Good morning … no shortage of walatility over the past 24hrs as markets were roiled Sunday evening and then were summarily unroiled into end of biz Monday, as both Mexico and Canada have apparently come to the table on bended knee … how many analogies can one mix and mush, in a single sentence you ask? Dunno, but lets keep going.

Just kidding but seriously, though, ‘47s strategy is working.

Get this, the ivory tower academics aren’t gonna like it, but the Superbowl isn’t gonna cost more (Chuck Schumer holding up an avocado and a Corona — funny, if you think of it — sad, though, if you REALLY think about what a fool he is / was / will be) and there isn’t gonna be a tariff-induced global depression and inflation expectations, well, might not be off ‘to the moon, Alice’.

Yet.

Granted, this can / will change in a months time (or by weeks end) but certainly those on the FOMC will likely have ample room to continue to absorb information, process it, and continue to sit idly by and do nothing until further notice, awaiting the next impetus which can / will impact growth and ‘flation picture.

But for now and by yesterdays end, well …

ZH: Gold Hits New Record High As Tariff-ic Monday Sparks Tumult Across Markets

Trade war OFF … ?

Bloomberg: Trudeau Says Trump Tariffs Delayed 30 Days After Call

ZH: Trade War Over? Mexican President Says Tariffs Delayed For Month After Deploying 10,000 Troops To Border To Halt Fentanyl

… Off, for NOW unless it’s back to game ON …

CNBC: China retaliates with additional tariffs of up to 15% on select U.S. imports starting Feb. 10

… AND there was some data …

ZH: Trump Effect: US Manufacturing Surveys Signal 'Expansion' For First Time In 16 Months

And ‘bout that bank lending …

CalculatedRISK: Fed January SLOOS Survey: Banks reported Weaker Demand for Residential Real Estate

ZH: Banks Report Tighter Standards, Growing Loan Demand As Conditions Ease Some More

Will the real narrative please step forward? Nevermind. About those time where supply creates its own demand, what IF there is less supply, will it then just create LESS demand …

ZH: Treasury Trims Borrowing Estimates After Issuing Much More Debt Than Expected Last Quarter

Less supply would / should be good for bonds, all things being equal.

Which they never are. Steeper and cheaper for the win (concession?) and so … here is a snapshot OF USTs as of 702a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly cheaper and steeper after digestion of the Canadian tariff delay and China’s targeted reprisals on energy imports and agriculture. A 244k/01 TU-TY block flattener was seen overnight, before a bear-steepening resumption into London hours with core sovereign yields backing up. UK gilts are showing under-performance despite good bidding metrics for the 5y Gilt auction, modest peripheral out-performance seen with France -1.5bps to Gmy in 10y. Crude Oil is -2%, Copper +0.6%, while the DXY is -0.4% with USDJPY back above 155. S&P futures are flat here at 6:45am, with DAX and the CAC40 both +0.2%. …

…10y Yields - Now showing a tactical sell signal with daily momentum bearishly crossing after the 4.50% level was aggressively rejected on yesterday’s reversal candlestick. The multi-month bear channel pattern resistance was also confirmed, suggesting renewed bearish pressure. Near-term support overhead comes in at 4.64% and then 4.735%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US equity futures modestly lower, Crude softer, Bonds and USD await tariff updates … Bonds pullback but remain above Monday's lows as we await tariff updates from US/China … USTs are essentially flat. Has a very mild bearish bias but this is minimal in nature with USTs at the mid-point of a slim 108-23 to 109-00 band; one which is entirely within Monday’s much more expansive 108-21+ to 109-15+ parameters. Treasuries picked up as US tariffs on China came into force, at which point China almost immediately retaliated with measures of its own on the US and an investigation into Alphabet’s Google. Amidst this, USTs lifted by around six ticks to print the above session high. Traders will keep a keen eye out for the readout from Trump-Xi's call; US JOLTS Job Openings and Fed speak also due.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Lets begin with a read from across the pond on … you guessed it …

ABNAmro: Year of the tariff kicks off with a bang | Insights newsletter

President Trump’s ‘will he, won’t he’ threats of a 25% tariff on goods from Mexico and Canada (a 10% additional tariff on Chinese goods has already been levied) have significantly raised the probability of a more economically damaging trade war between the US and its main trade partners.

Global Macro: US imposes 10% China tariffs. Beijing retaliates immediately, in a targeted, measured way. 10% US tariffs not a game changer, but more could come.

Construction Spending goes into the GDP calculus, best I reckon …

BARCAP: December construction spending rises on residential strength

Construction spending rose 0.5% m/m in December, driven by strong private residential spending. Today's data come alongside upward revisions to October and November, indicating that construction spending in Q4 was stronger than initially thought.

The manufacturing ISM rose 1.7pts in January, ascending above 50 for the first time since late 2022. We think that the improvement is exaggerated by unwinding disruptions from hurricanes and the Boeing strike that had weighed on activity during Q4 24.

Finally, same shop with few initial thoughts on stocks …

While Trump's aims could be primarily political, we estimate that his latest tariff announcements would amount to a low single-digit drag on SPX EPS if implemented and not rolled back this year. Energy, Materials, and Discretionary sectors appear most at risk.

Best in the biz with a few closing thoughts yesterday afternoon …

What began as a dramatic trading session in US rates following Trump’s tariff announcements very quickly moderated, although a few key aspects of the price action remain. First, the yield curve is flatter – a dynamic that reflects the 2- year sector’s cheapening back toward effective fed funds as investors have become increasingly concerned that the trade war will stall Powell’s ability to normalize policy rates any further. For context, the futures market continues to price in more than 40 bp of cuts this year, even as the nominal 2-year rate implies that the Fed will struggle to restart normalization so quickly. Of course, positive term premium can also account for at least part of the disconnect. This dynamic speaks to the importance of Wednesday’s Refunding Announcement and the Treasury Department’s guidance on the prospects for larger nominal coupon auction sizes – especially further out the curve in the durationheavy, 20- and 30-year sectors. We’re not anticipating any grand revelations, but investors will undoubtedly attempt to read the proverbial tealeaves given the importance of supply to the bear steepening of the last few months.

The second notable aspect of the price action was the emergence of an outright bid for duration. 10-year yields dropped as low as 4.46% as investors weighed the potential fallout from the trade war…

From Germany, a fan fav stratEgerist recapping tariffs (China o/n) and the UST moves yest …

Just after the US deadline for imposing 10% tariffs on Chinese goods, China announced countermeasures including tariffs on US goods, additions to its Unreliable Entity List, an antitrust probe into Google, and export controls on strategic materials. These actions may be bargaining tactics for upcoming US-China negotiations, which are expected to cover broader issues beyond the fentanyl concern that initially triggered the tariffs. We provide initial thoughts on the potential impact of these measures and what to expect next.

Firstly, China announced a 10-15% tariff on USD14bn of US goods as a direct countermeasure to US tariffs…

Secondly, China also decided to launch investigation against Google for potential antitrust violations…

Thirdly, China added two US companies to China’s Unreliable Entity List…

Lastly, China also announced export controls with immediate effect on tungsten, tellurium, bismuth, molybdenum, and indium-related items…

…If you're feeling dizzy this morning I can't blame you as the past 24 hours have seen a big roundtrip for many assets classes as strongly negative sentiment gave way to a relief rally on news that the planned 25% tariffs against Mexico and Canada would be delayed…

…The tariff delays came as leaders of Canada and Mexico announced new border measures, following calls with Trump. The Mexican President had agreed to supply 10,000 soldiers to the US border, which Trump posted “will be specifically designated to stop the flow of fentanyl, and illegal migrants into our Country.” Towards the end of the post, he also said that there would be negotiations, saying “I look forward to participating in those negotiations, with President Sheinbaum, as we attempt to achieve a “deal” between our two Countries.” Similarly, Canada’s PM Trudeau announced several security steps on top of a recent $1.3bn border plan, including appointment of a Fentanyl Czar, a new US-Canada joint strike force and $200m on a “new intelligence directive on organized crime and fentanyl”. Again, Trump posted that the delay would be used “to see whether or not a final Economic deal with Canada can be structured”. New executive orders formally delay the tariffs until March 4th…

…For US Treasuries, there was a sizeable curve flattening yesterday, which came as investors priced in stronger near-term inflation and dialed back their expectations for Fed rate cuts, with the move partially reversing as the tariff delay news came through. The 1yr inflation swap jumped from 2.65% on Friday to as high as 2.82% before retreating to 2.73% by the close. And fed funds futures are now pricing 41bps of cuts by the December meeting, down from 47bps before the weekend. In turn, that led to a notable rise in front-end Treasury yields yesterday, with the 2yr yield up +5.1bps to 4.25%. The 10yr yield was up +1.6bps to 4.56% after falling as low as 4.46% intra-day…

Same shop, different group with a note on trade and tariffs …

DB: Five long-term signals on trade not to miss (and 10 more charts)

Markets have navigated a great deal of uncertainty, volatility and back-and-forth on tariffs in the opening salvo of this year's trade war. Amidst all the noise, we highlight five long-term trends not to miss. Global trade is changing in fundamental ways, and markets should be thinking about these structural drivers as we move forward.

1. Trade has been a channel for massive global imbalances in production and consumption, which the US is now keen to shift…

2. The cheap goods game is up in the US, but may pick up elsewhere…

3. US-China trade routed through connector economies is coming into focus…

4. While tariffs combined with tax cuts moves the US tax structure in a historical direction, there are limits to how far this can go…

5. Watch China rates: while FX is a key retaliatory metric, the long-term macro signal is in rates…

Switzerland notes similar cadence to BMO above and a few words on yesterdays data …

US President Trump again retreated from imposing aggressive taxes on US consumers. Although taxes on goods from Mexico and Canada are in theory delayed for a month, after three retreats in a row markets are unlikely to take that threat seriously. US consumers would have been visibly affected by these taxes—even Republican senators became aware that tariffs are paid by their constituents and not foreigners, and tweeted pleas for exemptions.

Taxing goods from China is still happening, and China has retaliated. The inflation consequences of these taxes are less obvious to US consumers. China helped US consumers avoid earlier taxes by rerouting exports. China sells goods that are bought infrequently (so consumers are less price-aware). China’s goods tend to fall in price over time, so taxing slows disinflation rather than fueling inflation.

The long-term consequences remain. Foreign countries have less reason to trust that the US will honor trade treaties, reducing the incentive to make concessions. US consumers may have had a fright over trade taxes, changing their behavior. This may be partisan. One news channel barely mentioned the economic fallout on its website, others emphasized it heavily.

US job vacancy data is due. The survey response rate is tiny, making the data an imprecise guide.

ISM manufacturing expands for the first time since 2022 … …We wrote a note recently outlining our thoughts on the ISM in more detail — generally we wouldn’t be surprised to see the index move above 50 this year but equally we would see the index remaining around 50, with some months above and some below…

… Construction spending stronger in December, but still see fading fiscal here …We have been watching the dynamic in private manufacturing plant construction and public construction spending given the fading fiscal impulse — we've seen the pace of spending here slow markedly from that seen in 2023. In the December data the 3-month change in private manufacturing plant construction slowed to 0.2% and public construction spending to 0.1% — see the figure below. This is weighing on structures investment which declined 1.1% in real terms in Q4, after declining 5% in Q3.

SLOOS: Little change in conditions over all, mixed demand in January survey

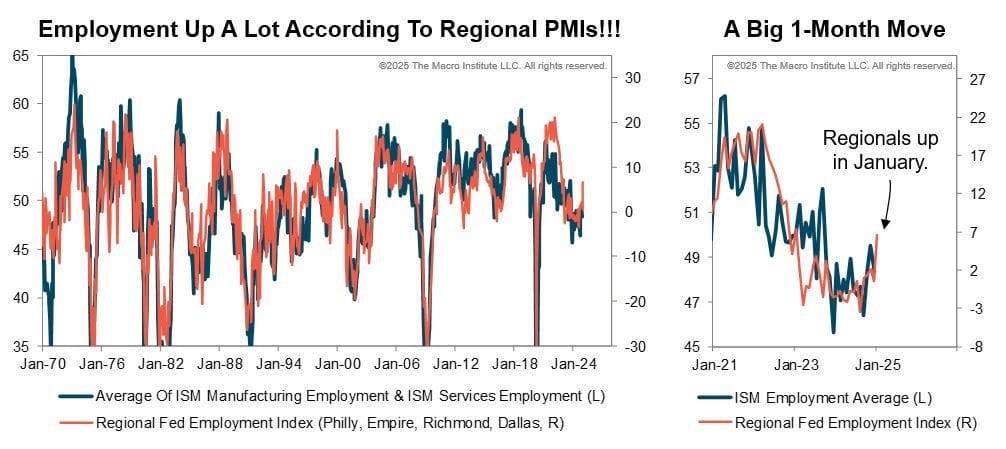

Back to (from) the future … economy expanding (and the trend / visual hard to read as negative …)

WELLS FARGO: In Pre-Tariff January, Manufacturing Expanded for 1st Time Since 2022

Summary Buoyed by gains across various sub-components, the ISM Manufacturing Index broke above 50 for the first time since 2022. Prices, production, employment and new orders all rose in a long-awaited rebound for a sector that has felt the pain of higher interest rates more acutely than others.

But WAIT, there was even some other corroborating positive news …

WELLS FARGO: Construction Spending Strengthens in December Single-Family and Home Improvement Construction Lift Outlays Higher

Summary Residential Improvement Counteracts Nonresidential Weakness Construction spending ended 2024 on a better-than-expected note with a 0.5% gain in December. As has been the case in recent months, private single-family construction and home improvement outlays propelled the overall increase. Private nonresidential spending also eked out a slight gain; however, traditional office, warehouse and retail spending remain subdued in the high-interest rate environment. That said, the build out of data centers is a notable green shoot. We expect construction spending to stay under pressure this year as interest rates remain elevated and trade and immigration policy changes increase construction costs.

AND same shop on … you guessed it …

WELLS FARGO: America's Next Top Model: Tariff Edition

Summary Prospects for a trade war are transitioning from a looming threat to looming policy. While most of the latest proposal is now on ice, our model simulations demonstrate how the latest round of proposed tariffs could introduce a modest stagflationary shock by negatively impacting growth and temporarily boosting inflation.

Finally, from MAGA to MMGA (with implications for Earl) …

Markets were abuzz with headlines from Washington today. The S&P 500 opened 1.7% lower on the weekend's news that President Donald Trump announced that he would slap 25% tariffs on Mexico and Canada on Tuesday. But losses were pared significantly after Trump's call with Mexican President Claudia Sheinbaum resulted in a one-month delay of tariffs as well as bilateral cooperation on fentanyl, immigration, and countering China.

Ultimately, the S&P 500 fell less than 0.8% today. A quick spike in the price of crude oil also fully reversed, and that was before a similar deal was reached between Trump and Canadian Prime Minister Justin Trudeau after the market closed. With energy security of the utmost priority to this administration, crude oil prices could retest their 2021 lows in the coming quarters (chart).

For all the chatter about tariffs upending global trade, US manufacturing—the sector that’s the most sensitive to such headlines—appears to be staging a comeback. Today's economic updates supported our view that the economy's strength and resilience can minimize any negative externalities from Trump 2.0's agenda…

… And from the Global Wall Street inbox TO the WWW … a few curated links …

Sent just after hitting send yest, still worth a moment, a pause and a click …

APOLLO: Tariffs on Mexico, Canada, and China Would Have a Significant Impact on the US Economy

Goods imports make up 11% of US GDP, and 43% of US imports come from Canada, Mexico, and China. This means that 5% of US GDP is directly impacted by higher tariffs on Canada, Mexico, and China. This is meaningful when annual GDP growth normally is 2%.

The biggest categories of US imports from China are computer and electronic products, electrical equipment and components, and textile and apparels, see chart below.

Bloomberg reporting on The return of The Kolanovic … Marco … Polo … Marco …

BLOOMBERG: Kolanovic Returns With Prediction for Pullback in S&P 500

Ex-JPMorgan chief strategist sees bevy of risks for stocks

‘Some probability’ of benchmark going lower into the 4,000s

The Federal Reserve cut interest rates for the first time in four years. Donald Trump captured the US presidency. The S&P 500 Index gained another 9%. And his former colleagues capitulated on their bearish views.

But to the celebrity strategist, who was among the last pessimists standing against this bull market when he left the business last year, not much has changed. US stocks face so many risks, from high concentration to geopolitical turmoil, that they’re still due for a substantial downturn, he says. The S&P 500 is trading above 6,000 and hit a new high two weeks ago, but Kolanovic sees it falling up to 1,000 points or more.

“I do think we’ll go back down in the 5,000s this year,” Kolanovic said on Bloomberg’s Odd Lots podcast. Potential turmoil from the new political climate could bring the gauge down “much lower into 4,000 — I think there’s some probability of that.”

While Kolanovic hasn’t changed his tune, this gloomy forecast looks timely with Big Tech stocks largely flat over the past six weeks, questions raging about US dominance in artificial intelligence, and concern that sticky inflation could force Fed officials to hold interest rates elevated for longer than originally expected. In addition, the new White House’s policies threaten to disrupt the economic and geopolitical landscape…

More about USTs specifically, from a shop taking a LONG view (in name, at least …)

Trade war risks have intensified over the weekend. On Saturday, Trump announced 25% tariffs on Mexico and Canada (with a lower/10% tariff on Canadian energy), and an additional 10% tariff on Chinese goods. Those countries have threatened to retaliate and, with that, several risk assets sold off overnight/this morning. That includes sharp moves lower in the CAD (-1.1%), and MXN (-2.1%).

US Treasuries, though, are broadly unchanged on the news, reflecting a mix of factors, including: (i) a safe haven bid (which is normal when equities/risk assets are sharply lower); and (ii) concerns about the inflationary impact of tariffs (e.g. see higher US 5 year breakeven rates this morning). How Treasuries behave in coming weeks will therefore be watched closely. Arguably, though, downside risks to US economic growth are beginning to build (with a trade war likely to add to those concerns).

In that respect our medium term Treasury models have recently generated a clear BUY message. Measured sentiment indices, for example, are bearish (a contrarian BUY signal), while speculative positioning remains net SHORT (albeit not at extreme levels). As such there’s plenty of fuel for further upside in Treasuries. Elsewhere our medium term technical scoring system has recently been on BUY (although is currently mid-range, see fig 1b below). See latest Longview Asset Allocation research for detailed US Treasury recommendations.

Fig 1: US Treasury 10 year government bond yields with 50, 90, & 200-day moving averages

Fig 1a: US 10 year bonds net speculative positions (deviation from trend) vs. US Treasury 10 year bond yields (inverted)

Fig 1b: Longview medium term technical scoring system vs. US 10 year bond futures

AND while tariffs certainly earning and taking all the oxygen out the room early on in the week, at weeks end it will be Macro wonderland …

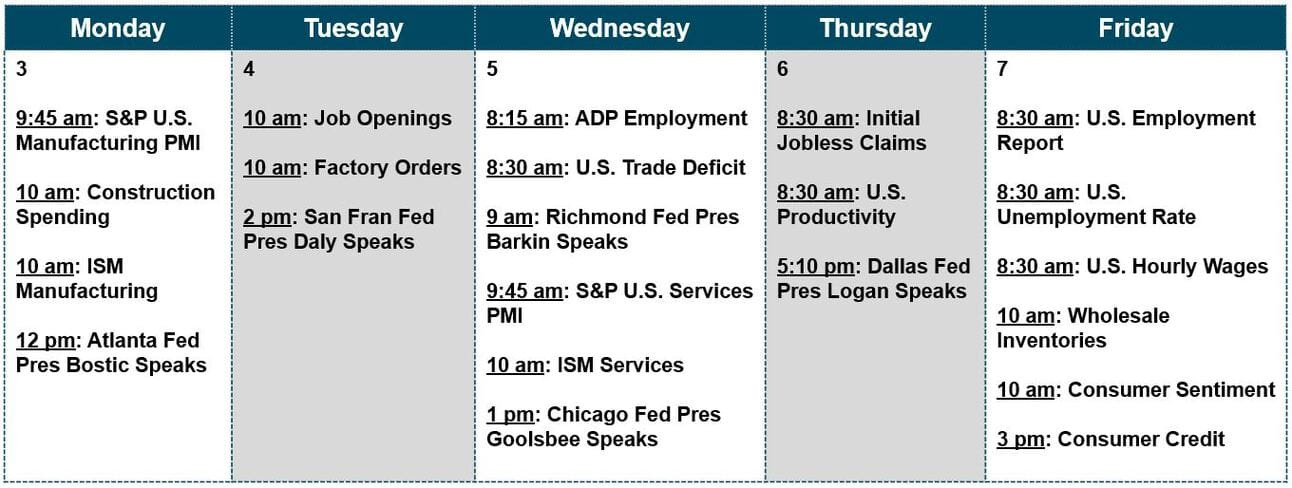

This is a big week for macro data. Kicking off Monday, we get January’s national PMIs, starting with the ISM Manufacturing Index. Then, on Friday, payrolls drop—but this isn’t just any jobs report. The BLS’s annual revisions are baked in, reshaping key metrics like Personal Income, Gross Domestic Income (GDI), and Productivity.

We already have some clues: three of the four major regional PMIs rose in January, including their Employment components (see chart above). Nothing’s certain until the data lands, but the odds favor a solid national PMI read. Stay tuned.

The Macro Week Ahead

The Fed Hits Pause: This week is packed with major macro data. The Bloomberg Economic Surprise Index has flipped from slightly negative to slightly positive, signaling stronger-than-expected U.S. growth and inflation figures. Last week, the Fed hit pause on rate cuts, with Chair Powell cautioning that inflation progress remains sluggish. Core PCE for December landed at 2.8% year-over-year (+0.2% month-over-month), still above the Fed’s 2% target.

January LEIs: A Turning Point?: At 10:00 am, ISM Manufacturing data is released, with the headline number expected to hit the critical threshold of 50 - the highest reading in over a year. December’s New Orders component came in at 52, hinting at a cyclical upturn from last summer’s contraction. Prices Paid climbed to 52 in December, with January forecasts at 55, reinforcing expectations for firm inflation in the near term. With the Fed having cut rates by 100 bps in an economy running above average capacity, inflation won’t cool easily.

On Wednesday, ISM Services is expected to hold steady at 54, with the Prices Paid component last month surging to 64. If recent shifts in U.S. immigration policy tighten labor supply in services, this index could stay strong.

It’s Jobs Week!: We kick off with ISM Manufacturing’s employment component, which was a weak 45 in December. On Tuesday, JOLTS data will show us job openings, quits, and layoffs for December. The openings rate peaked in mid-2022, and trends suggest we hit the cyclical low in fall 2024. Layoff rates remain low at 1%, and initial claims data point to a resilient labor market.

Wednesday brings ADP’s payroll estimate, with 150,000 jobs expected for January. Thursday follows with jobless claims and Challenger job cut reports.

Revisions & Payrolls: Watch the Data: Friday is a big day - the BLS Payrolls report drops, along with annual revisions to the establishment survey (April 2023–October 2024). The August preliminary revision cut 818,000 jobs - one of the biggest downward adjustments in a decade. Notably, Powell referenced this data when justifying last year’s rate cuts.

For January, non-farm payrolls are expected to show a gain of 170,000 jobs, down from December and November’s 200,000+ prints. The unemployment rate is forecast to hold at 4.1%, consistent with the past six months.

Finally from Wolfie …

WOLFST: Trump Agrees with Fed’s Pivot to Wait-and-See after the Fed Bows to Trump on Everything Else to Keep Monetary Policy Independent

We’ll see how long Trump’s side of this mutual understanding will lasts.