while WE slept: USTs pushed lower; GOLD; Fiscal Fears Grip Traders; G7 curves STEEPER; CC spending perked up; buy dips (MS on stks); WEAK Sept seasonals for long bonds

September 2, 2025 at 8:35 AM UTC Bloomberg: Stocks and Bonds Fall as Fiscal Fears Grip Traders: Markets Wrap

Stocks fell alongside bonds, driven by concerns over government finances and lingering inflation risks at a time when equities are hovering near all-time highs.

Futures for the S&P 500 retreated 0.5% as Wall Street returned from a long weekend, building on the tech-driven selloff that closed out last week. Europe’s Stoxx 600 fell 0.6%. Gold briefly topped $3,500 an ounce, fueled by mounting bets on rate cuts and unease about the Federal Reserve’s independence.

Global bonds staged a broad retreat, led by sharp declines in longer-dated debt. The yield on 30-year Treasuries climbed four basis points to 4.97%, while their UK counterparts hit the highest since 1998 amid Prime Minister Keir Starmer’s struggle to restore market confidence. The pound led losses among major currencies as the dollar headed for its first advance in six days….

… and as current market machinations don’t fit the F2Q narrative, it’s worth looking a bit beyond my normal lane …

Sep 2 2025 Reuters/CNBC: Gold races to all-time high above $3,500 on U.S. rate cut prospects

…“Gold’s rally is set to be heavily influenced by how much the Fed’s rate-cutting path adheres to market projections,” said Han Tan, chief market analyst at Nemo.money…

…Traders are currently pricing in a 90% chance of a 25-basis-point Fed rate cut on September 17, according to the CME FedWatch tool. Non-yielding gold typically performs well in a low-interest-rate environment…

… And so it seems all things are going to be won and lost on rate cuts bets. Place your bets and take it to the bank. Wondering if there’s any sort of consequence?

Maybe, just maybe as that old saying goes … NOTHING happens without consequence and perhaps one only need to look further out the curve (and the reason for it’s steepening …

The longer-end of the curve seems very topical (see below for MORE on upcoming poor seasonals), a quick look at 30s as the new month gets under way …

… momentum has adjusted and now leaning heavily overSOLD so it would seem to ME folks were prepared for this and at some point it will become overDONE and so, longer-dated bonds become a rental OR fiscal authorities lose control and things go from bad to worse … for NOW and on into September seasonally weakspot, one could not be blamed to be on hunt for dip-OR-tunties …

#GotBONDS?

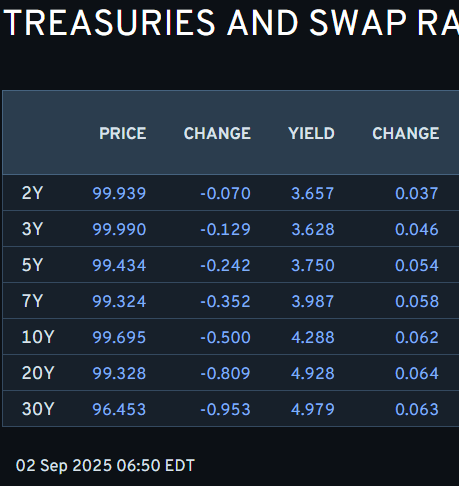

We’re at / very near (20bps is nothing in the Land of the BIG 01s) interesting levels and ahead of them and this weeks ending employment report, a snapshot OF USTs as desks in the US get back at it … USTs as of 650a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: DXY soars as GBP & JPY sinks, US equity futures also lower into ISM Manufacturing PMI … USTs are also lower, following peers. Overnight focus was on trade and Fed commentary from US officials. Firstly, Treasury Secretary Bessent said they are confident the Supreme Court will uphold Trump’s tariffs and highlighted that there are other ways of justifying tariffs. On the Fed, Bessent said we haven’t seen anything yet’ regarding the market reaction to President Trump’s pressure on the Fed, and believes there is a good chance Miran is in place before the September FOMC. USTs lower by 11 ticks at most, holding just off lows in a 112-05 to 112-16 band. Focus for the day is on any further trade updates, developments on Fed’s Cook (court document submission deadline) and ISM Manufacturing.

Reuters Morning Bid: Dollar, gold and long yields surge

…Today's key chart

Graphics are produced by Reuters.

As government budget season looms in Europe and anxiety about U.S. debt loads and central bank independence linger stateside, long-term public borrowing rates are climbing and the so-called yield curve gaps between 2-year maturities and 30-year tenors is widening to reflect much of that long-term uncertainty. French and British yield curves are now at their steepest since 2017 and the U.S. curve is at its steepest since 2021…

Our credit card data show that, with the exception of recreation, spending growth has sustained or exceeded prior years' momentum into August. Measures still imply a softening longer-term trajectory , but less so than in our June report, implying that the level of spending is on a lower trajectory…

… helping corporate earnings, they say, drive markets and so …

Strong 2Q25 results flowing through to FY estimates, but still dependent on a handful of sectors; 2H revisions look like they're baking in tariff impacts; valuations not cheap, but not extended either; NLP analyses point to still-high tariff/pricing concerns, but moderated from last quarter.

Earnings season comes through with strong headline numbers: EPS growth at +10.6%, sales growth at +6.1%, breadth and depth of surprise all come in above LT trend. Beats were helped by estimates getting too bearish into the print, which likely guided share price reactions (misses were punished more than beats were rewarded).

Below the line, earnings power remains dependent on a handful of sectors... TMT (especially Big Tech) and Financials remain the primary source of SPX EPS growth, margin upside and operating leverage. Other sectors printed weaker numbers, especially Consumer ex-AMZN, Materials and Utilities, which lagged their LT EPS growth cadence this quarter by the widest margin.

...as do revisions to forward EPS. Street FY25 SPX EPS went to $268 from $264 a quarter ago fueled by Big Tech, Industrials and Financials; meanwhile, Consumer ex-AMZN, Utilities and Healthcare detracted. Zooming in on 2H revisions compared to history, estimates look like they're baking in materially negative tariff flow-through for some industries, DC/AI upside for others.

SPX P/E has been rangebound between 22-22.5x since CQ2 end, a level that we highlighted in prior work as not necessarily a headwind for performance. Big Tech, the main engine of SPX EPS growth, is trading at ~29x NTM EPS, still down from YE24 levels and below its LT average premium to SPX. Industrials and the rest of Tech look extended by comparison.

NLP analysis of earnings transcripts suggests that tariff concerns remain elevated, although discussions have moderated Q/Q. In a similar vein, the share of executives talking about "pricing" or "pushing through" of prices declined Q/Q, as did references of consumer value-seeking behavior; our takeaway is that companies do not seem to more broadly plan on price increases compared to last quarter - at least there was less talk to this end. Also, executives seem to view inventory levels more favorably than in the previous quarter, with fewer mentions of "high" inventory and more of "competitive." We think this supports the narrative that peak tariff uncertainty has likely passed and mitigation efforts (such as inventory pull-forward) have yielded some results, but also that trade/macro uncertainty are still top of mind for company management—one notable uptick was discussions of "tariffs" in the context of "next year."

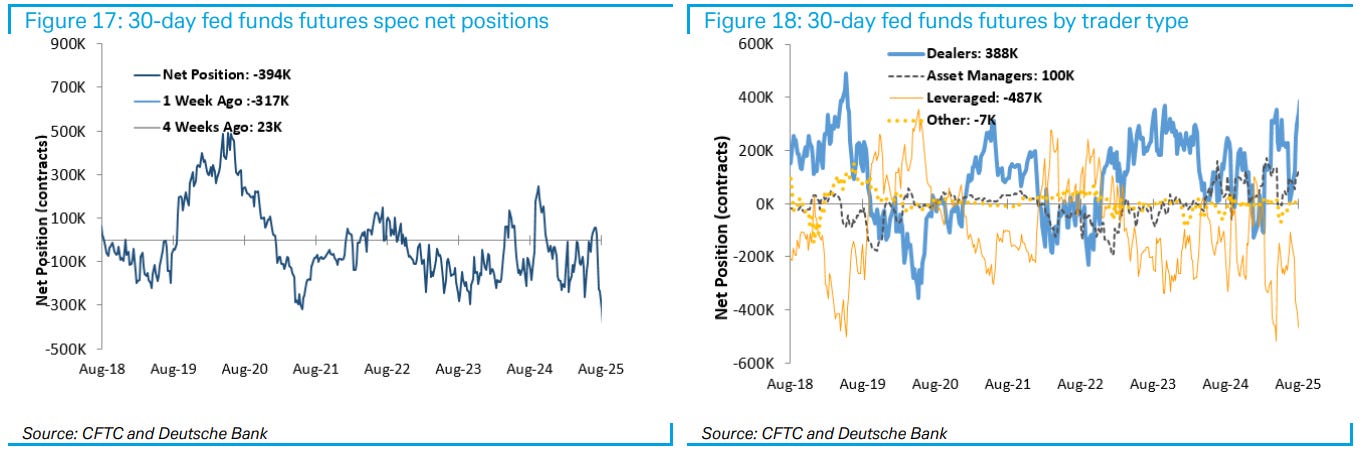

You say RECORD SHORT position and regardless of who and what, I stop to slow down and read …

…Fed Funds Futures: Speculators offloaded 77K 30-day federal funds contracts to extend their net short positions to record -394K contracts.

… Same shop with an early morning read thru of markets as global BOND markets making waves, offering direction for ALL sorts of mkts as the USA only slowly getting back online after holiday weekend …

… Today marks the start of the final stretch of the year as the US returns from yesterday’s Labor Day holiday. While the US was out, European markets traded on familiar themes, with long-end bond yields creeping higher amid ongoing fiscal concerns. Yields on 30-year German, French, and Dutch bonds reached their highest levels since the Euro crisis in 2011, while the UK’s 30-year gilt yield hit its highest since 1998. Even in orderly markets, we’re seeing a slow-moving vicious circle: rising debt concerns push yields higher, worsening debt dynamics, which in turn push yields higher again.

The immediate catalyst has been the upcoming no-confidence vote in the French government, scheduled for Monday, 8 September. French 10-year yields rose 2.5bps to 3.53% yesterday—their highest since mid-March—despite no fresh news. Enough parties in the National Assembly still say they’ll vote against the government, so we may be heading for another collapse, similar to what happened to Michel Barnier last December. Investors fear that more political paralysis will make fiscal tightening harder, which is worrying given France’s current deficit levels.

But it wasn’t just France. Yields rose across the continent: 10-year bunds (+2.2bps), OATs (+2.5bps), and BTPs (+2.2bps) all moved higher. In the US, although markets were closed, Treasury futures lost ground across the curve. In Asia, 10-year US Treasuries are up +1.7bps. Rate cut expectations have been dialled back slightly, with the amount of Fed cuts priced by December 2026 falling -3.7bps to 136bps over the last 24 hours. Japanese yields have partly bucked the international trend this morning with the strongest 10 year auction since October 2023 helping yields dip -1.4bps. However, 30 year yields have followed their international peers and are up +1.7bps in Asia trading, hovering around their highest ever yield since they were first issued in 1999. This is ahead of a 30 year auction on Thursday…

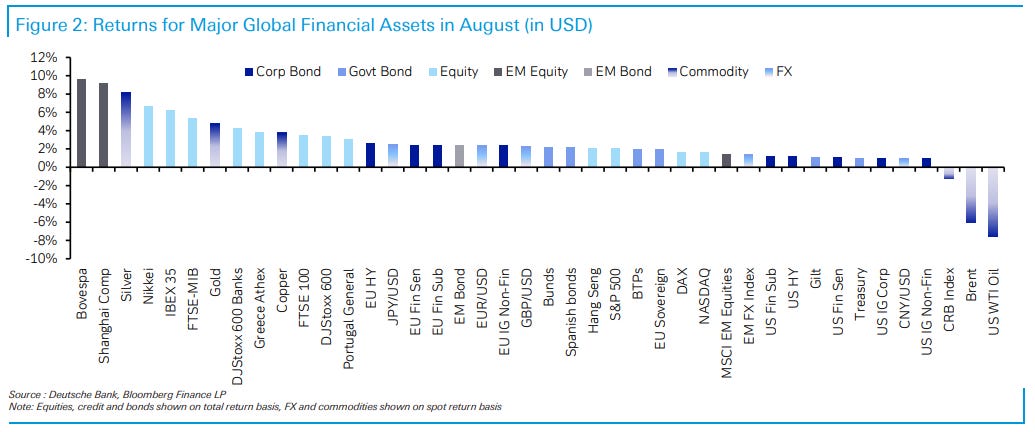

… that in mind, a review of markets performance for August …

1 September 2025 DB: August 2025 Performance Review

August was an eventful month for markets, with several competing narratives to digest. It began with a risk-off move as the August 1 tariff deadline passed, which was then followed up by an underwhelming US jobs report that revived fears about a slowdown. But markets soon recovered, and the S&P 500 continued to hit fresh records as it posted a 4th consecutive monthly advance. In large part, that was because of a dovish pivot by Fed Chair Powell at Jackson Hole, which led to growing expectations that the Fed would cut rates in September. Nevertheless, there were still several headwinds, including concern about the Fed’s independence that led to higher inflation expectations and steeper yield curves. Meanwhile in France, the upcoming confidence vote led to a fresh reappraisal of sovereign risk in Europe, and their 10yr yield moved closer to Italy’s than at any time since 2003…

…Which assets saw the biggest gains in August? …US Treasuries: Overall, August was a good month for US Treasuries thanks to a strong rally at the front end. Indeed, the 2yr yield fell -34bps on the month to 3.62%, marking its biggest monthly decline since August 2024, whilst the 10yr yield saw a smaller -15bps move to 4.23%. In total return terms, that left Treasuries up +1.0% for the month…

Some like it HOT HOT HOT … so naturally, equity markets remain IN FAVOR … buy dips (despite seasonals) … WHY? Largely because … rate CUTS …

We push back on the idea that rate cuts are already priced as equity returns tend to be strong during rate cutting cycles, and rate-sensitive areas like small caps are barely off the relative lows. We're respectful of the upcoming weak seasonal window, but remain buyers of dips should they come.

More Clarity on Fed Cuts...At Jackson Hole, Chair Powell appeared to confirm what the bond market was pricing—a September start to Fed rate cuts. The initial, positive reaction in equities to this policy development wasn't surprising, though stocks have largely consolidated those gains since August 22nd. The questions from here are what's in the price, what will drive the next leg higher into '26, and what are the risks in the short term.

Equity Returns Are Strong During Rate Cutting Regimes...While the bond market is already pricing ~5 cuts by year-end 2026, our work shows that equities typically deliver strong performance during Fed cutting environments. Further, valuation tends to remain supported when the policy rate is being reduced and earnings growth is above the long term median. This is our expectation for stocks over the next 12 months.

Run It Hot...The correlation between equity returns and inflation breakevens has risen significantly in recent months. While this policy environment is unique in many ways, a strong, positive correlation between equities and breakevens is very typical of an early cycle set-up—the backdrop we believe we're heading into today. It's also a potential indication that the equity market is focused on the administration's apparent desire to let nominal growth run hotter as the Fed cuts rates at the same time. This is a classic reflation strategy and similar to what we experienced during President Trump's first term.

What Are the Risks? This policy maneuver is not without risks, and we're heading into a weak seasonal window for stocks over the next 6-8 weeks. One potential risk scenario would be hotter inflation data in the near-term that reduces the magnitude of expected rate cuts. Another would involve a significantly negative payroll number and/or +0.2% upside in the unemployment rate that resurfaces growth concerns. In our view, this latter outcome would end up being bullish for stocks after an initial period of volatility. The reason is we think it would increase the magnitude of expected cuts and accelerate the early cycle transition from the trough of the rolling recession we believe occurred in April. While these risks are worth acknowledging and potentially trading, we remain buyers of dips and think any tactical consolidation would set up a strong finish to the year should it play out.

…it would appear as though the administration wants to let the economy run hotter, while the Fed cuts interest rates at the same time. Equities are not only an inflation hedge, but also tend to act well in Fed cutting backdrops as noted above. This is likely why the correlation between equity returns and inflation breakevens has risen dramatically in recent months (Exhibit 3). While this policy environment is unique in many ways, a strong, positive correlation between equities and breakevens is very typical of an early cycle set-up as Exhibit 3 shows. As discussed in recent weeks, we believe we're transitioning to an early cycle backdrop today—one where the nominal earnings growth environment strengthens and the Fed is cutting rates. Price action since April strongly supports our core view that Liberation Day marked the trough of the rolling recession that we believe began in 2022 with the pay-back in the initial surge of COVID-related demand. Since then, many sectors have been mired in a de facto recession as further evidenced by the very narrow equity market performance and unbalanced earnings growth/revisions across wide swaths of the market. Most notably, housing, consumer goods, manufacturing, and certain areas within commodities have seen anemic or outright negative growth at times over the past 3 years…

Exhibit 3: A Strong Positive Correlation Between Equity Returns and Inflation Breakevens Is a Typical Early Cycle Development

Gold prices hit a new record overnight. The gold rally has its foundations in central bank accumulation. Central banks that hold gold still hold a dollar reserve asset (just one that is independent of US Treasury control). That foundation has been built on with expectations of US rate cuts.

US President Trump is to deliver an Oval Office statement today. There are a number of topics the president may choose to address, and a number of directions that may be taken on each of those topics. Uncertainty about policy has economic consequences—relevant as markets consider the next employment report on Friday…

…US data is mainly business sector sentiment (and some construction spending). Things like prices paid and employment intentions attract attention in the sentiment figures. However, the actual importance of these figures depends on whether the observer believes the survey responses accurately reflect reality.

Covered wagons on REVISIONS to an important set of data …

September 2, 2025 Wells Fargo: Re-Point of Origin: The 2025 Preliminary Benchmark to Payrolls

The first look at the 2025 benchmark revision to nonfarm payrolls is likely to show that job growth was flying at a lower altitude even before the July employment report's eye-catching monthly revisions. How much closer to the ground have payrolls been flying, and what could that mean for the FOMC's interpretation of the jobs market?

Summary

Concerns about the labor market have been fanned by July's eye-catching downward revisions to payrolls. Those concerns are unlikely to be eased by the first look at the 2025 benchmark revision to employment, which we expect will show job growth was already flying at a lower altitude.

On September 9, the BLS will release its preliminary benchmark revision of the non-seasonally adjusted level of payrolls for March 2025. Based on the Quarterly Census of Employment and Wage (QCEW) data available through the end of 2024, a preliminary revision of -475K to -790K jobs strikes us as reasonable, which would rival last year's downward adjustment (-598K). This range equates to payroll growth in the 12-months through March 2025 averaging 83K to 110K versus 149K as currently published.

The likely overestimation stems from a variety of sampling and nonresponse errors inherent in surveys. While difficult to isolate, a few potential sources stand out:

Although the "birth-death" factor has been less generous this past year, we still see scope for overestimation given that data on business openings show the rate of net new firm creation has fallen below its pre-pandemic pace.

The establishment survey's overall response rate averaged 43% in the 12-months through March 2025, down from 59% in 2019. The falling response rate leaves greater room for firms who are responding to be systematically different from the non-respondents.

The primary source for the benchmark revision, the QCEW data, is based on tax filings for unemployment insurance. Its employment count is more prone to exclude undocumented workers since they are not legally eligible for these benefits versus the more informal payroll survey which simply asks for the total count of employees.

This year's benchmark revision appears somewhat less fraught than last year's due to the unemployment rate moving sideways since last July. Slower growth in the labor supply means that the economy does not need to be adding as many jobs to keep slack from building, as the "breakeven" rate of employment growth has fallen. Yet, with the benchmark revision likely to show a weaker pace of job growth through March, a loss of momentum at the beginning of the year would cast a shadow on the true strength of payroll growth since then. In short, even as the labor market is still standing, its footing is becoming more tenuous.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Anyone ELSE experience this …

September 1, 2025 Apollo: Expensive Labor Day Steaks

The price of steaks is rising rapidly. Live cattle prices have nearly doubled over the past five years and are at all-time highs, largely due to the US cattle herd being at its smallest size in decades, driven by years of drought and high feed costs, see chart below.

… Guessing I was NOT alone …

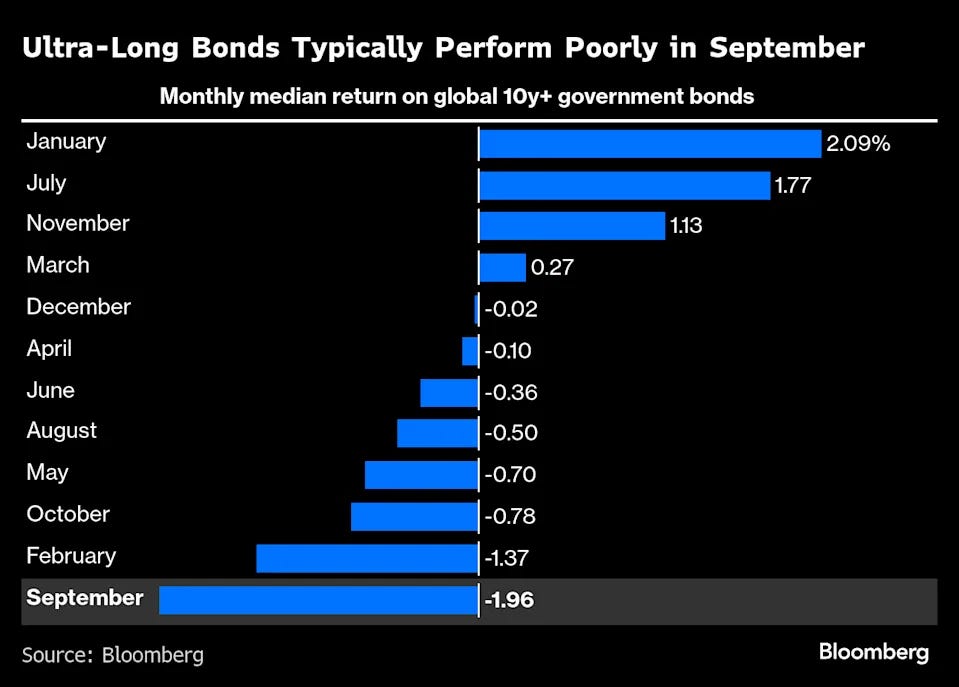

Terminal dot COM has an important note / visual for all marginally attached to the global LONG bond market …

September 2, 2025 at 4:49 AM EDT Bloomberg: World’s Long-Dated Bonds Face a Traditionally Terrible Month

(Bloomberg) -- Longer-maturity bonds may be in for a treacherous September, if history is any guide.

Over the last decade, government bonds globally with maturities of over 10 years posted a median loss of 2% in September, according to data compiled by Bloomberg. That’s the worst monthly performance of the year.

That trend will worry bond investors, with the longest-dated debt already lagging behind shorter maturities this year on concern governments will ramp up borrowing to fund spending pledges. What could worsen it is sticky inflation in Japan, political turmoil in France, and speculation that US President Donald Trump may push the Federal Reserve to cut interest rates, amplifying price pressures stateside.

“The market right now feels downright unpleasant,” said Hideo Shimomura, senior portfolio manager at Fivestar Asset Management Co. in Tokyo. “September is often when monetary policy takes a sharp turn,” and a month when positioning in anticipation of moves often shows up, he said.

The vulnerability of long-dated government debt reflects years of heavy issuance to fund public spending, exacerbating budget deficits. The concerns are particularly acute in the US, where Trump’s tax-cut and spending bill is forecast to add $3.4 trillion to deficits over the long-term, as well as in the UK and France.

Long-dated bonds were under pressure again Tuesday. The US 30-year yield rose to near 5%, while its UK peer hit the highest since 1998. The equivalent rate on French notes rose six basis points to 4.51%.

“Even in orderly markets, we’re seeing a slow-moving vicious circle: rising debt concerns push yields higher, worsening debt dynamics, which in turn push yields higher again,” Jim Reid, global head of macro research and thematic strategy at Deutsche Bank AG, wrote in a note.

European Central Bank policymaker Isabel Schnabel told Reuters in an interview that borrowing costs globally may start to be lifted sooner than anticipated, citing high government spending as one of the main reasons.

Near-Term Hurdles

US payrolls data on Friday poses a near-term risk for the market as traders wait to confirm bets on a Fed rate cut this month. Euro-zone inflation data is also on traders’ radar as they watch for any potential surprise, with policymakers widely seen keeping rates steady next week…

ALSO from The Terminal … All that glitters is … because of rate CUTS BETS and how awful the economy is (about to become?) …

September 2, 2025 at 3:28 AM EDT Bloomberg: Gold Punches Through $3,500 to Hit Record on Rate-Cut Bets

(Bloomberg) -- Gold hit a record as the prospect of US Federal Reserve rate cuts and growing concerns over the central bank’s future gave fresh legs to the multiyear rally in precious metals…

…The latest run has been fueled by expectations the US central bank will lower interest rates this month, after Fed Chair Jerome Powell cautiously opened the door to a reduction. A key US jobs report this Friday is likely to add to signs of an increasingly subdued labor market — supporting the case for cuts. That’s boosted the allure of precious metals, which do not pay interest.

“Investors adding to gold allocations, especially as Fed rate cuts loom, are pushing prices higher,” UBS Group AG strategist Joni Teves said. “Our base case is that gold continues to make new highs over the coming quarters. A lower interest rate environment, softer economic data and continued elevated macro uncertainty and geopolitical risks boost gold’s role as a portfolio diversifier.”

Both gold and silver have more than doubled over the past three years, with mounting risks in the spheres of geopolitics, the economy, and global trade driving increased demand for the time-honored haven assets. An escalation in President Donald Trump’s attacks against the Fed this year has become the latest cause for investor alarm, with concerns over the central bank’s independence threatening to erode confidence in the US…

… finally, was that YOUR dog chasin’ me over weekend …