while WE slept: USTs pulling back; "A lower low in 10y yields" (CitiFX), stock jockeys (MS) watchin' Fed and bonds and, "The Great Rate Divide" (10s and FFs)

Good morning … Opening Bell Daily (Phil Rosen) just below led this morning with this one titled, ‘Bull Wipeout’ …

On heels of a ‘robust’ note over the weekend recapping and victory lapping with regards to NFP and Wall-E commentary, offering a somewhat longer-term (weekly) look at 10s alongside a look at the DAILY chart, this mornings note may seem more focused on stonks than is necessary.

I will only say that in times like these, bonds are acting as one would think bonds SHOULD — catching that F2Q bid and being that ‘safety valve’ as planned by those who came up with the idea of the ‘60/40’ portfolio.

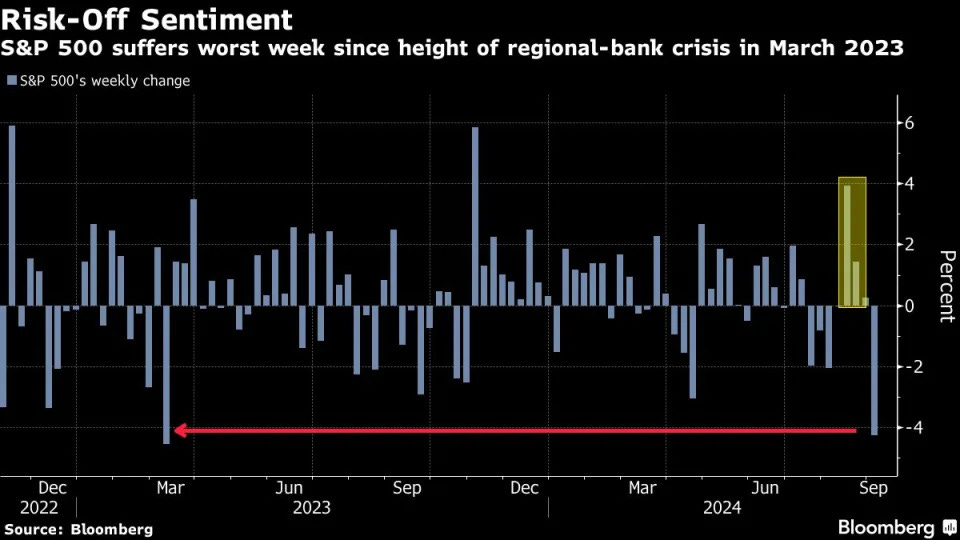

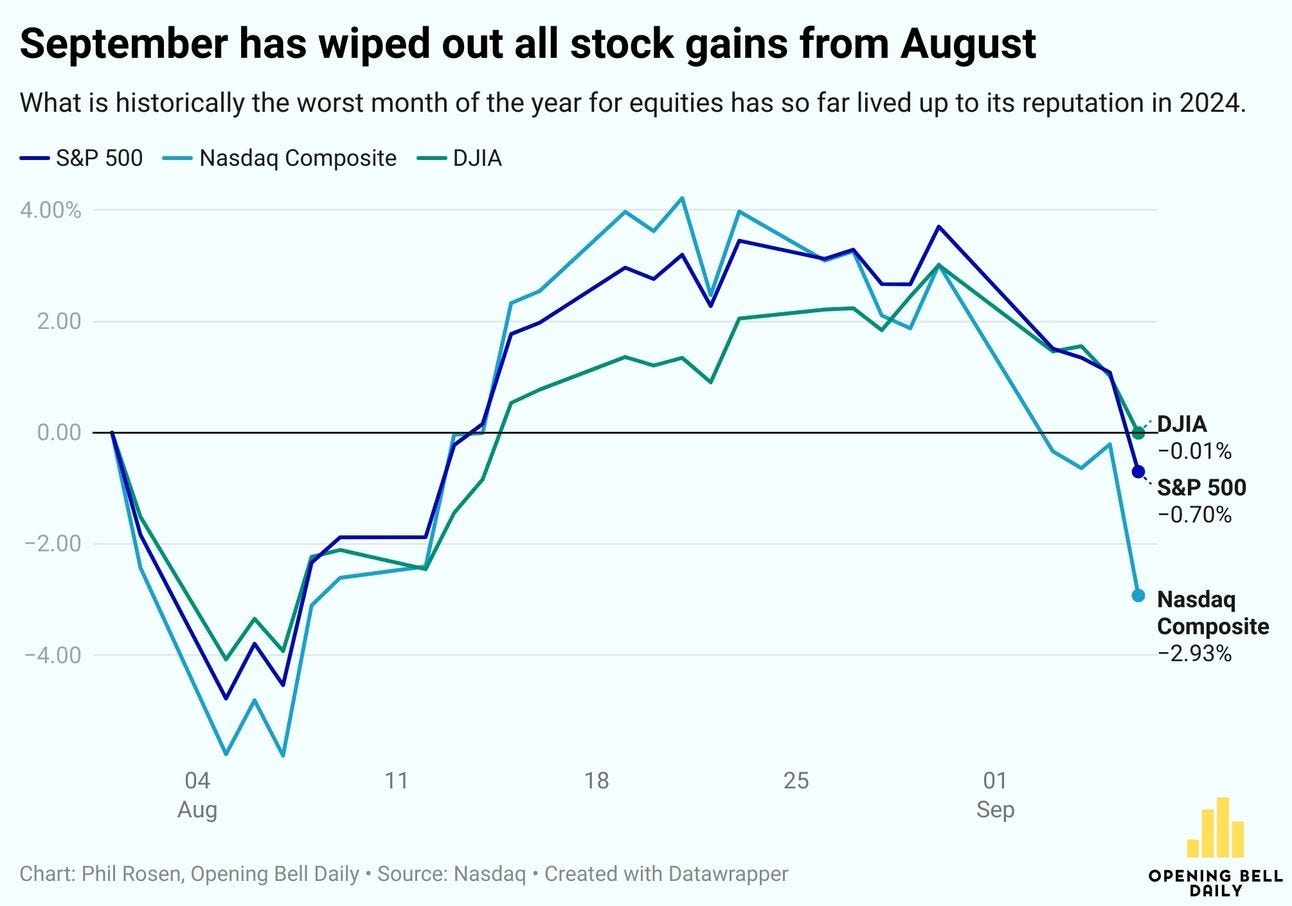

And so, today’s note SHOULD be short. The last thing you want / NEED is more noise after what was arguably the worst week for risk assets (S&P 500) since March of 2023 and the regional banking crisis …

Bloomberg: Traders Keep Half an Eye on CPI With Jobs Fear the New Inflation

… this is NOT — repeat, NOT — only a USofA experience as the next story / visual details …

Bloomberg: Risk-On Momentum in Stocks Succumbs to Mounting Growth Worries

“While the bears have plenty to work with — in terms of a softening labor market and a slowing economy — the facts still show an economy that is expanding and not one that is imminently headed into recession,” said Chris Zaccarelli, CIO of Independent Advisor Alliance.

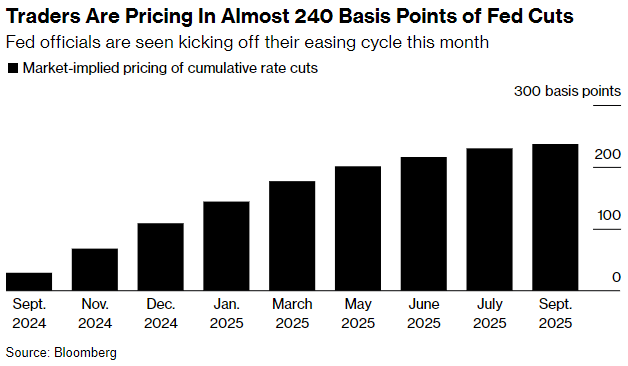

Now, the market chatter leading up to the jobs report had hoped for clarity on whether the Fed would be moderate or aggressive with its first interest rate cut next week.

As of late Sunday, CME data showed 70% odds for a 25-basis-point cut, and 30% odds for a larger half-point cut.

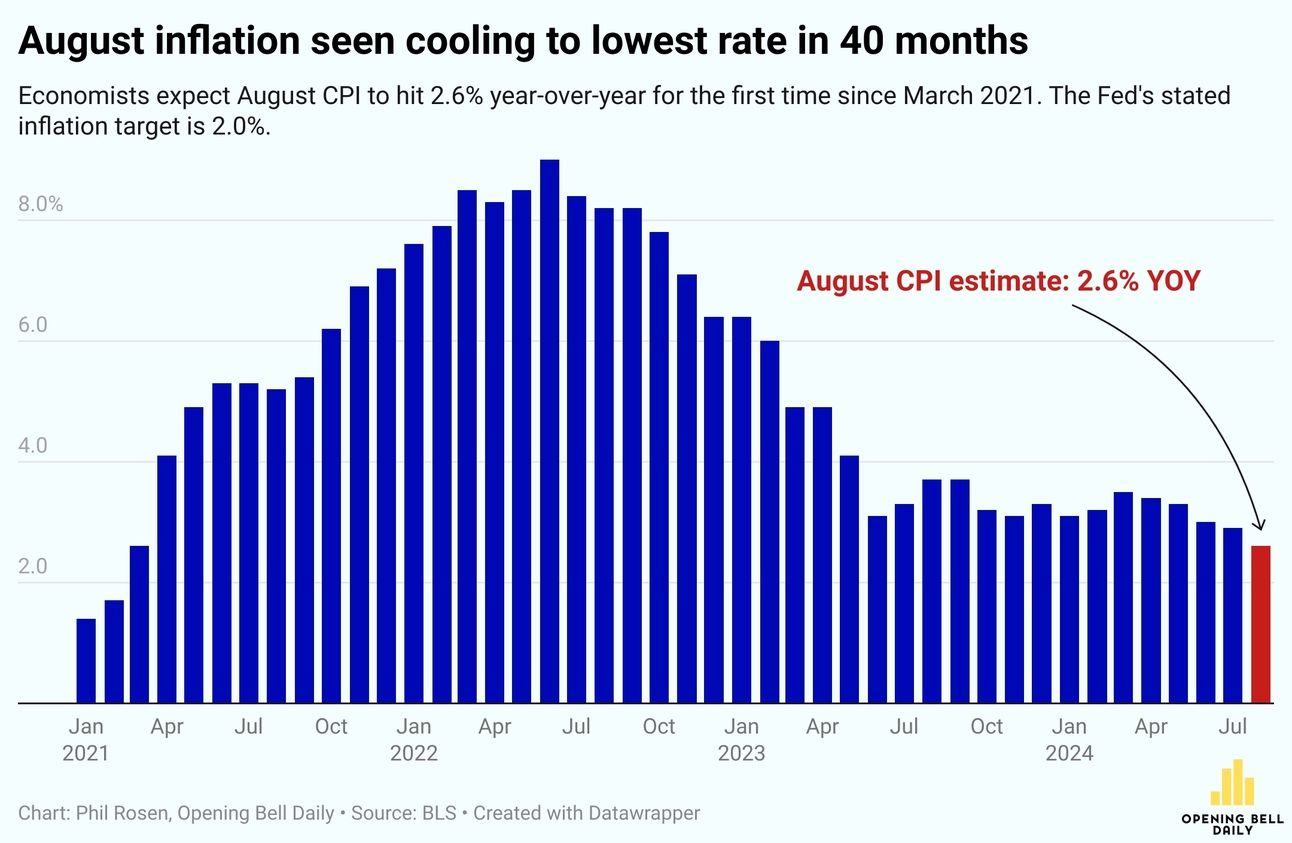

That could change this week as inflation comes due on Wednesday.

Wall Street estimates CPI will hit 2.6% compared to a year ago, cooler than the 2.9% seen in July.

If that holds, it would be the lowest print since March 2021.

“Although we are still looking for the Fed to start a series of 25bp rate cuts at the upcoming meeting, bigger cuts are on the table, because our read of the jobs report sees heightened risks that the slowdown will be more than our baseline assumes,” Carpenter said.

… the ‘good news’ is becoming less good by the moment, looking even further away (East)

… AND SO, as global equity and other MARKETS move, so too are policy prognostications …

Yahoo: Inflation back in focus, Apple's iPhone event: What to know this week

…The Goldman Sachs economics team led by Jan Hatzius reasoned Friday's Fed speak was consistent with Goldman's forecast for a 25 basis point cut in September but indicates "that the Fed leadership is open to 50bp cuts at subsequent meetings if the labor market continues to deteriorate."

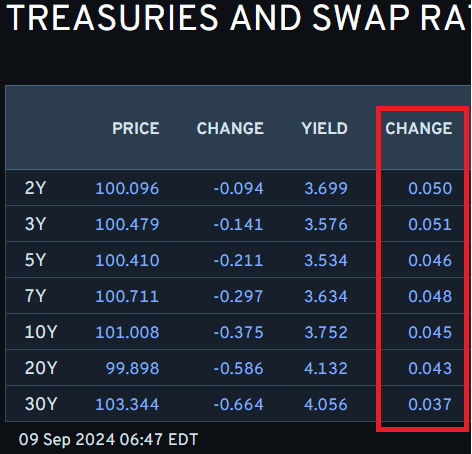

… and so it goes. As the sun rises and Global Wall gets back to their desks and fires up Bloomberg terminals preparing for the day and week ahead … here is a snapshot OF USTs as of 647a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: European equities gain, DXY stronger whilst JPY lags given the risk appetite … Bonds are entirely in the red and reside near session lows … USTs are pulling back following a session of gains on Friday in the wake of the August NFP print and comments from Fed's Waller, Williams and Goolsbee. Today's data docket remains light, focus is on NY Fed SCE, but traders will ultimately be attentive of the Presidential Debate on Tuesday and CPI on Wednesday. From a yield perspective, the 10yr has recovered to circa 3.75% after briefly taking out the August low @ 3.667%.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ in addition TO what was noted over the weekend (HERE: NFP and Wall-E …)

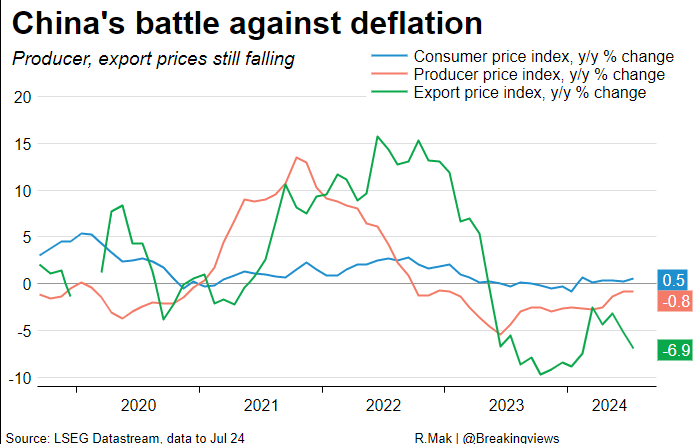

Here are some thoughts following up news from China overnight …

BARCAP China: Risk of entrenched deflation expectations is rising

August core CPI hit a 42-month low, and PPI deflation worsened. The broad-based moderation in nonfood items - healthcare, recreation, housing and transport - suggests risk that deflationary expectations could become entrenched. GDP deflator has been negative for a record five quarters, with no sign of end to deflation in H1

… This next note from France reiterates a view - 25bps confirmed by NFP and Wall-E …

The August NFP print and Governor Waller’s subsequent speech support our view that the Fed will kick off the easing cycle with a 25bp rate cut this month.

… The August payrolls data confirmed our expectation that the July report was muddied by inclement weather (Figure 1). Improvement in the pace of job creation in construction and leisure/hospitality speaks to the point. Moreover, a reversal in temporary layoffs, a major driver behind July’s rise in the jobless rate, further supports the view of no rapid deterioration in labor market.

Nevertheless, the magnitude of the rebound was smaller than we projected, consistent with a narrative from the recent series of disappointing data that “the cooling in labor market conditions is unmistakable,” to use Fed Chair Powell’s words. The flow of workers from employment to unemployment picked up, part-time employment for economic reasons increased, and the number of people remaining unemployed also rose…

We expect an out-of-consensus 0.3% m/m core CPI print this week, due to temporary factors. This should, however, translate to a 0.2% m/m core PCE number and keep the Fed’s focus on the employment side of the mandate.

We believe that the candidate debate this week will shift the market’s attention toward US presidential election risks. We like hedging via USDCNH topside.

… AND I interrupt regularly scheduled macro / funDUHmental read of the inbox for this next note from one of if not THE best techAmentalists out there …

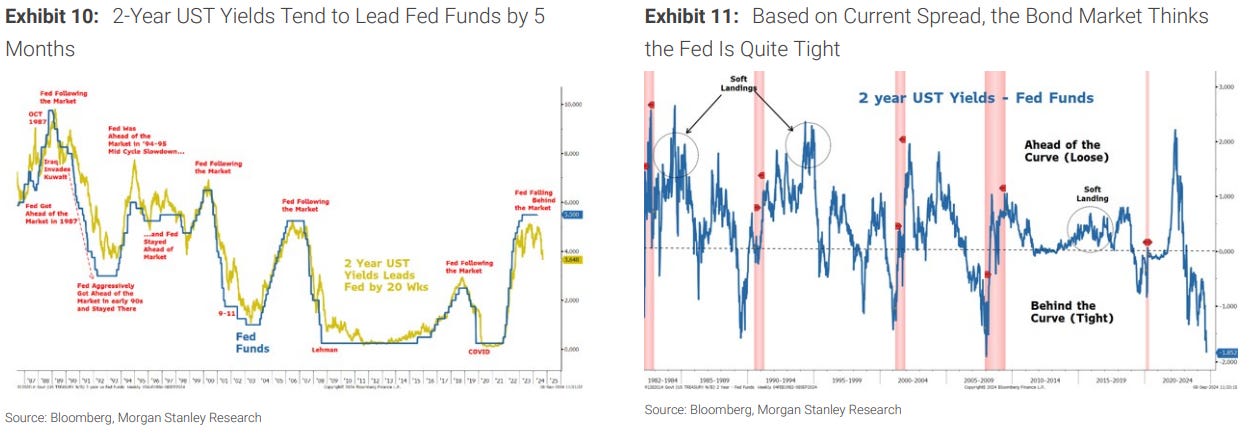

US 10y yields set the 'lower low' that we had been watching. Meanwhile, the US 2s10s curve finally disinverted on a weekly basis. We detail the levels we are watching:

US 2y yields: Support at 3.55% (March 2023 low) remains strong

US 10y yields: Set a lower low after the weekly break below 3.78-3.81% support. Next support is only at 3.25% (April 2023 low).

We have finally closed weekly below the very pivotal 3.78-3.81% support level (Dec 2023 and Feb 2024 lows). This sets a “lower low” and brings back the 55-200w MA setup into play. This suggests lower yields in the medium term horizon, with a formation indicated target at the 200w MA. The next major support level is only at 3.25% (April 2023 low).

Weekly slow stochastics, while in 'oversold' territory, is also not showing signs of crossing higher at the moment, supporting the case for lower yields. Resistance is at 4.03-4.09% (March low, 55d MA).

US 30y yields: Next key support is at 3.94%.

US 2s10s: Daily engulfing candlestick and double bottom formations continues to suggest we could see a move higher towards +57bps.

… Okie Dokie … from LEVELS to watch to a few thoughts from some of the best out of Germany …

DB: Mapping Markets: Why are markets so nervous right now, and is this justified?

Markets are very jittery right now. The S&P 500 just saw its largest weekly decline since SVB’s collapse in March 2023. And apart from the brief turmoil of early August, the VIX index closed at its highest since the regional bank turmoil as well.

On one level this makes sense. A significant fear is that a non-linear shift is about to happen where the economy turns sharply lower. Indeed, a common pattern in recent downturns has been that things appear fine until they suddenly aren’t. So even if payrolls at +142k doesn’t look like a recession, there’s no guarantee that continues. Plus the last 5 jobs report have all seen net downward revisions, so the fear is that things could be weaker than we currently realise.

But we shouldn’t over-egg how bad things are. Ultimately, the market decline has been driven by a narrow group, and we already knew that September is a seasonally weak month for equities. And on the bright side, jobless claims have been falling over the last month, payrolls growth remains positive, and financial conditions are still accommodative by historic standards. Moreover, given the weak track record of leading indicators in this cycle, it’s hard to put too much faith in them.

… AND from economists who were nearly ON the Fed and who are currently choosing remaining on Global Wall …

MS: Sunday Start | What's Next in Global Macro: Constructive outlook turning hazy

The August US nonfarm payrolls report came in softer than we expected, but not by enough to change our baseline view on the Fed—especially because recent spending and income data suggest continued momentum in the economy. Although we are still looking for the Fed to start a series of 25bp rate cuts at the upcoming meeting, bigger cuts are on the table, because our read of the jobs report sees heightened risks that the slowdown will be more than our baseline assumes. So, we are constructive, with a downside skew to risks … and all forecasts have risks. More soft payrolls prints, weaker spending, or very soft inflation will keep a 50bp cut squarely in play…

…For the Fed—and thus the path of interest rates and data the market can react to—the election reinforces the need to be “data dependent.” Historically, the Fed has not preempted the effects of fiscal policy but have generally waited to see what legislation is passed and looked for its effects on the economy. Judging from the 2018 Fed minutes, the central bank is attuned to both inflation and growth risks from tariffs, but their own uncertainty must be high, so again, they would likely wait to see what effects develop. As the saying goes, forecasting is hard, especially about the future. Never has that sentiment been more apt.

We retain our Fed call for 25bps in September and a total of 75bps in 2024. Payroll data showed clear slowing, but not enough to shift the Fed to 50bps in our view. In particular, because consumer spending remains strong, a recession is not the base case. We retain our call for 25bps, but the debate will continue. If the slowing in the labor market accelerates, the Fed could clear make bigger cuts, which makes it all the more challenging for markets. We continue to expect a broad deceleration into year end but without recession….

… Morgan Stanley continues, noting more questions than answers after Fridays NFP and so, looking towards CPI for resolution …

MS: The Weekly Worldview: Is inflation the only answer to central bank questions?

Central banks are data dependent. As inflation decelerates from its post-covid highs, the set of data that determine monetary policy paths are large.

Last month’s market turmoil is likely not over yet, given the inconclusive August US payrolls print. It was the July payroll print that triggered market focus on growth risks, but subsequent to that print, US consumer data consistently demonstrated resilience. And yet that fact does not allay growth concerns. Financial markets have reacted to the newfound uncertainty, with dollar weakness being noted by many clients. The converse of dollar weakness is yen and euro strength. The Sunday Start this week addresses the outlook for the US and the Fed , so we wanted to use this weekly to discuss other DM central banks…

… Morgan Stanley’s stock jockey getting us ready for the week ahead, talkin’ BONDS …

MS: Weekly Warm-up: Equities Getting Back in Sync with the Data and Other Macro Markets

The softer than expected jobs report did not provide the equity market with comfort that July's weakness was driven by one-off factors. Attention now turns to the policy response. In our view, a slowing labor market is consistent with a late cycle backdrop and quality + defensive leadership.

… As of Friday, the spread between the 2-year Treasury yield and the Fed Funds Rate reached new wides for this cycle at ~190bps, which matches the widest levels reached in the past 40 years. This pricing suggests the bond market believes the Fed is behind the curve from an easing standpoint. On Friday, the equity market appeared to start to question whether a 25bp cut in September would be an adequate policy response to the labor data. Our economists continue to see the Fed cutting 25bps in September followed by a series of 25bp cuts at consecutive meetings. Based on the current state of the labor data, we think the equity market would view a 25bp cut at the September meeting as an adequate policy response if a) it comes alongside guidance that cuts of more significant magnitude could come at future meetings if the data should warrant it or b) the Fed announces other policy support like ending QT completely by year end. Part of our thinking here is that the yen carry trade unwind may still be a risk factor behind the scenes. A quick drop in US front end rates could cause the yen to strengthen further, thus eliciting an adverse reaction in US risk assets tied to the carry trade unwind. A more measured 25bp cut at the September meeting with optionality for more significant cuts (depending on the data) seems to be more aligned with the current state of the jobs market and may reduce the risk of a rapid JPY move. A further reduction in QT would likely not have as significant of an impact on JPY/USD as larger rate cuts, in our view.

The bottom line, until the bond market starts to believe the Fed is no longer behind the curve (spread between 2-year yield and Fed Funds narrows), growth data reverses course and improves materially or additional policy stimulus is introduced, it will be difficult for equity markets to trade with a more risk on tone, in our view. This means valuations are likely to remain challenged for the overall index (21x moves toward our fair value multiple of 19x), while the leadership remains more defensive. We see two ways in which the Fed can get ahead of the curve—either faster cutting than expected (unlikely in the absence of recessionary data) or the labor data starts to improve in a convincing manner and 2-year yields rise. Given the Fed is in the blackout period until its next FOMC meeting, and there are not any major labor data reports due for another several weeks, volatility can remain elevated in the near term, which brings our previously discussed fair value range for the S&P 500 (5000-5400) back into view.

… And from Global Wall Street inbox TO the WWW where this first note has got to elicit a pause and raise MORE than a few questions … from BOTH Teams (Rate CUT and the other guys) …

…The bottom line is that the incoming data is more unreliable and creates extra uncertainty for investors and policymakers.

… NEXT up is what would appear to be a statement of the obvious from the press …

Bloomberg: The Bond Market Rally Rides on How Fast the Fed Will Cut Rates

A September easing is virtually assured as job market cools

With aggressive rate-cut path priced in, a risk seen to rally

… On Friday, the Labor Department’s employment report underscored the uncertain outlook. Employers expanded payrolls at a slower-than-expected pace of 142,000 in August, capping the weakest three months of job growth since mid-2020. But the slowdown wasn’t sharp enough to tip the debate over how swiftly — or how deeply — the Fed is likely to ease policy in the months ahead.

Traders are still putting the highest odds on the Fed reducing its target rate — now in a range of 5.25% to 5.5% — by a quarter-percentage-point this month, though those at Citigroup Inc. and some other banks are betting on a half-point move. By mid-2025, swaps markets are pricing in that it will be cut to about 3%, roughly around the level that’s seen as neutral to economic growth.

… next up a few words of opinion where it would seem there are STILL more questions than answers and the press knows how to ask them questions …

Bloomberg: Jobs don't justify a half-point rate cut. Will inflation? (Authers OpED)

When the data aren’t decisive, the Fed and markets will rely… on more data.

Non-Decisive Payrolls Friday dawned with a sense that something was about to be decided. It wasn’t. Non-farm payrolls data for August showed employment growing, but more slowly and by a bit less than had been expected, while the separately measured unemployment rate ticked down slightly. Two questions dominating market discussions — Will there be a recession? And will the Federal Reserve cut by 50 or just 25 basis points when it meets later this month? —were left unresolved. If anything, the answers seem a little further away.

Lindsay Rosner of Goldman Sachs Asset Management captured feelings neatly:

Labor market continues to show signs of deceleration. That is real. This report doesn’t clearly state 25 or 50 bps for the first cut, which was the answer the market was hoping to get. What is clear is the Fed is cutting and upcoming Fedspeak will help shed some light on the internal debate around September.

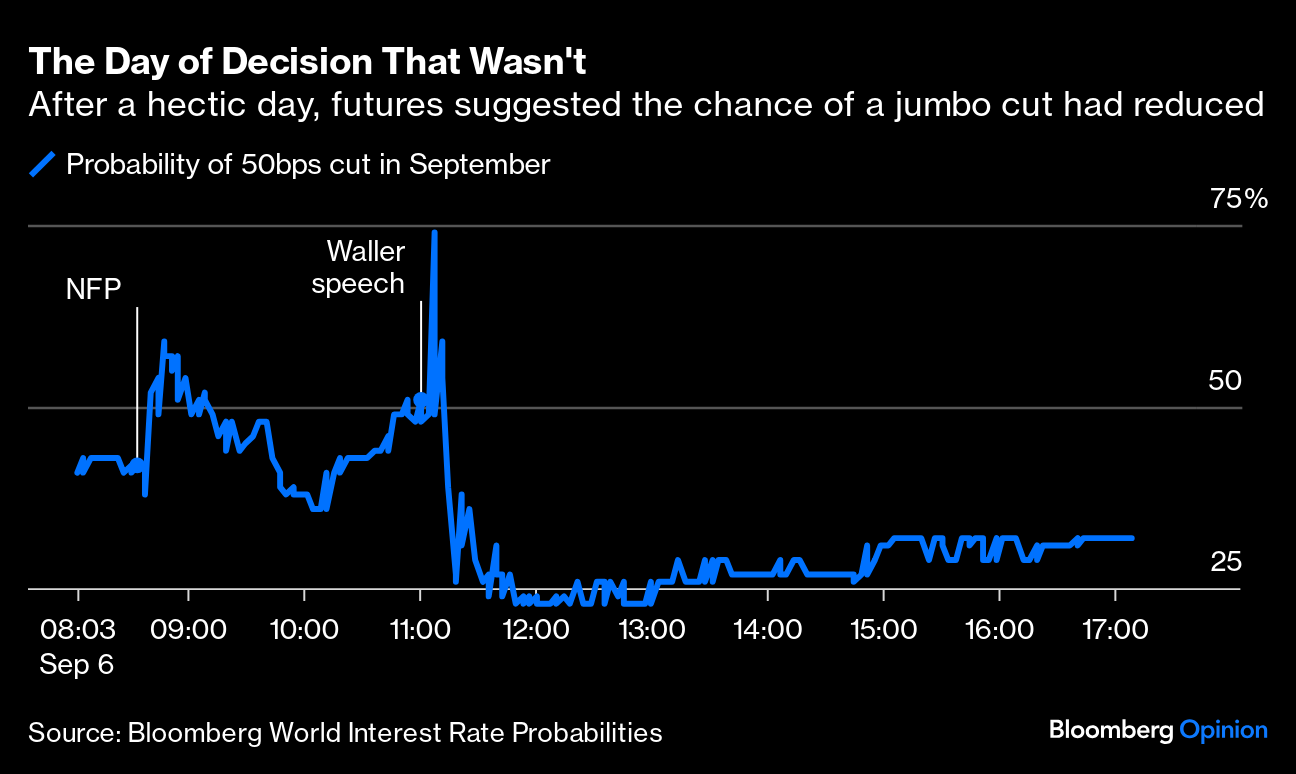

That proved prescient, as a mid-morning speech by Fed Governor Christopher Waller moved the market far more than the data. This is how the odds of a 50 basis-point cut (25 basis points already seems a total certainty) moved as Friday trading unfolded:

Waller’s speech is worth reading. He said the latest data reinforced the Fed’s view of “continued moderation in the labor market,” that “the balance of risks has shifted toward the employment side of our dual mandate,” and that monetary policy “needs to adjust accordingly.” Most strikingly, he said that the latest batch of data “no longer requires patience, it requires action.” That sounds like strong stuff from a governor generally regarded as a hawk. The immediate market reaction wasn’t surprising. But his final summing up merits closer reading:

As of today, I believe it is important to start the rate cutting process at our next meeting. If subsequent data show a significant deterioration in the labor market, the FOMC can act quickly and forcefully to adjust monetary policy. I am open-minded about the size and pace of cuts, which will be based on what the data tell us about the evolution of the economy… If the data supports cuts at consecutive meetings, then I believe it will be appropriate to cut at consecutive meetings. If the data suggests the need for larger cuts, then I will support that as well.

Emphases are mine…

…. not sure how / where to tuck this one away but noted / noteworthy chart of the week from Doubleline via Macrobond … funds rate and 10yy …

… Fed cuts have typically coincided with periods when the U.S. was heading into or already in a recession. This cycle seems to be different. While U.S. economic data suggests softening growth, the probability of a recession according to Bloomberg economists stands at only 30%.

Secondly, the yield curve has typically been either slightly inverted or flat when the Fed began cutting interest rates, with short- and long-term interest rates aligned. This time around there is a very visible divergence between the level of the Fed’s policy rate and the 10-year U.S. Treasury yield.

While longer-term treasury bonds have historically been a safe bet for investors anticipating post-rate-cut rallies, today's economic (and inflationary) context paints a more complex picture. The significant yield curve inversion and low odds of a recession complicate the outlook for long term yields unless the U.S. economy deteriorates more than currently expected.

… AND one from Sam Ro who always offers an interesting HEADLINE (aka ‘clickbait’) but then follows with whats normally a better than average ‘review of the macro crosscurrents)

Sam Ro from TKer: The other side of the Fed's inflation 'mistake'

… I can’t pinpoint exactly when the calls to tighten began when inflation was heating up three years ago. But we can all agree that these calls grew loudest ahead of the Fed’s first rate hike in March 2022.

As you can see in the chart below, the core PCE price index (blue line) — the Fed’s preferred measure of inflation — was at a high of 5.5% in March 2022. Clearly, inflation was a problem.

That same month, the unemployment rate (red line) was 3.6%, the lowest level since before the pandemic.

As inflation rates rose and the Fed waited to hike rates, the unemployment rate continued to fall. (Source: BEA, BLS via FRED)

The unemployment rate effectively bottomed that month, mostly trending sideways as inflation rates cooled…

…Here’s my point: While it’s fair to argue the Fed hiked rates too late in the context of inflation, I don’t think it’s fair to argue they made a mistake — especially when you consider the goals of monetary policy in their entirety, which include promoting maximum employment.

While high inflation is a headache for consumers, at least some of it was the result of newly employed people finally being able to afford to purchase goods and services.

Like I said before, the world is complex. So who knows? Maybe there’s a scenario where the Fed tightened monetary policy sooner and the unemployment rate continued to fall anyway as inflation cooled.

But the likely outcome of tighter monetary policy earlier in this economic cycle would have been unemployment bottoming at a higher level than what we’ve experienced.

I’m not suggesting the Fed was right or wrong to adjust monetary policy when it did. I’m just saying that you cannot talk about how monetary policy actions affect inflation without addressing how they affect employment.

How about instead of proclaiming that the Fed was late in the context of inflation — which is not a controversial view — we instead tackle the philosophical question of how we balance the tradeoff between price stability and employment. How many people is it okay to leave unemployed if it means improving price stability?

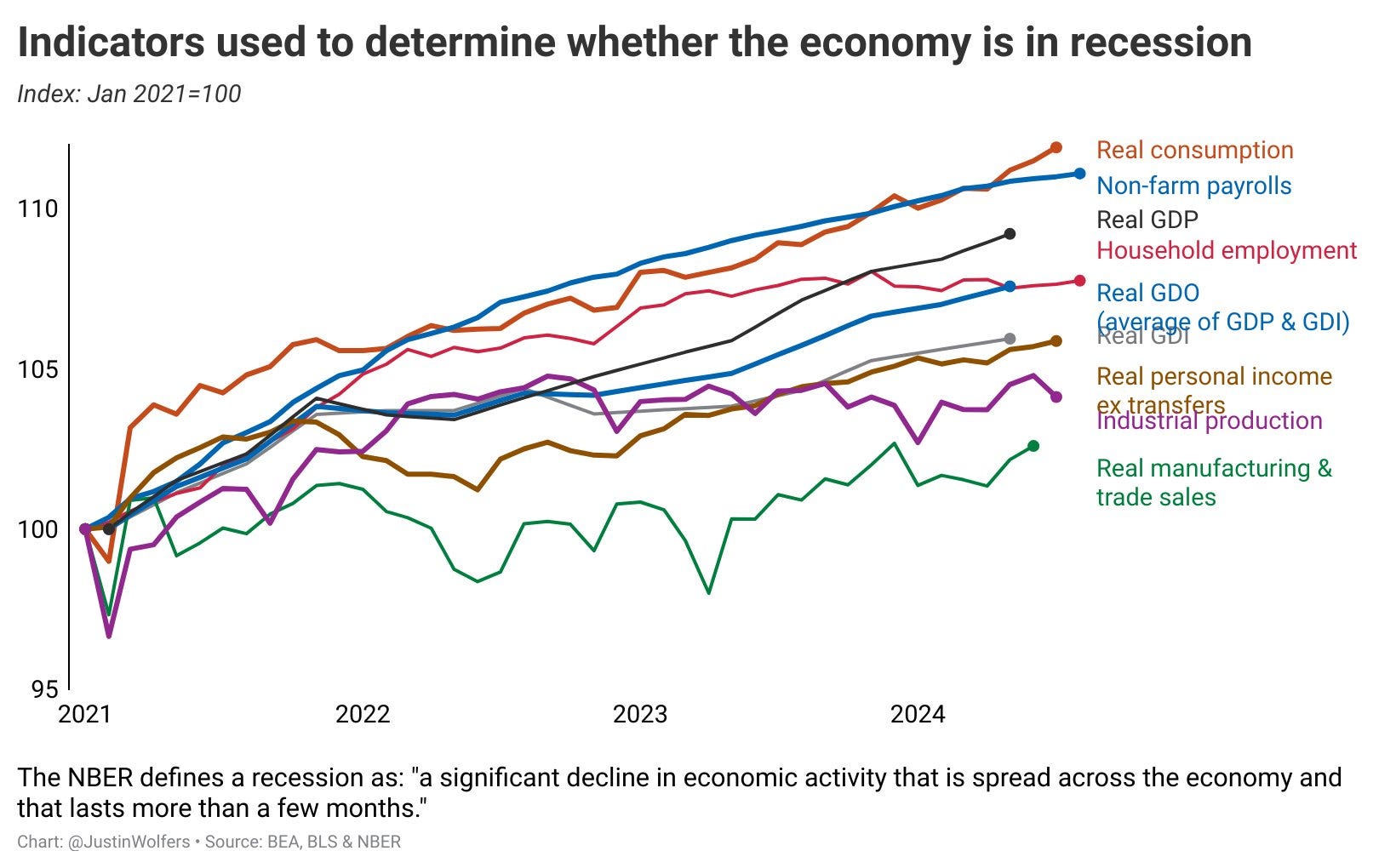

… Key recession indicators point to growth. Here’s a great chart from economist Justin Wolfers tracking the trajectory of key measures of economic activity.

WolfST: The Yield Curve’s Steep Inversion, now Partial Un-inversion, the Sag in the Middle, and its Predictions of Recessions

Over the past 25 years, the yield curve predicted 4 business-cycle recessions, two of which didn’t come. So we handle it with care.

…3-month to 10-year: With 3-month yields still at 5.13%, and the 10-year yield at 3.72%, this portion of the yield curve remains steeply inverted, with the spread between them at -141 basis points.

This part of the yield curve inverted in Jun 2019 and un-inverted in January 2020, and there was no business cycle recession either. But some weeks later, there was the pandemic, which yield curves do not predict and are not supposed to predict.

It also inverted and un-inverted in 1998, with no recession anywhere near (black up-arrows).

The yield curve and recessions.

The inversion and un-inversion of the yield curve was often followed by a business cycle recession. But QE started in 2008, profoundly distorting the Treasury market, and so when the Fed began cutting rates in 2019, after its feeble rate hikes through 2018 and QT through mid-2019, the yield curve inverted and then un-inverted, and there was no business cycle recession. What we got in March 2020 was a pandemic, which yield curves don’t and are not supposed to predict.

The yield curve also gave a false positive in mid-1998, when the yield curve inverted and un-inverted without business cycle recession anywhere near.

So that’s a very mixed record: Over the past 25 years, the yield curve predicted two business-cycle recessions that didn’t come (1998 and 2019), and two that came.