while WE slept: USTs soft tone; IJC > cpi; updated Fed call (4 cuts in row -MS); 25 or 50? 25 (but 7k S&P -Dr. Bond Vigilante); beware the Market Analyst (defined)...

Sep 12, 2025

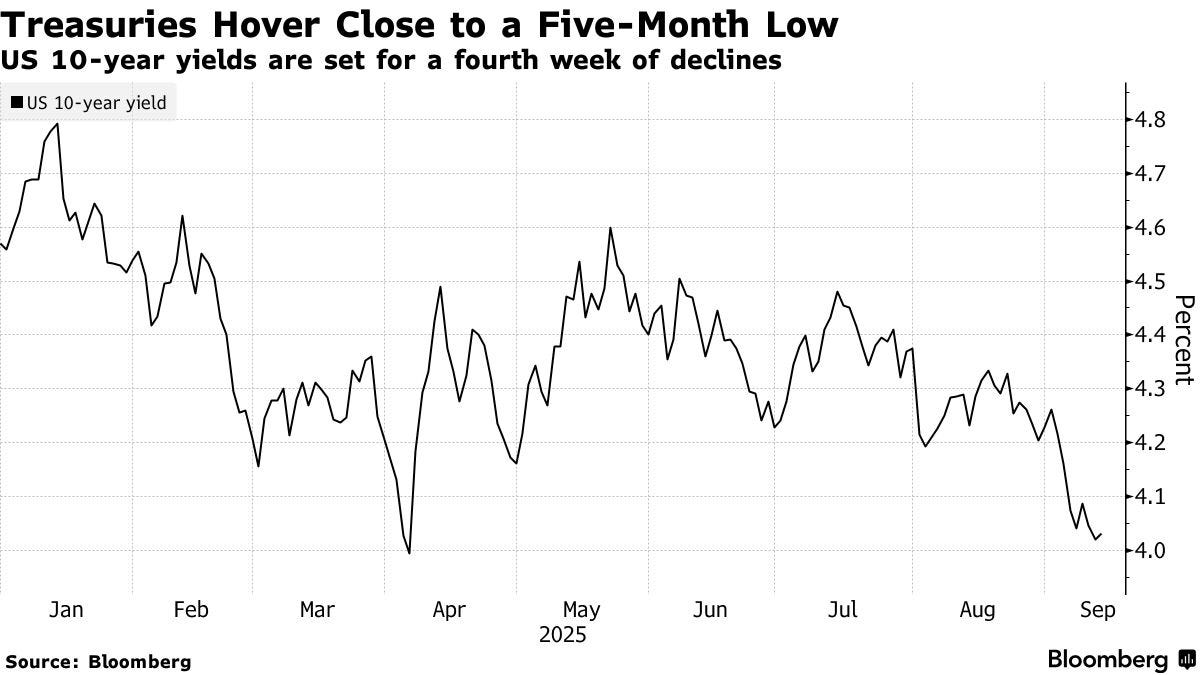

Good morning … Equity futures are MIXED and UST yields are inching higher … Yields have been down so long they look up? I’ll not make too much of the move higher and lean on a somewhat longer-term (ie weekly) visual of 10s …

10yy WEEKLY (line): 4.25% support and ~4.00% resistance in greater context…

… trend is yer friend … yes, watching bearish momentum …

… and moving along hoping to have a bit more over the weekend as this week does finally come to an end … But first, incorporated into price action … um, the data ahead of the long bond auction …

ZH: US Consumer Prices Rise More Than Expected In August From Services Not Tariffs

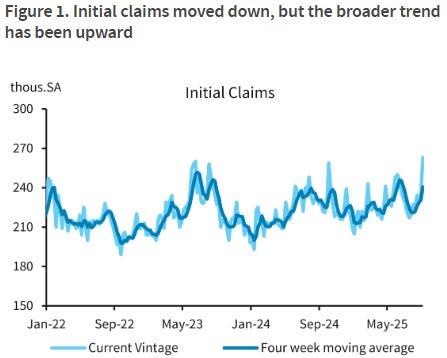

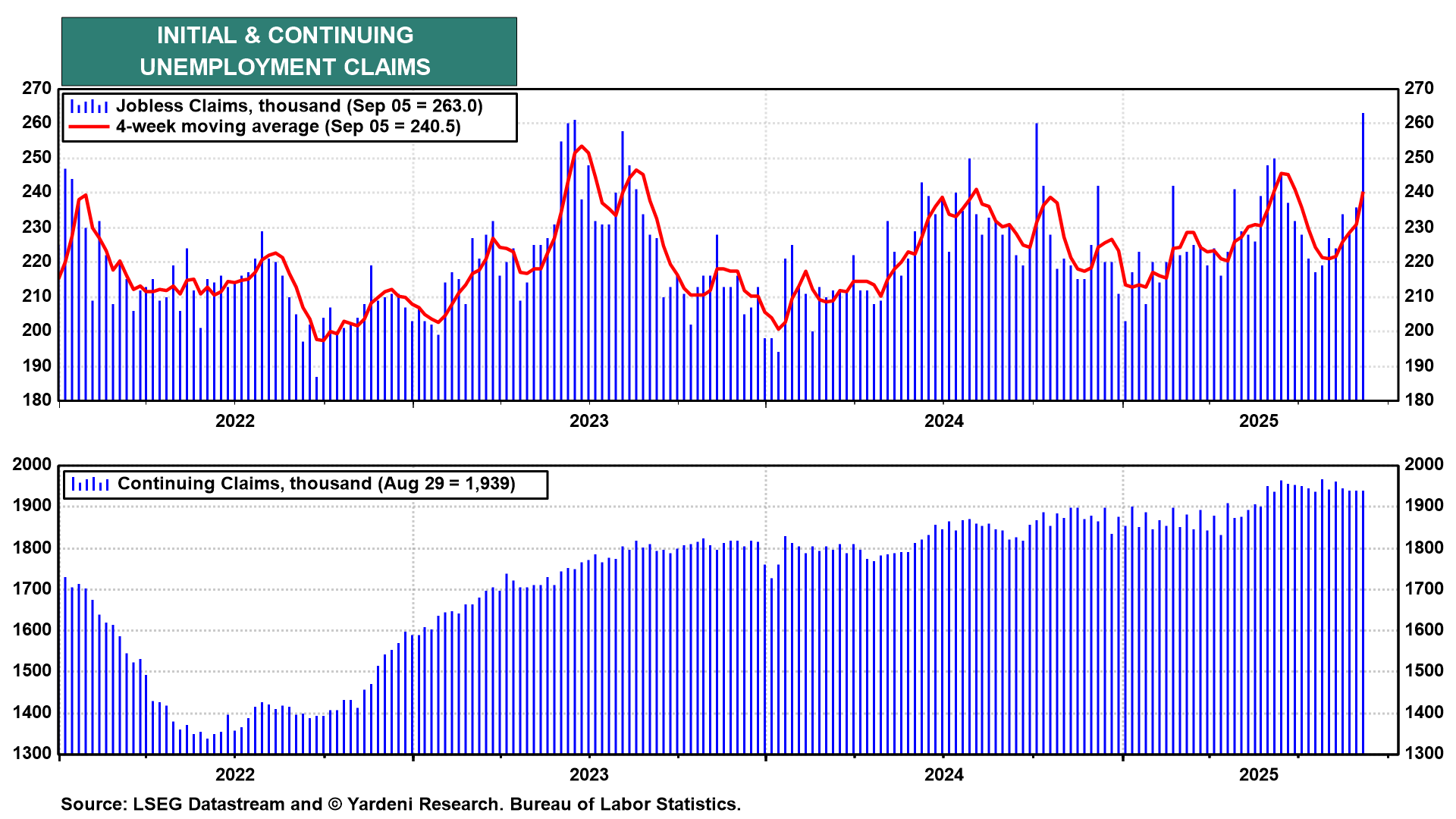

ZH: Texas Sparks Unexpected Surge In Jobless Claims To Highest In 4 Years

… and so, its my (un)educated guess the claims data were perceived to be far worse (for the economy and so, rate cuts) than the CPI (which, IMO, wasn’t good for rate cuts) … Then I got an email from contact at Brean … with a John Ryding update …

Large jump in IJC offsetting headline CPI and with the debate about employment side of mandate. Curve steepening…

JOHN RYDING 08:32:29 Core CPI in August rose 0.3% as expected, which kept the core CPI inflation rate at 3.1%, but the headline reading was higher than expected at 0.4%, which lifted the CPI inflation rate to 2.9% from 2.7%…

…And as far as the long bond auction goes … you say RECORD and you’ve got my attention …

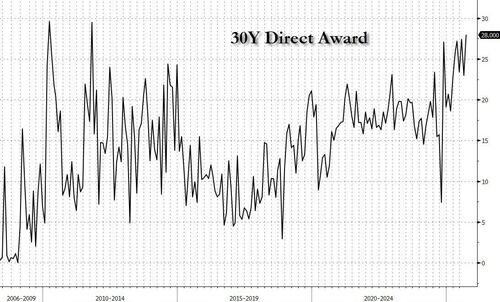

ZH: Impressive 30Y Auction With Near Record-High Directs Keeps 10Y Yield At 4.00%

… After two stellar, near-record coupon auctions earlier this week, including one of the best ever 3Y auction on Tuesday, and a similarly strong 10Y yesterday, moments ago the Treasury concluded the week's auction when it sold $22 billion in 30Y paper in what was again another remarkably strong auction.

Today's 30Y sale stopped at a high yield of 4.651%, down from 4.813% last month and the lowest since March; it also priced "on the screws" with the 4.651% When Issued, following last month's badly tailing auction…

…The internals were solid with Foreign buyers taking down 62.03%, up from 59.52% and the highest since June. It was also above the recent average of 60.9%. And with Directs jumping to 28.01% from 23.03% and the highest going back all the way back to October 2011, or right after the first US downgrade...

... Dealers were left with just 10.0%, the lowest since June 2023…

Generally speaking, this all makes sense. Dealers not required to warehouse supply this week on their balance sheet as there’s continued flow of buyers lining up ahead of rate cuts trying to lock in these rates before they are materially LOWER …

At same time, equities are priced for continued perfection and as you’ll note — don’t need ME to point out — stock jockeys leaning on rate cuts but if / when there is some sort of realization WHY cuts (ie JOBS matters more than inflation which is cooperating at moment), then bad news may become really bad. For those with 7k targets on the S&P?

If / when stocks say, were to decline, I’d be willing to bet bonds catch even MORE of those flows … and so … it makes perfect sense…for now. Then again, this…

"One of the frustrating things for people who miss the first rally in a bull market is that they wait for the big correction, and it never comes. The market just keeps climbing and climbing." - Martin Zweig

… here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures are modestly lower, DXY mildly gains whilst Gilts outperform post-GDP … Fixed income is in the red, though USTs are set to end the week near-enough unchanged. Gilts are the relative outperformer post-GDP … A softer start to the final session of a packed week. Today’s docket is a little lighter stateside, University of Michigan is the main data event while scheduled speakers are light aside from POTUS on Fox at 13:00BST, an interview likely to focus on Charlie Kirk. Currently, USTs are lower by a handful of ticks in a thin c. five tick range which is comfortably within Thursday’s 113-09 to 113-29 band. September aside, Treasury Secretary Bessent met this week with Warsh, Lindsey, and Bullard regarding the Chair position. Will be speaking with sitting officials’ post-blackout. His goal is to add one or two names to the list of candidates.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Knew it … everything IS BIGGER in Texas … and oh, yea, the ‘flation — slowly but surely — and this British shop ALSO reminds us not to fight the Fed OR the AI …

11 September 2025 Barclays US Economics Research: Initial claims: Everything's bigger in Texas, including idiosyncrasies

Initial claims jumped 27k, in SA terms, in the week ended September 6. Most of this was idiosyncratic to Texas (+21k). More broadly, initial claims have drifted into the upper end of the typical NSA range for this time of year, and remain consistent with the job market's low turnover equilibrium.

11 September 2025 Barclays US Economics Research: August CPI: Noisy core services and more evidence of tariff pass-through

Core CPI accelerated to 0.35% m/m (3.1% y/y) as expected, led by a run-up in core goods prices. While core services inflation remained elevated, there were lots of moving parts and less signal to extrapolate from. We are tracking core PCE inflation at 0.21% m/m (2.9% y/y) for August.

…We continue to expect tariff-related cost pressures to raise consumer prices in subsequent months. The statutory tariffs in place imply a trade-weighted tariff of 14-17%, substantially higher than the 2.5% going into this year, and undoubtedly inflationary for goods prices. We continue to expect about a 50% pass-through of tariff costs to prices, and expect this to play out over the next four to six months. The reasons we expect this staggered pass-through are the strong stockpiling by firms early in the year, and the fact that the effective tariff rate being paid, on aggregate, was still tracking "only" close to 11% through June, due to trade diversion. However, we expect this to tick higher as imports normalize and some exemptions potentially are removed (see Mind the tariff gap, August 2025).

The August CPI data added to evidence of tariffs passing through to core goods prices, albeit gradually. We tweak our core CPI forecasts to show a shallower peak in Oct/Nov, but more drawn-out effects into Q2 26 amid growing risks that the pass-through could be more staggered across categories.

…The new path implies a slightly lower annual rate for core CPI in December 2025, of 3.6% y/y (-0.1pp), but slightly higher for December 2026, at 2.6% y/y (+0.2pp). This implies core PCE price inflation is slightly lower, at 3.2%, on a Q4/Q4 basis in 2025, but higher in 2026, at 2.4%.

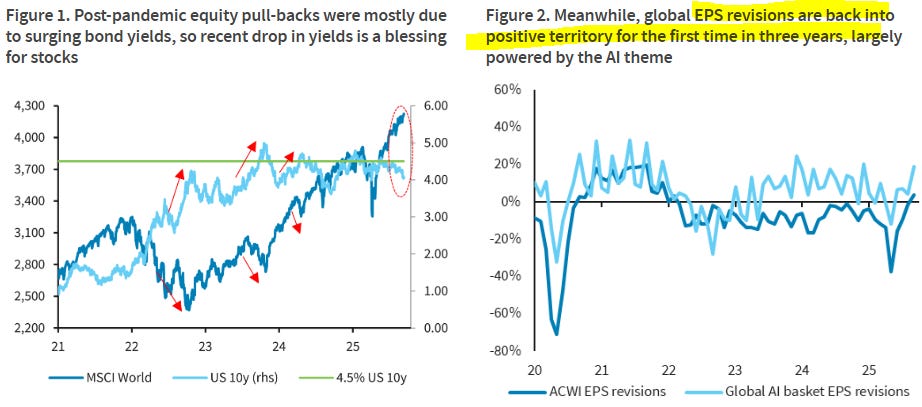

Falling yields and AI boom keep the party going for equity markets. But while stocks have taken softer employment in their stride, it warrants attention. As US, China & Japan make new highs, Europe is stuck in a range amid no AI support and geopolitical concerns. At least, euro rally has moderated.

Don't fight the Fed, Don't fight AI. Equity markets continue to melt up even as dovishness extends in the rates market. The latest inflation prints (both CPI and PPI) in the US reinforced this pricing further, with rates markets now looking for c.6x cuts over the next year and a terminal rate of c.3%. And after the soft labour market data last week (NFP, Jolts and ADP), the downward payroll revisions of 911k along with a further rise in jobless claims to cycle high this week solidified the case for Fed to resume its cutting cycle sooner rather than later. However, while restart of Fed cuts after a significant pause has historically come amid increased recession risk, it doesn't necessarily confirm one (see What happens after Fed cuts resume?, 10 Sep). So far indeed, activity remains resilient and data surprises are positive elsewhere, suggesting that the economy is still holding up okay, keeping downturn concerns at bay. Meanwhile, the AI theme remains another powerful tailwind for equities. Recent earnings from OracleandAlibaba highlighted strong momentum in their cloud and infrastructure divisions, triggering sharp rallies and lifting sentiment across the broader tech and AI ecosystem. Both US andChina tech sectors are seeing robust EPS momentum, which is increasingly supportive for aggregate equity earnings given the size and influence of these firms. Consequently, investors have taken a glass half full approach, which we agree with. But with equity markets at all time high, volatility at lows and rate expectations sharply lowered already, we believe that further weakening in employment would likely start challenging the well-priced Goldilocks narrative. So hedging for the left tail risk still makes sense to us.

… remind me again, then, WHY cuts needed? Oh, right, jobs … nvm

Claims UP, CPI meh … and as the day panned out …

September 11, 2025 BMO: Jobless Claims Highest Since Oct 2021; Core-CPI +0.346% in Aug

CPI in August came in at +0.4% MoM vs. +0.2% MoM in July and +0.3% MoM consensus. This is the highest since January. The YoY pace increased, as-expected to 2.9% vs. 2.7% prior. Core-CPI was +0.3% (unrounded 0.346%) -- in line with expectations. YoY core-CPI was unchanged at 3.1%. Core-CPI services ex-shelter came in at +0.225% in August vs. +0.550% in July while core-CPI services ex-rent/OER was +0.330% versus +0.479% prior. Core goods were +0.3% in August (+0.276% unrounded) -- indicating limited tariff passthrough. Initial Jobless Claims for the week of Sept 6 came in at 263k vs. 236k prior and 235k forecasted -- the highest since October 2021. Continuing Claims printed at 1939k vs. 1939k prior and 1950k anticipated. Overall, this set of data reinforced the limited inflationary fallout from the trade war (thus far) and the mounting concern that the labor market is quickly weakening. This clears the way for a 25 bp cut next week and leaves 50 bp on the table, although we remain in the 25 bp camp.

Ahead of the data, the front end of the market was slightly cheaper but relatively unchanged. Since the release, we've seen a solid rally across the curve that has been led by the 2-year sector. From here, the market will continue to digest the data and the monetary policy implications. Let us not forget this afternoon's $22 bn long-bond auction -- although the results are less relevant given this morning's data…

…Treasuries responded to the highest claims print since 2021 more than the as-expected core inflation figures. At 263k for the week of September 6, the initial jobless claims figures reinforced the labor market jitters that were already well-established ahead of today’s data. There are two key caveats – it was for the week containing Labor Day (seasonal adjustments can be challenging around holidays) and a large portion of the gains came from Texas, implying that there was a seasonal worker component. Nonetheless, the combination of the trajectory of payrolls, the unemployment rate, and claims more broadly cannot be so easily excused away – to say nothing of the -911k benchmark NFP revisions. Said differently, while the level of jobless claims might be attributable to idiosyncratic factors, it doesn’t change the fact that the US labor market has lost its prior resilience.

Our approach to Thursday’s dataset was one of expecting that it would either put a 50 bp cut on the table or take it completely off. At present, the probability of a 50 bp cut is 7% – suggesting that we were misguided in assuming that today’s session would be definitive regarding the chances that the Fed decides to go with the larger of the two options. It seems likely that we’ll now head into Wednesday’s decision with a non-zero probability priced in for a 50 bp cut, even as we struggle to envision the Fed being able to justify the angst implied by a half-point cut. There is also the concern about the perception of losing central bank independence and ostensibly relenting to Trump’s calls for a large rate cut. The data profile is now consistent with a less restrictive Fed policy but supercore inflation continues to point toward the prudence of being above neutral at the moment.

In our endeavor to be intellectually honest, it isn’t inconceivable that a sharp and widespread decline in retail sales during August (data released on Tuesday) could further downgrade the growth outlook and bring a 50 bp cut into the conversation – but it is still extremely unlikely. Instead, the market will be presented with a quarter-point move and forward guidance that we expect will be less dovish than investors are anticipating, or at least hoping for. The composition of CPI and PPI now have core-PCE estimates tracking at a low +0.2%. However, the limited evidence of tariff pass-through thus far doesn’t negate the risk that prices are increased in the months to come. The Committee will surely want to retain some flexibility on the pace of normalization due to this lingering risk.

Another key takeaway from Thursday’s session was that all three of this week’s auctions stopped through – reinforcing the perception that there is plenty of demand for Treasuries at these levels and in this environment. There is still scope for diversification away from Treasuries and into other core fixed income holdings, although the peak risk that such a rotation becomes a market event is behind us. Friday’s session isn’t likely to shift the prevailing momentum and following a fresh round of consolidation, we expect that the path of least resistance will be toward lower yields further out the curve. A tactical flattening in the near-term, although our core steepening view remains well intact as the FOMC readies to lower rates.

All the countries weighing in on the CPI and here’s France view …

11 SEP 2025 BNP US August CPI: Pass-through present, but looking more gradual

KEY MESSAGES\

Although the US August CPI print was solid overall, we think the underlying details were somewhat softer than the headline number suggested.

The print showed continued evidence of tariff pass-through, but suggestive of a more gradual process rather than an accelerated step-up.

We attribute some of the strength in services to residual seasonality, but improving fundamentals seem to be at play as well. This combination likely means service inflation remains firm through year end.

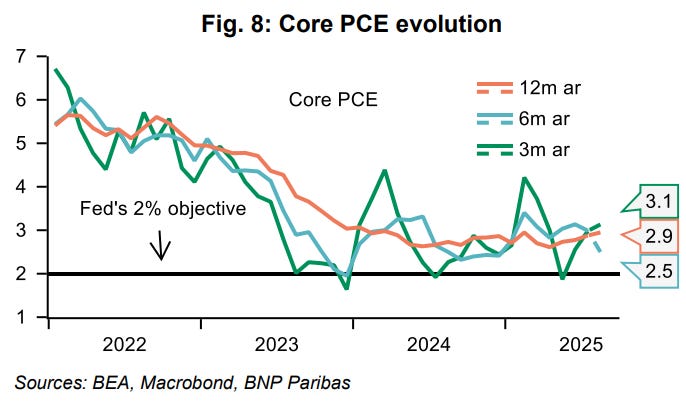

… Core PCE likely softer than core CPI: We revise our estimates for headline and core PCE downward to 0.27% m/m and 0.24%, respectively, following the CPI and PPI reports (prior est: headline 0.33%, core 0.31%). This implies the y/y rate for headline PCE edges up a tenth to 2.7% from 2.6% in July while core PCE remains steady at 2.9%. We attribute the decline in our estimates to core goods excluding vehicles and parts coming in at 0.12%, below our expectation of 0.55%. PPI hospitals, domestic airfares and portfolio management services all added about 9bp, supporting our PCE estimates from more of a decline.

Looking ahead, headline and core PCE would need to run at a soft 0.3% m/m on average from September through year end in order to achieve the June FOMC’s % q4/q4 median SEP estimates of 3.0% and 3.1%…

Germany weighing in with an early morning run through markets AND recap / victory lap of CPI (hmmm, I’m sure it’s nothing) …

…As we approach the end of the week, markets have been in a buoyant mood over the last 24 hours, continuing into this morning's Asian session, with investor attention squarely focused on the slightly higher than expected US August CPI release, and the notably higher than expected jobless claims data. The influence of the latter won out with December fed futures spiking to price in 76bps of cuts immediately after the numbers, having been at 68bps before the release. We ended up pricing in 72bps at the close. This overshadowed a slightly hawkish ECB meeting where sources later suggested that the ECB are inclined to keep rates on hold in this cycle unless there is an economic shock. Equities extended their recent rally, with the S&P 500 (+0.85%), Nasdaq (+0.72%), and the Mag-7 (+1.13%) all notching fresh record highs.

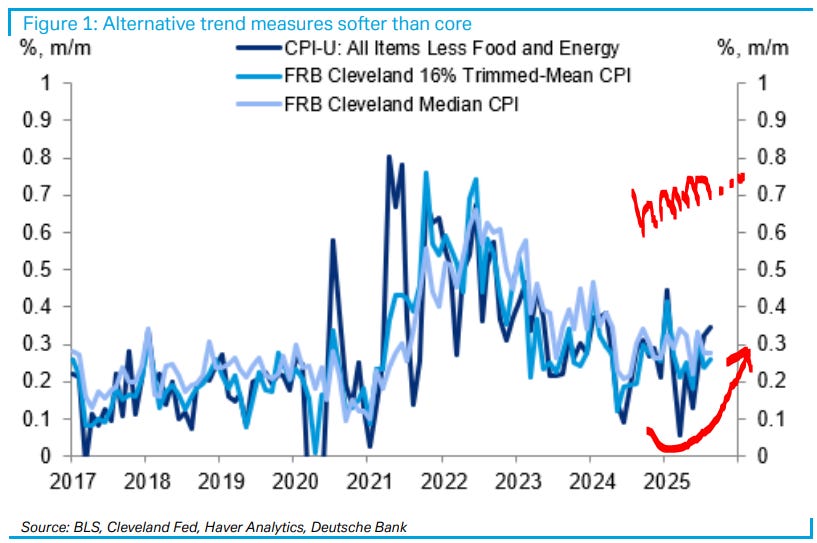

Starting with the US CPI report, headline inflation rose by +0.4% month-on-month (m/m) in August, up from +0.2% in July and above the +0.3% consensus forecast. Core inflation matched expectations at +0.3% m/m, unchanged from July but it did come in at 0.345%, just shy of rounding up. However, it was outsized increases in volatile categories such as airfares (+5.8% m/m) and lodging (+2.3% m/m) that pushed the core reading higher, with the Cleveland Fed’s trimmed mean CPI measure rising by a more moderate +0.26% m/m. Indeed, with airfares CPI not entering into the Fed’s preferred core PCE inflation measure, our US economists’ projection for August core PCE has declined to +0.22% m/m after the CPI print. Overall, they see the CPI data pointing to continued strength in service prices, but to potentially more moderate tariff impacts than previously anticipated. See their full take here

Alongside CPI, initial jobless claims for the week ending 6 September rose to +263k, well above the +235k expected. The state of Texas accounted for most of this increase so some of this spike was likely due to temporary distortions. Still, it was yet another data point adding to a picture of a softening US labour market.

The combined data prompted a rally in US Treasuries, with 10yr yields falling -6bps lower after the print before closing -2.5bp on the day to 4.02%. 30yr yields saw a larger -4.2bps decline, even as they sold off a little after an average 30yr auction. However, the front-end rally ran out of steam as the day went on and 2yr yields closed a mere -0.1bps lower as markets remained hesitant to price in much risk of a 50bps cut, with September Fed pricing unchanged at 27bps. The dollar index weakened slightly, posting a -0.25% decline…

…In response, markets effectively removed any pricing of an October rate cut, and are now pricing only 10 bps of easing by next March (-3.1bps on the day), which marks the first time that another 25bp rate cut has been less than 50% priced. That sent 2yr bund yields +3.3bps higher, though the 10yr yield (+0.4bps to 2.65%) was little changed amid the US bond rally…

11 September 2025 DB: August inflation recap: Hot core CPI but cooler core PCE

Both headline (+0.38% vs. +0.20% previously) and core (+0.35% vs. +0.32%) were marginally stronger (~2bps) than our expectations. The year-over-year rate for the former picked up two-tenths to 2.9% while the latter rose one-tenth to 3.1%. Shorter-term trends in core accelerated, with the three-month annualized rate increasing by eight-tenths (to 3.6%) and the six-month rate rising to 2.7% (from 2.4%).

As was the case in July’s data, monthly gains in trimmed mean (+0.26% vs. +0.24%) and median CPI (+0.28% vs. +0.28%) were slightly weaker than core, given the particularly large gain in airline fares. The year-over-year rate for the former ticked up a tenth (to 3.3%), while the latter remained roughly unchanged (at 3.6%).

In terms of the breakdown within the expenditure basket, core goods prices were strong again, increasing by +0.28% (vs. +0.21%). However, much of this was a function of larger gains in used cars and trucks and alcoholic beverage prices. Some goods which had previously shown strength because of tariffs moderated, while others have potentially begun to see tariff-related pass through into prices (e.g. apparel and new vehicles).

On the services side, airline fares and lodging away posted large gains, while owners’ equivalent rent spiked. The latter was largely geographically confined to smaller cities in the South, suggesting that the rise is more noise than signal.

Today’s CPI data and yesterday’s PPI data point to an 0.22% August gain in core PCE, which would have the year-over-year rate continue to round to 2.9%. On balance, the CPI data point to continued strength in service prices, but potentially more moderate tariff impacts going forward than we had previously expected. With respect to the Fed, the more muted read through to core PCE likely locks in a rate cut at next week’s meeting and could argue for further easing this year.

M2 growth slowing and compliant CPI so .. rate CUTS …

September 11, 2025 First Trust Data Watch - The Consumer Price Index (CPI) Rose 0.4% in August

…Implications: Inflation came in above expectations in August, with the Consumer Price Index increasing 0.4%, and the year-ago comparison climbing to 2.9%. “Core” prices, which strip out food and energy, rose a consensus expected 0.3%, while the twelve-month core comparison stood pat at 3.1%. Looking at the details of the report, the volatile energy and food categories led overall prices higher, with energy prices rebounding 0.7%. Notably, airline fares contributed the most to core inflation in August, with prices for the category jumping 5.9% after a 4.0% increase in July. Those are the two largest monthly increases for the airline fare since mid-2022. In the past year, the main driver of core inflation has been housing rents, which rose 0.4% in August. Other core categories to increase were prices for used cars and trucks (+1.0%), motor vehicle repair (+2.4%), and apparel (+0.5%). Meanwhile, the category for medical care dropped 0.2% in August, as both prices for prescription drugs (-0.2%) and nonprescription drugs (-0.9%) declined. In other news this morning, initial jobless claims jumped 27,000 to 263,000: the highest level since 2021. Meanwhile continuing claims remained at 1.934 million. These figures are consistent with a job market that is barely treading water in September, although the Labor Day holiday may have affected the report.Given the softening labor market and slow growth in the M2 measure of the money supply, we believe it’s time for the Fed to begin reducing short-term rates slightly in the months ahead, but cautiously. We expect the Fed to cut rates by 25 bps at the meeting next week. Yes, inflation remains above the 2% target. But tepid economic and job growth suggests monetary policy is tight and inflation will decline in the year ahead.

#GotInflation? #GotBONDS? What about Da FED …

11 September 2025 ING: US inflation remains hotter than hoped, but the Fed’s focus is now jobs

Inflation was a touch higher than expected and tariffs are likely to keep it elevated over coming months, but the the weakening of the jobs market is now the Fed's priority, with rising jobless claims hinting at a pick-up in lay-offs at a time when hiring is subdued

11 September 2025 ING Rate Spark: Bulls pushing down the back end

A hawkish ECB press conference helped our bearish case on 10Y swap rates, but markets will face resistance from the bullish momentum in the US. The US 10yr 4% level was breached twice, albeit briefly, on Thursday. It seems to be setting itself up for a break below. All it needs now is a solid excuse. Something like the buildup to a first rate cut in a year – maybe

Evidence of cooling consumer demand and a weakening jobs market is becoming more obvious. Inflation remains above target and tariffs are likely to keep it elevated in the near term, but the balance of risks are tilted towards the need for more support for the economy, starting with a 25bp cut on Wednesday, 17 September

Cuts to be faster or slower? SOME say slower and this next shop (long 5s) saying …

This week's CPI print translates to softer core PCE than we expected. Combined with the downside surprise in August's employment report, we think the Fed can move toward neutral faster. We now expect four consecutive 25bp cuts through January, followed by two more 25bp cuts in April and July.

Key takeaways

This week’s CPI print was firm at 0.35% m/m, but tariff passthrough effects were less pronounced. We now forecast core PCE for August at just 0.18% m/m.

Risks to the labor market have risen, with weaker payrolls and the vacancy rate slipping below 1.

Recent data warrant faster cuts towards neutral. We expect four consecutive cuts until the target rate is near upper estimates of neutral.

With potential residual seasonality in inflation in 1Q26, the pace slows after January. Cuts in April and July bring the terminal rate to 2.875%.

Exhibit 1: We now expect a faster cutting path, but with the same terminal rate of 2.875%

CPI. As expected and they told us so … and are sticking w/25bps call for next week …

11 Sep 2025 NatWEST: US Consumer Price Index (August)

The results of the August CPI report mostly matched our expectations though as always there were a few surprises within the details of the report (discussed below). The total CPI was up +0.4% (consensus +0.3%, NatWest +0.4%) in August, led by rebounds in the food (+0.5% after 0.0%) and energy (+0.6% after -1.1%) while the core CPI advanced by another 0.3% (consensus and NatWest +0.3%). The unrounded gain in the core CPI at 0.346% (NatWest +0.349%) was a bit firmer than the 0.322% print in July and above the H1(25) average monthly change of +0.221%. As expected, core goods prices ticked up by +0.3% (after +0.2%) while core services advanced by 0.3% (after 0.4%). On a y/y basis, the headline CPI edged up from 2.7% in July to 2.9% in August while the core CPI held steady at a six- month high of 3.1%…

…All that being noted, the weakness in core goods ex vehicles prices will feed through to the core PCE deflator with a larger weight while some of the strength in core services such as airfares will not feed through. This has pulled down our estimate for the August core PCE deflator to 0.2%m/m (from 0.3% we had after the PPI report), which if realized would leave the y/y pace steady at 2.9%. In any case, we don’t think the outturn of the August CPI report or its implications for the August core PCE deflator will alter expectations for a 25bp cut at next week’s FOMC meeting.

Covered wagons CPI recap / victory lap AND offering a flashlight …

September 11, 2025 Wells Fargo: August CPI: Dog Days of Summer

Summary The heat continues to gradually get turned up on inflation. Consumer prices in August came in a bit hotter than expected, with the CPI rising 0.4% versus consensus expectations for a 0.3% rise. Excluding food and energy, prices advanced 0.346%—in line with the consensus on a rounded basis but also a little stronger on an unrounded basis.

Goods inflation continued to pick up, posting its largest monthly gain since January. The initial burst of higher prices following increased tariffs this spring seemed to fade slightly in some categories like recreational goods and household furnishings, but a jump in vehicle prices over the month illustrated that upward pressure on goods prices from tariffs won't feed into consumer prices in a uniform fashion. It is also not just higher goods prices lifting inflation. Core services advanced 0.35% in August amid a rebound in travel-related prices and owners' equivalent rent.

For the FOMC, a core CPI reading of 0.35% and a three-month annualized rate of 3.6% is not what the Committee wants to see as it prepares to cut rates for the first time in 10 months. That said, as we have highlighted elsewhere, the downside risks to the labor market have grown considerably over the past couple of months, creating more urgency to act to keep the jobs market from falling apart. The FOMC also may take comfort in the more benign PCE inflation implications from today's CPI report and yesterday's PPI report. Taken together, we project that the PCE and core PCE deflators rose 0.26% and 0.22%, respectively, in August.

We suspect the broadening cost burden from tariffs will keep the monthly pace of goods inflation elevated through early next year, but the spillover into services inflation should be limited by the weakness in the jobs market, choosier consumers and anchored inflation expectations. As such, today's print does not alter our expectation for the Fed to cut by 25 bps at its September meeting next week and by 75 bps total by year-end.

September 11, 2025 Wells Fargo: Flashlight for the September FOMC Blackout: Cuts to Begin Again

Summary

We expect the FOMC to resume lowering the fed funds rate at its September meeting with a 25 bps rate cut that would bring the policy rate to a range of 4.00%-4.25%.

A more precarious picture of the labor market has become apparent since the FOMC last met in July. The three-month average pace of payroll gains is now reported at just 29K compared to 150K when the FOMC gathered in July. Furthermore, the unemployment rate has moved up to a cycle-high of 4.3%, putting it at the top end of the FOMC’s range consistent with “full employment.”

Additional policy easing this year has been delayed due to inflation. Reflation in the goods sector alongside slower services disinflation has kept core PCE running about one percentage point above the 2% target. That said, the outlook for inflation has been little changed over the past six weeks. Our own forecast looks for core PCE to rise 3.1% on a Q4/Q4 basis this year, the same as before the July FOMC meeting.

We think the meeting statement will mark down the FOMC's current view of the labor market but refrain from signaling that additional rate cuts will immediately follow September’s cut. This would give the FOMC the flexibility to reduce the policy rate again at its next meeting on October 29 or proceed with additional easing more slowly.

We expect the updated dot plot to signal more easing through the remainder of this year and next (Table). The composition of the Committee looks set to tilt in a more dovish direction with Stephan Miran on track to be confirmed prior to the meeting. However, the more significant driver of the revision, in our view, is the combination of increased risk to full employment and the generally stable inflation outlook. We think the median dot for 2025 will move down to project 75 bps of cuts compared to 50 bps of cuts in June. For 2026, we anticipate the median dot will fall 50 bps from the June SEP projection of 3.625% to 3.125%, implying an additional 25 bps cut next year. We do not expect any changes to the median longer-run estimate.

Our base case forecast for the federal funds rate is three 25 bps rate cuts at the three remaining FOMC meetings of the year, followed by two 25 bps rate cuts at the March and June FOMC meetings before a prolonged hold at 3.00%-3.25%. For further reading on our fed funds projections and broader economic outlook, see our recently released monthly economic outlook.

Finally, Dr Bond Vigilante conjuring up Shakespeare … and at same time, INCREASING S&P f’cast and joining the 7k club as he also thinks ONLY 25bps …

Sep 11, 2025 Yardeni: 25 Or 50 To Be Or Not To Be?

Following yesterday's cooler-than-expected PPI and today's as-expected CPI, expectations are that the FOMC will cut the federal funds rate by 25 basis points on September 17, with no dissenting votesamong voting members. Following today's jump in last week's initial unemployment claims, meeting participants might consider a 50-basis-point cut, but we doubt that they will opt for that, as the majority would likely dissent. Instead, the committee might signal the likelihood of more rate cuts in its Summary of Economic Projections.

Speaking of projections: We are raising our year-end S&P 500 target from 6600 to 6800. That’s our base-case scenario with a subjective probability of 55%. We currently assign a 25% subjective probability to a meltup that lifts the S&P 500 to 7000 by year-end 2025 and 20% odds to a correction in the index by the end of this year. If the Fed lowers the federal funds rate on September 17 and signals more rate cuts ahead, we will increase our odds of a meltup and decrease our odds of a correction.

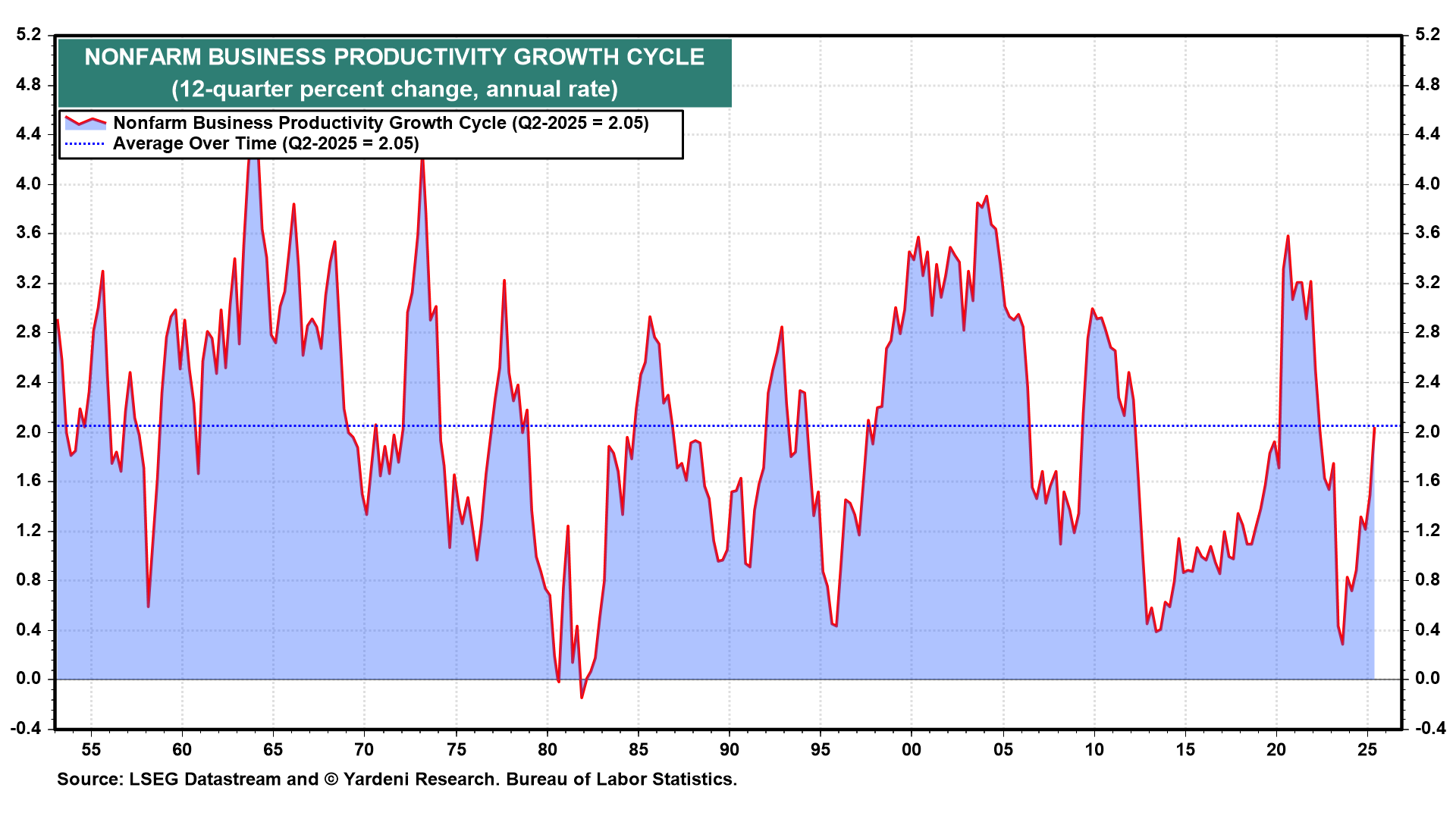

We are still not convinced that the economy needs to be stimulated by the Fed. Inflation remains closer to 3.0% y/y than to the Fed's 2.0 target. Real GDP is growing solidly despite the recent downward revisions in payroll employment. The unemployment rate remains between 4.0% and 4.3%. All this implies that either real GDP will weaken significantly and the jobless rate soon will rise sharply, or that productivity growth is making a strong comeback. We pick Door #2!

Consider the following:

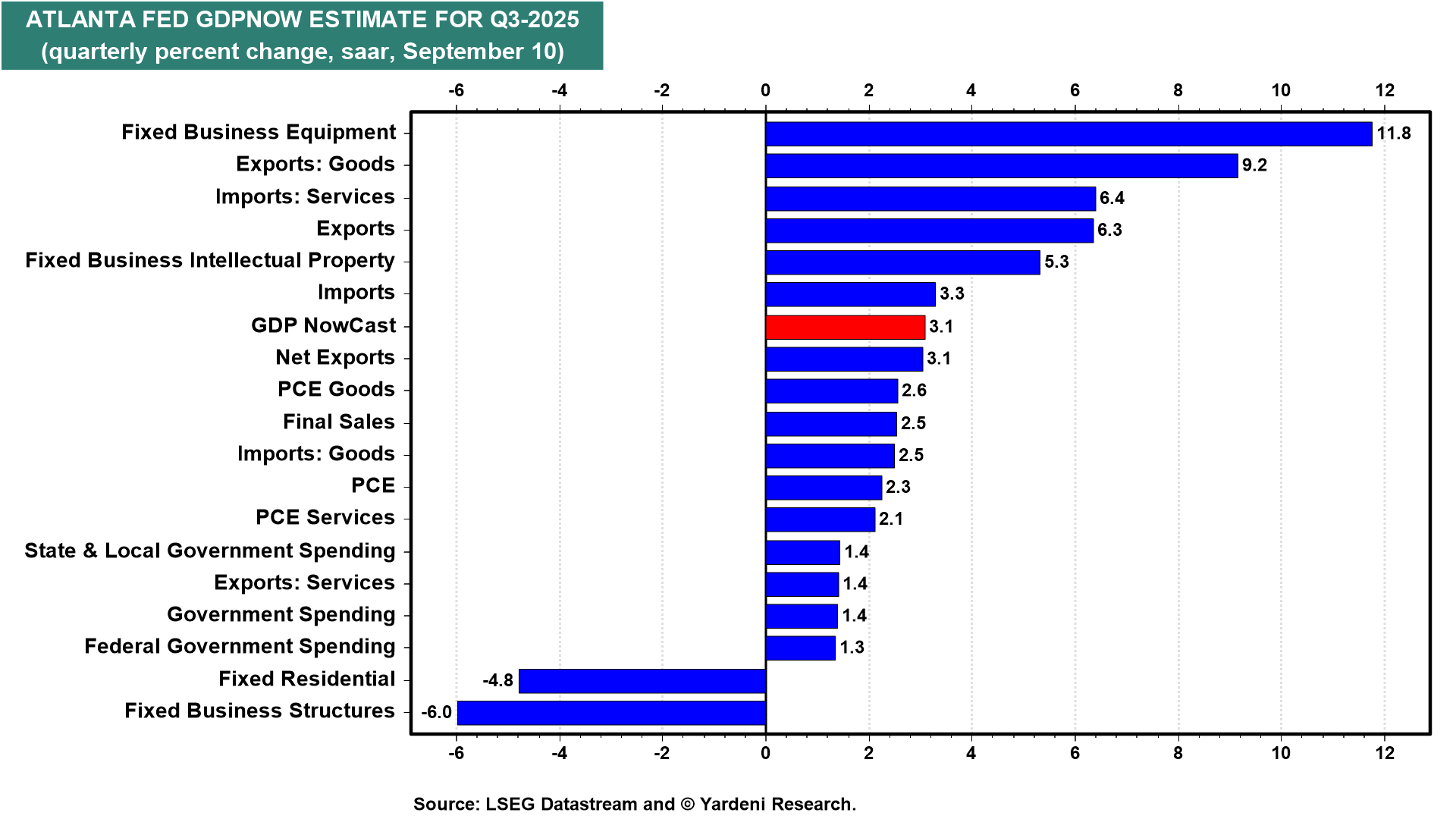

(1) GDP. Yesterday, despite August's weaker-than-expected employment report, the Atlanta Fed's GDPNow model estimated that real GDP rose 3.1% (saar) during Q2, up from 3.0% on September 4 (chart). Capital spending on equipment and exports are robust. Consumer spending is solid at 2.3%. Real GDP was up 3.3% during Q2.

(2) Labor market. Initial unemployment claims jumped 27,000 last week to 263,000 (seasonally adjusted), the highest reading so far this year (chart). This number could persuade a few FOMC participants to press for a 50-basis-point rate cut. So far, it is only a one-week spike, which has occurred occasionally in the past. In addition, 15,000 of the increase (not seasonally adjusted) occurred in Texas. That seems like a one-time aberration, unless a large number of oil field workers were let go last week.

(3) Productivity. Strong GDP growth, coupled with a seemingly weak labor market, suggests that productivity growth must be robust. Over the past 12 quarters, productivity growth has averaged 2.1%, precisely the same as its average over time. In our Roaring 2020s scenario, we expect growth to approach 3.0% over the remainder of the decade.

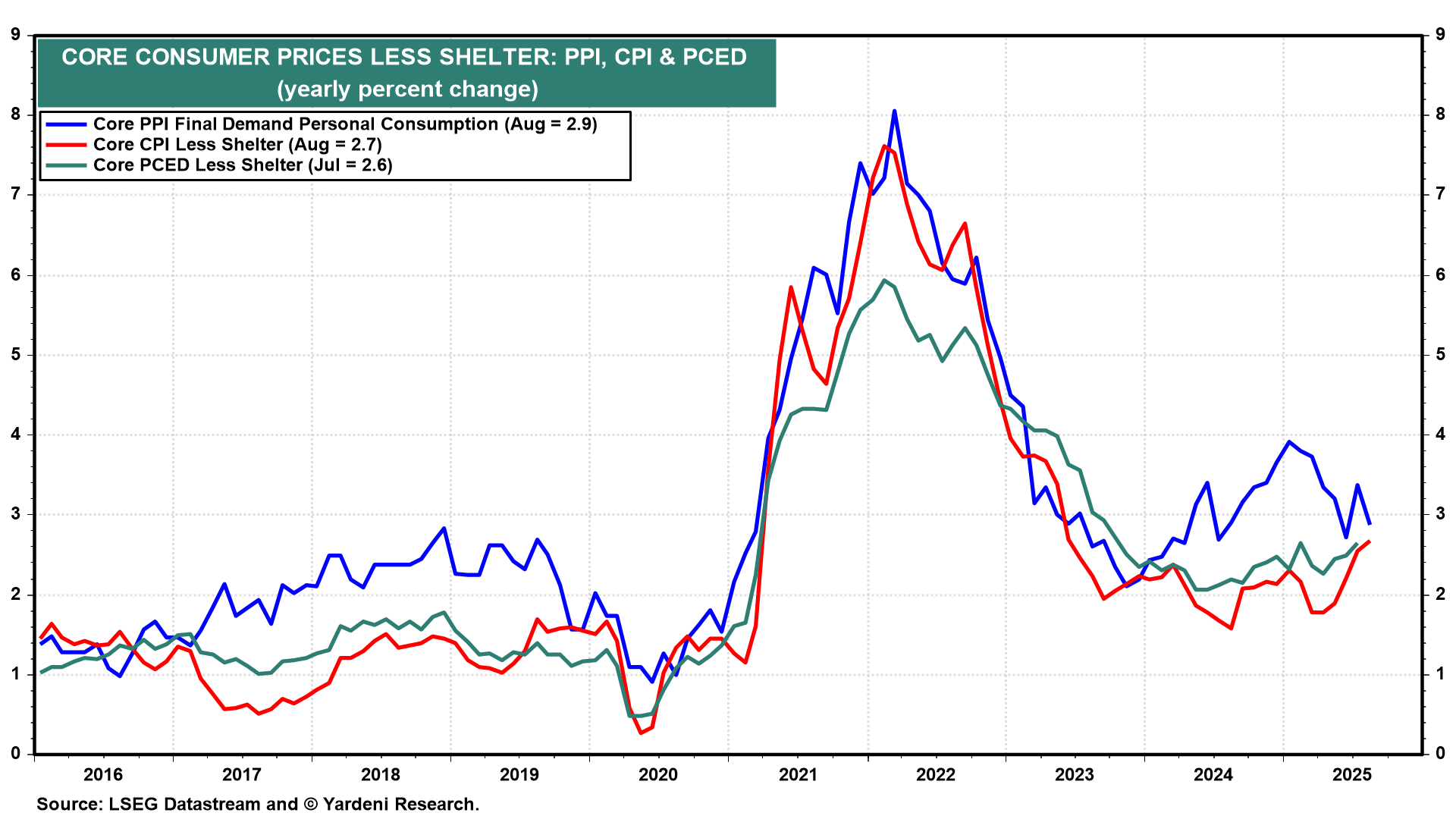

(4) Inflation. Meanwhile, the core CPI, core PCED, and core PPI for consumption—all excluding shelter—are closer to 3.0% than to 2.0%, as noted above (chart).

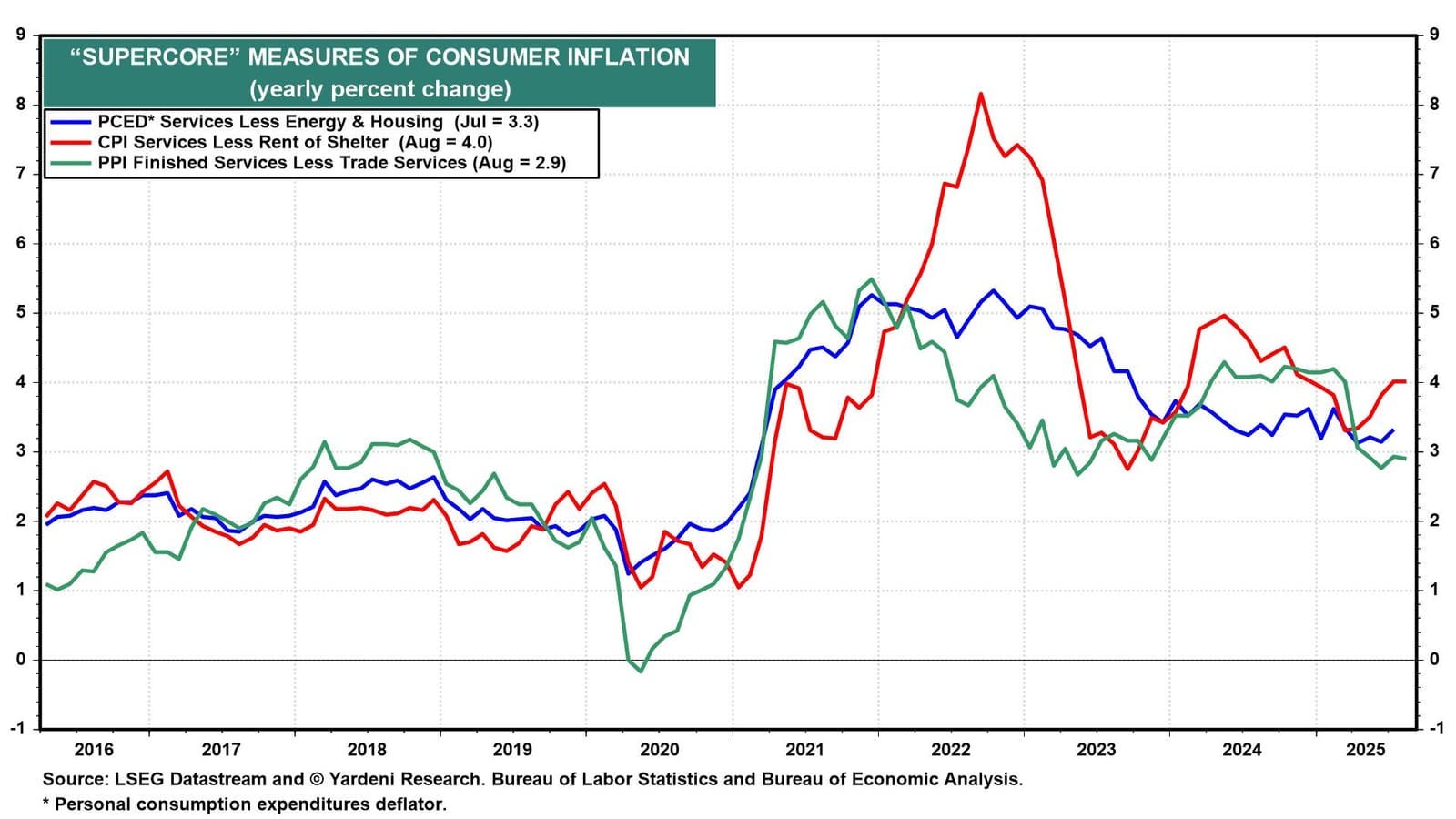

Trump's tariffs have caused a slight increase in durable goods inflation. That is likely to be a transitory problem. A stickier problem is that measures of the "supercore" inflation rate remain sticky between 2.9% and 4.0% (chart).

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Terminal SAYS …

September 12, 2025 at 9:40 AM UTC Bloomberg: Traders Lock In Fed Bets, Boosting Treasuries for Fourth Week

Treasuries were set to extend their rally into a fourth week after Thursday’s jobless claims data cemented expectations the Federal Reserve will cut interest rates next week.

The yield on US 10-year debt edged two basis point higher to 4.04% after falling to a five-month low Thursday, but still remained on course for a fourth week of declines, the longest streak since February. The more rate-sensitive two-year rate edged up to 3.55%.

With a quarter-point rate cut next week fully priced in, focus now shifts to the pace of easing for the rest of the year. US President Donald Trump has been vocal about his preference for much lower interest rates, but until yesterday, traders were more cautious. Now money markets are assigning an 80% chance of two further cuts by year-end.

“Given the weakness of the jobs market, we believe the Fed will feel obliged to act with or without political pressure,” Vincent Mortier, chief investment officer at Amundi SA, said on Bloomberg TV. “We are still expecting three cuts this year.”

Amundi is positioned for the Treasury yield curve to steepen, led by the short-end. Others are more cautious, with Allianz and Pimco saying they used the recent rally to pare back some curve risk.

This week’s jobless claims numbers eclipsed the August inflation numbers, which at 2.9% matched economists’ estimates. The Fed’s preferred gauge is expected to maintain a similar 2.9% pace when the August figures are published at the end of the month.

… and they call ME Capt Obvious … and another nasty CPI surprise …

Sep 11, 2025, 3:54 PM WolfST: CPI Inflation Dishes Up another Nasty Surprise, as it Tends to Do

Fed’s Nightmare, but it’ll cut anyway: CPI, Core CPI, and Core Services CPI all over 4% annualized. Goods prices spiked for Used Vehicles, Food, Gasoline.

Core services, which dominate the inflation index and include many of the essentials that consumers cannot do without – housing, healthcare, insurance, etc. – rose by 4.3% annualized in August from July, the second month in a row over 4%. In goods, the biggie was the spike in used-vehicle prices, continuing a year-long trend. Food and gasoline prices jumped…

Finally, did you know am striving to achieve full MARKET ANALYST designation which will clearly make this note more readable and of value to one and all …?

I thought it was a joke at first....RIP Charlie Kirk

https://www.zerohedge.com/news/2025-09-11/russia-exposes-us-plot-dump-37t-debt-crypto-reset

Please give me your thoughts and opinions on this, Steve and Anthony or anyone else.