… More from the pros below … and with such a strong (?) jobs report, obviously hard to find ready and willing buyers of 10s …

ZH: Dreadful 10Y Auction Sees Biggest Tail Since 2024, Foreign Demand Slides

… don’t forget to get those bond bids in early and often … and I’m done … moving right along …

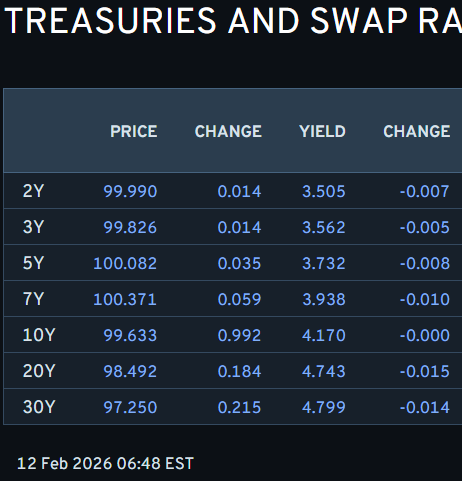

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 648a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures broadly in the green; China’s MOFCOM announces a tariff of up to 11.7% (prev. 42.7%) on EU dairy products … A similar story for USTs, rangebound in APAC hours towards the mid-point of the post-NFP drop. Holding at 112-11+ in thin parameters that are well within Wednesday’s 112-00 to 112-20 bound. Today, the US docket is comparatively light, with supply and weekly jobs the highlights. Barring a surprise on those, it may be a bit of a filler day into Friday’s CPI.

Finviz (for everything else I might have overlooked …)

…Moving from some of the news to some of THE VIEWS of Global Wall you might be able to use … Here’s a healthy but perhaps incomplete list of some of the NFP recaps and victory laps …

January's employment report defied indications from alternative indicators of a softer labor market, with stronger-than-expected readings for job gains, the unemployment rate and payroll income. Although the numbers speak to diminished downside risks for employment, the jobs signal is exaggerated.

…We retain our view that the FOMC will deliver two 25bp cuts to the funds rate this year, in June and December. This is conditioned on the FOMC seeing evidence this spring that cost-push pressures from tariffs are receding, and that the labor market is not tightening sufficiently to reignite worries about upward wage pressures. We regard risks to this outlook as being tilted to the upside, with the FOMC delaying pushing back the timing of rate cuts amid sluggishly elevated inflation and a more resilient economy…

USTs selloff bigly, reluctance repriced IN …

February 11, 2026 BMO Payrolls gain +130k, UNR 4.3%, TSY Selloff Sharply

…Overall, it was a much stronger-than-expected payrolls update that comes in contrast to the private measures. This divergence will be topical as the market continues to digest the data. Treasuries rallied into the data and since the print, have cheapened sharply with 10-year yields back to 4.20%. From here, this afternoon's 10-year refunding auction will be in focus. The combination of payrolls and the short set-up present a challenge for underwriting the new issue…

… On the surface, January’s BLS employment figures were strong, but a few caveats have left investors reluctant to assume that the labor market is out of the woods. First, job gains were highly concentrated in construction and health care. Second, the annual benchmark revisions brought the average monthly payrolls change for 2025 down to just +15k from +49k. Third, the 4.3% unemployment rate came with the caveat that, "The severe weather did impact the collection of household survey data, and the January response rate of 64.3 percent was below average.” Nonetheless, the data was strong enough to push the market-implied odds of a March rate cut down to 6.0%. While the Fed will still have the benefit of one additional BLS payrolls report before it reconvenes next month, the fact that the unemployment rate is 4.3% sets a high bar for the balance of the intermeeting data to justify a rate reduction in Q1…

…Technical Analysis …30s – Daily stochastics have crossed and curled in favor of lower rates in the 30-year sector. First resistance is 4.85%, which also represents the Bollinger mid. 4.817% is the 50-day moving average before a bullish hurdle at 4.80%. Through there, 4.775% is the Bollinger Band bottom before the bottom of the local trading range at 4.769%. 4.75% will serve as clear resistance, which also resonates with the 100-day moving average at 4.747%. In terms of support, we like the 9-day moving average at 4.874%, then see little until 4.90%. The Bollinger Band top is 4.926%, then a push above the level would find support at the top of the six-month trading range at 4.945%.

Jobs encouraging, fine, but what about the ‘swans’ out there …

January’s solid employment report underscores what we think will be Fed caution on delivering further rate cuts, which aligns with our base case of no cuts through 2027.

The drop in unemployment to 4.3% in January will likely ease Fed concerns about the US jobs market. We see bidirectional risks to the unemployment rate ahead.

The revision to nonfarm payrolls shows better momentum in the back half of 2025 and early 2026 than many had feared, in line with our expectations and supports our glass-half-full view of the US jobs market amid a solid GDP growth trajectory.

The biggest market moves are frequently caused by the least-anticipated events – but those events might just be anticipated with a bit of work. Investing in tail-risk analysis is rewarding most of the time, but perhaps unusually so in 2026, at a moment when politics, investor flows, technology and financial risks are all arguably in flux. Here we analyse 10 of these 'grey swans' across asset classes, themes and regions – and aim to explore how investors might best prepare for the unusual…

…Handling grey swans: The bigger market moves often occur when something previously thought of as unlikely suddenly happens (Figure 1). These ‘grey swans’ – considered possible but unlikely – often have an outsized impact both because they surprise and because few have planned or positioned for them…

…US Treasuries: 30y yields exceed 6% Why it’s important: US Treasuries enjoy a unique place in the global financial system as a ‘risk-free’ asset, making them an input into valuations of ‘risky’ assets worldwide. If investors price the US’s fiscal path as unsustainable, Treasuries might lose their unique risk-free status, with an unbounded rise in yields in which 30y Treasuries top 6%. Such a re-rating could have lasting impacts on Treasury valuations, valuations of risk assets, and the ability of US fiscal policy to support growth.

How it might happen: The administration’s efforts to address affordability concerns ahead of November’s mid-term elections affect market perceptions of US finances and encourage ‘bond vigilantes’ to sell Treasuries. A rise in yields is sharper if overseas investors, especially in Europe, decrease their Treasury holdings, and even sharper if the Fed resists using its balance sheet to control yields, amid above-target inflation. Unreliable liquidity and a vulnerable market structure exacerbate conditions.

Which asset class is most exposed: An unbounded rise in Treasury yields would affect valuations across asset classes, including FX, credit, and equities. Risky assets in particular could suffer big drawdowns.

What is causing long-end yields to rise? Fiscal stresses are expanding in the G4. When we published Tail risks 2025: BNP Paribas grey-swan analysis in February 2025, the most pertinent example of a fiscal-stress-driven bond sell-off was in the UK – the ‘Liz Truss moment’ of 2022. However, in 2025, there were at least a couple more instances of fiscal concerns weighing on markets, including the most recent turmoil in the JGB market with long-end JGB yields hitting multidecade highs. Political and fiscal uncertainty in France in the summer of 2025 also drove OAT–Bund spreads wider. In many ways, these episodes could serve as a warning for the UST market, which is in a delicate state to begin with.

Higher yields could limit US fiscal support: The biggest consequence of the current delicate setup on the fiscal side is that it limits the room to provide fiscal support to the US economy if yields climb sharply higher. Bond yields were discussed before the 2025 One Big Beautiful Bill Act, highlighting the feedback loop. If 30y yields head to 6% or more, it would be harder to deploy any fiscal measures, even in economic downturns – which is apparent in the UK (Figure 2).

Bond yields and risk assets price structural cheapness: An episode of 30y yields moving to 6% might inject a structural feature of a ‘credit risk premium’ into US Treasuries, and by extension risky assets. Such a premium would make Treasuries less likely to rally in economic stress, shifting the distribution of Treasury yields, and structurally depress valuations of risky assets as well.

Charts … I like them and here are a few from Germany on the jobs market along with a few words from fan fav stratEgerist …

…That jobs report was the big story yesterday, with the release proving much stronger than expected. The headline was that nonfarm payrolls grew by +130k in January (vs. +65k expected), marking their biggest monthly jump since December 2024. Indeed, it was a big contrast from fears earlier this week about a low number, as Kevin Hassett had warned on Monday that markets should expect “slightly lower jobs numbers”, albeit without specifics about when this might be. Then on top of the upside payrolls surprise, the unemployment rate unexpectedly fell back to 4.3% (vs. 4.4% expected), so the print very much leant in a more hawkish direction. Admittedly, there were some negative revisions to previous months, with the 2025 total payrolls gain revised down from +584k to +181k. But we already knew the downward revisions were coming, so markets were much more focused on the strong print for January rather than the backward-looking content.

With the jobs report coming in strongly, markets moved to price out the chance of rapid Fed rate cuts this year. For instance, the chance of a rate cut in one of Chair Powell’s final two meetings (March and April) plunged from 47% to 23%. And looking at the full year, the amount of cuts priced by the December meeting fell -7.1bps on the day to 53bps. In turn, that more hawkish profile led to a clear bear flattening in the Treasury curve, with the 2yr yield (+5.8bps) up to 3.51%, whilst the 10yr yield (+3.0bps) moved up to 4.17%…

11 February 2026 DB US Economic Chartbook - January jobs report: Another strong start to the year

…Importantly, the January household survey data show notable improvement – particularly, amongst younger age cohorts where there has been significant concern over the AI threat to entry level jobs. Case in point, the unemployment rate for 20-24 year-olds fell by a full percentage point to 7.1% in January – its lowest level since April 2024 (6.7%). The employment / population ratio for the 20-24 age cohort (66.3%) is now at its highest level since last March. Similarly, the unemployment rate for 16-19 year-olds declined by two percentage points to 13.6% last month – its lowest since last September (13.3%). Though we hesitate to put too much stock into any one employment report, the recent improvements in labor slack in younger age cohorts should somewhat diminish fears that AI has had a noticeable impact on entry-level jobs.

In summary, the January employment report was strong across the board, similar to what we’ve seen at the beginning of the past two years. In turn, Fed officials are likely to remain firmly on the sidelines near term. While the report doesn’t solve all debates over the underlying health of the labor market, at minimum, it does point to supply factors perhaps starting to edge out demand. Indeed, a recent Fed’s Notes concluded that the slowdown in the second half of 2025 was primarily driven by labor supply, though there were some signs of weakening demand…

…Private payroll gains of 172k in January well exceeded expectations

AND if still here, not yet bored or seen this one …

February 11, 2026 First Trust: Data Watch - Nonfarm Payrolls Increased 130,000 in January

…Implications: … In addition, the Labor Department updated it’s “birth/death” model for businesses, which pushed down the estimate for job growth after March 2025. As a result, it now says nonfarm payrolls only gained 181,000 last year versus a prior estimate of 584,000. Keep in mind that federal payrolls, excluding the Post Office and Census, are down 312,000 from a year ago, the steepest drop in decades. But even factoring that in suggests private payroll growth is trending well below 100,000 per month, much less the 172,000 in January. Look for much slower headline numbers on payroll growth in the months ahead.

Strong data, USTs bear flatten …

February 11, 2026 MS PULSE: U.S. Data Pulse: Strong payrolls and a lower UE rate. Labor market rebound in 4Q.

Key takeaways

Payrolls jumped in January despite a drag from government employment, and the unemployment rate continued to retreat from its November high.

Benchmark revisions subtracted 72k/month on average in 12-m through March 25, as expected. But revs were small since then, subtracting 10k per month on average.

Payrolls show more weakness early last year & more rebound recently; the labor market rebound is made more convincing by the further drop in UE rate.

Unemployment rate printed at 4.28% but would have been a 4.1% without the rise in LFPR.

For the Fed: a stronger rebound in payrolls and a lower unemployment rate lessen chances of any near term cut. Cuts will depend on disinflation.

February 11, 2026 MS PULSE: U.S. Data Pulse: Benchmark revisions to nonfarm payrolls imply faster productivity growth

Key takeaways

Benchmark revisions reduced the level of payroll employment in March 2025 by 836k, or by 72k per month on average between April 2024 and March 2025.

We estimate this will boost nonfarm productivity. We project it will be revised higher to 2.4% y/y through 3Q 2025, up from 1.9% previously

The tug of war on potential growth continues. Immigration controls pull capacity for hours worked down, while productivity pushes in the other direction.

US rates bear-flatten with payrolls at +130k and unemployment at 4.3%; CAD and MXN underperform as US reportedly weighs exiting the USMCA; RBA's Hauser emphasizes inflation concerns; potential tweaks to US-India trade agreement; DXY at 96.89 (+0.1%); US 10y at 4.17 (+3.0bp)…

…US rates bear-flatten (2y: +6bp; 30y: +2bp) as markets price a more hawkish Fed policy path. Consensus still expects two 25bp rate cuts by year end, but the implied timing of the next cut has been pushed from the June meeting to July. The weak demand is reflected in the afternoon’s 10y auction, which tails by 1.4bp. Our US economists agree that the stronger rebound in payrolls and falling unemployment rate lessen the chances of a near-term Fed cut.

NFP and CPI matter as well as whatever incoming Fed chair does with balance sheet…

… In the US, our call for June and September remains unchanged after the Fed Chair nomination and nonfarm payrolls. The recent Fed meeting affirmed our stance and the subsequent nomination of a Fed Chair does not alter our outlook, as discussed. Our Fed path follows our view on inflation, where, after a strong December print, we expect core PCE inflation to abate as we move into 2Q26. Market focus also pivoted to the Fed Balance Sheet with the Warsh nomination — we do believe the balance sheet will be in focus, but it will take time for any real changes to happen …

The January US employment report signaled sufficient strength to cool market expectations of an urgent US rate reduction. There is no evidence of political interference in the data. However, the data quality is questionable—survey response rates remain low, and the Bureau of Labor Statistics has lost staff. There was a surprise sharp increase in foreign-born US worker employment and a drop in US-born US worker employment in the past two months. The 2025 data showed a broad-based decline in manufacturing employment, even in sectors protected by tariffs.

The US affordability crisis is having a political impact, with several Republican members of Congress siding with Democrats to oppose tariffs on US importers of Canadian products. This is unlikely to change anything as US President Trump would presumably veto any anti-tariff legislation…

Far from perfect …

February 11, 2026 Wells Fargo: January Employment: Strong Start Out of the Gate

Summary …The U.S. labor market is far from perfect, with hiring still concentrated in a handful of industries, certain demographics enduring elevated unemployment rates and cyclical demand for new labor still tepid. That said, it appears the labor market is closer to stabilization than rapid deterioration, and this will embolden the hawks on the FOMC to push for no changes to the fed funds rate for the foreseeable future. We have been saying for some time now that the window for the FOMC to cut rates is closing, and today’s data suggest another rate cut under Chair Powell is increasingly unlikely. If cuts are coming this year, it appears that it will be up to a future Chair Warsh to win over the hawks on the Committee and deliver before year-end.

Source: U.S. Department of Labor and Wells Fargo Economics

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

Jobs … perhaps not as good as it seemed? An OpED and more from The Terminal…

Updated on February 11, 2026 at 4:19 PM UTC Bloomberg: Fed’s Path to More Rate Cuts Challenged by Jobs Surprise

February 12, 2026 at 5:00 AM UTC Bloomberg: About the US jobs market? It’s complicated Strength in non-farm payrolls makes further interest-rate cuts that much harder to justify.

Bang!

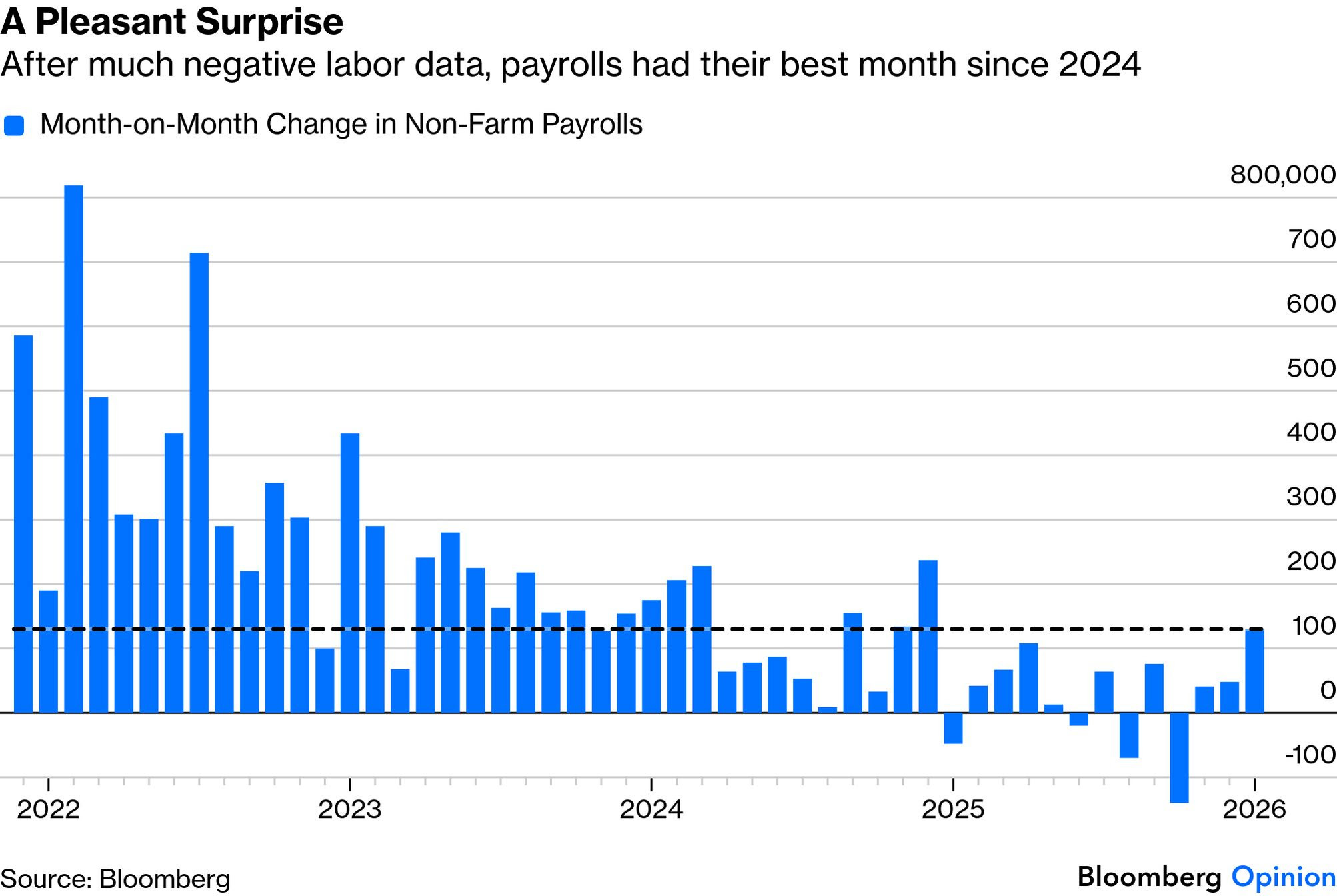

Good economic news makes a pleasant change. Or does it? Wednesday dawned with traders braced for another decline in jobs growth. Instead, non-farm payrolls grew by 130,000 in January, better than any month of 2025, while the unemployment rate fell. That’s evidently good news for the US workforce, and for those who’ve been arguing that the global economy is in something of a sweet spot:

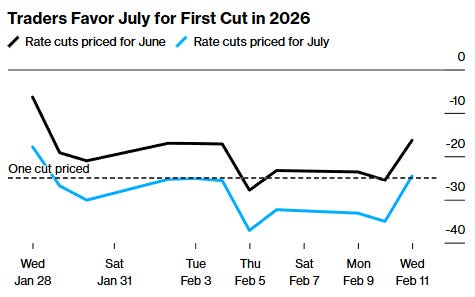

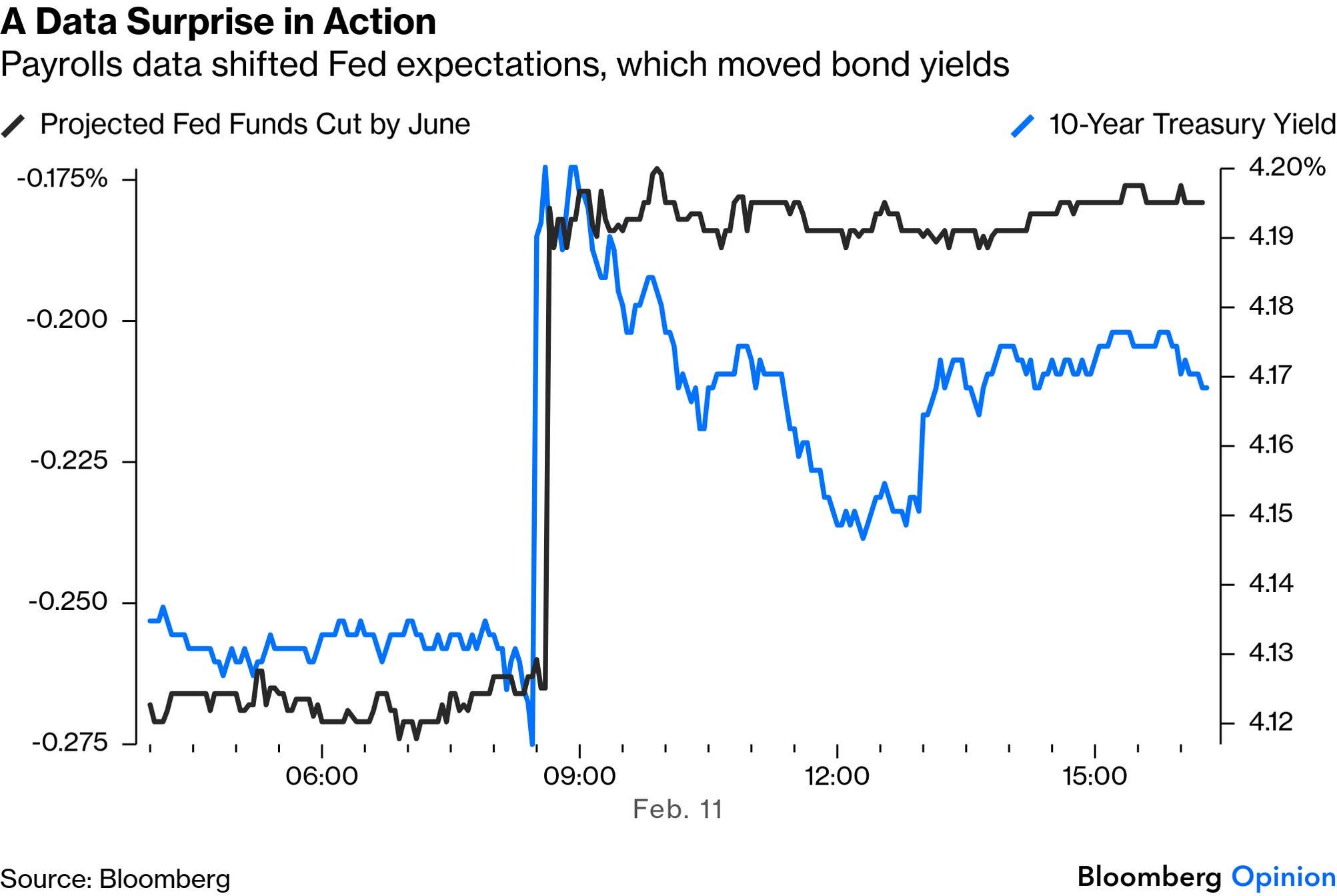

No news is ever unalloyedly positive, however. Strength like this in the jobs market makes further interest-rate cuts that much harder to justify. Futures pushed back the likely date of the next easing to July from June. That had a direct knock-on effect on bond yields, which rose sharply:

Futures are still pricing in two cuts for the full year, but it’s questionable whether that is a fair bet. The available workforce is smaller than it used to be, thanks to demographics. The ratio of those in employment to the entire population is unimpressive. But repeating that exercise for those in the prime working ages of 25 to 54 yields a very different outcome. For all practical purposes, the US appears to be close to full employment:

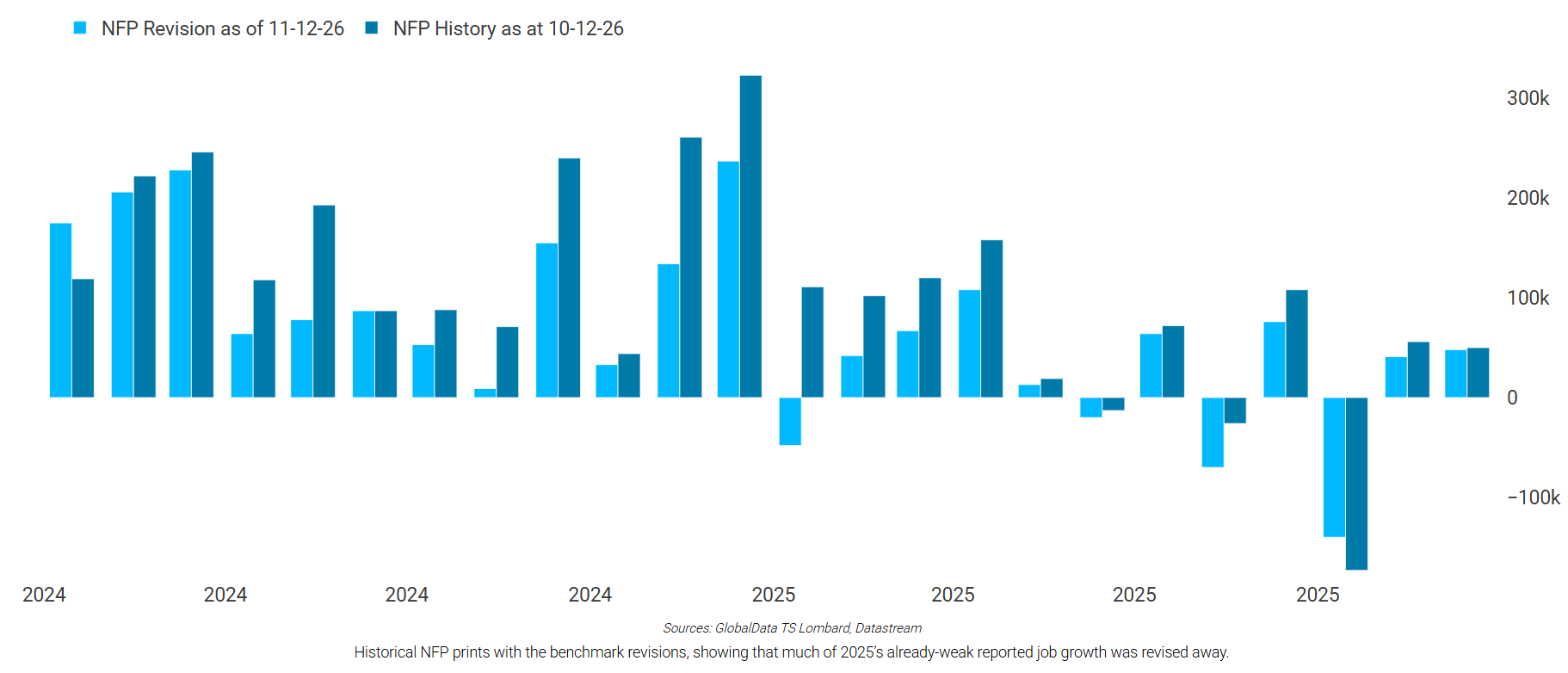

All of this has to come with the caveat that payroll data is noisy and revision-prone at the best of times, and even more so after the shutdown forced government statisticians to down tools late last year. Freya Beamish of TS Lombard shows that much of 2025’salready anaemic growth has been revised away:

But she points out that the potential supply of workers has also been revised down, suggesting that the economy is still running close to capacity. The unwelcome corollary is the risk that any stimulus will be channeled into creating more inflation, still arguably the biggest political issue confronting the US. Projections in the swap market have risen a bit, but remain under control:

The next big data release, taking the payroll’s usual spot on Friday morning, will be January CPI. If the consensus of economists polled by Bloomberg has it right, core inflation will drop to a new post-pandemic low of 2.5%. In combination with the latest jobs numbers, that sounds almost like Goldilocks financial conditions — not too hot, not too cold — and would maintain the chance of rate cuts later this year:

At the margin, however, the confidence in two cuts is beginning to look overdone, despite the president’s clear expectation that Kevin Warsh, his nominee to take over the Federal Reserve chairmanship in May, will deliver at least this much easing. “The market is saying that Warsh will come in and cut twice,” says Beamish. “That’s certainly what he intends to do, but maybe the market won’t be confident with him doing that later in the year.”

And there remains a more negative way to view the labor market. This is not a dynamic US economy and inequality is intensifying. Viktor Shvets of Macquarie Capital points to continuing low wage growth (with average hourly earnings now up 3.7% year-on-year), while gains flow mostly to those who already own assets:

These factors are key to reconciling depressed surveys with strong output: People know they are falling behind, absolutely and relatively, and it is unlikely that middle-class jobs will ever come back. The immigration crackdown is making things worse, as immigrants are mostly complements not substitutes for local labor.

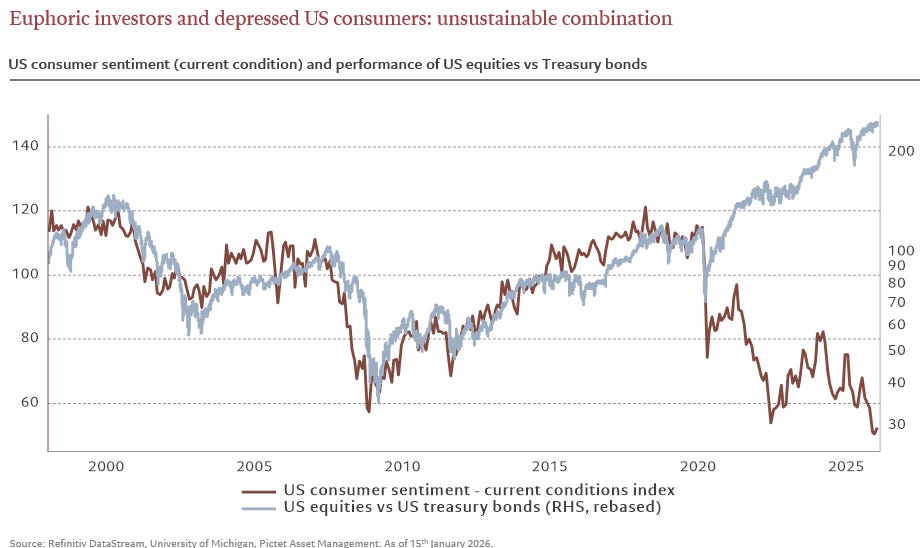

This helps explain the “K-shape” divergence between consumer sentiment and the stock market. Normally, they move together. Since the pandemic, the dispersion has been extraordinary, as demonstrated by this chart from Pictet Asset Management:

It’s hard to frame the biggest rise in employment in more than a year as anything other than good news. But many in the markets have managed to do it.

Charts … I … never mind …

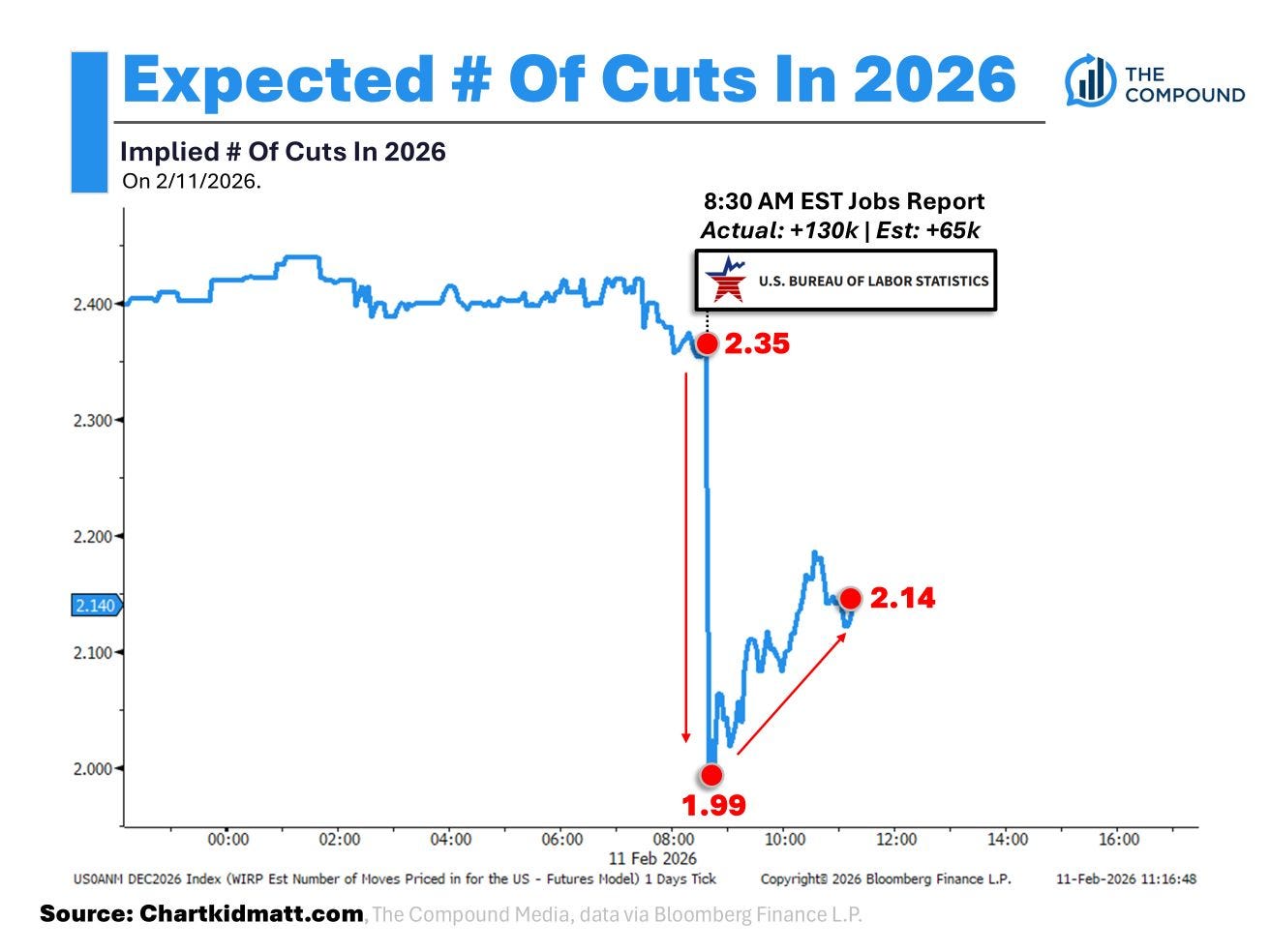

Feb 11, 2026 Chart Kid Matt: Charting The Jobs Report Charting The Jobs Report - Four Charts To Summarize The Data.

…Fed Fund Futures initially took the report as “hawkish” with the # of cuts expected in 2026 falling from 2.35 pre report to 1.99 post report.

The initial reaction seems to be exaggerated, however, as the # of rate cuts expected in 2026 has been creeping higher after the initial downward reaction.

…2. NFP revisions. "Payroll gains for 2025 have been revised down to +181k ... in the full history of payroll data, the only year that has been weaker when it comes to gains is 2003".

If the Employment numbers were so strong....why are 10yr yields down...

Even after an abysmal auction......4.128%