STILL watching long bonds vs triangulating range support (4.93) and tomorrows WEEKLY closed will be scrutinized a bit more.

Markets — for NOW — remain calm based on futures just above but there are a few things bubbling under the surface.

Heading TO Bloomberg.com early today and you’ll see a host of funTERtaining headlines to consider (or help explain) this mornings atmosphere …

From trillion dollar wipeout (tech) to ‘sudden’ 17% plunge in Silver. And oh, just for good measure, lets throw in survey offering reminder that stocks to beat bonds (on vol adjust basis).

I’ve got some links below and with little else on MY mind at this very moment, a couple / few visuals to consider … Tech wreckin …

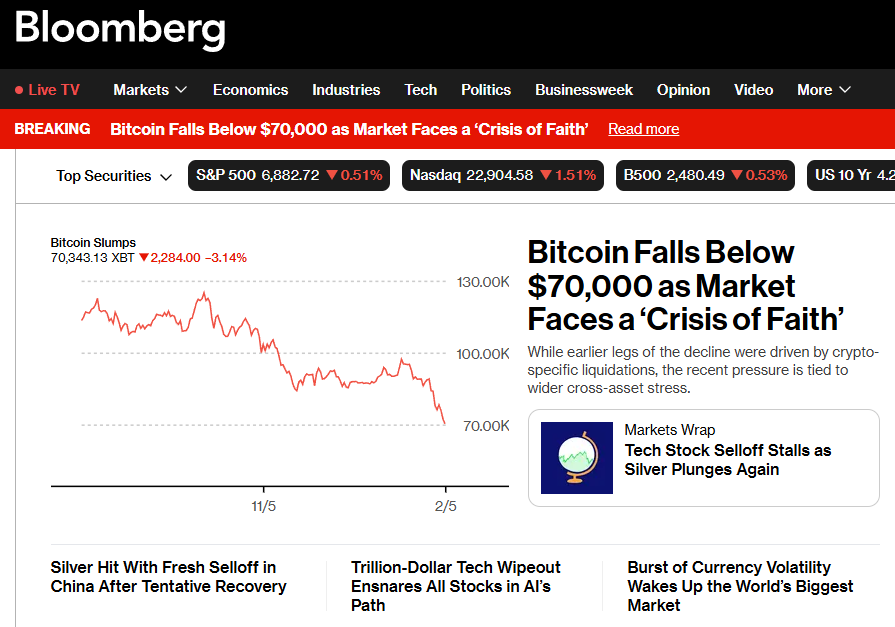

Bloomberg: Trillion-Dollar Tech Wipeout Ensnares All Stocks in AI’s Path

… and markets which became safe haven ‘ish are, well, not so, any more … Overnight, back to watching Hi Ho Silver …

ZH: Silver Crashes 20% As China Opens, Gold & Bitcoin Also Plunging

… and we thought flows TO metals were solidified as crypto was selling off …

Bloomberg: Bitcoin Falls Below $72,000 as Market Faces a ‘Crisis of Faith’

… and there were also some geopolitical turmoil h’lines to be consumed …

ZH: White House Nukes Friday's Planned Iran Talks, Oil Spikes

… and with them in mind, there is never a shortage of funDUHmentals …ADP showed a GAIN … that’s good BUT it was ‘far short’ of the CONsensus …

Feb 4 20268:15 AM EST CNBC: Private payrolls rose by just 22,000 in January, far short of expectations, ADP says

Private companies added just 22,000 positions for January. The total was less than the downwardly revised 37,000 increase in December and below the consensus forecast for 45,000.

The report starts 2026 off on basically the same note where 2025 ended: A lackluster job market in a low-hire, low-fire environment…

… AND then some solid growth troubles (?) …

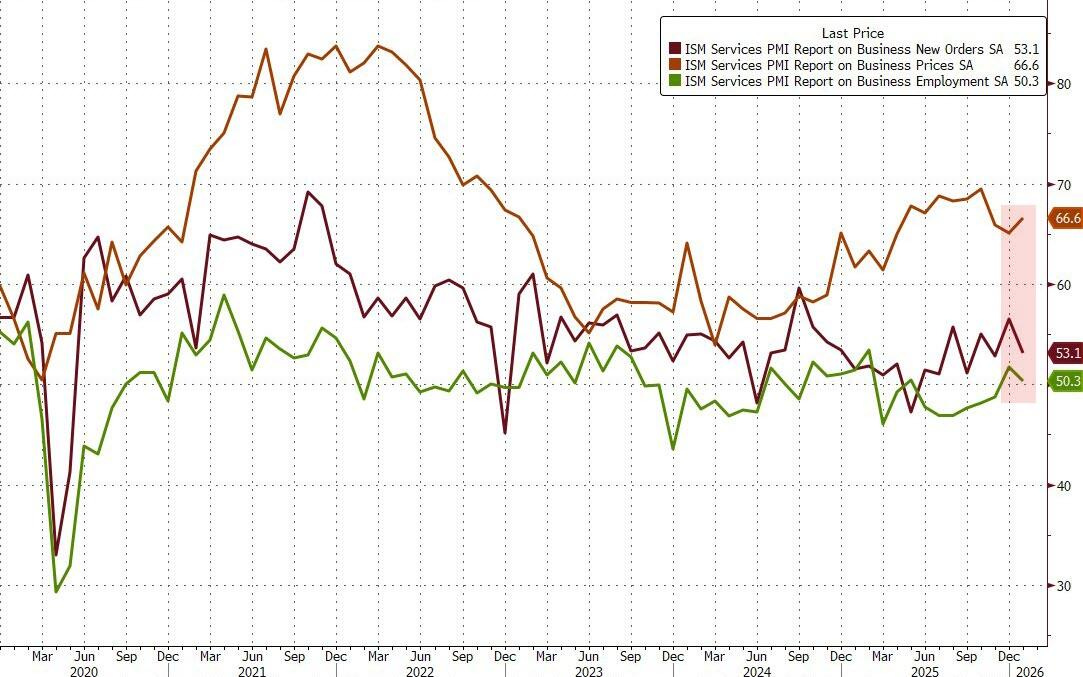

ZH: US Services Sector Surveys Signal Solid Growth In January, But...

…However, that is a lower gear compared to the pace of expansion seen prior to December’s slowdown, and hints at GDP growth cooling in the first quarter.

Consumer-facing companies are increasingly reporting a challenging environment, with demand for services falling in January having nearly stalled in December, “reflecting low levels of consumer sentiment and cost of living pressures,” Williamson noted.

The ISM data showed a triple whammy of higher prices, lower new orders, and lower employment...

However, as Williamson concludes, “inflationary pressures in the service sector meanwhile remain elevated, blamed on the pass though of tariff related price increases and wage growth, though stiff competition is often reported to have limited the impact on final selling prices.”

“While financial and business service providers are reporting a more resilient picture, demand growth here is also showing signs of fraying amid heightened concerns over the economic outlook, in turn often blamed on political uncertainty.

However, there is a silver lining, as Williamson concludes: “lower interest rates and favorable financial conditions, higher government spending, combined with more active sales and marketing efforts, are propping up business sentiment and spending, and also encouraging modest hiring.”

… and we can always rely on / HOPE (not a strategy) of that old adage whereby supply creates it’s own demand …

ZH: No Surprises In Treasury Refunding Statement: No Auction Size Increases For "Next Several Quarters"

… and we’ll have NEXT Wed to look forward to …

ZH: January US Jobs Report Rescheduled For February 11

… good luck, Warsh (IF he gets the official nod and votes) …

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 649a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Global equities mixed; markets await ECB and BoE rate announcements … Fixed income benchmarks are mixed; USTs incrementally firmer, whilst Gilts underperform on political woes … USTs are currently firmer by a couple of ticks and trade within a narrow 111-18+ to 111-24 range. Not much driving things for the benchmark this morning, but the focus has been on geopolitics. On Wednesday, it was reported that the US-Iran talks were cancelled, but are now back on and set to happen on Friday. Back to the US, the BLS provided an updated data schedule following the recent partial shutdown. JOLTS is set to be released today; NFP on Feb 11 and CPI on Feb 13. That aside, Jobless Claims is due today, with traders looking to see if the labour market remains in its recent “low hiring – low firing” environment.

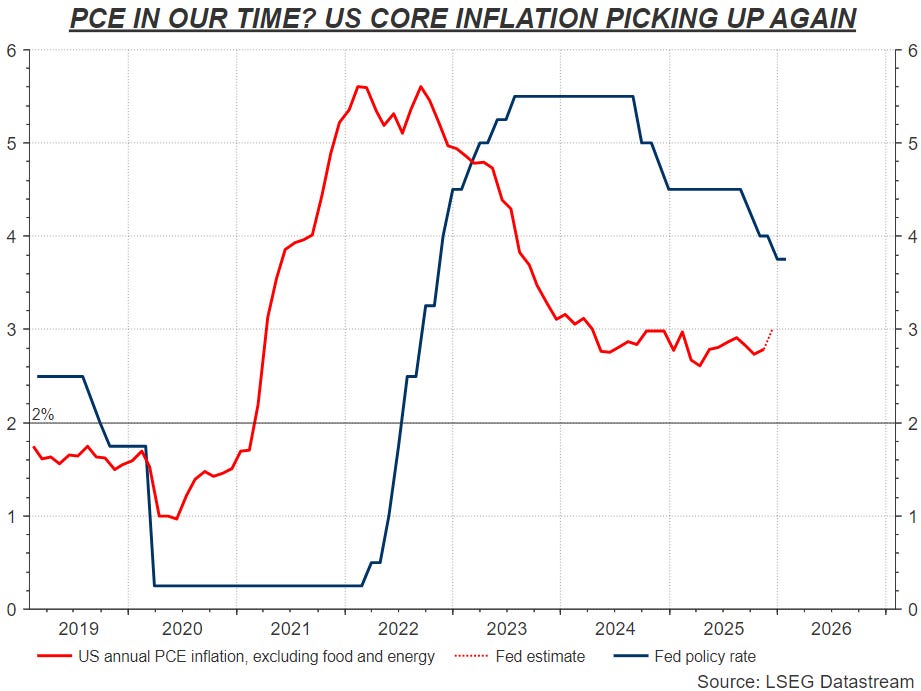

…US inflation isn’t subsiding. It’s heating up again The main reason political pressure on the Federal Reserve has not caused markets to price in deeper interest rate cuts is perhaps the simplest: U.S. inflation is just too high to justify it, and there are signs it may be picking up again.

The Fed’s favored measure of inflation - core personal consumption expenditures (PCE) inflation, which excludes volatile food and energy prices - is creeping higher again, and several alternative gauges of retail prices also show some heat building as 2026 is getting underway.

Even though the December PCE report is not due out for another two weeks, Fed Chair Jerome Powell, opens new tab made clear last week that the central bank now assumes that core PCE inflation ran at 3% in the final month of last year.

Not only is 3% core inflation a full point above the Fed’s inflation target, but it’s going in the wrong direction. It would be the fastest rate in over two years, more than 40 basis points higher than it was running last April.

The ISM services PMI held steady at a solid 53.8 in January, with mixed readings across major components. The main news was in the comments, which indicate a resurgence of unease amid January's renewed tariff threats.

BEST in show … data and a few thoughts as mkts came to a close …

February 4, 2026 BMO ADP Disappoints at +22k vs. +45k anticipated BMO: February Refunding: Coupons Steady; “Several Quarters” Language Retained BMOISM Services Unchanged at 53.8; Details Mixed; UST Bounce

February 4, 2026 BMO Close: Setting the Stage for Steepening

…The unifying theme throughout Wednesday’s session was that of a steeper yield curve. 2s/10s moved above 71 bp while 5s/30s breached 109 bp. The resumption of the steepening trend was encouraged by the refunding. More specifically, what the Treasury Department didn’t announce – buybacks weren’t increased, and bond issuance wasn’t decreased. We were not expecting either change, although it’s fair to characterize such moves today as outlier/ low-probability risks, but risks, nonetheless. As a result, underperformance of duration is best viewed as simply the passing of yet another event risk, and we see the US rates market settling comfortably into the range. All else being equal, we would have expected a more bearish move in the wake of the refunding. Weaker stocks and the disappointing ADP print likely prevented more compelling selling momentum…

…Our core steepening bias has clearly found solace in Wednesday’s price action with 2s/10s now easily within striking distance of the local extreme of 72.6 bp. Bessent didn’t increase the size of 10s and 30s, but that doesn’t eliminate the need for an auction concession. Moreover, progress through earnings season will rekindle conversations about corporate issuance and rate-lock selling ahead of the weekend. The incoming data is unlikely to materially shift investors’ interpretation of the crosscurrents of economic momentum. Consumers, while low in confidence, continue spending and until there is a more dramatic increase in unemployment, we expect this will remain the case. With a watchful eye on the performance of risk assets, we’ll be tracking the overnight price action for evidence of dip-buyers given the most recent cheapening of duration…

Stimmy and supply … unrelated or …

04 Feb 2026 18:38 GMT BNP US: Taking stimulus proposals seriously and literally

KEY MESSAGES

Although President Trump’s interest in fiscal stimulus checks seems to have waned in recent months, we still see additional fiscal stimulus measures (aimed at affordability concerns) as a key upside risk to our US economic outlook.

Sending $2000 stimulus checks to households would push growth and inflation higher, potentially lowering the unemployment rate to levels last seen during the pandemic reopening.

We think the Fed would be deeply reluctant to consider rate hikes, especially under new leadership. However, this option likely remains on the table if necessary to prevent an inflationary reacceleration.

04 Feb 2026 17:17 GMT BNP US rates: Treasury refunding - keeping it short

KEY MESSAGES

February refunding showed that the Treasury is evaluating “future increases to coupons” with a “focus on trends in structural demand”, which shows “growing demand” for Treasury bills, suggesting that if the US Treasury does deliver coupon increases in 2027, it will happen at the short end of the curve, along with higher T-bill supply (i.e. “T-bill and chill”).

We see this as a covert endorsement of our view of underweighting long-end issuance versus the short end in a bid to help with affordability concerns. Overt backing would involve specifying no coupon increases at the long end or hinting at coupon cuts.

We think the focus on affordability remains, and is likely to manifest in ways that keep UST yields bid versus swaps. 30y swap spread remains attractive outright in our eyes, but also as a hedge for our 1s30s steepener view.

Trade: Maintain long 30y swap spreads..

Trade: Maintain 1s30s swap steepener…

K shapes and disconnects (labour mkts and growth?) to continue driving the Fed … and oh, ‘bout that GOOG report and on UST supply …

…Last night Alphabet’s results delivered a solid revenue beat, with Google Cloud revenue growing 48% to $17.7bn in Q4 (vs $16.2bn expected). However, this was accompanied by a surge in the company’s CAPEX plan to $175-185bn in 2026, effectively doubling its 2025 spend and well above the average analyst estimate of $120bn. Alphabet’s shares saw some sizeable volatility in after-hours trading (falling -7% at one point) but were little changed in the end after falling by -1.96% in the regular session. This morning, S&P 500 (+0.03%) and NASDAQ 100 (+0.14%) futures have been fluctuating between gains and losses…

…Lastly in the US, we had the Treasury’s quarterly refunding announcement, which came out unchanged in line with expectations. Treasury yields were mixed in response, with the 2yr yield falling -1.6bps amid the risk-off mood but 10yr (+1.0bps to 4.28%) and 30yr (+2.3bps to 4.92%) yields continuing to rise. Indeed, that brought the 2s10s slope up to 71.6bps, its steepest since January 2022, before the Fed started its post-Covid hiking cycle. Overnight, 10yr USTs are -1.0bps lower trading at 4.26% as we go to print…

04 February 2026 DB: Growth-labor disconnect likely to drive Fed and sentiment in '26

Over the past year, the economy has been characterized by a breakdown in a typically strong economic relationship. During the pre-Covid period, changes in the hiring rate were significantly positively correlated with economic growth. However, the pandemic broke this typically strong relationship.

This breakdown drove Fed rate cuts in 2025 despite strong growth and elevated inflation and also explains soft consumer sentiment in the face of still low unemployment (see “Downbeat labor sentiment reflects less dynamism”). We, therefore, see the potential resolution of this divergence as a critical determinant of the Fed outlook and possibly the midterm election outcome.

Importing of AI — OK — inflation, though, well not so much … a note on AI, CPI and oh, yeah, ‘bout that there supply creating of its own demand …

February 4, 2026 MS: February US Treasury Refunding Reaction | US Rates Strategy

Treasury plans to hold coupons steady for several quarters; any future increases likely take into account recent demand trends and a shortening SOMA portfolio. Larger cash management buybacks and ongoing Fed RMPs are a strong mitigant to cheaper funding; stay long 2y UST spreads.

Key takeaways

Treasury announced plans to keep coupon sizes unchanged for – not only the February quarter – but also for at least the several quarters.

Treasury monitoring SOMA purchases of bills and growing demand for bills from the private sector offer flexibility on the timing of coupon increases.

Potential future coupon increases are still under evaluation, but the composition is likely to account for a SOMA portfolio that is shortening its duration.

We interpret this – and recent demand trends for Treasuries – to mean eventual coupon increases are limited to the front-end and belly.

Cash management buybacks of short coupons were boosted to $75bn for the quarter vs. $59.5bn last year, which aids in dealers’ capacity to intermediate.

February 4, 2026 MS: US Inflation Monitor: CPI Preview: Seasonal push

We expect a January acceleration to 0.36% m/m (vs. 0.24% in December, 2.6% y/y). Tariffs amplify the usual start‑of‑year price resets, and shutdown noise adds a modest upward bias. New seasonal factors pull the January SA m/m lower. Headline 0.26% m/m, 2.5% y/y, NSA Index: 325.554.

US AI-linked imports help show the scale of AI capex to date as well as the drive for investment going forward. At a fundamental level, the pace of technological change requires continued investment to keep pace for AI to reach its full potential.

Key takeaways

AI linked imports now account for ~17% of US total imports, up from ~6% two years ago, running at an approximate rate of ~$550bn annualized in 4Q25.

AI investment is otherwise hard to see in macroeconomic data because imports offset part of the investment.

We expect AI spend to contribute ~3pp to nonresidential fixed investment by 2027.

The non-linear rate of AI capabilities meant that to harness the technologies, ever greater investment into data and systems integration is required.

Tech wreck tech schmeck …

05 Feb 2026 UBS: Different sorts of central bank inaction

The technology sector of the equity market might be experiencing a dilemma. If artificial intelligence is disruptive, will it disrupt technology companies? If it is not disruptive, are technology companies overvalued? The drop in technology share prices suggests that there has not been a bubble—the adjustment is relatively focused, and there has been little borrowing behind this. This mutes the economic consequences of recent moves…

Mixed data so one can choose their own ending, then …

February 4, 2026 Wells Fargo: Service Sector Dilemma: Expansion Amid Soft Labor Market & Rising Prices

Summary The service sector is still expanding as ISM services starts 2026 in the same spot it ended 2025: a reading of precisely 53.8. The underlying details reflect some nuance in the orders component but more importantly signal a backdrop of stubborn price pressure amid a tepid labor market.

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

The Terminal dot BOMB …

February 4, 2026 at 11:50 PM UTC Bloomberg: Trillion-Dollar Tech Wipeout Ensnares All Stocks in AI’s Path

There have been many AI-driven selloffs in the three years since ChatGPT burst into the mainstream. Nothing, though, quite rivals the rout rippling through stock and credit markets this week…

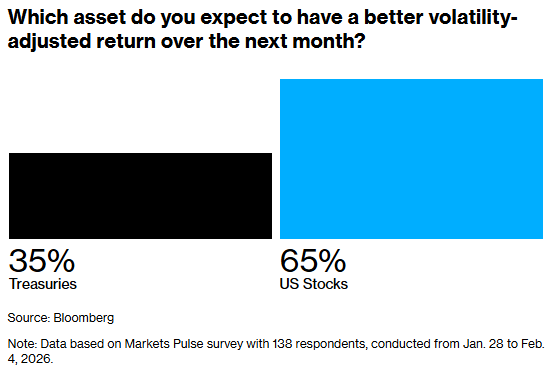

February 5, 2026 at 9:47 AM UTC Bloomberg: Stocks to Beat Bonds as Geopolitics Rock Assets: Markets Pulse

Stocks will offer better volatility-adjusted returns than bonds in a world where international policy developments drive markets, according to a majority of respondents to the latest Markets Pulse survey…

…“It’s important for investors to separate headline noise from an otherwise robust macroeconomic backdrop,” Deutsche Bank macro strategist Henry Allen wrote in a note Wednesday. “When we’ve historically seen more durable market downturns, it’s consistently coincided with a fundamentally negative reassessment in the macro outlook, which we haven’t seen today in any meaningful sense.” …

…In contrast, Treasuries have been on the back foot as investors brace for a leadership change at the Federal Reserve, with many fearing chair nominee Kevin Warsh’s preference for a smaller balance sheet will roil bond yields…

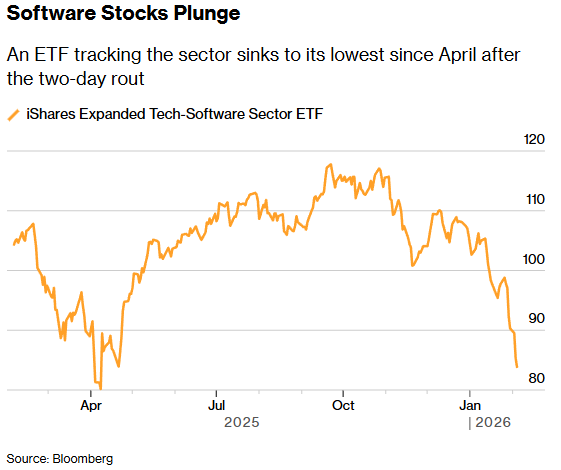

“Yields on the 10-year are still hovering near 4%, not exactly an attractive yield when risk assets have achieved returns of a multiple on that in the past three years,” said Gareth Ryan, managing director at IUR Capital. “Risk appetite remains healthy” despite the selloff in software shares, he said…

A few more thoughts on more current / weekly / ctrlALTdata …

Feb 4, 2026 WolfST:ADP Employment Report Massively Revised to 2010 with Huge Erratic Differences in Month-to-Month Job Creation & Losses

Rendering reliance on it for indications of employment trends useless.

Fantastic breakdown of the cross-asset carnage. The point about supply creating its own demand in Treasuries is kinda ironic when silver and crypto are both puking at the same time despite being 'alternative stores of value.' I actualy watched this unfold in real time yesterday and the synchronized selling felt way too mechanical tobe just fundamentals. Once volatility spikes that hard liquidity just evaporates everywhere.

Fantastic breakdown of the cross-asset carnage. The point about supply creating its own demand in Treasuries is kinda ironic when silver and crypto are both puking at the same time despite being 'alternative stores of value.' I actualy watched this unfold in real time yesterday and the synchronized selling felt way too mechanical tobe just fundamentals. Once volatility spikes that hard liquidity just evaporates everywhere.