while WE slept: USTs under modest pressure; "...spikes in geopolitical risk have had no observable effect on 6m SPX returns over the last few decades" (Barclays)

Mom always said that if you don’t have anything nice to say, well, don’t say anything at all and so, here’s a nice look at WEEKLY 30yr yields with a bullish look and feel …

30yy WEEKLY: TLINE resistance closer to 4.50% and support up at recent cheaps (5.00 - 5.10) …

… momentum clearly presenting itself as a bullish impulse within the grander bear (TLINE)scheme of things … I’d note i’ve circled previous TLINE hold just as rates were CUT 50bps in September of 2024 …

…AND with that in mind — let us hope it is going to be different this time — this bullish momentum looks to be confirmed on longer-term (ie monthly) charts as well and this should get / keep one and all on the hook, lookin’ for 'dipORtunities’ (higher rates) to get (or stay) long in some way shape or form.

In as far as WHY, a look back at some of what helped shape / shift the price action yesterday (those who don’t learn from history doomed to … never mind …)

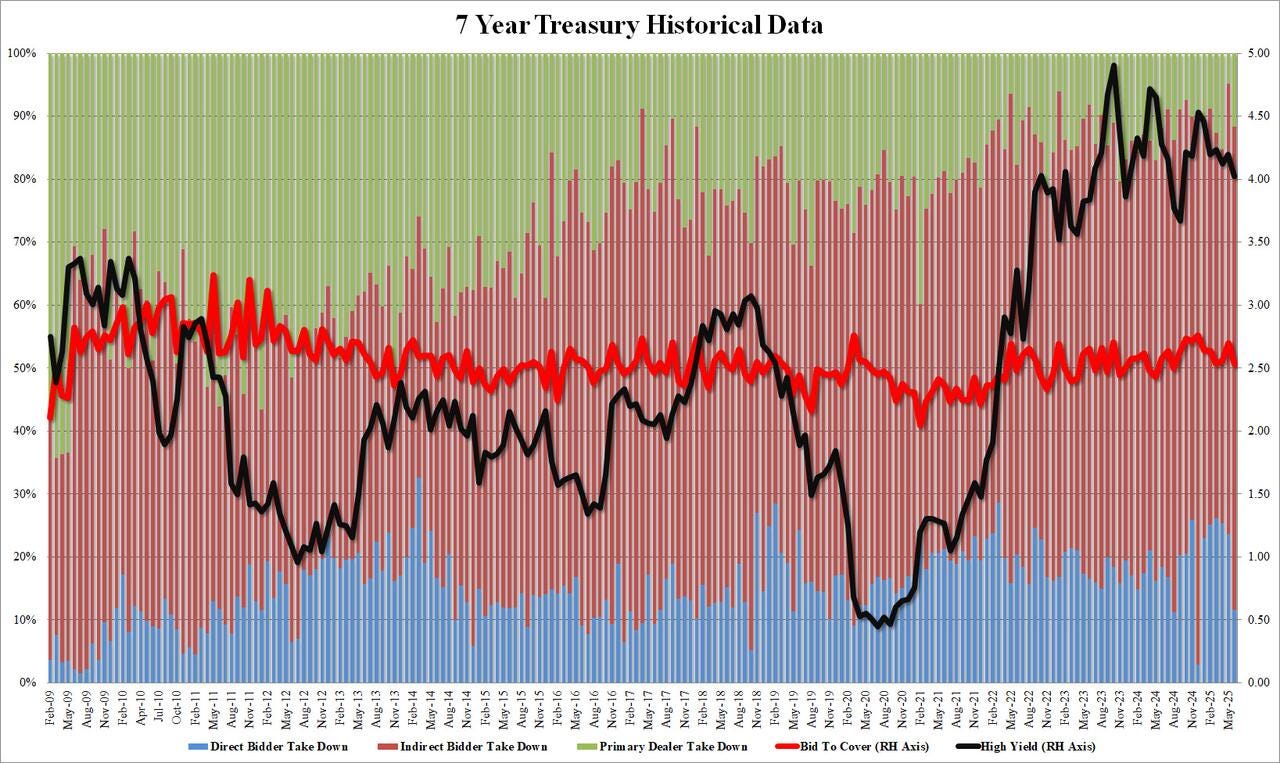

Supply now fully in the rear-view mirror and 7s went OK …

ZH: Stellar 7Y Auction Stops Through After Jump In Foreign Demand

After two mixed coupon auctions this week (a solid 2Y, a subpar 5Y) moments ago the Treasury concluded the week's final coupon auction when it sold $44 billion in 7Y paper in a well-received sale…

…The bid to cover was ugly: it dropped from 2.695 to 2.531, the lowest since August 2024 and obviously well below the six-auction average of 2.637.

The internals were most solid, with Indirects rising to 76.7%, up from 71.5% in May and the highest since December. And with Directs taking just 11.62%, the lowest since December's record low 2.85%, Dealers were left with 11.6%, up from May's record low of 4.85%.

Overall, this was a solid auction, arguably the best of the week, and one which came with yields across the curve already near session lows so there was little movement: the 10Y was down at 4.257% after the auction broke for trading, barely changed from where it was earlier.

The liquidity event went well despite / because of the mixed flow of data earlier in the session.

Data continued to indicate cracksforming and Team Rate Cut(s) at attention …

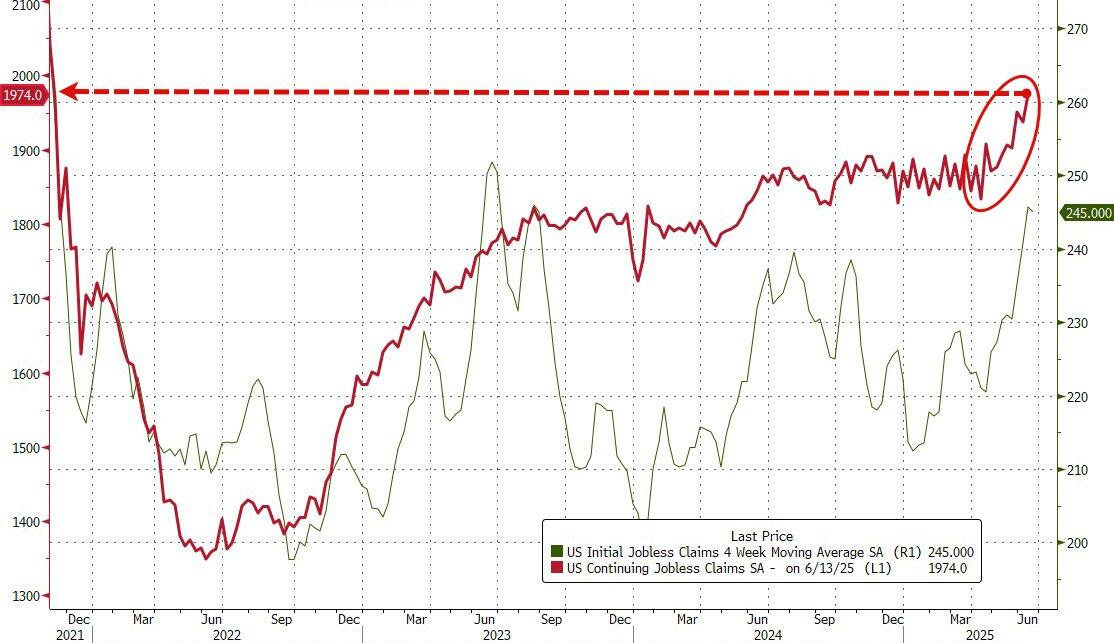

ZH: Labor Market Creaks... Continuing Jobless Claims Highest Since Nov 2021

… Continuing jobless claims kept rising to 1.974 million Americans - the highest since Nov 2021...

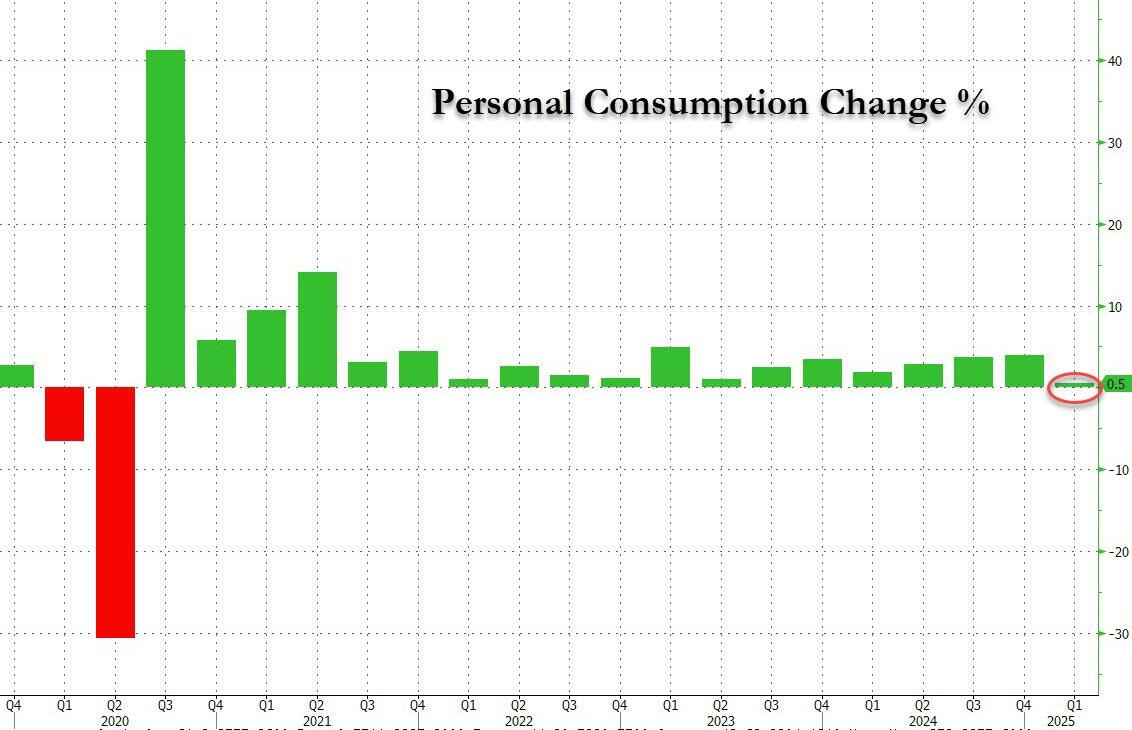

ZH: Q1 GDP Revised Lower As Personal Spending Unexpectedly Prints Weakest Since Covid

… While there were few notable changes between the initial report and the first and second revision, the most notable one was in personal consumption which has continued to deteriorate, and was first cut by a third from 1.7% increase in the original print to 1.2% in the first revision, and today, to just 0.5%, making this the weakest quarter for personal spending since the covid crash.

… but then, for each and every data point, there’s an equal and opposite one, equally compelling …

ZH: Boeing Binge-Buying Sparks Biggest Jump In US Durable Goods Orders In 11 Years

ZH: Biggest Export Decline Since COVID Lockdowns Unexpectedly Widens US Trade Deficit In May

… The tariff front-running is over... obviously.

As Bloomberg reports, the wider May deficit indicates trade may contribute less to second-quarter growth than initially anticipated. Prior to the latest figures, the Federal Reserve Bank of Atlanta’s GDPNow estimate showed net exports contributing more than 2 percentage points to second-quarter GDP.

… and then there was a point of light for either / both opposing views reading this however one wants …

ZH: US Pending Home Sales Rose In May, But Remain Near Record Lows

… More over the weekend but for now, no need to get in the way as …

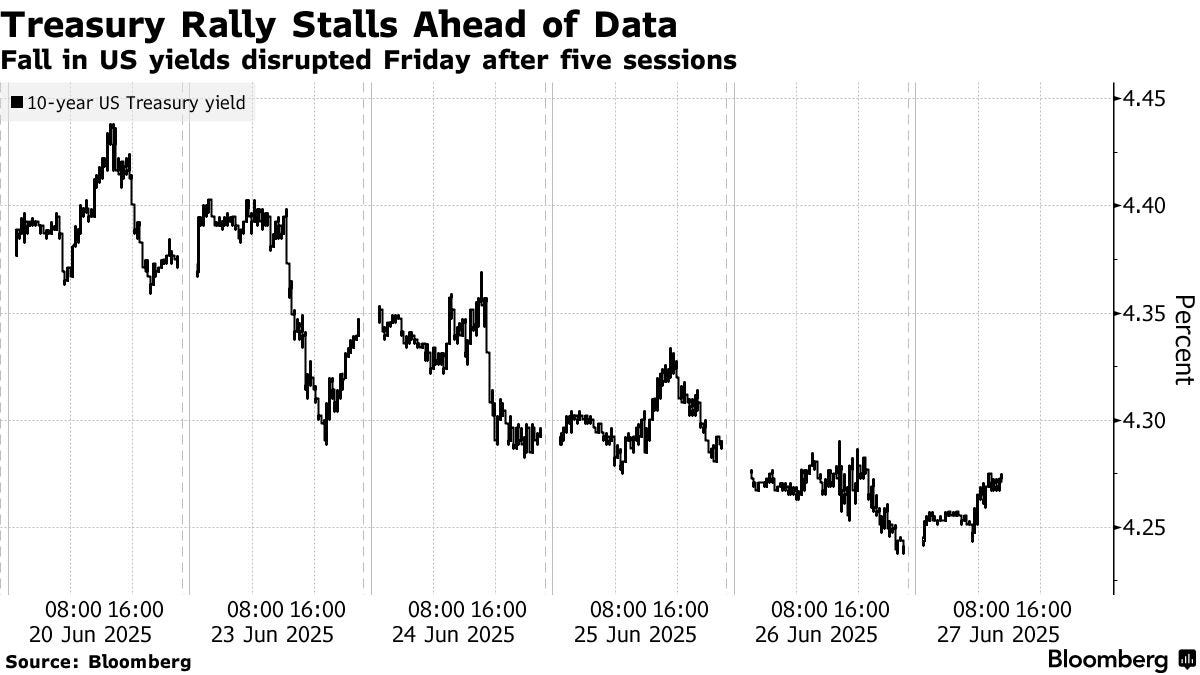

… here is a snapshot OF USTs as of 658a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: European bourses benefit on US-EU trade optimism, DXY lower & US equity futures gain into PCE … USTs are under modest pressure with Bunds also hampered following French/Spanish inflation figures … A contained/slightly softer start to the day for USTs. Benchmark pulling back from Thursday’s 112-03 MTD high, but only marginally with the current trough at 111-26+, comfortably clear of Thursday’s 111-21 base. Focus overnight has been on the latest US-China framework agreement, but essentially just firming the prior Geneva/London talks. Focus today now turns to US PCE and a couple of Fed speakers.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Claims, a JOBS REPORT PREVIEW and GDP recaps from across the pond …

26 June 2025 Barclays: June employment preview: Moderating into summer

Available indicators suggest that nonfarm payroll employment will slow in June, with the headline moderating from +139k to +100k. We think the unemployment rate likely held steady at 4.2% and that hourly earnings will post a trend-like increase of 0.3% m/m (3.9% y/y).

26 June 2025 Barclays: Initial claims: Resilience restored

Today's initial claims estimates leaned against the narrative that the labor market is losing vigor, with initial claims dropping to their lowest level in five weeks, while continuing claims remained elevated. We see little in the details that would have us downplaying today's estimates.

26 June 2025 Barclays: Third estimate of Q1 GDP revised lower on consumer spending

The BEA's third estimate reduced Q1 GDP growth by 0.3pp, to -0.5% q/q saar, with downgraded consumption more than offsetting an upgrade to net exports. The incoming GDI estimate placed growth at 0.2% q/q saar, a sharp deceleration from the prior quarter's 5.2% q/q saar growth.

26 June 2025 Barclays: Incoming data shake up Q2 GDP tracking composition

We received a plethora of data today including the third estimate of Q1 GDP, and multiple advance economic indications for May. The cumulative effect of all of these data provided a slight bump to our GDP tracker of 0.1pp, now at 1.3% q/q saar. This comes amid some sharp component tracker changes.

Same shop with a few words (and a picture) ‘bout stocks in / around geopolitical events …

History suggests that recent unrest will pose little headwind for US equity returns; spikes in geopolitical risk have had no observable effect on 6m SPX returns over the last few decades. At the sector level, Industrials tend to outperform following geopolitical risk spikes, while Energy lags.

…Treasuries continued to rally on Thursday, a move that was more a reflection of the ongoing speculation that the President will soon announce his preferred replacement for Powell as Fed Chair. It goes without saying that the incoming Fed Chief will be viewed by market participants as more dovish, although we’re beginning to worry that the ‘Dove in 2026’ trade has been overpriced. At present, the futures market has fed funds approaching 3.0% by September of next year. In contrast, the SEP indicates a much more gradual process of normalization over the next two years before the eventual return to the Fed’s working definition of neutral at 3.0%. To be fair, we remain in the 50 bp camp for 2025 and another 100 bp in 2026 – so we’re not arguing with the market pricing as we think it accurately reflects the risks. Instead, the fact that the front-end of the market remains biased toward even lower rates and another leg lower in 2s implies that the arrival at neutral is priced in as a June/July 2026 event. Hence, our concern that the market is getting ahead of itself, or chasing the dove, as it were.

Recall that earlier this year, the 50 bp cut camp was viewed skeptically as chatter regarding no cuts or even a potential hike made the rounds. As recently as mid-February, 2-year yields were ~4.40%. Now at 3.72%, the market has renewed confidence in the Fed’s messaging regarding returning to rate-cutting mode as the goods inflation linked to the trade war is expected to only have a temporary impact on consumer prices. The dovish tone from certain policymakers has reinforced the prospects for a near-term cut and the futures market shows investors seeing a 21% probability of a 25 bp cut next month. 21% odds at this stage seem appropriate as the market awaits next week’s BLS employment report – which we expect will be the deciding factor for market expectations, although not necessarily for the Fed.

The path toward a July Fed cut would not only involve convincing evidence that the labor market has softened materially, but also further confirmation that the pass-through of higher tariffs to consumer prices remains muted. Therefore, in the event of a weaker payrolls print next week, the Fed would also need to see the details of the June CPI data (released July 15) before being comfortable in signaling that the Committee is actively considering a cut at the upcoming meeting. This isn’t our base case. Moreover, the weakness in labor data required to put a July cut on the table is significant and would need soft inflation as well – neither of which are foregone conclusions.

Instead, our base case remains that the FOMC will maintain a steady policy rate throughout the summer and won’t seriously consider restarting normalization until mid-September…

US stock futures have broken above highs this week, and we continue to think that technicals remain very positive. We take a look at key levels to watch in this note …

…Nasdaq 100 futures (NQ1): Nasdaq 100 futures have already cleanly broken the 22320 resistance level, and are now testing the 22769 resistance (ascending short term resistance). Bullish signs are similar to S&P e-minis:

Bullish break above 22320, after completing the bull-flag suggested move towards ATH.

Weekly slow stochastics continue to tick higher in overbought territory.

CTAs continue to be 'max long' in Nasdaq 100 futures according to our CETS team's CTA tracker.

Broader macro trends suggest further room for a move higher.

While resistance is nearby at 22769, we think this is likely to be broken as well. We see stronger resistance at the longer term ascending resistance at 23238.

A rather large German bank highlighting some positive developments after the close of stocks yesterday and with regards to TRADE …

… The continued positive momentum in equities was impressive. We seem to be in a sweet spot post Middle Eastern calm and pre the July 9th reciprocal tariff extension deadline. This will start to come into view soon, and headlines are starting to bubble up. Lutnick last night said that an agreement with China has now been agreed and that imminent plans have been made to agree deals with ten of its major trading partners. It's not clear if this includes the EU and trade was clearly a key subject at the EU leaders’ summit that concluded last night. European Commission President von der Leyen revealed that the EU was assessing the latest counter-offer proposed by the US, saying “We are ready for a deal. At the same time we are preparing for the possibility that no satisfactory agreement is reached”. There have been some tensions over the EU’s approach to the talks, with Germany’s Chancellor Merz earlier calling the Commission’s negotiating strategy “far too complicated” as he favoured a “quick and simple” deal. Meanwhile, France’s Macron said last night that he would settle for 10% tariffs from the US but that this would result in the same levy being applied to US goods. So some event risk to watch out for over the next couple of weeks …

Cuts. Rate CUTS … well, it appears things are lining up for the doves … or so they say …

27 June 2025 ING Rates Spark: Things are lining up for the doves

Friday's economic data could help build the case for more dovish market pricing. In the US, markets may start assigning a higher probability to a July cut. A stronger euro adds to the disinflationary forces at play and could push markets to consider a 1.5% landing zone again

Earlier Fed cuts could have dovish spillovers to the eurozone The dovish vibe in US rates markets may be fuelled further by Friday’s personal spending and PCE inflation data. The core PCE is likely to be just 0.1% month-on-month, which would by itself support a cut as early as next month. Of course, the fear of tariff-related inflation is not yet over. But if the personal spending numbers from May show significant weakening on the back of worsening consumer sentiment, then markets should be willing to increase the chance of a July cut. Right now, the probability already stands at around 25%, and with payroll numbers next week, a lot can still happen.

Lower US rates helped the dollar weaken and consequently pushed the euro stronger, weighing down on the eurozone’s inflation outlook…

… AND ‘bout said CUTS, there’s another angle to consider if only indirectly …

27 June 2025 ING: How President Trump’s plans will impact the US deficit

Big isn’t beautiful when it comes to government debt, but tariffs and the Department of Government Efficiency (DOGE) help to plug the hole left by President Trump’s latest fiscal bill. The net effect will be weaker growth, with US government debt remaining on a worrying trajectory

…Here's how US debt dynamics continue to worsen, driven by the primary deficit...

In the US, the primary deficit ran at around 4% of GDP in 2024 and is projected at around 3% of GDP in 2025. If we assume a 3% primary deficit, for the debt/GDP ratio to fall, then the value of GDP must grow by more than the average coupon print plus 3%. The weighted average fixed coupon print right now is around 2.85%. Bills then tend to account for around 20% of total debt and are rolling over at a cost of around 4.25%. That comes to an average interest rate cost of a little over 3%.

The average coupon print plus the primary deficit is around 6%. So the value of nominal GDP needs to rise by some 6% for the debt/GDP ratio to stabilise. A repeat of 2024’s c.4.5% value increase risks adding 1.5% to the debt/GDP ratio on an annual basis. Something similar over subsequent years would continue to build the debt/GDP ratio. And, as the debt/GDP ratio rises above 100%, the problem is amplified.

Given we see some upside risk to the CBO’s assumption that interest rates move lower from current levels, we expect the debt-to-GDP ratio to rise by between 1.5pp and 2pp of GDP per year.

… AND ‘bout those rate CUTS … it’s when not if and the when is not likely in the near-term … Why? Because the data ‘bout to turn up the heat …

Japan exhibited some disinflation with the June Tokyo consumer price data. Using the international definition of core inflation, the rate slowed to 1.8% y/y. A lot of the headline inflation seems to be driven by non-fresh food, perhaps suggesting relative price shifts rather than strong, broad inflation momentum.

France and Spain offer the flash estimates of June consumer price data. Both are likely to produce fairly stable headline rates. Goods prices are signaling disinflation (or in the case of France are comfortably showing outright deflation). This reflects expectations of a slowing US economy, and ongoing consumption shifts in favor of fun.

US May personal income and consumption data is due. There is likely some payback after consumers brought forward durable goods purchases ahead of trade taxes (that pattern was more Democrat than Republican consumers). The deflator will not show much impact from trade taxes yet—that will be looked for a couple of months hence.

US Trade Secretary Lutnick declared an agreement with China over trade. Markets do not care, as this seems to be just a codification of the agreement made in Geneva and reaffirmed in London. Lutnick promised ten trade deals were coming (no news on whether this includes the penguins of the Heard and McDonald Islands).

Same shop with some reason to think cuts maybe NOT on way here, in the USA, so quickly …

27 June 2025 UBS: US Economic Data Retail spending shows signs of recovery

UBS Evidence Lab Nowcasts provide an early read on June indicators UBS Evidence Lab Nowcasts provide timely projections of several key monthly US economic indicators ahead of the official releases and other forecasts. Nontraditional big data is used to generate the Nowcasts using available data before the end of the month. These Nowcasts differ from the data forecasts published by the US Economics team, whose projections use a separate methodology and often incorporate additional data. The June Nowcasts are shown in Figure 1. Links to the real-time history of the modelgenerated Nowcasts are below the table, in order to allow clients to backtest and assess the signal.

Nowcast suggests recovery in retail spending Preliminary retail spending excluding autos and gas is estimated to rise 0.36% in June, flipping positive from May's 0.12% decline. For June, UBS Evidence Lab Nowcast expects core CPI to increase by approximately +23bps, slightly above the US Economics team's preliminary estimate of a +21bps increase (link here). CPI rents are expected to increase 25bps in the UBS Evidence Lab Nowcast. Estimates indicate a rise in CPI lodging and airfares. New car prices are estimated to rise 21bps from the previous month, whereas used car prices are expected to decline in the UBS Evidence Lab Nowcast. The Nowcast points to a headline CPI SA monthly increase of 21bps. The US Economics team's preliminary projection for headline CPI is +22bps (link here)…

… AhhhhDURABLEs …

June 26, 2025 Wells Fargo: Beyond Aircraft-Related Pop, Durable Orders Steady in May

Summary A surge in aircraft orders is responsible for the leap in durable goods for May, but even beneath the surface underlying orders activity perked up a bit. Still, durable shipments as well as other data out this morning on Q1 GDP, trade and jobless claims suggest a weaker first-half of the year for U.S. growth.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

About those impending rate cuts …

June 26, 2025 at 2:15 PM EDT Bloomberg: Majority of Fed Officials Leaning Against July Interest-Rate Cut

(Bloomberg) -- A flurry of Federal Reserve officials this week made clear they’ll need a few more months to gain confidence that tariff-driven price hikes won’t raise inflation in a persistent way.

… and somewhat more …

June 27, 2025 at 10:19 AM UTC Bloomberg: Treasuries Slip as Investors Take Breather on Fed-Driven Rally

… “We do not see a further rally in Treasuries from these levels,” said Mohit Kumar, chief European strategist at Jefferies, who predicts US bonds will underperform German peers. “We believe that fiscal deficits would be the dominating concern for markets in the second half of the year.”

…Fed officials including Christopher Waller and Michelle Bowman, two Trump nominees, signaled in recent days they’d be open to lowering rates as soon as the next meeting. That’s as candidates jostle to replace Powell, with investors and analysts reckoning his successor will most likely share Trump’s dovish bias…

…Wells Fargo strategists see the potential for the spread between US 10-year and 30-year yields to widen to 75 basis points by end-2025, in what they describe as a “fiscal blowout” scenario. The difference in yields is currently around 55 basis points.

“We expect very long duration bonds to continue lagging their five- and ten-year counterparts,” a team led by Michael Schumacher wrote in a note. “The significant relative rise in 30-year yields is due to investor concerns about potential supply.”

and … More on GDP ahead of tariffs …

Jun 26, 2025 WolfST: The Corporate-Profit Explosion Stalls in Q1, on the Eve of the New Tariffs

In some industries, profits surged. In others, profits sagged. By major industry.