Good morning … Equity futures are pointing down and EARL and bond yields are heading higher … seems to be carrying over from Friday and so, an update on EARL …

ZH: In Parting Gift To Trump, Biden Sends Oil Prices Soaring With Russian Sanctions Days Before Inauguration

… But now that Biden is out of the White House (having easily won the "worst US president" designation many times over), the Democrats are in disarray, and the world looking with some semblance of hope toward Trump's second term, Biden has decided that it is finally time to do the "right thing" and send oil prices surging by announcing the most sweeping and aggressive sanctions yet on Russia’s oil trade, making life for his successor hell as gas prices are about to soar following closely the spike in oil.

Indeed, it was last Friday, with less than 2 weeks to go until Biden is kicked to the curb, when we got the shocking news that the US Treasury would enforce sanctions against Russian oil giants, Surgutneftgas and Gazprom Neft, while also dramatically expanding a highly effective program of targeting individual oil tankers expanding the list to some 270 total tankers sanctioned for carrying Russian oil, listing traders organizing hundreds of illicit shipments, naming pivotal insurance companies, and telling two US oil service providers to exit …

… for somewhat more from Global WALL …

… Overnight in Asia, markets are catching down to Friday's falls despite stronger than expected Chinese exports data this morning (YoY growth of 10.7% vs 7.5% expected). The CSI 300 is down -0.52%, with the Hang Seng declining even more (-1.20%). Elsewhere in the region, the Kospi has dropped by -1.04% so far with Japanese markets closed for a holiday. Meanwhile, US equity futures show continued risk-off sentiment with the S&P 500 losing -0.44% and the Nasdaq 100 down by -0.60% as we go to print. As you'll see below a further spike in Oil isn't helping…

… Recapping last week now and the main story for markets was the relentless bond selloff, with long-end borrowing costs pushing higher across the world…

… All that reignited concerns that the Fed and other central banks would have to keep rates higher for longer. In fact by the weekend, markets were only pricing 29bps of cuts by the Fed’s December meeting, down from 39bps at the start of the week. And in turn, that pushed the 10yr Treasury yield up +16.1bps (+7.0bps Friday) to 4.76%, which is its highest closing level since October 2023. That momentum was clear in Europe too, where yields on 10yr bunds moved up +17.0bps (+2.8bps Friday) to 2.59%, their highest since July. It also marked a 6th consecutive weekly increase for the 10yr bund, which is the first time that’s happened since 2022, back when the ECB were hiking by 75bps per meeting.

…Those bond moves weren’t helped by fresh rises in commodity prices, which added to fears about inflationary pressures. Brent crude oil saw its highest weekly close since July at $79.76/bbl, with a +3.69% jump on Friday after the outgoing Biden administration announced a new broad set of sanctions against the Russian oil industry. Brent crude futures are up another +1.88% this morning. In addition, copper posted its biggest weekly gain since September, with a +5.66% rise (-0.13% Friday), whilst gold was up +1.88% (-0.89% Friday). -DB EMR, 13 January 2025

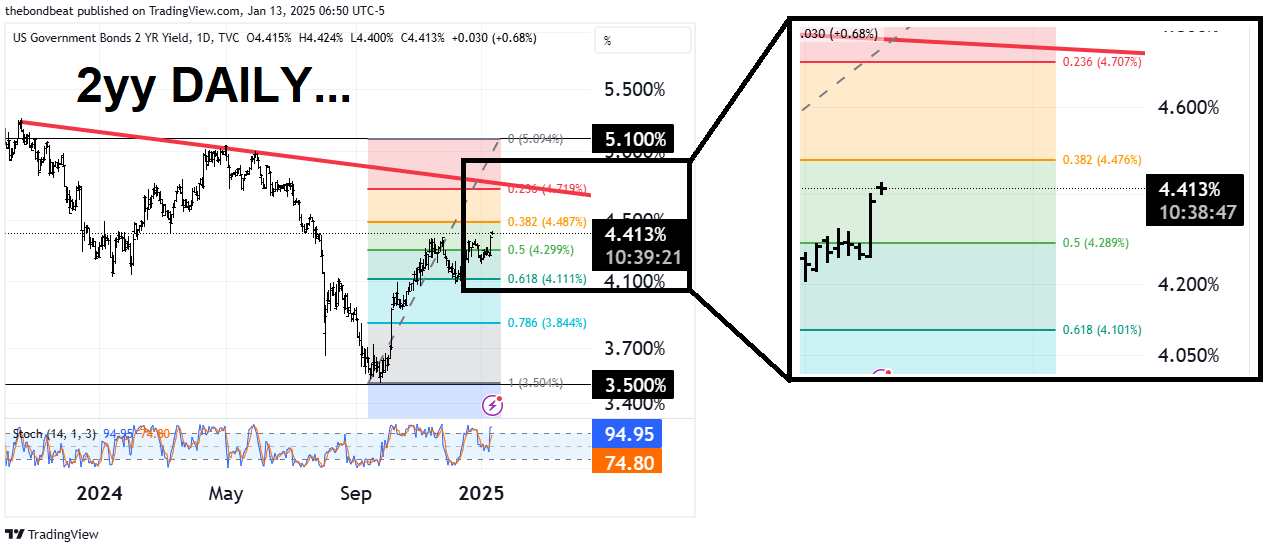

… NOTED and jumping right to an updated visual of the front end, carrying along with this past weekends note / picture where this morning I’ve attempted to add some fibo retracements highlighting why 4.50% ‘ish might be next level to watch …

2yy DAILY

… above here and we’re looking towards TLINE / fibo retrace up nearer 4.75% and I’d be guessing something happens before then to suggest front end a buy (or a short-term rent) … Unless, of course, you believe in your heart of hearts the Feds next move is to HIKE rates … I’ve not jumped to that conclusion and with situation in CA (5th largest econ in the world) would seem that leap of faith getting incrementally harder to make …

… here is a snapshot OF USTs as of 655a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: DXY tops 110, Gilts hit another contract low & crude in focus amid Gaza ceasefire reports … Fixed benchmarks weighed on in a continuation of the post-NFP trade, Gilts hit another incremental contract low … USTs start the week under pressure, continuing the hawkish impulse from NFP on Friday with strong Chinese export data not helping; on this, we wait to see if President-elect Trump comments on the data with reference to his touted tariffs. As it stands, USTs are at the low-end of a 107-06+ to 107-15 band, which marks another contact trough. Amidst this, yields are firmer across the curve with the short-end leading and reflecting the trimming of Fed easing expectations.

Opening Bell Daily: TOO many jobs? The US economy is too strong for investors' liking … Stocks turned red and Fed rate cuts came under question after the December jobs report.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

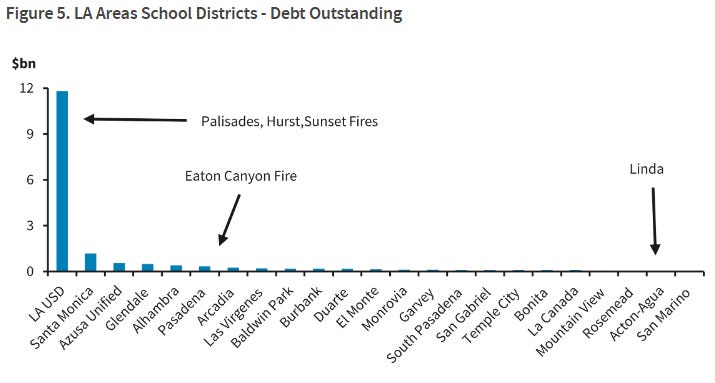

First up, some have asked for a view relating to the fires given CA is largest state in the union and in a GLOBAL context, well, clearly as the WORLDS 5th largest economy, the fires matter. Impacts are to be felt for quite awhile and then there will be some who say the ‘rebuild’ will be a boon to growth — it is THOSE folks we should not may much heed too as there’s nothing … NOTHING … good ‘bout death and destruction. Whether or not a recession has now been all but assured is to be determined … a couple MUNI NOTES on the topic …

Munis enjoyed a relatively quiet post-holiday week. Looking ahead, a lot will depend on the strength of the US economy and inflation - if rates continue selling off, munis will undoubtedly be negatively affected. However, the higher muni yields go, the more investors they will likely attract.

… Fires in Los Angeles and Muni Aftermath This week's fires in Los Angeles attracted a lot of focus from investors. There are five active fires in the Los Angeles region at the moment, with the two largest in the Pacific Palisades and near Pasadena. The fires, driven by hurricane-strength wind gusts, have killed at least ten people and and forced more than 180,000 residents to flee. Altogether, it is likely to be one of the costliest wildfires and natural disasters in US history. An initial estimate from AccuWeather Inc. put the total cost as $52-$57bn, but most likely the damage is overstated to a degree, in our view.1

At this point, there are no indications on what caused the fires, but LADWP's spreads have been moving wider, as some investors got concerned that the fires might have been caused by LADWP Power System's (AA-/Aa2/AA-) equipment; they are more concerned than they would normally be, as it operates in the area and because utilities have been found liable for causing fires in California, Hawaii and Washington in the past several years.

LADWP one of the largest municipal utilities in the nation, serving approximately 1.6mn customers, providing a large and diverse revenue base for the self-regulated monopolistic utility. The Board increased the Base Rate revenue target for FY 2024 by 5.6%, following a 2.035% increase in FY 2023; the next rates schedule begins on July 1, 2025, according to Moody's. The company's total available liquidity was $2.2bn in FY23, and LADWP has consistently demonstrated its willingness and ability to adequately adjust its rates to maintain a sound financial metric profile with strong liquidity, sound coverage ratios, and steady total leverage, according to the rating agency…

…LA USD is the largest credit, and it is the most exposed to loss or property damage, and would likely rely on help from the City and the State, but we would not be surprised to see some credit widening, especially for some of the smaller and lower-rated names.

Early on, the muni market was slow to react as usual, and there has been very little trading on the back of this disaster, but we expect more clarity and a more pronounced market reaction in the near term, when the extent of damages and the cause of the fires becomes clearer.

As best we can tell, CAL Fire's listed coordinates of active wildfires are not directly located on mapped transmission lines owned by LA DWAP Power System.

LA DWAP does not serve Pasadena and Altadena.

For the Hurst fire, the number of impacted structures is likely lower than the others.

LA DWAP, per S&P, maintains nearly $200 million of wildfire coverage and over $2 billion in liquidity.

MS: Insurance - Property & Casualty, Municipal Strategy: How the California Wildfires Change Our Investment Thesis

Given the LA County wildfire insured loss estimates continue to rise, we believe the P&C investment thesis could shift due to this event. Personal lines could see more impact given the fundamentals are shifting after a profitable 2024, while the impact to reinsurers will be limited.

Moving on and offering a couple notes on China …

BARCAP: China: Exports surge as front-loading continues

We think the double-digit export growth (led by the US and Asean), along with the increase in the PMI new export orders, suggests continued front-loading. Our channel checks with manufacturers confirmed export front-loading was seen in various sectors, including electronics and textiles.

Geopolitics and tariff threats dominate investor concerns, while tumbling equity, currency, and bond yields add to the PBoC's challenges as it balances multiple objectives. As deflationary forces persist and fiscal underdelivers, we expect CPI to stay low for longer, and PPI to remain negative.

Here’s a note on OIL and one from same shop dropped early Sunday morning …

BNP: US sanctions on Russian energy likely to boost near term strength

The new US sanctions on Russian energy were deeper and broader than the market anticipated, and we expect disruptions to amplify current market strength.

The volumes of crude, diesel, fuel oil and LNG at risk are significant and may tighten markets initially as mainly China and India will need to source alternative barrels and cargoes.

A significant number of new sanctioned vessels adds upside to freight rates.

We think the impact will eventually be more limited given domestic alternatives and potential evasion, but that will take some time.

With US and EU refinery maintenance commencing soon, this might cap the downside to crude and amplify the upside to diesel and fuel oil cracks.

EU gas may see further spot and summer price upside from tighter LNG.

Stronger-than-expected US economic data continues to support our out-of-consensus call for no Fed rate cuts this year and brings into question whether a hike might be on the table.

The combination of long US breakevens and long USD remains our preferred macro expression of the “Trump trade”.

Our preferred FX shorts are in CAD and GDP as the former faces immediate tariff risks and the latter grapples with worrying fiscal dynamics.

Next up an important narrative UPDATE from Germany …

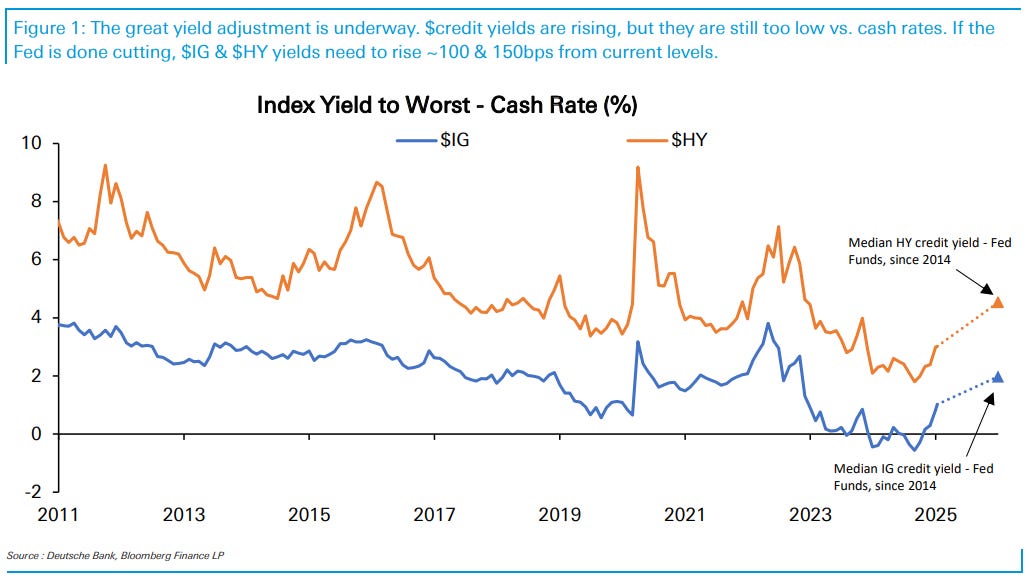

DB: Higher, Steeper, Wider? US credit yields to keep climbing

The thesis of our 2025 Outlook is materializing: Fed policy, in aggregate, is too loose for a Fire & Ice US economy. While past hikes hurt capital-constrained small businesses and consumers, recent cuts + a Trump victory are unleashing animal spirits, and creating room for US employment to exceed expectations. Investors need to brace for the next stage of monetary tightening, via a move higher in long-duration Treasury yields.

This leaves 2 questions for us in this report. 1) Are credit yields set to keep rising? Since Dec 1, $IG & $HY yields have increased by 50bps & 40bps to 5.5% & 7.5%, respectively. And 2) When will higher yields lead to wider spreads? Since Dec 1, $IG & $HY spreads are only wider by +2bps & +10bps, to 80bps & 274bps.

On the first question, credit yields are far from hitting a maximum. The great yield adjustment is still underway. The chart below illustrates $IG & $HY index yields are still historically low relative to US cash rates. If the Fed is unable to cut rates further, $IG & $HY index yields still need to climb ~100 & 150bps from current levels.

Very low recession odds + a Fed unlikely to hike implies the next move higher in yields should still be led by steeper Treasury curves. Our US recession gauge indicates 10yr & 30yr Treasury yields could still be up to 60 & 90bps too low today. And the bar for Fed hikes is elevated; core PCE trending at a 2.5-2.6% Y/Y pace isn't great, but is far from a disaster. If Fed policy is loose, but a long hold is more likely than hikes, the only practical release valve to slow down the US economy (tomorrow) is higher long-duration Treasury yields (today).

And investors should prepare themselves for Treasury & credit yields to overshoot higher. Households & large $IG corporates are sitting on a wall of equity/cash. The positive? US economic activity should remain resilient to today's level of rates. The negative? Long-duration US rates will likely need to keep rising to actually produce a US landing & tame US inflation to 2%, at some point in the future.

Hence, to our second question: The 3 criteria below highlight when we expect higher yields to widen spreads. The drivers are more likely to occur via weaker technicals, not fundamentals. But if yields keep rising at their current pace, we expect a minimum ~10bp widening in $IG & ~50bp widening in $HY spreads before Q1 ends…

Same shop with a regularly scheduled Monday / weekly update …

DB: Mapping Markets: Why markets can hold up in a no landing scenario

Markets witnessed a relentless bond selloff last week that’s continued into this morning. For all the reasons put forward why, it’s clear that the two big spikes in Treasury yields were in response to economic data that signalled growing inflationary pressures, not other factors like deficits. This makes sense from a market perspective, as several inflationary forces are clearly building, including higher commodity prices and easier monetary policy, whilst Friday also saw the highest long-term inflation expectations in the UMich survey since 2008.

Given this, there’s been renewed speculation about the “no landing” hypothesis, whereby inflation remains sticky above target, even as growth stays resilient. That’s led investors to price in higher rates for longer, and last week saw a combined bond-equity selloff as a result.

But recent history tells us a “no landing” isn’t necessarily the worst outcome for risk assets. After all, it’s only a problem because the data is strong, as seen with last week’s jobs report.

This echoes a repeated pattern over the last two-and-a-half years, whereby investors worry about sticky inflation and start to price in higher rates. But to the extent that’s happening because of good news and strong economic growth, we also know that risk assets have held up well in that environment, as 2023-24 have demonstrated. And despite the “bad news is good news” narrative that’s developed, we know from the turmoil of last summer that’s only true up to a point, and markets have sold off much more aggressively when there’ve been genuine fears of a slowdown.

Here’s a note for all the inner stock jockeys that may have found themselves here, for whatever the reason …

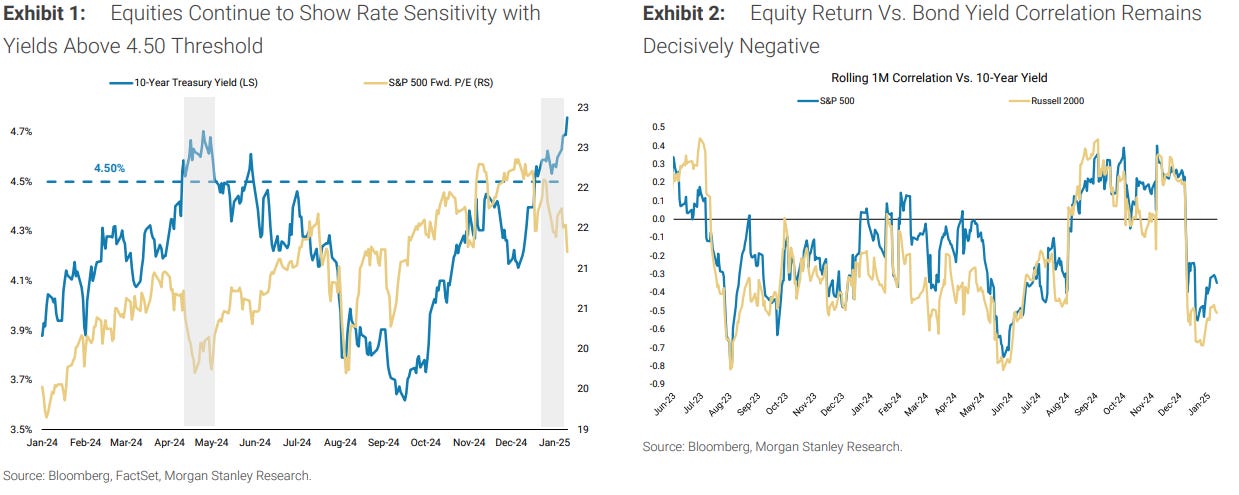

MS: US Equity Strategy: Weekly Warm-up: Rate Move Is Key, While Dollar Should Drive Dispersion

Rates remain the most important variable for equity market direction (beta), while dollar strength is more of a factor at the stock level. We stick with quality, which has been more resilient and reiterate our preference for Consumer Services over Goods into earnings season.

Rates Remain Key for Equity Valuations...As discussed last week, with the correlation of bond yields versus equity performance turning decisively negative in December, interest rate sensitivity has returned as a key driving force for equity markets. Friday's hot payroll report furthered that dynamic as the 10-year yield pushed higher, acting as a headwind for valuation. Amid this rate move, we have increased conviction in our pro-quality stance, which is rooted in (1) our view that we're in a later cycle extension as opposed to the start of a new cycle; (2) the fact that earnings revisions are inflecting higher for the quality factor; and (3) the notion that companies with higher quality balance sheets are likely to show less interest rate sensitivity…

… Oh, right. RATES matter in as far as STONKS go …

Here’s a(nother) note dropped early Sunday morning …

MS: Sunday Start | What's Next in Global Macro: Do the Evolution: Four Themes for 2025

Thematic work has long been a focus of Morgan Stanley Research. We launched Blue Papers and Insights as part of our rebranding in 2016, and in 2021 we established Thematics as a Research discipline. Last year, seven of our ten most-read reports fell under this rubric and, according to our calculations, ten companies levered to our themes arguably contributed more than half of the S&P 500’s total return of 25% in 2024. These numbers underscore the importance of the annual gathering of analysts, strategists, and economists that our Global Head of Research Katy Huberty highlighted in Sunday Start | What's Next in Global Macro: Asking the Big Questions, December 15, 2024.

Let’s drill down into the four key themes for 2025 that emerged from our global collaboration. While none are completely new, all are ‘evolved’ in their application to investment strategy.

Rewiring commerce for a ‘multipolar world…

Longevity…

Future of energy…

AI tech diffusion…

And what if we’re wrong? We’ll evolve our list and research focus. Along the way, we’d love your questions, feedback, and pushback…

SAME SHOP with a global economic and WEEKLY view of the world …

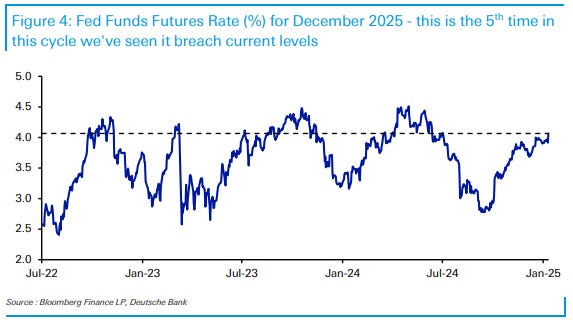

We have said that this year will be a year of many revisions to forecasts, and in our last weekly of 2024 we suggested that the roller coaster ride for central banks was not over yet. The Fed is on the mind of investors around the world, and last year had many swings: from first pricing in almost 7 cuts, then mostly pricing them out, only to reverse on a growth scare in the summer. The run up to and aftermath of the election flipped the narrative again, and then a more hawkish-sounding Fed at the December meeting. But as noted by our US economics team in their write up of the Fed, we may be in store for another year of swings in expectations for the Fed, but also other central banks around the world.

The US is starting the year on solid footing. Last week’s very strong job report showed 256k new jobs in December and we are expecting another solid consumer spending report. That said, we also look for continued deceleration in CPI in this week’s report. After lowering the policy rate by 25bps at the December meeting, Chair Powell was very cautious, and we shifted our forecast to two cuts this year, one in March and one in June. The minutes to that policy meeting, however, read much more nuanced. The Committee sees the same underlying strength in the economy, and upside inflation risks, but generally believe that inflation is trending down. So the cautious tone is from uncertainty, not a fundamental change in strategy. We have stressed that tariffs and immigration restriction will boost inflation but restrict growth. For markets watching central banks, it is important to remember that the inflation effect from tariffs comes quickly, after just a couple of months, while the drag to growth will take a couple of quarters. For now, we will debate how much the strong job report changes the probability on March as the next rate cut, as inflation is likely to trend lower in the first half of the year….

This next note from another French shop and a long-time fan fav (Albert Edwards) offers a couple / few chart favorites of HIS and I’ll highlight a couple which speak to the confusing jobs data (note: this one dated Jan 7, so ahead of the NFP report) …

I never publish a ‘year ahead’ outlook but readers won’t be surprised that I’m sticking with my extreme caution. Adding to the well-known concerns about the extent of the equity valuation bubble, breadth within the equity market deteriorated notably at the back end of last year. This comes at a time when bond yields continue to be squeezed higher, crushed under the weight of super-sized fiscal deficits. Eventually, something will surely snap, just like it did in 1987.

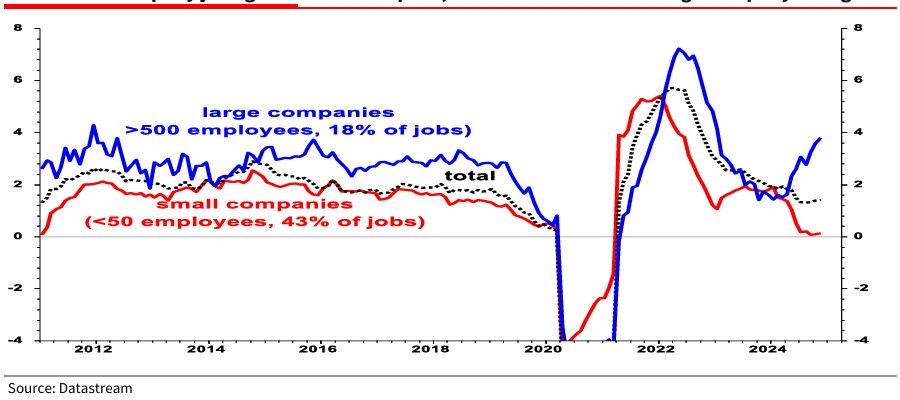

…Another trend that shocked me in 2024 was the K-shaped recovery of jobs. While the ADP jobs survey shows hiring by large companies rising sharply, smaller companies are clearly in pain from higher rates hence their hiring has slumped. The latter is consistent with the Household Survey. US smaller company jobs growth has collapsed, in stark contrast with large company hiring …

On heels of UoMissAgain Friday, seems this snarky commentary is thematic (see WFC HERE, this past weekend) …

China’s December trade data showed even more strength in exports than had been anticipated. This is being attributed to US companies stockpiling ahead of threatened taxes from US President-elect Trump. Such stockpiling may delay the consumer price inflation effects of the taxes (though the narrative of the tax increase is powerful, and may lead to consumer price increases regardless).

Another reason for stronger Chinese exports may be the relatively healthy position of the US consumer. The US December employment report showed low unemployment and job creation, which keeps fear of the future low (and spending high). The New York Fed survey of inflation expectations is due today, but this sort of data is subject to partisan bias (Republicans think inflation risks are collapsing, Democrats think they are soaring)…

A look at the economic week ahead by bond vigilante group …

The week ahead is packed with inflation, consumer, and manufacturing indicators. Long-term Treasury yields could climb closer to 5.00% this week if fears about stickier inflation intensify. We're expecting solid updates on consumer spending. In addition, Q4's S&P 500 bank earnings reported late in the week should be strong and counterbalance any hit to stock valuations from higher yields (chart).

Here's more on what we are expecting this week:

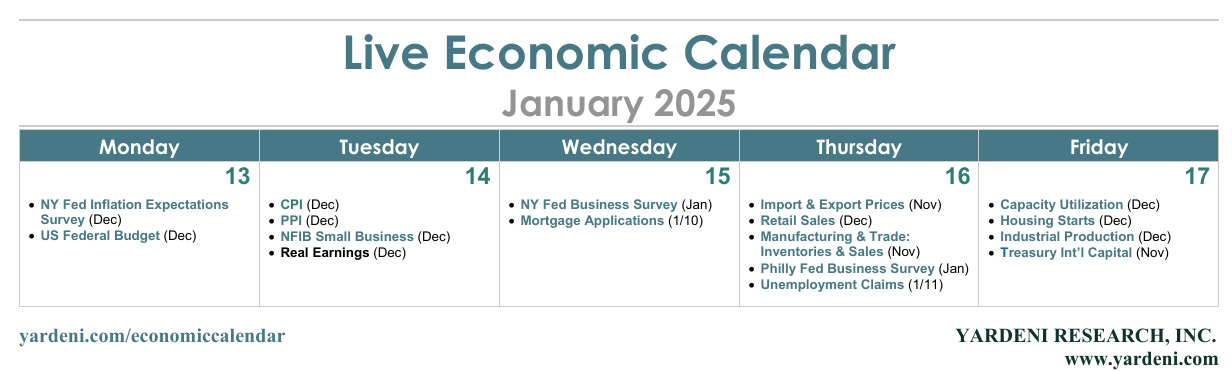

(1) Inflation. According to the Cleveland Fed's Inflation Nowcast, December's headline and core CPI (Tue) are projected to be up 0.38% and 0.27% m/m, respectively. That would put the y/y readings at 2.9% and 3.3%. December's CPI and PPI (Tue) are likely to show core consumer services inflation remains stuck well above 2.0% (chart).

… And from the Global Wall Street inbox TO the WWW … a few curated links …

First up from someone opposing Team RateCUT is a note that, in MY VIEW — which you didn’t ask — supports … well .. Team RateCUT…

Apollo: The Problem with the Current S&P 500 Narrative

The narrative in markets is that the outlook for the US is great, and the outlook for Europe, UK, and China is not good.

For markets, the problem with this narrative is that 41% of revenues in the S&P 500 come from abroad. If we have a recession in Europe and a continued slowdown in China, it will have a significant negative impact on earnings for S&P 500 companies.

AND then this morning there’s this one …

Apollo: The US Household Sector Enters 2025 in Excellent Shape

US stock prices and home prices have increased much faster than US household debt over the past 15 years, see chart below.

As a result, debt in the US household sector is at the lowest level in 50 years relative to assets.

In other words, US households benefit tremendously from the exceptional performance in US financial markets and the continued rise in US home prices.

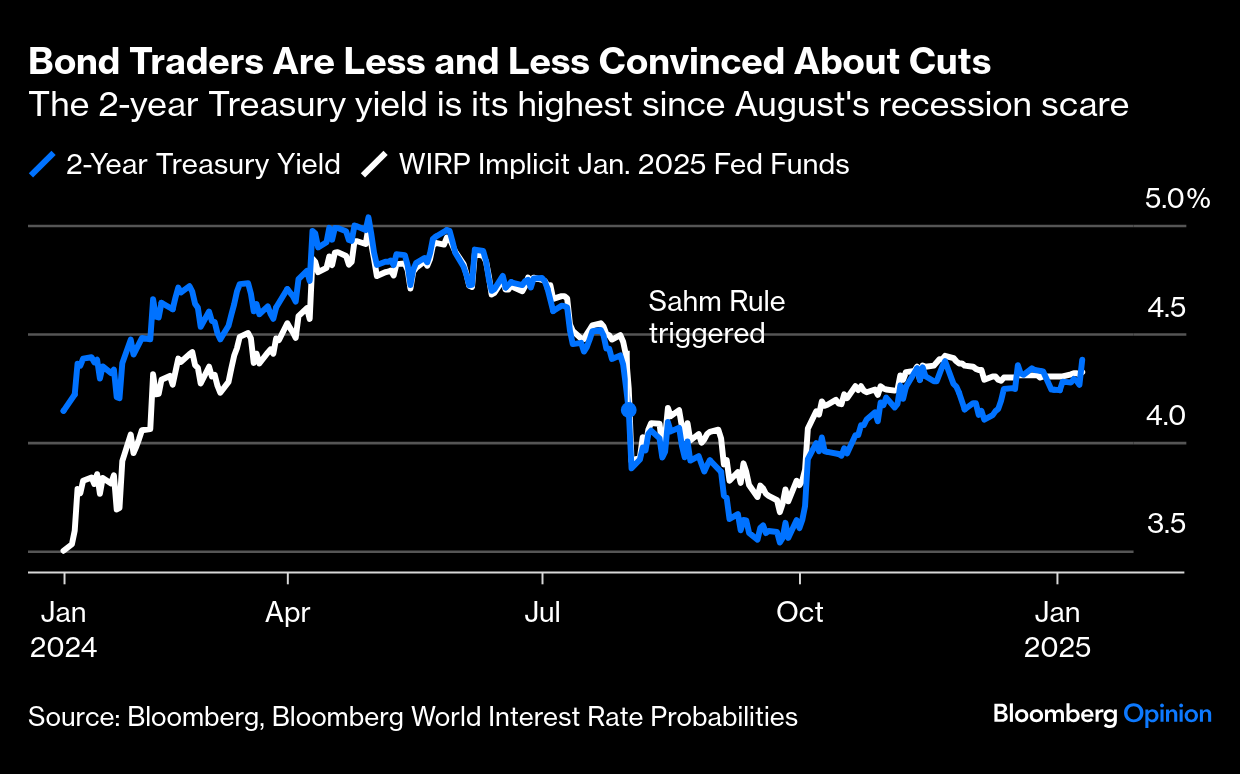

AND next is a view from THE Terminal — with an excerpt and visual caught my eyes (given MY attention TO the front-end noted HERE over the weekend…)

Bloomberg: Doubting America can still cost you a lot of money The bottom line is an economy growing faster than anyone else, though that may not be great for rate cuts.

… Is the sudden change in rate expectations an overreaction? Treasuries’ response suggests otherwise. Friday’s release was a classic example of when good news sounds like bad news, with the two-year yield now its highest since last July, immediately before a disappointing jobs report triggered the Sahm Rule, named for Bloomberg Opinion colleague Claudia Sahm, which predicts a recession once the unemployment rate has risen 0.5% from its low. Expectations for fed funds have always been closely aligned with the two-year:

… As for cuts, Jack McIntyre of Brandywine Global suggests that the December jobs report further proves that the Fed made a policy mistake by cutting rates 100 basis points last year. The longer the Fed is on pause, the more likely that the next move will be a hike, MacIntyre adds. “As important as the labor situation is, the critical variable for the Fed and markets is all things inflation. This week’s inflation data will be more important.”

AND more charts from one of the very good POSITIONS sources out there …

Hedgopia: Even Before Friday’s Jobs-Induced Selloff, Sellers Showed Up Last Week At Important Technical Resistance On Major Equity Indices

… Giving credit where credit is due, the 10-year treasury yield was expecting this. The FOMC began an easing cycle last September by slashing the benchmark rates by 50 basis points, followed by two more 25-basis-point cuts. The 100-basis-point cut currently puts the fed funds rate at a range of 425 basis points to 450 basis points. On the day the FOMC began its two-day meeting in September, the 10-year tagged 3.6 percent intraday; last Friday, it closed at 4.78 percent. The long end of the yield curve has gone the other way.

The 10-year has now rallied above both horizontal resistance at 4.3s and trendline resistance from October 2013 when it hit five percent and headed lower (Chart 2). Rates are overbought on the daily, so could come pressure potentially. In this scenario, there is immediate support at 4.5s, which, if defended, could then open the door to a test of five percent in due course.

…Simplistically, the higher the interest rates the lower the valuations accorded equities, as their underlying businesses get discounted using these rates. It is worse if leverage is used, which is mostly the case in the small-cap arena….

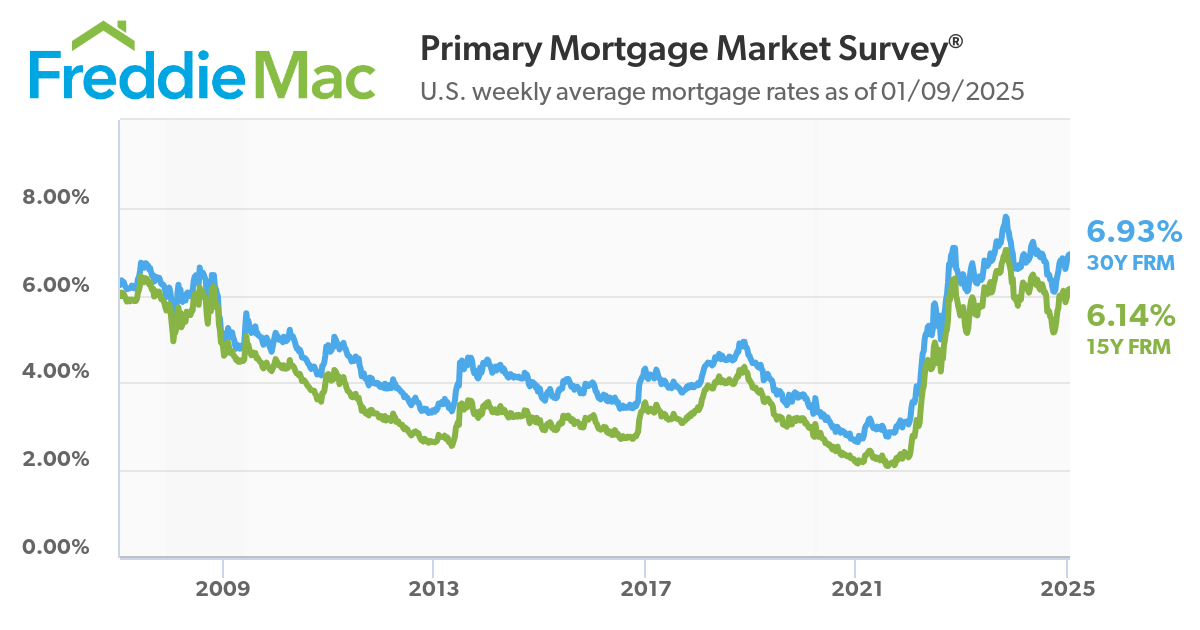

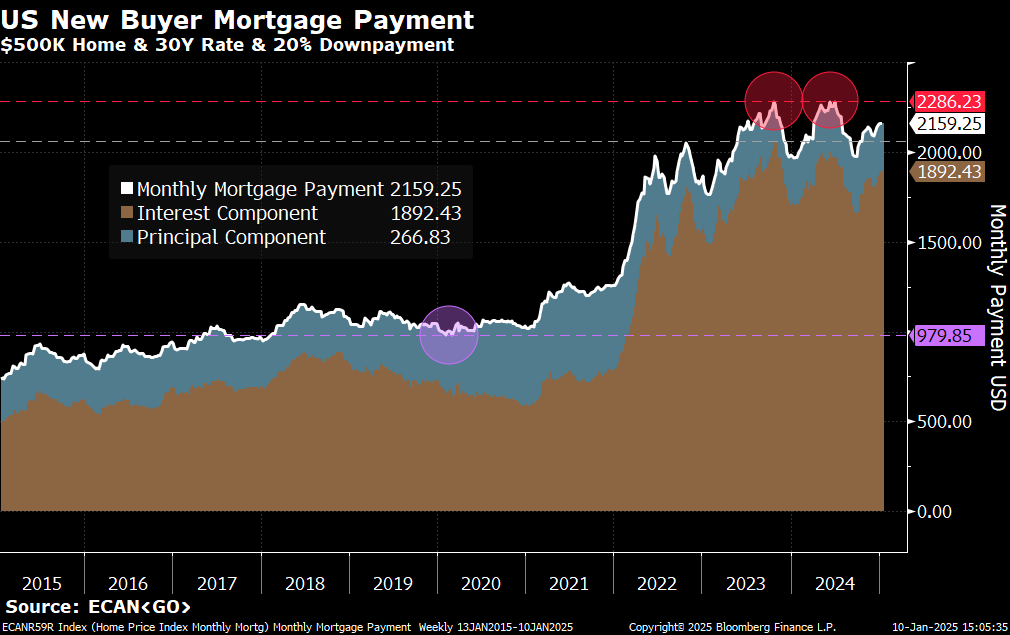

AND as you know by now, I’m a visual learner so this one speaks to me (as well as those maybe on Team RateCUTS) …

…Home affordability Mortgage rates used to be very low. For much of 2020 and 2021, the average 30-year fixed mortgage rate was below 3%.

With tighter monetary policy and the improving outlook for economic growth came higher interest rates, including higher mortgage rates. In recent months, the average 30-year fixed mortgage rate has hovered around 7%.

To better understand what this means for homebuyers, Bloomberg’s Michael McDonough charted the trajectory of monthly mortgage payments based on reported mortgage rates. For a $500,000 home, a new homebuyer is paying about $2,100 a month today versus about $980 at the 2020 low.

Among other things, the U.S. housing market faces supply challenges. But affordability has certainly played a role in home sales activity cooling from once-hot levels…