openings/closings in excess of what’s recognized within the processing of the payroll sample

We describe how the net birth-death estimate is created: through comparison of payroll sample data to the UI tax record data from the QCEW.

In the past, the net birth-death adjustment has lessened the size of benchmark revisions

BLS will now start incorporating some payroll-sample data into its current net birth-death estimates, as they did for a short time in late 2024.

The new method may amplify swings in payrolls, but effects look small relative to the overall benchmark revision.

The sharp decline in gold and silver prices has relatively little economic significance. While attempts will be made to spin this as a reaction to fundamental economics, it seems more likely that the “fear of missing out” trade became exhausted. The run-up in prices was over too short a period to have created major wealth effects, so correcting to a price more in line with economic fundamentals would be regarded as an economic positive (avoiding a misallocation of resources)…

…The quarterly US Treasury funding announcement is not a market moving event, but it is a reminder of the state of US fiscal finances. While avoidance, planning, and carve outs have reduced tariff revenue, money was still raised. If some tariffs are ruled illegal, that will damage the US fiscal position further…

The week ahead has an anything-goes energy as a variety of key data and earnings reports vie for attention amid peak geopolitical intrigue.

Last week left quite an impression on global markets. Trading in gold and silver went off the rails. “Dollar debasement” concerns competed with yen-intervention chatter. Donald Trump’s White House kept everyone on their toes, hinting at military action in Iran and threatening new tariffs. Yet President Trump clarified, too, naming Kevin Warsh as his choice for the next Fed chair. If confirmed by the Senate, he will start on May 15.

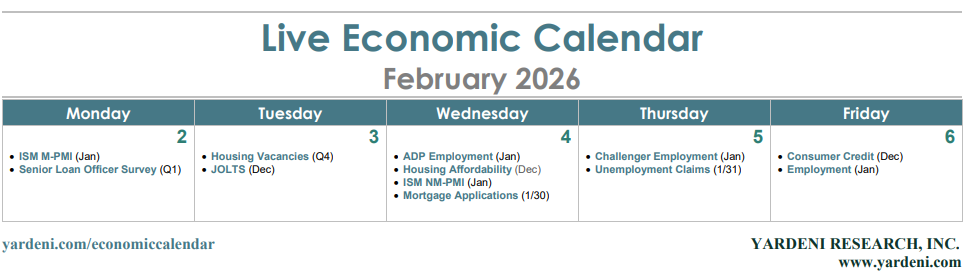

Investors will be assessing how this week’s bevvy of labor market indicators might affect the timing of any future Fed rate cuts. They include December’s JOLTS data (Tue), January’s ADP release (Wed), January’s Challenger layoffs survey (Thu), weekly unemployment insurance claims (Thu), and January’s employment report (Fri)…

…Here’s a look at the key data reports this week that might influence the timing of the next Fed rate move:

(1) Employment. We expect a slight improvement in the labor market in January, with payrolls rising by 60,000 following a 50,000 gain in December (chart). Any upside surprises could boost the dollar and buttress current Fed Chair Jerome Powell’s contention that the US doesn’t require fresh monetary stimulus.

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

Bloomberg on INFLATION (views of some of the biggest money managers on the planet — BLK and Beachboys) … Warsh and the balance sheet AND OpED’er in chief on WARSH …

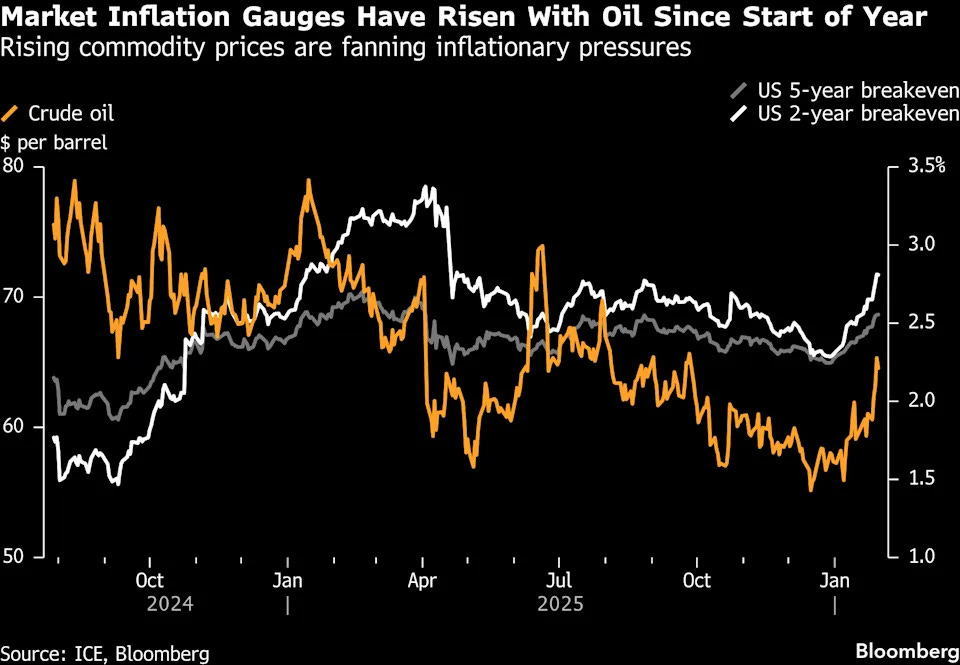

February 2, 2026 Bloomberg: BlackRock, Pimco See Inflation Risks the Wider Market Doubts

(Bloomberg) -- Money managers at BlackRock Inc., Bridgewater Associates and Pacific Investment Management Co. are shoring up their portfolios against a fresh bout of inflation.

A BlackRock fund is building short positions in US Treasuries and gilts in case lower interest rates fail to materialize. Bridgewater prefers stocks to bonds. Pimco likes the buffer afforded by Treasuries that have an inflation adjustment baked into their yield.

There are growing signs their concern is warranted: The difference between yields on ordinary Treasuries and inflation-protected notes has climbed sharply in January to the highest levels in months. Inflation swaps, another gauge of market expectations, have also risen.

It’s a view motivated by expectations a robust US economy will reignite price growth, particularly if Kevin Warsh — nominated by US President Donald Trump on Friday as the next Federal Reserve chair — steers policymakers toward quicker or deeper interest-rate cuts. More globally, higher commodity prices, heavy government borrowing and soaring artificial intelligence spending add to the pressure.

A US-led “inflationary boom” is the biggest risk underpriced by investors this year, according to Ben Pearson, a senior trader at UBS Group AG…

February 2, 2026 Bloomberg: Warsh’s Return Revives Tensions Over the Fed’s $6.6 Trillion QE Hangover

(Bloomberg) -- For much of the time that President Donald Trump was mulling his potential choice for the next chair of the Federal Reserve, the debate in markets swirled around whether his pick would lower interest rates as aggressively as he preferred…

…Shrinking the Fed’s footprint won’t be easy. Should he be confirmed, Warsh would face a balance sheet that’s orders of magnitude greater than when he was last at the central bank.

Money markets in particular have proved sensitive to even the slightest changes in the amount of liquidity in the system. A prime case was in 2019, when the Fed had to step in to ease funding strains that sent short-term lending rates skyrocketing.

More recently at the end of 2025, an increase in government borrowing, combined with the Fed’s ongoing unwind of some of its holdings — a process known as quantitative tightening — caused a smaller but still notable squeeze by siphoning cash out of money markets…

…For BMO Capital Markets’ Vail Hartman, the Fed’s adoption of the ample-reserves framework makes it difficult to imagine a near-time pivot, but the addition of another “balance-sheet hawk” on the FOMC should help keep a check on future asset purchases or reinvestment policies, he wrote on Friday. Beyond that, “a significantly smaller balance sheet would likely require a major shift in the Fed’s existing bank regulatory framework,” Hartman wrote…

February 2, 2026 at 5:00 AM UTC Bloomberg: A hawk or a dove? Understanding Kevin Warsh The appointment signals that the bare-knuckles legal fight to control the Fed is over…

…What was all the fuss about? The Warsh appointment matters above all as “an implicit acknowledgment that Trump cannot bend the Fed to his will,” as the macro strategist David Woo, who publishes the David Woo Unbound newsletter, puts it. The chairman is only one vote of 12, and the opportunity to impose a new slate of Fed regional presidents is gone, along with any effort to embed a pro-Trump majority. The Supreme Court might well rule out any future attempts to do this. Appointing Warsh signals that the bare-knuckles legal fight to control the Fed is over.

That is good news, but to make a final point, which isn’t quite “I told you so” (but does, I admit, come close). Way back in April, when the president had made his first online fulmination about firing Powell and withdrawn it within days, Points of Return was headlined “We Need to Talk About Kevin (and Jerome).” My argument then was that there was no need for a risky fight over Fed independence when Powell’s mandate was almost up and there was an obvious replacement — Kevin Warsh.

As a former Fed governor, with a record of cutting against orthodoxy, with Wall Street and Republican party cred (but without mentioning his looks), my argument at the time was that Warsh was just what Trump needed politically: a “rare combination of genuine change with the stability of continuity.”

With such an obvious candidate in the wings, I averred, it was “absurd for Trump to make such a fuss over the last few days,” and that if the administration really wanted to change the Fed it could “wait until next year with a new man” rather than provoking an unnecessary crisis. Nominating Warsh early could have hastened Powell’s lame duckdom.

Instead of that, the White House gave us nine more months of dangerous stupidity before accepting the option that had been glaringly obvious all along. There are times when Trump is “crazy like a fox” and gets leverage by starting out with a big demand. On this occasion, it’s hard to see that anything was gained by the prolonged maneuvers, beyond learning what most people knew all along…

Charts. I like ‘em. Here are (2 of)5 to watch as Warsh becomes more familiar to markets …

Feb 02, 2026 Shadow Price Macro: Five charts to track the Warsh sentiment shift Friday’s crash in gold and silver made many think Warsh is hawkish - he won’t be

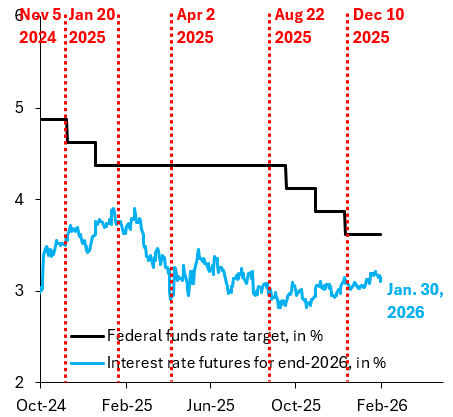

…Market pricing for Fed cuts: the obvious place to start is federal funds futures, which show what markets price for Fed cuts on different horizons. The black line in the chart below shows the midpoint of the Fed’s 25 basis point target range for the policy rate. The blue line shows what futures price for this rate by the end of this year. The latter fell on Friday - a sign US rates markets think Warsh will cut more and earlier - and should keep falling as we move forward.

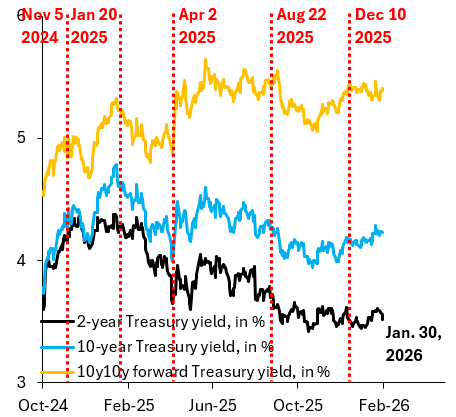

US yield curve steepening: as I noted above, the 2-year Treasury yield fell on Friday, consistent with interest futures pricing more and earlier cuts. If markets continue to move in this direction, it signals greater political dominance of the Fed, which should cause investors to demand higher risk premia at the long end of the yield curve. We should therefore see more steepening of the yield curve, which is something that already got going on Friday. The best way to see this isn’t the 10-year yield, which is the blue line in the chart below, but instead to focus on the 10y10y forward yield (orange line). That’s because the 10y10y forward yield cuts out what’s going on in the front end of the yield curve and is therefore a better measure of risk premia at the long end.

Bessent sold $766bb and curve (bear)steepened … as long as it steepens, most of Global Wall in the right trade and so …

Jan 31 2026 WolfST: US Government Sold $766 Billion of Treasuries this Week. Yield Curve Steepened as 30-Year Treasury Yield Rose to 4.87%

The spread between the 2-year and 10-year Treasury yields now the widest since January 2022…

…The spread between the 2-year yield and the 10-year yield widened to 74 basis points on Friday, the widest spread since January 2022, indicating to what extent the yield curve has steepened between the two.

Part of the reason why the spread has widened is because the 2-year yield is still so low, at 3.52%, and has barely ticked up since September 16. Investors in the 2-year yield are still counting on a rate cut or two later this year:

$766B in treasurys sold in a wk seems....insane! Remember the good ole' days when a $500B trade or budget defecit caused paniced headlines. For the nat debt to double from $19T in 2016 to $38T now seems insane too. I do believe math will win in the end....

$766B in treasurys sold in a wk seems....insane! Remember the good ole' days when a $500B trade or budget defecit caused paniced headlines. For the nat debt to double from $19T in 2016 to $38T now seems insane too. I do believe math will win in the end....

Strong ISM mfg, reported today.