while WE slept: USTs steady, equities under pressure; "Fed priced to be MOST dovish in world" (may be wrong -DB) and this same pricing driving historical EQUITY price action ...

ZH: Saved By The Seasonals: Headline SpendingSurprises As 'Real' Retail Sales Plunge

… said another way …

… AND much to MY surprise (?), some resilient data combined with some Fedspeak blowing wind in the sails of Team Rate CUT, Fed Governor Kugler commented on LABOR MKT CONDITIONS suggesting that

… This continued rebalancing suggests that inflation will continue to move down toward our 2 percent target …

… and so, the lower yields narrative continued to dominate trading activity in stocks as well as bonds where 10s dropped to 4mo lows and 2s fell to 5mo lows!! The good news is that 20s are still NOT through multi month lows (‘DIP-portunity’?) and ahead of this afternoons 20yr auction …

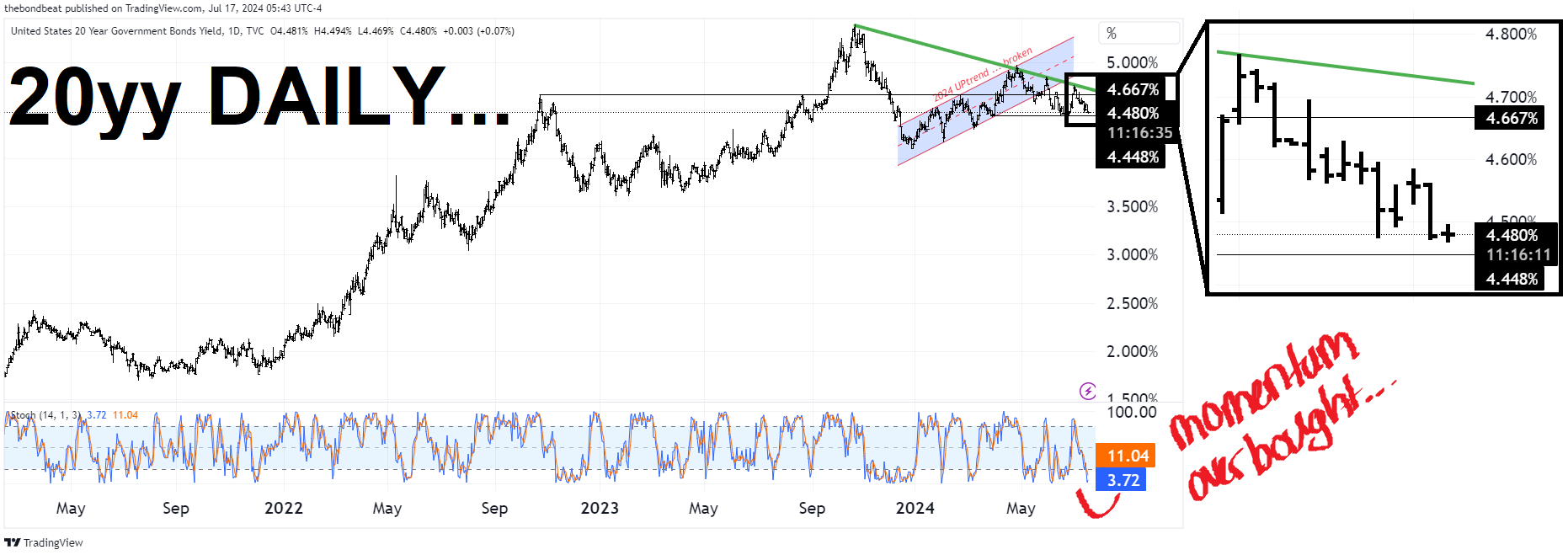

20yy DAILY: momentum (stochastics) extended (ie overBOUGHT) and this has not mattered (yet)

4.45% is resistance (TLINE drawn off the UPTREND channel which defined H1 of 2024) and should we break below, well … I’ll head back TO drawing board

… for somewhat more / comprehensive look at levels to watch and what implications of breaks MEAN, kindly refer to techAmentals noted HERE (think 2s TO 4.12, 5s TO 4.00, 10s TO 4.00 and long bonds TO 4.20) …

Before moving on, I’d like to interrupt and mention there will be an interruption of normal spammation of the intertubes as I will be travelling over the next few days with limited access things (charts, Global Wall inbox, etc) and so there will be NO output tomorrow and there’s a small chance of nothing until early next week. That can change if time and ‘conditions’ (capabilities) change and I apologize in advance for any inconvenience …

And now, here is a snapshot OF USTs as of 632a:

… and for some MORE of the news you might be able to use…

Reuters Morning Bid: Small caps soar in catch-up rotation, Trump jars Taiwan

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ ‘bout surprise ReSale TALES (is it me or is everyone thinking this a one-off and completely underwhelmed by the data … i mean yea, sure it’s anti rate cut narrative but …) and otherwise…

BAML: Global Fund Manager Survey: In Soft We Trust

Bottom Line: FMS investors remain bullish driven by Fed rate cuts & soft landing; July growth expectations lower and FMS cash level up to 4.1% but change in “long equityshort bond” conviction awaits shock to soft landing narrative (and politics entrenching existing conviction); BofA Bull & Bear Indicator remains at 6.3.

FMS on Growth: global growth expectations fall from -6% to -27% (net), largest drop since Mar’22 (Chart); but investors very optimistic on “soft landing” (68%) versus “no landing” (18%) or “hard landing” (11%); 67% expect no recession in next 12 months.

BARCAP: June Retail Sales: Don't call it a comeback

Control group sales jumped 0.9% m/m in June, continuing their ascent following April's soft patch. Carryover effects position consumer goods spending for a solid increase in the third quarter, with an Amazon Prime Day sale and favorable payback effects for auto sales likely on tap for July.

BMO: Retail Sales and Import Prices Surprise Higher

… Overall, it was a bond bearish round of data that suggests the slowing trend in spending has stabilized and imported inflation remains a relevant factor. That said, there isn't anything in the release that would shift expectations for a September Fed cut…

DB: US Inflation Outlook: May's good news becomes great with rent downshift

Primary rents and OER seem to have finally normalized

DB: No, it's not a "Trump trade" (Saravelos speaks, we listen … actually the visual is what caught MY attention)

… If the market was putting on a "Trump trade", we think the exact opposite should be happening: the dollar should be strengthening and US yields should be rising. Why? We are gaining rising conviction on three things happening under a Republican Sweep.

The likelihood of a US recession goes down… The likelihood of a dramatic shift in trade policy goes up… The dollar would likely remain the pre-eminent safe-haven currency of choice…

… Bringing it all together, the market over the last few days has priced the Fed to be the most dovish central bank in the world (chart 1). In contrast, we think the market should be pricing the Fed to be one of the most hawkish central banks in the world…

Markets have done very well recently: the S&P 500 keeps hitting new records, and Treasury yields are around their lowest in months.

This has been driven by several factors, including much better news on inflation, which in turn has led to anticipation that the Fed might soon cut rates for the first time since the pandemic.

But the current rally is now in historic territory. Since the inflation news started to meaningfully improve in late-2023, the S&P 500 has been up for 28 of the last 37 weeks. That hasn’t been seen since 1989. Alongside that, we’ve seen a massive market rotation, and the small-cap Russell 2000 is up by more than 11% in the last 5 days, even as the Magnificent 7 is down by more than -2% in that time.

1. The S&P 500 is now up for 28 of the last 37 weeks for the first time since 1989.

… Several factors are responsible, but the latest moves reflect a growing belief that the Fed are finally about to pivot in a more dovish direction…

DB: Early Morning Reid (on rotation, ReSale TALES and FedFunds)

… Rotation is the key word in financial markets at the moment as the leadership of the US market has very rapidly shifted away from the Mag-7 to the wider market. This trend is only a few days old but so far its been done without any damage to the overall market as last night the S&P 500 (+0.64%) closed at its 38th all-time high of 2024 so far, having now risen for 10 of the last 11 sessions. A further rise today would be the first 11 out of 12 run since April 2019. Zooming out the S&P 500 has risen for 28 out of the last 37 weeks, the best such streak in 35 years…

… For the most part, sentiment was supported by the retail sales data, which showed headline retail sales were unchanged in June (vs. -0.3% expected). The details were also pretty good, as the measure excluding autos had its fastest growth in 3 months at +0.4% (vs. +0.1% expected), and there were positive revisions to the May number as well. In turn, that led to growing optimism about the Q2 GDP release next week, and the Atlanta Fed’s GDPNow estimate now sees growth coming in at an annualised rate of +2.5%. It got as low as +1.5% on July 3.

Admittedly, that strength in retail sales did work against the other main theme at the moment, which is the growing anticipation about rate cuts. But ultimately, near-term expectations for rate cuts didn’t shift too much, as the positive retail sales data wasn’t enough to push back against the other data over recent weeks, and futures are still fully pricing in a rate cut by the Fed’s September meeting. Those expectations for rate cuts got some support yesterday from commodity price moves, with Brent crude oil prices (-1.28%) falling back to a one-month low of $83.76/bbl. In addition, Canada’s CPI also surprised on the downside in June, coming in at +2.7% (vs. +2.8% expected).

Altogether a lower yield narrative dominated, as 10yr US yields (-7.1bps to 4.16%) closed at their lowest level in 4 months with a temporary 4bps intra-day sell-off after retail sales not holding. And 2yr yields fell to a 5-month low (-4.1bps to 4.42%). The rally in Treasuries was helped along by dovish-leaning comments from Fed Governor Kugler who said that “continued rebalancing (in the labour market) suggests that inflation will continue to move down toward our 2% target” …

NatWEST: US: Retail Sales (June … where GDP upwardly revised = rates to be cut?)

Retail sales ex-autos and gasoline rose in June by 0.8%, stronger than expected and well above trend

We have raised our Q2 real GDP forecast from +1.5% annualized to 2.0% (given evidence of a somewhat stronger spending pace at quarter end)

Wells Fargo: Despite Upside Surprise, Retail Sales Show Lost Momentum (headline ‘bout lost momentum but … )

Summary Despite lower sales at autos dealers and at gas stations, retail spending held steady in June. Excluding those categories, it was the best month since January 2023, and that means upside risk for Q2 consumer spending.

… In stripping out a few more components, like restaurants and building materials, the control group measure of sales came in even stronger, rising 0.9% last month. Recall that this measure feeds directly into the BEA's calculation of real goods spending in the GDP accounts, and while retail growth has outpaced broader goods spending recently (chart), the better-than-expected outturn positions for a rebound in Q2 goods consumption after a weak first quarter. Real goods spending slipped at a 2.3% annualized rate in Q1, and today's data present some upside to our estimate for total real personal consumption expenditures to rise at a 1.6% annualized rate in Q2.

We've been predicting a broadening stock market meltup in the event that the Fed starts cutting the federal funds rate (FFR) as inflation moderates while economic growth remains solid. Last week's CPI and today's retail sales report confirm that's what's happening in the economy. Fed Chair Jerome Powell's dovish comments yesterday sealed the deal: As of this morning, markets were pricing in a 100% chance of a 25bps FFR cut in September, per the CME FedWatch Tool, up from a 70% chance a month ago. A total of five such cuts are expected over the next 12 months (chart).

Also fueling the meltup: The betting marketplace PredictItis now showing 2:1 odds of former President Donald Trump winning in November, up from a coin-flip two months ago. For now, investors may be focusing on Trump's low tax-rates policy rather than his high tariff-rates policy. Trump is also likely to deregulate business with the help of the recent SCOTUS ruling that reduced the power of the government's regulatory agencies…

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Bond Traders Look Past Trump Trade to Bet Big on Fed Rate Cuts (Bolingbroke on POSITIONS…)

Past week reveals dovish positioning shift in derivatives

JPMorgan Treasury client longs jump to largest since January

It’s game on in the Treasuries futures and options markets where traders are piling into bets for earlier, deeper interest-rate cuts from the Federal Reserve…

… Monday also saw a huge block buy over the morning session that established new long positions in the October tenor. Those bets would benefit from 25-basis point rate cuts in both July and September — or a fifty-point move at the September meeting. Trading in many of these contracts is anonymous, which makes it difficult to identify the firms behind those bets.

That sentiment has spilled over into the cash market, too. The latest JPMorgan Chase & Co. survey released Tuesday showed outright long positions rising to the most since January…

While auto and gasoline station sales fells heavily in June, there was significant strength elsewhere that provided an equal offset. It may be that the weather has boosted retail footfall as people try to escape the heat, but there are still challenges for the sector from weak real income growth, a run down in savings levels and high borrowing costs

… Nonetheless, the data reflects nominal US dollar value changes. The chart above shows that real (volume) terms retail sales remain around 4 percentage points below their 2021 peak and it is volume growth that matters for GDP – the advanced second quarter estimate is released next Thursday. Moreover, retail sales as a proportion of total consumer spending is converging on the pre-pandemic trend after having spiked in 2020 and 2021.

WolfST: Retail Sales Excl. Autos & Gasoline Jump by Most in 18 Months & Pushed Up Atlanta Fed GDPNow to 2.5% from 2.0% Last Week

Auto sales hit by CDK hack. Gasoline and auto sales in dollars hit by dropping prices, but they boost inflation-adjusted consumer spending.

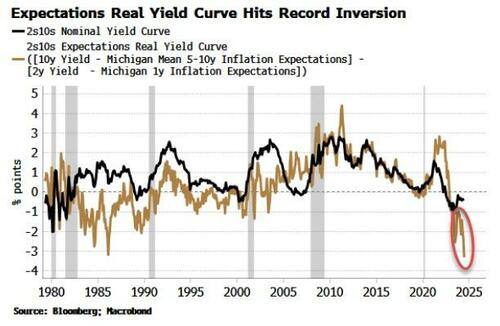

ZH: 'The Other Yield Curve' Flashes 'Trump Trade' Warning

Authored by Simon White, Bloomberg macro strategist,

The yield curve based on inflation expectations has flattened significantly and is now more inverted than it ever has been - and it will remain under pressure in the event of a Trump presidential victory. This “expectations curve” shows that consumers are anticipating much tighter financial conditions than inferred by the market via the nominal yield curve, presenting a risk to consumption, broader economic growth and equity valuations and returns.

The so-called Trump trade received a boost this week after the attempt on the likely presidential candidate’s life. That has drawn extra attention to the steepening yield curve, but the easing in financial conditions it implies is in stark contrast to a lesser-followed curve.

The expectations real-yield curve uses consumer inflation expectations to deflate yields. Inflation is an inherently backwards-looking measure: the latest data tells you where price growth was over the last month or year, not where it is going. Inflation’s anticipated path can inform the decisions consumers are more likely to make, rather than looking in the rear-view mirror at the effects of decisions that have already been made.

Using the University of Michigan consumer survey’s estimates of long and short-term inflation expectations we can construct the expectations real-yield curve. As the chart below shows, the curve is now the most inverted it has been since the data begins in 1979.

The expectations yield curve has tracked the nominal curve pretty well apart from in the mid-1980s and the 2000s. The curves have closely followed each other since the GFC, but lately the divergence has grown almost as deep as it ever has been, representing a widening gulf between the market’s and consumers’ views on financial conditions.

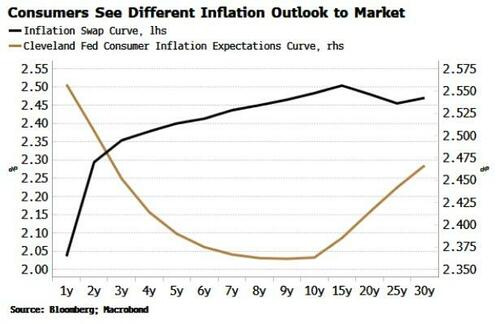

The stark contrast between the market and Main Street can also be seen in the difference between the inflation-expectations curve and the inflation-swap curve. While the latter is positively sloped, with the market anticipating (marginally) higher inflation in the longer term versus the near term, consumers see the opposite, with the expectations curve inverted out to 10 years (based on data from the Cleveland Federal Reserve).

As an important aside, the extreme inversion in the expectations curve in the first chart above is not just an artefact of the rapid rise in Michigan’s mean measure of 5-10 years inflation expectations. If we use the median value, or indeed the Cleveland Fed’s data, we still get a heavily inverted curve near its extremes…

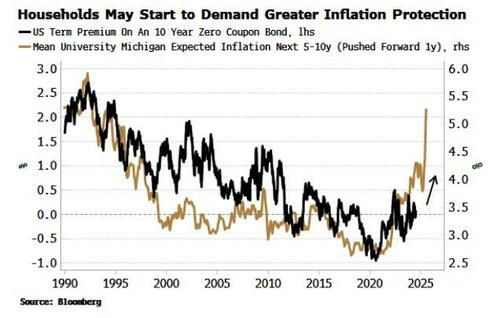

… Rising inflation expectations also risk feeding through to higher bond yields. Households have been the marginal buyer of USTs for most of the last two years. Term premium has remained low, but persistently elevated inflation expectations may lead to households demanding extra compensation for taking on the greater real risk of holding bonds.

Even so, real yields could still fall if inflation outpaces the extra yield demanded…

… Before I close, a reminder … there will be an interruption of normal spammation of the intertubes as I will be travelling over the next few days. I will have a very limited access to things (charts, Global Wall inbox, etc) and so there will be NO output tomorrow and there’s a small chance of nothing until early next week. That can change if time and ‘conditions’ (capabilities) change and I apologize in advance for any inconvenience …

Finally …

TBP: Gold Keeps Rising No Matter What Powell Says (really for the visual but also given highs and that I was approached at my local Costco over the weekend offering me 2400.00 / ounce for gold that’s about to sell out — our location has NOT had this before and likely won’t get inventory again soon — the workers I spoke with suggested it was selling like hotcakes !! ?? !!!! anyways, the picture here says a LOT, IMO)

Thanks for the Simon White piece, that was paywalled on ZH. Safe travels bud!