while WE slept: USTs UNCH; 'Moving 1st CUT back to SEPT' -Goldilocks; "There Are No Easy Bond Trades Is 2024's Lesson" and "Atlas shrugged as bonds steal Nvidia's thunder" -BBG

Good morning … First a quick review as yesterday began …

ZH: US Initial Jobless Claims Refuse To Budge From Near Record Lows

… making mention of IJC as they relate TO the upcoming NFP report and so, take on somewhat increased / perceived importance. Moving from IJC being ‘hot’ TO …

ZH: US New Home Sales Tumbled In April Amid Further Downward Revisions...

… AND then there were the PMIs which beat. Or did they …

ZH: S&P Global Says US Business Activity Is At Its Strongest In Two Years, But...

With both 'hard' and 'soft' data declining rapidly recently, why should we be surprised that S&P Global's preliminary PMI prints for May would suddenly surge, with manufacturing back into expansion?

Flash US Services Business Activity Index at 54.8 (April: 51.3). 12-month high.

Flash US Manufacturing PMI at 50.9 (April: 50.0). 2-month high.

Just ignore the plunge in hard data in May...

And just to rub salt into the wounds... S&P Global claims that US business activity accelerated in early May at the fastest pace in two years, largely reflecting stronger growth at service providers and accompanied by a pickup in inflation…

…BUT...Selling price inflation has meanwhile ticked higher and continues to signal modestly above-target inflation.

“What’s interesting is that the main inflationary impetus is now coming from manufacturing rather than services, meaning rates of inflation for costs and selling prices are now somewhat elevated by pre-pandemic standards in both sectors to suggest that the final mile down to the Fed’s 2% target still seems elusive,” Chris Williamson, chief business economist at S&P Global Market Intelligence, said in a statement.

Factory input prices advanced at the fastest rate since November 2022, the report showed…

… So while growth macro data is surprising to the downside, this survey says growth is killing it and Bidenomics rules!

Let's see if this "good news" on growth prompts gains (or losses) in stocks.

… Team Rate Cut NOT having a good day, at least not in the early goings OR … had best. day. ever…depending on HOW you read tea leaves…

Truth be known … ALL markets were unsupportive by days end as …

The cheer from Wall Street darling Nvidia's strong results didn't last long as fears that interest rates would stay higher for longer once again dampened the AI rally…

… I guess the rate inspired equity rally then, had been postponed until … this morning? I’d suggest not and whatever it was we witnessed yesterday more than likely the first of the summertime’s Hamptons Hedge.

Folks unwound positions and got risk OFF the books so they could head out east TO LIs Hamptons for the holiday long weekend making whatever price action today somewhat less interesting.

Bonds close at 2pm and Global Wall’s trading desks will be ‘thinly staffed’ (if they’ve not yet figured out how to have AI field all trades and phone calls?) and so … a quick look at 10yy from a weekly (and more bullish) point of view…

… gotta be honest with you … doesn’t look as bullish as I might have thought it would. Momentum is ‘middling’ and while the UPTREND has broken, there’s just nothing here that screams BUY BUY BUY (or sell, either, if we’re being intellectually honest) and best I reckon, there’s been no clear signals the ‘flation has been eliminated and jobs about to disappear.

Furthermore, when you listen to / read all the Fedspeak in the week just passed, well, Wall-E I thought was pretty clear when he said,

… While the April inflation data represents progress, the amount of progress was small, reflected in the fact that I needed to report the monthly numbers to two decimal places to show progress. The economy now seems to be evolving closer to what the Committee expected. Nevertheless, in the absence of a significant weakening in the labor market, I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy

… here is a snapshot OF USTs as of 705a:

… the very definition of aggressively UNCH and …in lieu of the normal morning writeup which has yet to hit MY inbox, I’ll defer TO Newsquawk who notes

NEWSQUAWK: US equity futures modestly firmer, Dollar softer in quiet trade and Bonds gain modestly … Bonds are very modestly firmer, attempting to claw back some of the US PMI-induced pressure … USTs are marginally firmer with prices unable to launch much in the way of a meaningful recovery after yesterday's PMI-induced losses and awaiting impetus from US Durable Goods. Today's range is well contained within yesterday's 108.17+ to 109.06 parameters …

… and for some MORE of the news you might be able to use…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: FOMC Minutes NLP Analysis: A bit less conviction on monetary policy

Participants' degree of conviction about the course of monetary policy and the economic outlook was a bit lower in the April-May meeting than in prior meetings. Although views converged on the labor market and inflation, our analysis points to continued dispersion on the interpretation of recent inflation prints.

Faced with elevated uncertainty and activity accelerating faster than anticipated, we now think the GC will move more gradually this year. We continue to expect 25bp of cuts at each forecast meeting (Jun-Sep-Dec), but no longer expect a cut at July's nonforecast meeting. We continue to expect 150bp of cuts in the cycle.

KEY MESSAGES Three signposts will guide whether we enter structural USD shorts over the next few months: a deterioration in the US labour market; upside surprises in eurozone data; and a substantial Biden lead in US opinion polls.

For now, however, we think it is premature to position for a broad decline in the USD, and conclude trading the range more on the long USD side remains appropriate.

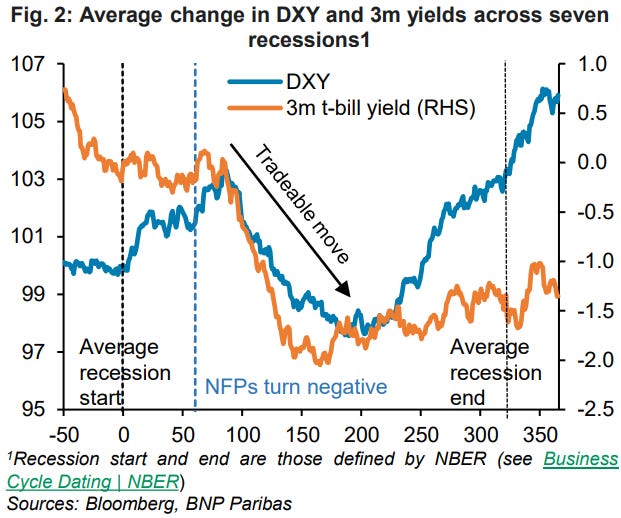

… We find the USD tends to follow a distinct pattern in downturns: up, down, up (Figure 2). The USD rallies in the first three months of a recession, on average, before more than fully unwinding its initial gains once the market prices a more imminent Fed rate cutting cycle.

The tradable move is selling the USD when the Fed gets priced to cut more imminently. We find the key signal in this respect is if nonfarm payrolls growth inverts from positive to negative, because that typically coincides with the market pricing deeper Fed cuts (Figure 2), thereby driving the USD lower.

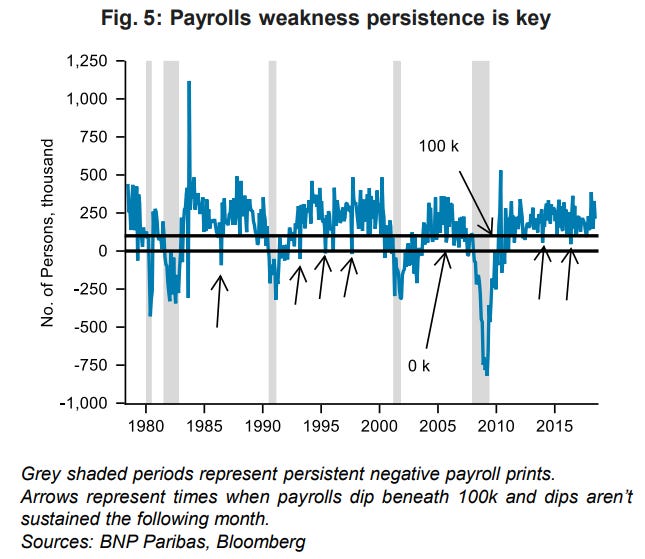

… Payrolls growth remains below 100k for severalmonths: A persistent weakening in payrolls growth to below 100k over the next few months from April’s 175k would, we think, be consistent with GDP growth falling short of potential.

We emphasise that persistence is key here. Of the 34 instances when payrolls dipped beneath 100k, 62% of the time the subsequent payrolls release bounced back above 100k.

…. US manufacturing PMI beat, up 0.9pts to 50.9 in the prelim read for May, consensus looked for a 0.1pt decline. Services much better, up 3.5pts to 54.8, highest since May last year, consensus also looked for a 0.1pt decline. Composite at 54.4pts, highest since April 2022.

… Euro manufacturing PMI beat. Manufacturing up 1.7pts to 47.4 in the prelim read for May, consensus looked for a 0.4pt gain. Services steady at 53.3, weaker than consensus at 53.6. Still, that left the composite up 0.6pts at 52.3, consensus at 52. Francis Yared thinks the improvement is consistent with leading indicators and lends some credibility to the rebound in Eurozone activity.

Goldilocks: Moving the First Fed Cut Back to September (breaking news, this just in … attn all us muppets…and please note the hedged / uncommitted view recognizing how diff this call and timing IS … in other words, it’s at best a coin flip and they know it … )

We are moving our forecast of the Fed’s first rate cut back one meeting, from July to September. Earlier this week, we noted that comments from Fed officials suggested that a July cut would likely require not just better inflation numbers but also meaningful signs of softness in the activity or labor market data. After the stronger May PMIs and lower jobless claims, this does not look like the most likely outcome.

n Four additional CPI reports will be available by the September meeting, and if monthly core CPI inflation averages in the high 20s and core PCE in the low 20s, as we expect, then we think most FOMC participants will support a rate cut. We interpret Chair Powell’s recent comments as pointing toward a middle-of-the-road path of cutting gradually in recognition of both the considerable cumulative progress made in solving the inflation problem and the realities that inflation is likely to remain noticeably above target this year and the economy is performing well at the current level of interest rates.

The timing of the first cut remains a difficult question for a few reasons. First, we continue to see rate cuts as optional, which lessens the urgency. Second, inflation is likely to be much improved by September but hardly perfect and still at a year-on-year rate that makes cutting a less than obvious decision. Third, while the Fed leadership appears to share our relaxed view on the inflation outlook and will likely be ready to cut before too long, a number of FOMC participants still appear to be more concerned about inflation and more reluctant to cut.

Goldilocks: Initial Claims Fall Back to Previous Trend

BOTTOM LINE: Initial jobless claims declined to 215k, slightly lower than expected and roughly in line with the average weekly level of claims so far this year.

Goldilocks: S&P Global PMIs Above Expectations in May

BOTTOM LINE: The S&P Global manufacturing and services PMIs increased in May, against consensus expectations for modest declines. The underlying composition of the services PMI was strong, with increases in the new business and employment components. The underlying composition of the manufacturing PMI was strong, as the output, new orders, and employment components all increased.

Goldilocks: Global PMI Monitor: Services Strength in the US and Germany; Weakness in France

Goldilocks US Consumer Dashboard: May 2024: Outlook Still Positive Despite Recent Signs of Slowing (so still positive OR SLOWING … or STILL POSITIVE but slowing … how you see it is what matters … fact of the matter here IS Goldilocks has bases covered)

The latest data shows that a full-blown global easing cycle is still a long shot. The pricing for European Central Bank cuts in 2024 is down to 60bp, which means two cuts are now deemed more likely than three. And the pricing could go even lower in our view. For the US, the case for higher yields based on the latest figures is even stronger

… US Michigan consumer confidence data is just noise, but it is always entertaining to check in on the political polarization represented by the gulf between Democrat and Republican views. Michigan inflation expectations do not necessarily reflect how consumers actually perceive inflation, given the overlay of partisan bias. US durable goods orders data is also due…

Plentiful Supply and Softer Price Pressures Remain an Advantage Summary Higher Rates Headwind for New Home Sales in April

New home sales dropped 4.7% during April. Although a pullback was expected, the drop was a bit sharper than anticipated. The weakness in new home sales can largely be explained by early April's spurt higher in mortgage rates. Rising inventory levels in the resale market appears to be another factor weighing on sales.

Looking ahead, builders still enjoy several advantages that are likely to support sales this year. Although slightly improved, existing home inventories remain low, which should continue to push buyers into the new home market where inventories remain plentiful. Builders also appear willing to reduce prices and offer incentives to stabilize demand. Builders surveyed by NAHB stepped up their use of price cuts and mortgage rate buydowns in May, which could potentially help to bring buyers back from the sidelines.

Wells Fargo: Comparing America's National Debt to Its Peers (both Team Rate Cut AND the other guys are watching … seems to ME that no matter WHO wins in Nov, easier / looser / supportive FISCAL policy coming — in form of larger govt and MOAR spending OR … tax CUTS … making the problem … worse?)

Summary

The fiscal challenges facing the United States government are top of mind for decision makers. The federal government's debt-to-GDP ratio is near its highest level since World War II, and the federal budget deficit is much larger than the long-run average over the past half century, raising questions about the sustainability of the U.S. public debt on its current trajectory.

Yet, many of the drivers of America's fiscal imbalance are not unique. Other countries face similar or even bigger public finance headaches. In this report, we compare the U.S. fiscal position to some of its largest advanced economy peers.

There is no one single metric that fully encapsulates a country's public finances, and differences in accounting and methodology can make a perfect apples-to-apples comparison elusive. That said, by looking at a variety of measures largely put together by the International Monetary Fund, we can get a feel for the general government fiscal positions across the Group of Seven (G7) nations.

The United States has a general government debt-to-GDP ratio that is near the middle of the pack across the G7. The public debt burden is larger in places like Japan and Italy but smaller elsewhere, such as Germany and Canada. This is true when looking at both “gross” and “net” public debt. In short, the United States is not much of an outlier when looking narrowly at accumulated public debt.

In addition, the current U.S. debt burden is not unprecedented. The U.S. government's debt-to-GDP ratio was similar during and shortly after World War II.

However, other fiscal indicators look less favorable for the United States. The U.S. appears likely to run the largest structural budget deficit in the G7 at 6.7% of GDP in 2024. The U.S. government has the shortest weighted-average maturity of its public debt across the G7, and its net interest spending is also on the high side. In addition, the Federal Reserve holds a smaller share of the U.S. debt relative to central banks in other G7 nations.

The good news is that the United States government has some unique advantages relative to its peers. The U.S. dollar is the world's reserve currency and is backed by the world's largest and most diversified economy. The market for U.S. Treasury securities is the deepest and most liquid bond market in the world with a long history of strong creditworthiness.

That said, the U.S. fiscal outlook is concerning given debt levels that are high by historical standards and a budget deficit that is large relative to both its peers and history.Furthermore, net interest costs have climbed substantially amid the rise in interest rates from the low levels that prevailed in the 2010s. In our view, the problem is not so much the previous debt accumulation in the United States, which is large but manageable, but rather the outlook for sizable budget deficits as far as the eye can see.

An aging population, elevated interest rates and heightened national security concerns amid mounting geopolitical tensions will make fiscal consolidation a difficult task. That said, the optimal time for fiscal consolidation is during a period of wide budget deficits, low unemployment and elevated inflation. Deficit reduction via higher revenues, lower spending or some combination of the two would help set U.S. fiscal policy on a more sustainable path.

… General government interest payments as a share of tax revenues are on the rise in the United States, and the IMF projects that U.S. interest costs by this measure will be closer to what is typical in emerging market economies over the next few years (Figure 10). In short, debt servicing costs are increasingly becoming a new source of budgetary pressure in the G7, and this is especially true in the United States.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: What’s happening in Sonoma? (wine and long bonds … what could possibly be better? other than the term RIPPER and who talks of a 50wk anything? whatever … stock jockeys talking about bonds this is what yer gonna get … )

… Meanwhile, look at the ripper in yields.

After a 40 year drawdown, the 50-week rate of change for US 30yr yields is like nothing we’ve ever seen before!

Demographic trends will weigh on inflation over the coming decades, but the secular stagnation forces pulling inflation down are currently being offset by upward pressures on inflation coming from deglobalization, energy transition, defense spending, restrictions on immigration, easy financial conditions, and easy fiscal policy.

Put differently, the structural forces pushing inflation down are currently being offset by cyclical forces putting upward pressure on inflation.

That’s the reason why interest rates will not only be higher for longer in the short term but also in the longer term, see also the second chart, which shows that the market is currently pricing that the Fed funds rate will be between 4% and 5% over the coming years.

Bloomberg: Atlas shrugged as bonds steal Nvidia's thunder (Authers’ OpED)

So much for the AI chipmaker lifting risk assets. The Fed still has the upper hand.

So much for that. Nvidia rose 9.3% Thursday; the S&P 500 fell 0.74%. An “S&P 500 excluding Nvidia” index would have dropped 1.2%. Traders’ tendency to treat the company as the steering wheel for the entire market suddenly halted. “Quite frankly, if you told me that Nvidia would be up over 10% by midday while the S&P 500 is up only slightly, I would have thought that impossible,” said Steve Sosnick, chief strategist of Interactive Brokers, earlier in the day. “Like the mythical Titan, Nvidia is the Atlas holding up the broader market.”

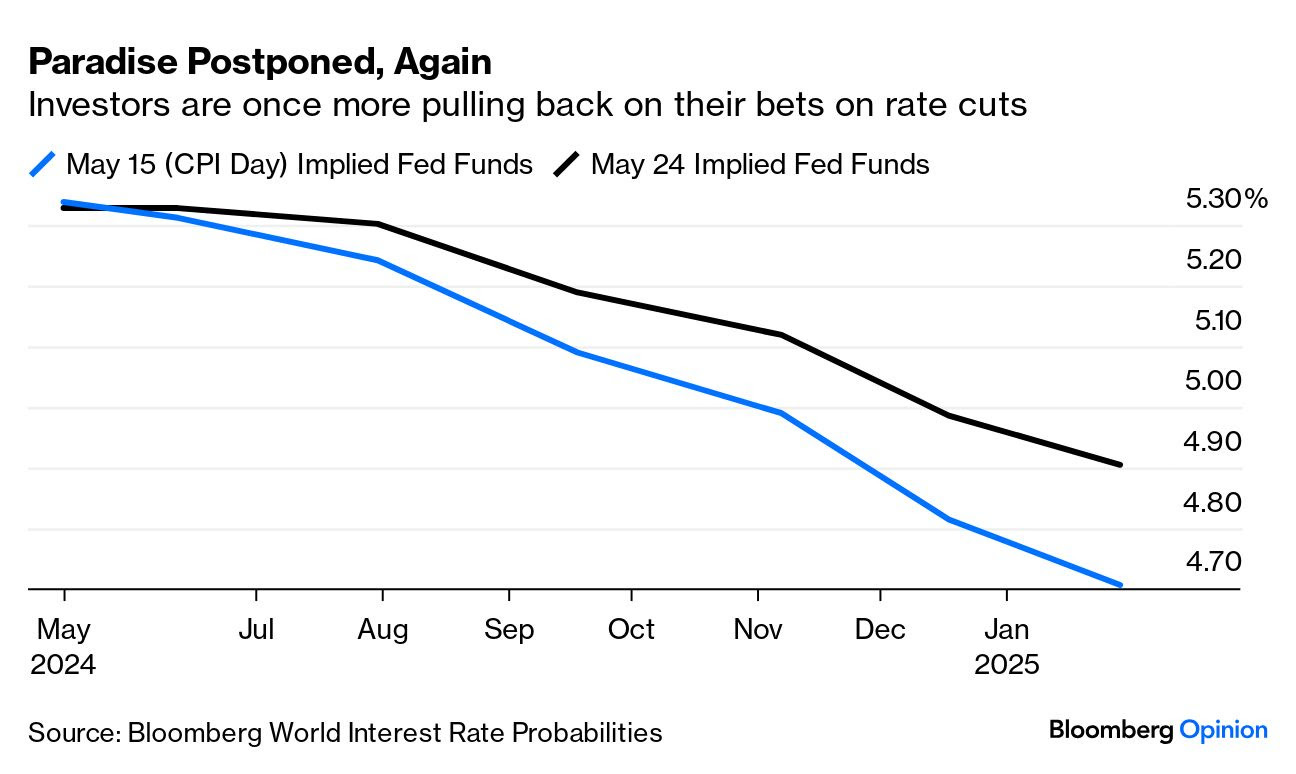

What was the problem? Ultimately, it was the bond market. After a big dip earlier this month, the two-year Treasury yield is almost back to 5%. The confidence to buy bonds that was engendered by a Federal Open Market Committee meeting that was regarded as dovish, and then the April consumer price index that was no worse than expected, seems to have quickly retreated:

Driving this is a change in expectations for the Fed. The Bloomberg World Interest Rate Probabilities model, based on fed funds futures, shows how the projected course of rates has moved since May 15, when the CPI data was released to a warm reception:

Bonds took their cue from macro data releases. While good news for Nvidia is treated as good news for everyone, the same doesn’t apply to great bulletins about the macroeconomy. Thursday brought news that S&P Global’s version of the purchasing manager index for US combined manufacturing and services had risen to its highest level in two years. While still only at 54.4, where 50 marks the boundary between recession and expansion, this was still taken as disquieting evidence that the Fed’s monetary tightening hadn’t had much effect on the economy. There was also a gloomy reception for initial jobless claims, which were lower than expected — although the four-week moving average of new claims is now at its highest since September, so these numbers are perfectly consistent with an economy steadily slowing down.

Investors took a negative view thanks to the last FOMC minutes, published Wednesday afternoon. The main points were that “many” Fed officials had expressed uncertainty over the degree to which policy is restraining the economy (some disagree that the current monetary settings are restrictive), while policymakers agreed this year’s disappointing inflation data meant it “would take longer than previously anticipated for them to gain greater confidence” that it was heading for the 2% target…

… The minutes also chimed with a noticeable move toward more aggressive language by the Fed’s regional presidents. They are usually more hawkish than the central bank’s governors, who are based in Washington, but analysis by Oxford Economics shows the gap is widening:

That could mean resistance if Powell wants to cut rates later this year.

Later Rather Than Sooner This newsletter has opined before on the difficulty of timing the Treasury curve steepener, which Goldman Sachs Asset Management called the “easiest trade out there in rates” in its year-ahead outlook. Nearly halfway into 2024, it’s still not working.

The spread between 2- and 10-year yields sunk to -46 basis points on Tuesday, hovering near the most inverted levels of the year. While traders expected the curve to normalize this year as the Federal Reserve’s rate cutting cycle drew closer, that expectation has been repeatedly pushed out, extinguishing any meaningful steepening impulse.

“The problem with the steepener in this cycle is that the market already prices — and has priced for a while — a full cutting cycle over 2 to 3 years,” Bank of America strategists including Mark Cabana wrote in a note this week.

While it’s not their base case, betting on the 2-, 10-year curve to invert further works as a positive carry, out-of-consensus position given the risk that rates stay on hold for even longer than expected, they wrote.

With two-year yields all but anchored in place by current rate cut pricing, that leaves a lot of heavy lifting for the long-end to bring the curve back into positive territory. It’s unlikely that would be the dynamic — a so-called bearish steepener —that un-inverts the curve, according to Ian Lyngen of BMO Capital Markets.

“The real steepener will be a bull steepener,” said Lyngen, BMO’s head of US rates strategy. “The only bear steepener will be if inflation doesn’t cool and the Fed is forced to cut soon because of a massive spike in the unemployment rate, but even that wouldn’t necessarily translate into sustainably higher 10- and 30-year yields.”

Bloomberg(via ZH): Red Or Blue, Rich Or Poor — Recessions Don't Care (sending not for political angle but rather the PMI and stonks visual … Team Rate Cut to weigh in shortly …?)

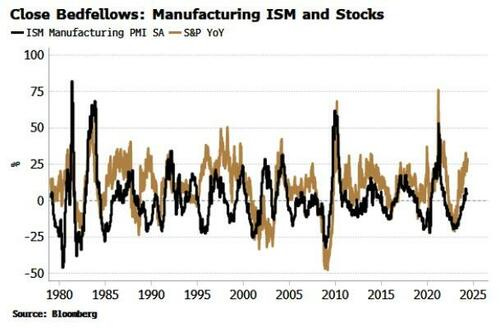

… This is critical. Recessions metastasize when we get a negative feedback loop developing between hard and soft data. Hard data deteriorates, and this feeds into soft and market data. That in turn hits the wealth effect, which affects investment and spending and feeds back into worsening hard data. Unchecked, a recession typically develops.

The ISM’s role is as a key artery from survey data to the market, and thence ultimately into hard data. The other surveys simply don’t have the same influence, with all of them displaying a much weaker relationship with the S&P.

There is some reflexivity in that ISM-survey respondents’ level of optimism will be affected by the level of the market. But the market also responds to the ISM, as one of the first data points out each month.

Despite Cameron’s view that the ISM does not matter as much as it used to, it in fact remains one of the most important data points (I’ll write more on this very soon).

But we also needn’t overstate its importance. There is no single “killer” recession predictor. The ISM’s utility comes from it having a long history, being minimally revised, having an early release time and its role in facilitating recession-causing negative feedback loops. But other data matter too…

… It’s hard to pinpoint any systematic wealth bias in the data, and likewise it’s hard to find political bias in data that matters for recession prediction, or if so any that we can’t smooth out by exploiting state heterogeneity.

So while it’s recommended to “know your data,” when it comes to what matters - avoiding steep market drawdowns ahead of downturns - investors need not get distracted by second-guessing who votes for whom, and how well-off they might be.

Bloomberg(via ZH): If CEOs Are Right, Things Can Only Get Better For US Earnings' But...

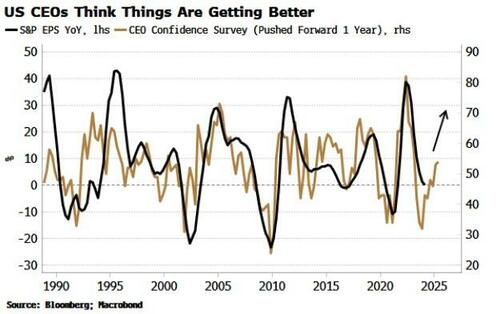

… You may have heard there’s going to be a UK election soon. When Rishi Sunak made the announcement outside Downing Street, D Ream’s 1990s’ pop-synth hit Things Can Only Get Better echoed in the background. Based on survey data, US CEOs might be bopping along to the same tune. CEO confidence has been rising, which often means earnings soon follow suit.

EPS growth for the S&P 500 has been flat, and if CEO confidence isn’t misplaced, it should soon start to rise. That’s even more the case, as when CEOs are upbeat stock buybacks tend to rise too, reducing the share count and providing another EPS tailwind…

LPL: Sure, Cash Is Cool Again, but Bonds Are Better

… Bonds Tend to Outperform Cash Over Time

Trailing 5-year Annualized Total Returns

Investing is largely about setting up portfolios for future success. We definitely consider cash as a valid asset class now, especially for investors with short-term goals spanning a few quarters to a couple of years. However, unless investors have short-term income needs, they may be better served by reducing some of their excess cash holdings and extending the maturity profile of their fixed income portfolio to lock in these higher yields for years to come. Bond funds and ETFs that track the Bloomberg Aggregate Index, along with separately managed accounts and laddered portfolios, all represent attractive options that will allow investors to take advantage of these higher rates before they disappear.

WolfST: Remember Headlines 2 Weeks Ago, Labor Market “Suddenly” Weakens as Unemployment Claims “Spike”: It just Got Unwound

AND ahead of an early bond market close and holiday long weekend, a reminder …

AND… THAT is all for now. NOT SURE what weekend will bring but hope to have some thoughts out before Sunday Monday evenings' (CASH)UST market open.