Good morning … PPI slowed, remained tame <insert your very own narrative here> and has soothed markets a bit … term structure adjusted lower and the bid for bonds ushered in some green on the equities screens and that was nice…

… Treasuries rallied on Tuesday in a move that found support from the softer-than-expected PPI print. Yields were already drifting lower ahead of the inflation update and therefore, we’re cognizant that something else was also underlying the bid. Geopolitical tensions are very top of mind at the moment and surely have contributed to the dip-buying sentiment. In addition, while the details of PPI didn’t point toward any clear downside when refining core-PCE estimates, there was also nothing to suggest reflation should be on investors’ radar. Instead, the takeaway was that CPI will clear yet another hurdle on the Fed’s path toward lowering policy rates next month. The equity market responded well as the major indexes continue to recover recent losses with the Fed’s forward path for rates widely viewed as a net positive for stock prices – a dynamic that’s difficult to fade given the present trend higher in risk assets…

… Volumes were light on the day with cash trading at 56% of the 10-day moving average. 5s were the most active issue, taking a 30% marketshare, and 10s followed behind at 22%, with two-way flows in 5s and selling in 10s from real money accounts. 2s and 3s combined for 30%, taking 18% and 12%, respectively, with two-way flows in 2s from real and fast money. 7s garnered 7%, 20s claimed 2%, and the long bond rounded out the curve with an 8% allocation, with buying in 20s and 30s…

… LIGHT VOLUMES but a decisive move, nonetheless. All told, Bostic didn’t seem to be impressed …

RTRS: Fed's Bostic says a 'little more data' needed to support cutting rates

… if you recall (#FOMC101), Bostic IS a voter and so, his words matter.

Moving on then from yesterday for a moment and noteworthy development overnight, Kiwis welcomed into the ‘cutting club’ …

… AND from overnight TO this mornings global macro / economic landscape …

RTRS: UK inflation picks up less than expected, boosting rate cut bets

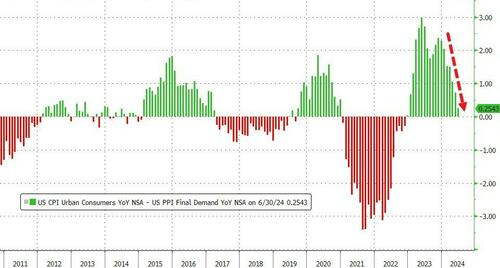

… so some further ‘wind in the sails’ of USS HOPE for a lower CPI print not unlike yesterday’s PPI which then was the proverbial rising tide which lifted ALL ships…

Ahead of today’s CPI, a quick look at USTs, this time a bit further out the curve …

30yy: momentum flipped back to bullish (albeit from levels which were far from extreme)

… AND SO, that was then and this is now … in as far as the PPI data

ZH: Producer Price Inflation Slows As Services Costs Slump

…For stocks, the read-through to profit margins is less welcome and may stymie gains, as companies are feeling the squeeze as they eat the difference between CPI and PPI...

Not exactly a good sign for the economy.

… and as far as YESTERDAY rising tide came in and went …

ZH: Dollar Dumped To 4-Mo Lows, Bitcoin & Big-Caps Pumped Ahead Of CPI Tsunami

… But, it was the dollar index that stood out today, tanking to post-payrolls plunge lows...

... dumped to its lowest in four months, breaking below its 200DMA...

… Rate-cut expectations jumped around 10bps on the day, mainly focused on the 2024 shift...

… here is a snapshot OF USTs as of 622a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures trade tentatively & DXY below 102.50 ahead of US CPI, Kiwi underperforms post-RBNZ … USTs are essentially unchanged, Gilts benefit from softer-than-expected inflation metrics, with particular focus on the Services component … USTs are unchanged ahead of US CPI. The 113-22 peak printed alongside the release of UK CPI before the benchmark then eased a touch, alongside EGBs, to the 113-19 mark where it remains.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ in response TO PPI and beyond …

BARCAP: PPI data provide slightly more impetus to core PCE in July

The July PPI data showed core price pressures (ex food, energy) receded in June. However, the subcategories that feed into core PCE were firmer on net relative to June, led by financial services, but broadly in line with our prior assumptions. We leave our core PCE forecast unchanged, at 0.20% m/m SA.

BMO: Headline PPI underwhelms and bullish steepening extends

… There isn't anything in this data that would suggest the Fed will have any hesitation cutting rates next month. That said, tomorrow's consumer inflation update is far more relevant to near-term policy expectations.

Treasuries were slightly richer ahead of the inflation update with a steepening skew. Since the headlines hit, we've seen an extension of the move -- albeit well within the recent range and therefore a non-event. From here, there is nothing on the data calendar ahead of Wednesday's CPI update…

… Turning to the details of the PPI, this undershot expectations on both the headline (+0.1% month-on-month vs +0.2% expected) and on the core measure (0.0% vs +0.2% expected). Indeed, for core PPI this was the weakest reading since December, and with June revised down from +0.4% to +0.3%. In annual terms, headline PPI rose +2.2% (vs +2.3% expected) and core by +2.4% (vs +2.6% expected). The bulk of July’s miss came down to trade services, which measures changes in ‘margins’ received by wholesale and retail. This dragged overall services PPI down -0.2%, the first monthly decline since March 2023. The PPI categories that feed into the core PCE deflator – health care services, portfolio management, airfares – saw mixed moves but leant softer in aggregate. So, an encouraging print all round.

The easing of producer price pressures added to investors’ confidence that the Fed will be increasingly comfortable cutting rates over the next few central bank meetings. In line with this, year-end Fed cut expectations rose by +7.5bps to 108bps. This came even as we heard some hawkish-leaning comments from Atlanta Fed president Bostic, who said that he’s looking for “a little more data” before supporting rate cuts. So together with Bowman over the weekend, that leaves two of the FOMC hawks still framing the Fed decision as when to cut rather than the 25bp vs 50bps choice for September priced by markets. We’ll see if the tone shifts more after today CPI data and as we move to Jackson Hole late next week.

Against this backdrop, the bond market rallied, driving the 2yr yield down -8.7bps and below four percent again to 3.93%, and the 10yr yield by -6.1bps to 3.84%. European bonds saw a similar rally, with yields on 10yr bunds (-4.0bps), OATs (-4.9bps) and BTPs (-6.5bps) all visibly lower. The decline in US rates sent the broad dollar index -0.56% lower on the day, with the euro reaching its highest level year-to-date against the greenback at 1.0993…

PPI miss supports UST rally; UK labor data exhibit mixed signals; Bunds brush off fall in German consumer sentiment; Fed's Bostic needs "a little more data" before cutting rates; weak China credit data; tone shift from BSP's Remolona; DXY at 102.65 (-0.5%); US 10y at 3.843% (-6.1bp).

… Atlanta Fed President Bostic reiterates that he expects to cut rates "by the end of the year” given that he is looking for "a little more data" as the Fed must be "absolutely sure" before lowering the policy rate; market-implied pricing currently has over 100bp of cuts priced through the end of the year…

Our Market Sentiment Indicator (MSI) has turned positive, exiting the neutral reading it has held since January 12, 2024. This regime has been associated with above-average one-week forward returns for global equities.

The publication of US consumer price inflation forces economists to become used car salespeople and real estate fantasists. Part of the disinflationary trends come from used cars (which most US households will not buy this year) and the fictional owners’ equivalent rent (which no one pays). Disinflation in these categories does not improve the spending power of most consumers.

Federal Reserve Chair Powell’s two big policy errors were to elevate the importance of consumer price data, and to stress data dependency. Market expectations about rate cuts in September will thus be influenced by today’s data. Real interest rates justify rate cuts—but a broad range of inflation measures should be used to calculate real rates. Repressive real rates is why the Fed is late, but not disastrously late in cutting rates…

Wells Fargo: Small Business Optimism On the Upswing Greater Sales Expectations Lift Outlooks in July

Summary Outlooks Brighter, but Fed Cuts Still Incoming The NFIB Small Business Optimism Index rose to 93.7 in July, its highest reading since February 2022. It’s hard to mistake this four-month string of upticks for anything other than a trend improvement in sentiment. Although the index remains below its 50-year average of 98, the outlook for business conditions shot up 18 points in July, driven by brighter sales expectations. Yet, the underlying details continue to reveal hesitancy about the demand outlook amid a cloudy economic and political landscape. The clearest takeaways from July’s survey are vital for the Fed: labor demand continues to ease and price pressures continue to fade. These soft elements of the survey measures, in concert with hard data on inflation and nonfarm payrolls, support our view that the Federal Reserve will begin cutting its policy rate next month at the September meeting.

Wells Fargo: 2024 Benchmark Payroll Revision: Your Questions Answered

Summary

Despite having slowed in recent months, the strength of nonfarm payroll growth over the past year has been a notable outlier among other indicators showing a significant cool down in the labor market. Could upcoming benchmark revisions be the key to resolving the mystery over payrolls' seeming exceptionalism this past year? In this report, we address questions about the Bureau of Labor Statistics (BLS) annual benchmark process, including what to expect for the upcoming preliminary benchmark estimate and what it could mean for the current perception of the jobs market.

Why is an annual benchmark needed and what period does it cover? Each year the BLS aligns the level of employment as reported by the Current Establishment Survey (CES) to more comprehensive data from administrative sources (such as unemployment insurance systems) to address response and sampling errors in the survey. The CES estimated count of nonfarm payrolls in March of each year is revised to correspond with the actual employment count in that month, leaving the benchmark period to cover the 12 months through March of each year.

Does it usually alter the current labor market landscape? The benchmark revision has typically not left a meaningful mark on the present view of the jobs market. It is somewhat dated upon its release; the preliminary estimate is not available until August of each year, while the final benchmark revision is not issued until February the following year (with the release of the January jobs report). Further, the benchmark revision has had a historically small effect on the level of payrolls each March. Over the past 10 years, revisions averaged an absolute change to the level of employment of 0.1%, with a maximum impact of 0.3%.

Could 2024's benchmark be more meaningful? Data through Q4–2023 from the Quarterly Census of Employment and Wages (QCEW), the key administrative data used in the annual benchmarking process, imply a negative revision ahead. Year-over-year job growth in the CES is currently reported at 2.0% in December—0.5 percentage points higher than the 1.5% annual growth in the QCEW data. If that percentage point gap persisted through March 2024, the average monthly pace of payroll growth in the CES for the year through March would be revised down from 246K to 189K—a less remarkable albeit still strong pace of job growth. Nevertheless, that would equate to the largest downward revision since March 2009.

Why has the Establishment Survey likely overstated payroll growth? The birth-death model may not yet be capturing a more difficult business climate and slowdown in business formation. Declining response rates to the CES and differing characteristics between the firms that do and do not respond may be another factor.

Could the preliminary benchmark estimate affect the FOMC's near-term rate path? We doubt the preliminary benchmark estimate will be a complete game-changer for FOMC members' current perceptions of the labor market. The months covered by the benchmark period—April 2023 to March 2024—will make even the preliminary estimate somewhat dated and will not say anything explicit about job growth in the subsequent months. In addition, FOMC members, including Chair Powell, already seem dialed-in to the potential for a downward revision. That said, a large negative revision would indicate that the strength of hiring was already fading before this past April, making risks to the full employment side of the Fed's dual mandate more salient amid widespread softening in other labor market data.

… And from Global Wall Street inbox TO the WWW,

Apollo: S&P 500 Firms Less Worried About a Recession

The media is full of anecdotes from earnings calls about the economy supposedly slowing down.

But the reality is that firms on earnings calls talk less and less about recession, see chart below.

In fact, we have never had a recession at the current low level of recession talk, see again chart below.

Bloomberg: Bond Traders Are Set for Rally to Extend as CPI Test Looms (Bolingbroke)

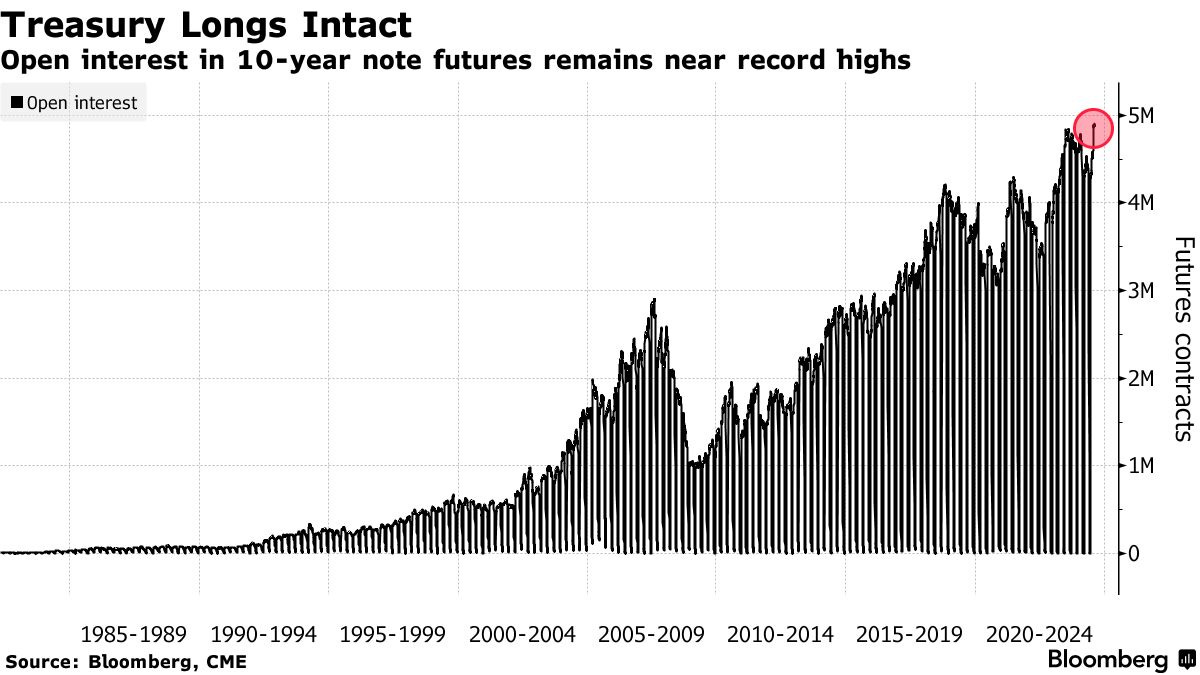

Long positions remain intact, but off recent extreme levels

JPMorgan Treasury survey shows net longs at biggest of year

… Open interest, or the amount of risk taken on by futures traders, has started to rise in some tenors over the past couple of sessions, consistent with fresh long positions after an aggressive period of liquidations across the Treasury curve. Meanwhile, in the cash market, JPMorgan Chase & Co.’s Treasury client survey released Tuesday showed net long positions among clients at their most since December.

On Tuesday, US bonds advanced across the board after US data showed producer prices rose less than forecast in July, adding to evidence that inflation is under control enough to allow the Fed to start monetary easing next month. A report due Wednesday on consumer prices is expected to provide further support…

Bloomberg: Hedge Fund Mount Lucas Sells Treasuries as Fed Bets Gone Too Far (dunno the operation but get the concept …)

US-based firm has taken profit on long position last week

Traders have started to pare bets on Federal Reserve rate cuts

Bloomberg: The Fed is setting the mood, not Trump or selloff (Authers’ OpED)

Small-business owners and global fund managers feel good at a moment when you might think they wouldn’t be.

Having priced a high chance of an inter-meeting Fed rate cut last week, interest rate expectations have moderated in the wake of better data and calming words from Fed officials. Nonetheless, uncertainty surrounding the path for Fed policy rates remains high so here we look at our base case versus market pricing and how alternative scenarios could pan out

…Scenario 1 (ING base case) Fed cuts rates 50bp in September with 25bp cuts in November and December. The Fed funds rate is then lowered to 3.5% in 2025 (50% probability)

The economy is still growing, adding jobs, and inflation is above target. But of course, the Fed doesn’t want to cause a recession by keeping policy too tight for too long, if it can avoid it. Inflation continues to look well-behaved, allowing the Fed to put more and more emphasis on its labour market target of “maximum employment”. Nonetheless, the Fed acknowledges that its June forecasts were far too optimistic (unemployment ending the year at 4%, for example). In the absence of any financial system threat, the Fed kicks off its loosening cycle with a 50bp cut as it “catches up” with where the data currently is, but then reverts back to the more typical 25bp increments. It takes policy to a “neutral” level of 3.25-3.5% with a “soft landing” achieved.

This is a mildly bearish scenario for the dollar. EUR/USD can probably trade up to 1.10 at the start of the Fed easing cycle, but further gains may be harder to come by as Europe is also engaging in a tighter fiscal/looser monetary policy mix.

WolfST: Services PPI & Core PPI YoY Were Pushed Down by Extreme Base Effect That’ll Flip Next Month for Rest of 2024

The whiplash-inducing month-to-month services PPI fell in July after hot readings in prior months. Core goods PPI is well-behaved.

AND … good luck as you plan your CPI trades and TRADE your CPI plans.