Good morning … rough start here after a day outta pocket watching markets from afar, woke up to a 2am power outtage and loss of intertrubes and so I hope to have a somewhat more coherent post tomorrow / over weekend for now …

Bloomberg: US Inflation Data Was Accidentally Released 30 Minutes Early

Agency says it has reported incident to independent watchdog

Full investigation underway, Bureau of Labor Statistics says

… “In advance of today’s CPI and Real Earnings releases, BLS inadvertently loaded a subset of files to the website approximately 30 minutes prior to the release,” BLS said in a statement posted on its website Wednesday evening.

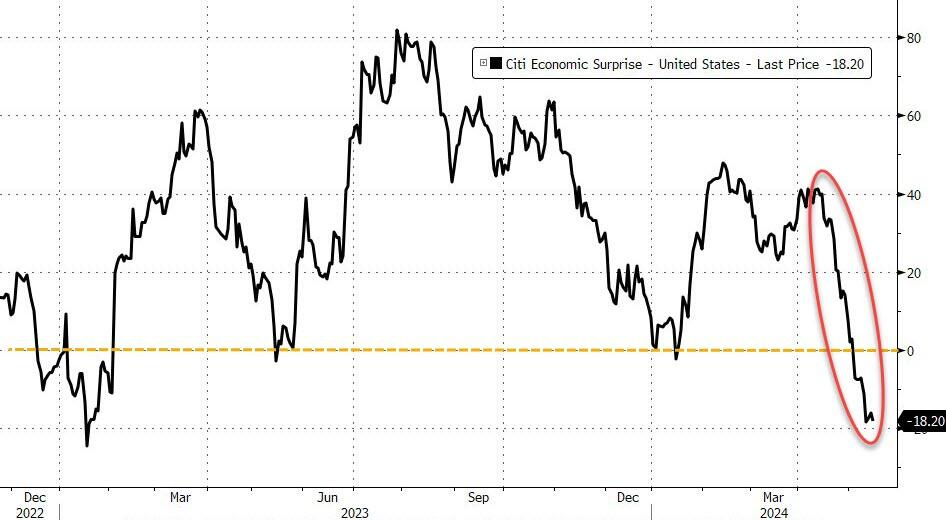

… this report does not meaningfully move the ball towards ‘price stability’ and leaves the Fed – if they’re being honest – still in a bind between slowing growth and sticky inflation…

ZH: "Trifecta Of Dovish News... Consistent With Fed Cutting In September": Wall Street Reacts To Weaker CPI Print

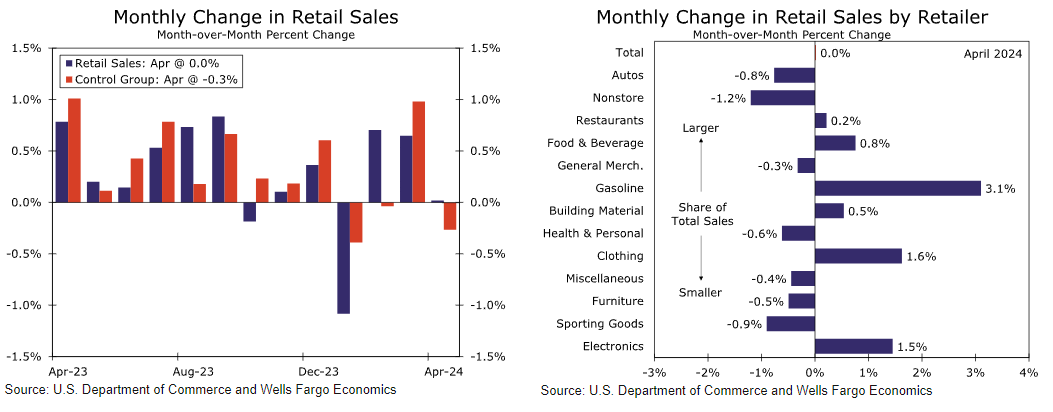

ZH: Despite Surging Gasoline Spending, US Retail Sales Missed Big In April

ZH: Stocks, Bonds, Gold, & Crypto Soar As Rate-Cut Hopes Rise On Small CPI Miss

ZH: Consumer Prices Have Risen Every Month Since 'Bidenomics' Began, Up 19.5% To Record High

AND … when all was said and done, the data dust settled …

ZH: Soft CPI & Sloppy Sales Spark Run To Record Highs For Stocks; Bonds, Bullion, & Bitcoin All Bid

Nothing good - all bad... and new record highs for stocks.

SuperCore CPI hotter than expected (but headline and core CPI in-line/small miss), Retail sales way uglier than expected (but gas station spending surged), homebuilder sentiment slumped, and Empire Fed Manufacturing ugly...

… here is a snapshot OF USTs as of 732a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are twisting flatter in the middle of the overnight range, volumes running ~115% the 30d average. Antipodean and Japan FI saw decent follow-through performance overnight, with weaker AUS labor conditions and weaker Japan GDP adding to the moves. In USTs, flows indicated modest profit-taking in the belly, with 5s slightly vs the wings (block flow was seen in tu/fv/uxy, which our desk believes was a sale of the belly). Fast$ flatteners in 2s10s were noted as well, with some outright selling from banks in the 10y bucket. APAC equities saw solid performance overnight (NKY +1.4%, KOSPI +0.8%, SHCOMP +0.1%), but FX-majors and commods are close to UNCH’d here at 7am. S&P futures are +2.5pts , with the DAX and Eurostoxx -0.2%.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures modestly firmer, Dollar attempts to recoup recent losses & AUD lags post jobs data; US IJC due … Bonds are steady, though with a very mild negative bias … USTs are steady thus far with benchmarks slightly shy of this morning's peak but still in the green. A relative pullback which is being led by the short-end with the 2yr basically unchanged and lagging a touch, with an unusually sizeable for the time block trade perhaps impacting; USTs in slim 109-24 to 109-31+ bounds.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: April CPI and PCE inflation to provide some comfort to the FOMC

Core CPI for April surprised to the downside, rising 0.29% m/m (3.6% y/y), helped by another month of deflation in core goods and easing in core services costs. After incorporating the CPI and PPI data, we estimate that core PCE decelerated to 0.24% m/m (2.8% y/y), about 8bp lower relative to the realized March estimate…

… All told, we think the April inflation data, coupled with the weaker-than-expect retail sales data, should make the FOMC more comfortable holding rates unchanged until it gains greater confidence that inflation is on a sustainable path to 2%. Yesterday, Chair Powell noted the lack of progress on inflation in Q1 24, and said that while he expected inflation to decline on a m/m basis in the coming months, his confidence about it was not as high as it was earlier in the year. He indicated that the implication for policy was that the FOMC would likely need to be patient, as it will take longer for it to become confident that inflation is moving sustainably to 2%. This morning's dataflow somewhat bolsters our conviction in our call that the FOMC will deliver one 25bp rate cut this year, in September. However, we continue to view a first cut in December as being nearly as likely.

Retail sales were flat in April, with the control group retreating somewhat from a robust March reading on a downswing in the nonstore component. Although this positions consumer spending for a softer gain in the current quarter, as expected, fundamentals suggest that the resilient underlying trend remains intact.

Core CPI printed in line with expectations for the first time in four months in April, with the details supportive of a continuation of softer inflation readings than Q1.

Specifically, we think shelter inflation has downshifted to a lower monthly run-rate, which should help moderate core CPI inflation through the balance of the year.

We are not quite out of the woods yet for April core PCE, however, with a stronger-than-expected PPI print putting our unrounded forecast at 0.24% m/m.

The Fed will likely welcome this modest progress but remain cautious on the inflation front, requiring multiple more months of improvement before seriously considering a rate cut.

Preliminary May CPI forecast: 0.3% m/m headline, 0.3% core.

While the April headline CPI (0.31% vs. +0.38% in March) was a little softer than expected, core (+0.29% vs. +0.36%) was exactly in line with our forecast (even down to the third decimal place). Taken together, the year-over-year rate for headline ticked down a tenth to 3.4%, while that for core fell by two tenths to 3.6%. Shorter-term trends were mixed, with the three-month annualized rate falling by four tenths to 4.1%, while the six-month rate increased a tenth to 4.0%.

At the component level, the breakdown was also largely as we expected: decreases in core goods prices paired with still-elevated services inflation. Core goods fell 10bps, a function of continued declines in durable goods prices partially offset by gains in apparel and medical commodities. Core services ticked down a tenth to 0.4% showing tentative signs of disinflation after Q1's surge. Importantly, rent slowed slightly faster than we expected and showed signs of returning to disinflation.

The PPI data were relatively neutral, so taken together with the CPI data, we think that April core PCE should increase +0.26% m/m, which would have the year-over-year rate tick down 5bps to 2.77%.

Given the relatively few surprises in the April data, our inflation forecast is largely unchanged. Our initial read on the May core CPI data is that it should come in at +0.27% m/m, with the year-over-year rate falling by a tenth to 3.5%. We continue to expect core CPI to end the year at 3.5% (Q4/Q4) before falling to 2.5% in 2025 and 2.4% in 2026 (all unch.). Our core PCE forecasts are similarly unchanged: 2.7%, 2.2%, and 2.0% for 2024-2026 respectively. The analogous numbers for headline CPI are 3.0%, 2.5%, and 2.3% for 2024-2026 and 2.3%, 2.2%, and 1.9% for headline PCE, respectively.

While the April inflation data continue to run well above the Fed's inflation target, this morning's print was a step in the right direction relative to hot Q1 prints. Further progress over the coming months will be needed to give the Fed enough confidence to cut on declining inflation alone. We still expect such conditions to be in place by the December meeting (see “(Pushed) Back to December”). An earlier cut is possible, but it likely requires a string of more favorable inflation prints and some softening in labor market data.

Goldilocks: Core CPI Inflation Slows Two-Tenths to 3.6%; Core PCE Tracking Still at 25bp; Retail Sales, Empire Manufacturing Below Expectations

BOTTOM LINE: April core CPI rose 0.29% month-over-month, 1bp below consensus and the slowest pace since December. The year-on-year rate fell 0.2pp to 3.6%. The composition of the report was encouraging, with a 31-month low for the primary rent gauge, declines in both new and used car prices, and much of the strength still coming from lagged catch-up in OER and car insurance. After incorporating the details of the CPI report, we have left our April core PCE inflation estimate unchanged at +0.25% month-over-month, corresponding to a year-over-year rate of +2.77%. We continue to expect the Fed to cut the funds rate by 25bps in July and proceed with cuts at a quarterly pace thereafter. Core retail sales declined by 0.3% in April, against consensus expectations for an increase. Headline spending remained unchanged. The Empire manufacturing index declined in May, against consensus expectations for an increase. The composition of the report was mixed, with declines in the new orders and employment components and an increase in the shipments component. The April retail sales report was even weaker than our below-consensus expectations, and we lowered our Q2 GDP tracking estimate by 0.4pp to +3.0% (qoq ar) and our domestic final sales estimate by 0.3pp to +2.4%. We lowered our past-quarter GDP tracking estimate for Q1 by 0.2pp to +1.3% (vs. +1.6% originally reported).

Incorporating inputs from CPI, we now forecast core PCE inflation increased 0.247%M in April vs. 0.32%M in March. This would lower the y/y from 2.82% to 2.76%. Headline PCE is preliminarily forecast at 0.25%M vs. 0.32%M the month prior. Core services ex housing translation points to 0.26%M in April vs. 0.39% prior. This CPI print comes after yesterday's PPI print that added inputs to forecast healthcare, financial services, and airfares.

This weaker print compared to 1Q24 is the first month this year adding to the convincing evidence the Fed needs to start cutting in soon. We still expect more deceleration ahead, especially in 2H24, and we maintain our call for a first cut in September this year.

The consumer price index (CPI) for April came in aligned with expectations. Core CPI increased 0.29%M vs 0.359% prior (MSe 0.29%M, consensus 0.3%M, annual rate 3.61%Y). Core goods prices were down this month (-0.11%M) driven by lower used and new vehicles prices. Core services ex housing stepped down from 0.65%M to 0.42%M, with payback in car insurance inflation and weaker rents. Rent and OER showed more progress, deceleration from 0.43%M to 0.41%M. On a 3-month annualized rate, core CPI decreased from 4.5% to 4.1%.

Headline was below expectations due to lower than expected food inflation, coming in at 0.31%M (MSe 0.38%M, consensus 0.4%M) vs. 0.38%M prior.

RBC: April saw a small relief in surging U.S. inflation

… Bottom line: The on-consensus CPI turnouts in the U.S. in April is a small relief but far from a cause of celebration. Price pressures moderated slightly but for the most part remained heightened, as readings for core measures stayed high. The diffusion index that measures the breadth of price pressures has changed little since last summer. That still leaves plenty of more room for further improvement relative to the scope that was seen in pre-pandemic 2019. In previous communications, Fed Chair Powell was assertive that interest rates are already restrictive enough, and more time is needed for it to work to further slow inflation. With that, we expect the Fed will stay on the sideline for most part of the year before opting for a first rate cut later in December. That's of course contingent on CPI readings continuing to move lower in the interim.

Yesterday’s US consumer price data was less weird—no 4% monthly increases in rent in Detroit (as in March). The detail showed for almost every business sector, there is deflation somewhere in the United States. For the benefit of non-economists (like the Chair of the Federal Reserve) this is not remotely consistent with sticky prices.

The US retail sales data highlighted some of the structural shifts of the US economy. The bias to spending on things that are fun is more or less in evidence, and deflation in durable goods prices is weighing on the value of sales in that sector. The ongoing rise of online retail is evident—with wider implications for productivity, real estate use, and transport…

Summary The first CPI report of Q2 should be seen as welcome news by the FOMC. The headline CPI rose 0.3% in April, a tenth below consensus expectations, while the core CPI also increased 0.3%, in line with expectations but a downshift from the pace registered in Q1. Flat food prices and a decline in energy services prices helped to partially offset a jump in gasoline prices in the headline index. Excluding food and energy, more deflation for vehicles prices and a moderation in price growth for medical care services, motor vehicle insurance and motor vehicle maintenance contributed to the slowdown in core CPI.

Based on the April CPI and PPI data, we estimate the core PCE deflator increased 0.25% month-over-month in April. If realized, this would bring the three-month annualized and year-over-year rates to 3.4% and 2.8%, respectively. On balance, the April inflation data should help restore some confidence at the Fed that price growth is continuing to moderate through the month-to-month noise. That said, we think it will take more than just one solid CPI report to induce the first rate cut. We believe it will take at least a few more benign inflation readings for the FOMC to feel sufficiently confident to begin lowering the fed funds rate. We continue to look for the first rate cut from the FOMC to come at its September meeting, but any additional bumps in the road would likely push that timing back, absent a marked deterioration in the labor market.

Wells Fargo: What the Stall in April Retail Sales Says About the Consumer

Summary There are plenty of reasons to be skeptical about the sustainability of consumer spending, but today's soft print for retail sales says more about one-off factors than it does a meaningful downshift in spending activity.

… Higher Rates Finally Slowing Consumer Spending? One theme of this Fed tightening cycle, now entering its third year, is how consumers have been undaunted by higher borrowing costs. Yet, the fact that retail sales stalled in April is not necessarily a sign the consumer is spent; but for once at least it does not show continued evidence of an unstoppable consumer.

Not only did the unchanged headline number come in short of expectations, but the control group aggregation of sales categories gave back 0.3% of last month's 1.0% gain (chart).

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Bond Yield Volatility Presents New Risks and Opportunities for Investors

Buy-and-hold strategies get left behind for trading riches

Bond mutual funds flip Treasuries at ratio 49% higher vs. 2022

… As with most things in the bond market, the volatility starts and ends with central bankers. Their retreat since 2022 as the bond market’s biggest buyers has ushered in price-sensitive investors who demand bigger payouts to sweep up a glut of supply.

“Volatility is also an opportunity,” said John Madziyire, a portfolio manager at Vanguard, which manages $9.3 trillion. “If you are a long-term investor it gives you better entry levels to get in.” …

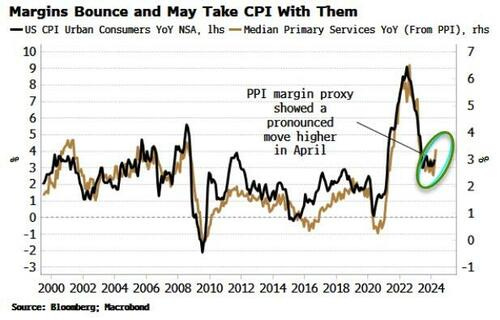

Bloomberg: CPI Does Not Signal Re-Emergence Of Disinflationary Trend

… Yields are in an interim trend lower as recessionary risks resurface, but the primary uptrend is intact.

There will be another bond selling opportunity later in the summer.

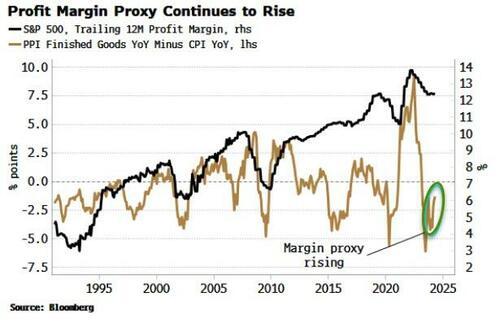

This rise in the profit-margin proxy matches the message from the primary services component of the PPI data...

Nothing moves in a straight line, and it is far too early to declare that the disinflationary trend has resumed.

WolfST: Beneath the Skin of CPI Inflation, April: After Some Zigs, a Zag. But 6-Month Core CPI Hits 4.0%, 6-Month Core Services CPI 6.0%, Highest since mid..

Month-to-month data is volatile. We’ll look at the trends.

… “Supercore CPI” — core services without housing — is whiplash volatile month to month. In April, it rose by 3.4%, after red-hot readings in January, February, and March (blue in the chart below).

The six-month reading – to soothe the whiplash of the month-to-month readings – jumped by 6.5%, a slight acceleration from the prior reading (+6.4%), the hottest since October 2022.