while WE slept: USTs touch lower ahead of NFP; "Bitcoin's 2025 Outlook" -Opening Bell; (JPM clients) outright LONGS highest in year; 'Earls home on the RANGE

Good morning … sorry for ‘radio silence’ yesterday … had to be in NYC for meetings and holiday gatherings. What did I miss?? A quick review of the charts and it would seem, well, not much, at least NOT as far as volatile 30yr yields price action …

30yy: aggressively UNCH in middle of (4.50 - 420) range

… momentum on DAILY is overBOUGHT so perhaps a strong NFP hitting RESET button, cheapning things up a bit, bringing in buyers (or those doubling down on longs — see JPM insights via BBG below) …

… A quick review in chronological order…

ZH: ADP Employment Disappoints, US Manufacturing Sees Biggest Job Losses Since June 2023

ZH: ISM Services Sentiment (Oddly) Slumps In November; Prices Up, Orders Down

ZH: Unexpectedly Hawkish Beige Book Finds Economic Activity "Rose" In Most Districts As "Slowness" Tumbles

NEWSQUAWK: US Market Open: Stocks steady ahead of upcoming US jobs print … USTs are a touch lower following yesterday's flattening of the curve. Fresh macro drivers for the US are on the light side in the run-up to today's NFP print … USTs are a touch lower following yesterday's flattening of the curve. Fresh macro drivers for the US are on the light side in the run-up to today's NFP print. Mar'25 UTSs are currently towards the top end of yesterday's 110.28+ to 111.08+ range …

Reuters Morning Bid: Long bond yields defused ahead of payrolls, France rallies

… The 30-year 'long bond' yield fell to 6-week lows of 4.31%, flattening the 2-30 year U.S. yield curve gap to just 16 basis points - its lowest since August …

Finviz (for everything else I might have overlooked …)

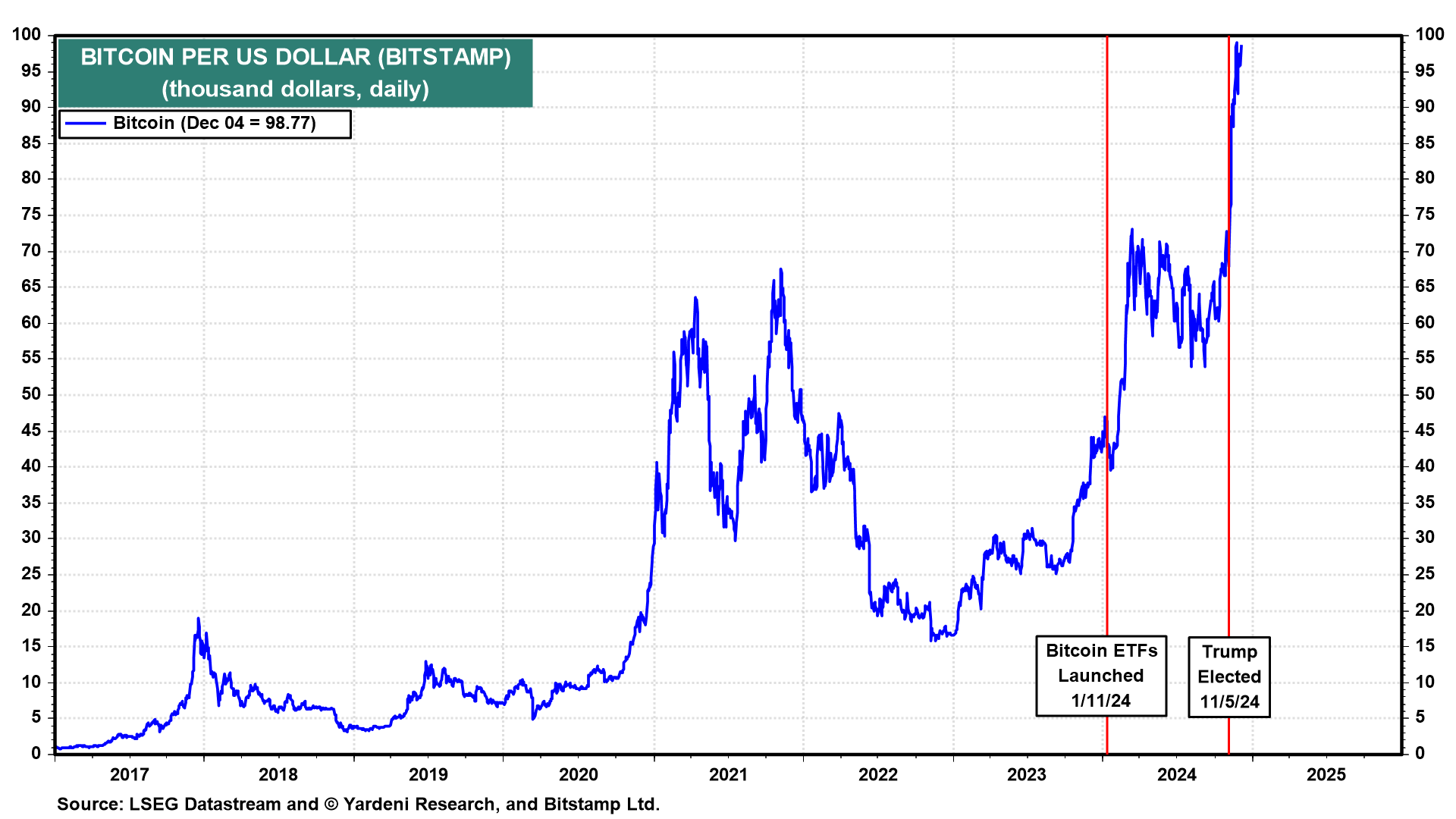

Opening Bell Daily: Bitcoin's 2025 Outlook … For bitcoin investors, $100,000 is just the start … Industry veterans shared their outlook for the cryptocurrency in 2025.

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ and which I may have missed AND which includes more than one NFP and CPI precap and victory lap …

BAML: Ten Macro Themes for 2025: Equity upside but not in a straight line

…3) US bond yields to remain in a range In 2025, Mark Cabana expects a relatively tight range for the 10Y, similar to 2024, and expects to end the year at 4.25%. Our forecast is built from relatively robust US econ macro projections. We expect to trade the 10Y range around 4-4.5% tactically …

The BLS updated its estimates of employment from the Quarterly Census of Employment and Wages through Q1 2024. At face value, these revisions imply that the upcoming benchmark adjustment will be about -668k, somewhat smaller than the -818k preliminary estimate.

BARCAP: U.S. Equity Strategy: Food for Thought: GOP Trifectas and Equity Returns

We find only 4 instances of unified GOP control of the US government prior to this year and since 1949. While a limited sample set, these periods were more beneficial for equities than GOP White House + split Congress, especially cyclicals, small caps and high-vol stocks.

Our baseline is for a 0.3% m/m core CPI, but we think it will be a close call between a rounded 0.2% and 0.3%.

In past months, airline fares have flown above past years’ pricing patterns despite falling jet fuel prices, evidently reflecting strong consumer demand for air travel and constrained airline capacity. We think airfare growth slows, but we could be surprised.

Recent noisy prints in motor vehicle insurance and ongoing uncertainty about owners’ equivalent rent pose bidirectional risks to our forecast.

Our forecast implies a preliminary 0.24% m/m core PCE reading for November, which would result in a higher sequential 3m, 6m and 12m rate of inflation for the second straight month.

…A worse look, but not so bad to prevent a December cut: Our November CPI forecast implies a 0.24% m/m increase in core PCE for the month. While this would avoid a rounded 0.3% print – barely – it would likely mean increased core PCE at the 3m, 6m and 12m horizons for the second straight month, the first such occurrence since December 2021. As Figure 10 shows, however you cut it, core inflation progress appears to be stalling…

…Our baseline remains for a cut in December, though we continue to see it as a close call. We think a significant upside surprise in either non-farm payrolls or CPI could sway the Committee into holding rates steady; likewise, moderately higher-than-expected readings in both prints could do the same. Conversely, seeing rates as still restrictive and having already laid the communications groundwork to pursue a pause next year if they choose, we think most officials will be comfortable proceeding with a December cut if just one of payrolls or CPI deliver a moderate upside surprise while the other prints in line with expectations.

… Just when you thought it was safe to relax into Christmas, along comes US payrolls today to keep you on your toes, especially with an upcoming close call as to whether the Fed cuts in 12 days time. Futures are currently pricing in a 70% probability that they will.

The Santa Claus rally we've seen over the last few weeks took a little breather last night in the US ahead of the data today. The S&P 500 (-0.19%) just missed out on 12 days of gains in the last 13 sessions, which would have been the first such run since 2013. However a more recent run continued in Europe yesterday as the STOXX 600 (+0.40%) was up for a 6th consecutive session.

As a background to today's report, last month underwhelmed, with nonfarm payrolls printing at just +12k, which was the weakest since December 2020 when the pandemic was still buffeting the economy. Private payrolls were at -28k, the first negative print since December 2020. But those numbers were impacted by strike action, whilst Hurricane Milton also hit Florida during the survey reference period. Our US economists expect a decent bounce back to +215k today. That would leave the unemployment rate unchanged at 4.1%, and they also see average hourly earnings growth at +0.3%. For more details and how to sign up to their subsequent webinar, click here…

ING Rates Spark: The ratchet lower in yields is far from done

…US 2yr finally manages a second leg lower The US 2yr has finally managed to break below the 4.15% area (now at 4.11%), following three failed attempts in the past week. In the past couple of weeks, it has had a tendency on a few occasions to test lower through the US afternoon, only to be pulled higher again in the European morning. We suspect this time it might be different.

There is an element of path of least resistance to the move lower, with the fall of the French government not deterministic, but at the very least symptomatic of a host of mad political manoeuvres in the past few weeks, and factors like eurozone macro malaise pushes in the same direction.

The US 2yr yield averaged 3.3% during the noughties, effectively at a 30bp spread over the funds rate. We reference the noughties as we view it as something of a neutral reference when averaged over the full decade. Currently, the 2yr trades some 40bp through the effective funds rate. If, as we expect, the Fed cuts by 100bp and nothing else happens, that would pitch the funds rate at 60bp through the 2yr yield. Based off that there is some room for the 2yr yield to test lower, likely to the 4% area. And there is scope to dip below 4%.

For the 10yr the floor should really be 4%. It can go as low as it wants to of course, but below 4% would look stretched from a relative value perspective, as it would push 10yr SOFR towards 3.5%. That's a stretch versus a market expectation for the funds rate not to get to 3.5% at all. Still tactically bullish though.

MS: US Economics: CPI Preview: Goods-Driven Strength

We see core CPI at 0.28% in November (3.3%Y). The lagged effect of hurricanes keeps used and new cars inflation positive, but OER and airfares inflation decelerate. Stronger food and energy move headline CPI close to core: 0.27%M (2.7%Y, NSA Index: 315.317)…

… On a 4Q/4Q basis, we forecast core PCE inflation slows from 3.2% last year to 2.9% (two digits: 2.85%) this year and 2.5% in 2025. Note that we boosted our 2025 inflation forecast adding the potential effect of tariffs – we were at 2.2% before the elections (see our Outlook for more details). Our 2024 inflation forecast is higher than the Fed's latest number (2.6%) published in the Summary of Economic Projections (SEP). The Fed will likely revise up their inflation numbers in the next FOMC meeting, and perhaps reduce the number of rate cuts in 2025 as a result.

US employment report Friday looms, when markets get excited about what an unreliable survey tells us about the economic outlook. The aftermath of strikes and hurricanes adds a lot of uncertainty to this report, and there is not really a consensus expectation for employment growth—just a wide range of random expectations. The forward guidance of this report is also diminished. Whatever the trends in employment, US President-elect Trump is proposing policies that might mark a structural break in employment conditions (most obviously deportations and tariffs)…

Summary Stalling progress on the inflation fight should be evident in the November Consumer Price Index. We expect headline CPI to advance 0.25% over the month and 2.7% over the past year. The core index should similarly rise around 0.25%, which would keep the 12-month change stuck in the narrow range of 3.2%-3.3% for a sixth straight month. While some key sources of inflationary pressure, such as an overheated labor market, continue to dissipate, new headwinds to disinflation have emerged (e.g., the potential for tariffs and tax cuts) that make the final leg of inflation's journey back to the Fed's 2% target look increasingly difficult.

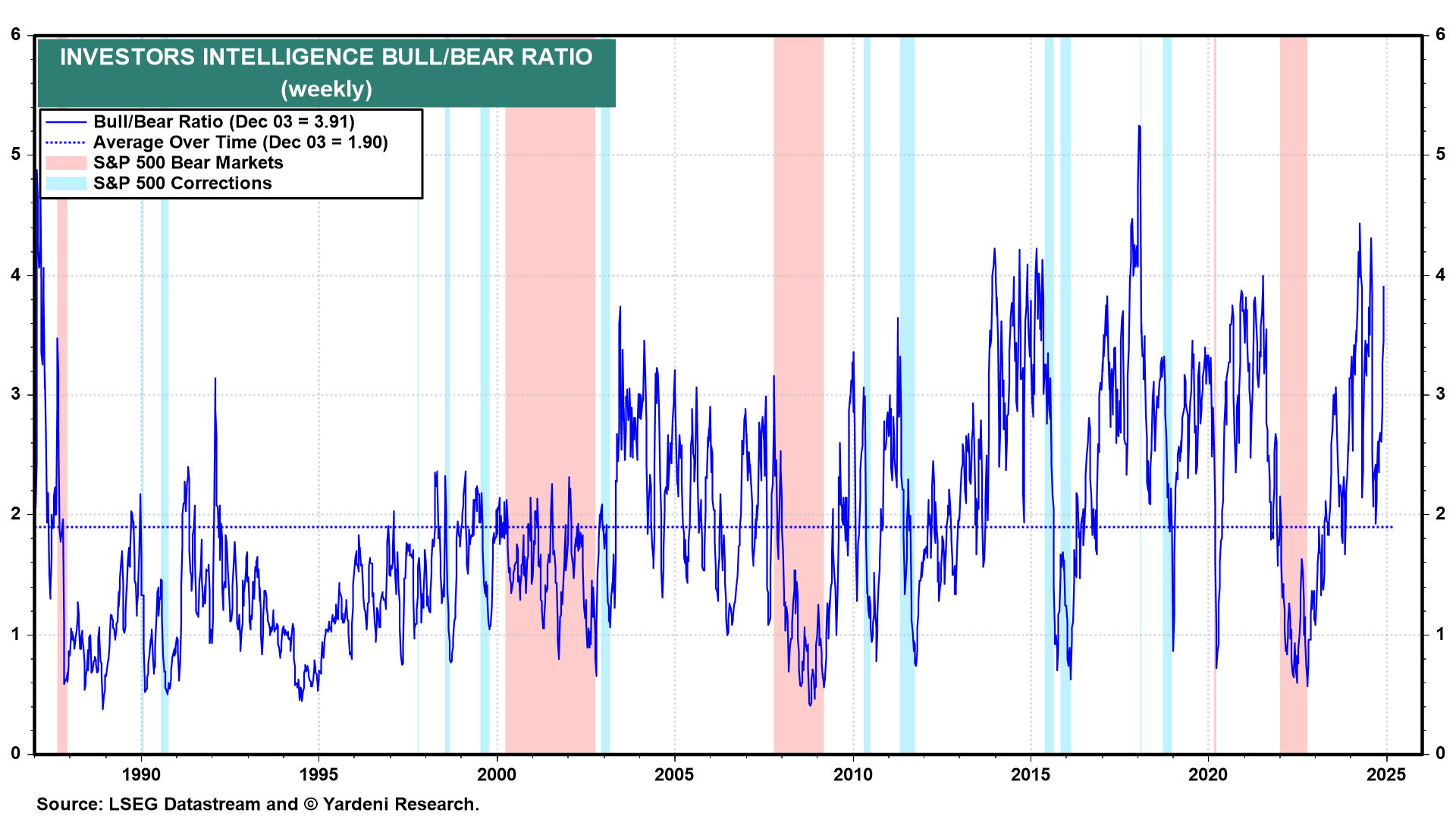

Yardeni: Contrarian Indicators Showing Too Many Bulls

We were very bullish at the start of this year with a Street-high year-end price target of 5400 for the S&P 500. That level was surpassed on June 12. We weren't bullish enough as the stampeding bulls left hoof marks on our backs. So we raised our target to 5800 on July 10, which was surpassed on November 6 (chart). So we raised our target to 6,100 last month thanks to Trump 2.0 and the Fed's dovishness. We remain bullish on the outlook for the US economy and stock market through the end of this year and decade. We think the Roaring 2020s could turn into the Roaring 2030s.

However, for the here and now, there may be too many charged up bulls. Of course, the most charged up ones are in the Bitcoin market (chart).

Contrarian indicators are turning bearish suggesting the new year might start with a stock market pullback. If so, that will probably be attributable to rebalancing portfolios at the start of the new year rather than the end of the old year to postpone taxes on substantial capital gains. So it shouldn't last very long and would be a buying opportunity. Here's what we're seeing:

(1) Bull/bear ratio. The Investors Intelligence Bull/Bear Ratio has surged from 2.3 in mid-October to 3.9 last week. The percentage of bulls is up to 62.9%, around historical highs.

… And from Global Wall Street inbox TO the WWW …

AAA: An Early Holiday Gift? Gas Prices Plunge to Three-Year Low

…Today’s national average for a gallon of gas is $3.03, seven cents less than a month ago and 19 cents less than a year ago.

The Plaza Accord was a meeting held in September 1985 at the Plaza Hotel, where the G7 countries agreed to intervene in FX markets to depreciate the US dollar, see chart below. We will not see a repeat of the Plaza Accord today for two reasons. First, the dollar is far from the levels of appreciation seen in the mid-1980s. Second, the economic outlook for Europe, the UK, Canada, and Australia is weak, and the rest of the G7 wants to continue to depreciate their exchange rates to boost their exports.

Bloomberg: Bond Traders Position for US Treasury Market to Extend Rebound

JPMorgan client long bond positions rise to biggest in a year

Trading surge after Fed’s Waller leans toward Dec. rate cut

… JPMorgan Chase & Co.’s weekly survey on Tuesday showed that its clients’ have boosted their long positions in US government debt to the highest in a year, dropping what had been a neutral stance toward the securities. The change follows a rally over the past two weeks that was aided by strong demand at the Treasury’s note auctions.

JPMorgan Treasury All-Client Positioning Survey Outright longs jump to biggest in a year

WolfST: Everybody Should Get Used to these Mortgage Rates, Says Fannie Mae CEO: Mortgage Rates, 10-Year Treasury Yields, QT, and Spreads

“Current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades.”

“It’s important for mortgage investors, the housing market, and consumers to understand that it is unlikely we will again see the low mortgage rates we had during the COVID-19 pandemic, when a unique combination of monetary and fiscal policy sent rates to near all-time lows,” wrote Priscilla Almodovar, the CEO of Fannie Mae, the largest of the Government Sponsored Enterprises that have been in conservatorship of the federal government since the mortgage crisis. They buy mortgages from lenders, guarantee them, package them into MBS, and sell the MBS to investors around the globe.

“In fact, current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades. Since 1990, the 30-year fixed-rate mortgage has averaged 6%,” she said in the post published by MarketWatch today.

In fact, the average 30-year fixed mortgage rates were never below 5% in the data from Freddie Mac, which goes back to 1971, until the Fed started buying MBS in January 2009, which pushed mortgage rates below 5% for the first time ever.

In fact, in fact, in fact… mortgage rates were above 6% the entire time in the data until October 2002, after the Fed had embarked on slashing rates to create Housing Bubble 1 to make up for the imploded stock market. And three years later, by October 2005, after the Fed had embarked on blowing up its Housing Bubble 1, mortgage rates were back above 6% and stayed there until January 2008, when the Fed kicked off QE by buying Treasury securities to deal with the financial system that was on the brink of imploding due to the imploding mortgages. And mortgage rates began to descend, and in January 2009, with Housing Bubble 1 having collapsed and morphed into the mortgage crisis and the broader Financial Crisis, the Fed started buying MBS which pushed down mortgage rates further…

AND …

… somewhat more (NFP recaps / victory laps) to follow over weekend but for now … THAT is all for now. Off to the day job…