while WE slept: USTs on backfoot, Bunds outperf; #Got20s?; CNN reports and 'Earl is BID; "It speaks for itself" (where "IT" is USDJPY and 10yy, via DB); 10s TO 3.45; RIP, NORM!

Oil prices spiked and havens caught a bid after CNN reported, citing US officials, that new intelligence suggests Israel is preparing a possible strike on Iranian nuclear facilities in what would be a brazen break with US President Trump, although there is internal disagreement in the US government on the likelihood of an attack. (CNN)

… bonds don’t (YET)seem to be one of the ‘havens’ catchin’ a bid and yields are grinding HIGHER … 30s back up OVER 5% and 20s, 200 (without a Terminal cannot be sure)

… I can see ‘Earl looks bid.

This, of course, continues to present inflation and Fed Funds issues to consider but we know the Fed does not react in real time to geopolitical tensions. They continue to wait, watch and HOPE for the best … a bit more from THE source …

6:01 PM EDT, Tue May 20, 2025 CNN: New intelligence suggests Israel is preparing possible strike on Iranian nuclear facilities, US officials say

(CNN) — The US has obtained new intelligence suggesting that Israel is making preparations to strike Iranian nuclear facilities, even as the Trump administration has been pursuing a diplomatic deal with Tehran, multiple US officials familiar with the latest intelligence told CNN.

Such a strike would be a brazen break with President Donald Trump, US officials said. It could also risk tipping off a broader regional conflict in the Middle East — something the US has sought to avoid since the war in Gaza inflamed tensions beginning in 2023…

20yy DAILY: 5.00% has been breached and while only psychologically important …

… up ABOVE 5.00% now the market’s searching for another level of importance and frankly, it’s ALWAYS like a couple teenagers feelin’ around in the dark … NO idea what they’re lookin’ for but here we are and i’ve attempted to shine light on 20s vs 5.086% but now, without Terminal, lets just call it some sort of level just South of 5.10% … momentum (stochastics, bottom panel) are becoming overSOLD and ripe for either consolidation (turn of the page from 2024 into 2025) OR rolling over and supporting, then, LOWER yields…keep yer friends close and yer stops closer …?

I’ll quit while I’m behind as I’ve really not much to add to the moment (obvious, I know) and so … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries took an early leg higher in early Tokyo on light volumes, but quickly faded in a steepening down-trade with bonds again testing 5%. Our desk saw interest around this level with some consolidation, but the level failed to hold with the long end cheapening further into the US open. Flows remain on the light side with some selling materializing in intermediates; overall volumes remain consistent with the 20d avg. The US point has led the down-trade (1.5bps cheaper on the 10s30s fly). Light ASW selling out the curve has been seen with US invoice -1bp tighter. S&P futures are -0.7% here, DXY -0.7% as well, while Brent Oil is +0.9%, Gold +0.6% and 30y yields +6bps to 5.03%.

… The auction concession and result itself should be attributed quite a bit of importance given the point’s term-structure status as a ‘weak link’, while we also note that foreign involvement in the point has been declining rapidly this year. After foreign & Intl account allotments remained fairly stable ~14% of the total accepted bids through 2024, the last four auction events have seen a steady decline: 8.5% in January, 9.5% in February, 7.8% in March , and 7.5% in April (attached).

… #Got20s?

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: DXY lower and oil prices boosted on reports that Israel is looking to attack Iranian nuclear facilities … USTs started the day on the backfoot, down to a 109-25 base and a few ticks beneath the 109-28+ low from Tuesday. If the move continues, then the 109-20 WTD base is next. The bearish bias has been moderate so far, ahead of an expected floor reading of the US tax/spending bill on Thursday, a 20yr auction this evening in addition to Fed’s Barkin & Bowman.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Amsterdam weighin’ in on big bold and beautiful bill…

20 May 2025 ABN AMRO: Trump’s big beautiful bill is primarily big

Moody’s downgraded US debt while Congress debates a bill that significantly worsens the debt outlook. The proposed bill plays tricks with temporary and permanent policy, setting bad precedent. With or without the bill, the US’ debt trajectory is unsustainable in the long run. If the Trump administration addresses the debt problem, it seems likely to follow Japan’s playbook of increasing domestic demand for debt. They have also been pushing the Fed to lower rates, which may result in inflating their way out of the real debt burden.

…The selloff in the 30-year sector was the most compelling price action in US rates on Tuesday. As with Monday’s bid, there was no obvious trigger to the selling pressure. This isn’t to suggest that there aren’t reasons to sell 30-year bonds – supply concerns, deficit spending, forward inflation uncertainty, and the allure of 5.00% all come to mind. Investors approached this week wary that the absence of any top-tier data would pave the way for choppy, limitedconviction moves and that’s precisely what we’ve seen thus far. Friday’s recommended early close ahead of the long holiday weekend is further weighing on investors’ willingness to establish high-conviction positions without the catalyst of new fundamental information. As Trump’s 90-day tariff pauses remain in place, we’re unlikely to hear anything particularly market-moving on the trade front in the near-term. The resulting trading conditions imply that wait-and-see translates into more-of-the-same. In this instance, similarity insofar as choppiness, not necessarily outright direction of US rates.

The 30-year bond weakness is worth a nod for several reasons. First, the price action has reinforced the idea that 5.0% is a line in the sand for investors. Second, Monday’s 5.035% yield peak represents the highest 30-year rates have reached since November 2023. Even that selling pressure still only saw long-bond yields reach as high as 5.176% on supply worries before the move brought in dip buyers and moderate issuance objectives. Third, it strikes us that despite the choppy nature of some of the price action, May’s trend toward higher 30-year yields has been consistent and relatively orderly – implying that the repricing could prove more durable than the early-April correction. Fourth, as recession fears subside and the US exceptionalism narrative edges back into conversations, it follows intuitively that investors would seek greater compensation to move further out the curve. For context, 30-year breakevens are >230 bp – well above the 200-day moving-average of 225.6 bp and biased higher given the balance of risks.

From a technical perspective, there isn’t much preventing 30s from moving above 5.00% beyond the obvious handlechange. It’s the 5.035% threshold that is more likely to provide support, although even that becomes less daunting the longer the long bond remains >4.90% without drawing more buying interest. In the event of a material leg higher in 30-year rates – which we’re more open to in the wake of May’s steady selling pressure – attention will be focused on the ability of risk assets and domestic equities to handle such a move. Unlike in early April, the safe-haven character of Treasuries has been reestablished – at least for the time being.

Germany offering a look at recent TICS data … def speaks to those naysayers … and an early morning REID as well as more proof of that saying where a picture is worth a thousand words …

20 May 2025 DB: A TIC up in foreign Treasury purchases

To track the theme of investor allocation away from USD assets, our colleagues in FX strategy developed ETF-based indices that measure flows into US equity and fixed-income funds. These are particularly useful because the most comprehensive data on foreign flows – from the Treasury International Capital (TIC) system – are released with a significant lag. Indeed, it was just at the end of last week that we got data covering the month of March.

What did we see in the March TIC release? Foreign purchases of USTs hit an all-time high. At some level this is unsurprising given the record March trade deficit, but it is still notable given that the theme of diminished foreign demand for dollar assets was already gaining steam ahead of April 2nd (see here).

In the underlying details what jumps out most are elevated private purchases, in particular of short-term Treasuries (<1y). As shown in the chart below, total net private purchases hit a record of over $200bn and more than half of that went into short-term securities, exceeding purchases in spring 2020 and the GFC (not shown). The concentration of flows at the front-end likely reflects a desire to position defensively amid elevated policy and market uncertainty.

Looking ahead the market will be keenly focused on the April TIC data out next month. Foreign flows into USTs have averaged roughly $500bn per annum in recent years, around 25% of net issuance (see here). Signs confirming a pull-back in demand could drive clearing yields up significantly, especially given the outlook for continued large budget deficits that rely on external financing …

US fiscal matters have dominated again over the last 24 hours, as investors continue to grapple with what the long-term unsustainable nature of US debt means in the near term. After a complete round trip back to pre-downgrade levels on Monday, yesterday saw the 30yr Treasury yield (+6.7bps) moving up to 4.97%, whilst the S&P 500 (-0.39%) ended a run of 6 consecutive gains. And notably, those moves weren’t just confined to the US, with Japan’s long-end yields surging after weak demand at an auction, pushing their 30yr yield (+12.1bps) up to 3.082% - a near 25-year high. They are another +8.9bps higher this morning …

… Meanwhile for Treasuries, longer-dated maturities struggled amidst the fiscal situation, with the 10yr yield (+3.9bps) up to 4.49%, whilst the 30yr yield (+6.7bps) rose to 4.97% as discussed at the top. But there was a stronger performance at the front-end, where the 2yr Treasury yield (-0.5bps) posted a modest decline to 3.97%. At the same time, near-term Fed rate cut expectations continued to dwindle, with pricing of a rate cut by July falling to only 30%, the lowest this has been since the last cut in December. St Louis Fed President Musalem said that “tariffs are likely to dampen economic activity and lead to some further softening of the labor market” but also noted the potential risk posed by elevated inflation expectations. This morning in Asia, 10 and 30yr USTs are another couple of basis points higher with the 30yr hovering just below 5% …

21 May 2025 DB: It speaks for itself George Saravelos

We wrote last week that a widening gap between US Treasury yields and USD/JPY would be the single most important market indicator of accelerating US fiscal risks. The chart below speaks for itself: the JPY is strengthening even as US yields are rising. We consider this as evidence that foreign participation in the US treasury market is declining. To be sure, Japanese back-end yields have also risen strongly in recent days. Some have interpreted this as a sign of rising fiscal worries in Japan but we disagree. If this was the case the yen would be weakening and it is strengthening.

As we pointed out in our global macro framework last week, Japan has plenty of fiscal space given its positive net foreign asset position (figure 2). We would argue the JGB sell-off is a bigger problem for the US treasury market: by making Japanese assets an attractive alternative for local investors, it encourages further divestment from the US.

At the core of our views in coming months is that the market is becoming increasingly driven by external asset positions, and this is putting combined downward pressure on US bond markets and the USD. A metric for how concerned the market is about twin deficits is the beta (slope) of the NIIP/yield relationship in figure 2. This effectively gives us the global market price of deficits. Plotting this over time we show that it has been in a very well defined range since the Global Financial Crisis. We would argue the risks are shifting towards a bigger steepening of the line (effectively a widening in US - RoW differentials) and a reversion to the pre-2008 regime (figure 3). As we wrote in our FX Blueprint yesterday, a weaker USD is the release valve to America's twin deficit problem.

Netherlands calling … and has a few words on longer end which caught MY attention, esp ahead of today’s 20yr auction …

21 May 2025 ING Rates Spark: Long end pressured with Dutch pension reform on course

Without much data, the US fiscal story provides for a bearish bias as 10-year Treasury yields probe above 4.5% again. The 20y bond sale might garner more attention than usual in this context. EUR rates reacted with a steepening of the ultra-long curve as the Dutch parliament voted against an amendment that could have derailed the pension reform

… a domestic outfit out with some mid year outlooks and repeat after me, ‘narratives follow price’ and I’m NOT just saying it as if I don’t do the very same thing (all goofy charts above with TLINES etched in with real thick crayons …) … but what I am saying is these folks ARE some of the best in the biz and have the privilege of doing this — narrative creation — for a living!!

US risky and risk-free assets are attractive versus the RoW against a backdrop of a slowing but still expanding global economy despite policy uncertainty, along with deregulation and more rate cuts than priced in the markets. We are OW US equities, OW core fixed income, and expect a weaker dollar.

… G10 rates – eye of the storm: US Treasury yields should remain range-bound until 4Q25 when markets price in more Fed cuts in 2026. In the euro area, sluggish growth and external factors drive rates lower. We expect curves to get steeper in the US, UK, and euro area and flat in Japan. We see the UST 10-year yield at 3.45% by 2Q26.

…Key investment ideas In the US, we expect Treasury yields to remain range-bound until 4Q25, when we think that investors will grow more confident that rate cuts are coming. The Fed cuts rates by 175bp in 2026 – more than markets currently price. 10-year Treasury yields reach 4.00% by end-2025 and finish 2026 just above 3.00%…

We discuss the US policy path that underpins our mid-year economic and cross-asset outlook. Tariff escalation moved faster & along a different path than we expected, arriving earlier at the state we still expect to persist into 2026: higher tariffs in the aggregate, but skewed toward China. Fiscal and immigration policy impacts are progressing in line with our expectations.

The Bottom Line

Tariffs: We expected US tariffs in the aggregate to ramp over time in 2025 toward a state in which tariff levels would not only be skewed toward China, but also incorporate levies on Europe and product-specific tariffs, with USMCA products largely spared. This has happened, though much faster than expected and alongside a 10% blanket tariff. We expect geographic-focused current levels to persist, albeit with rolling deadlines and potential temporary escalations as negotiations unfold globally (i.e., China tariff levels hold around ~30%; EU faces escalation risk but willlikelybe maintained at 10%, in line with RoW). Product-specific, 25% Sec 232 tariffs (existing and those to be announced) will have more durability.

Taxes/Fiscal: We expect a modest incremental deficit (~$130b ex tariff revenue) from tax policy changes next year, when combined with underlying macro variables (mainly weaker receipts and higher scheduled outlays tied to inflation), reflecting ~7.1% of GDP. Expect TCJA extension + some incremental policy changes, offset by savings via spending cuts.

Immigration: Border crossings and deportations, both slower than prior estimates, balance out for a largely unchanged picture.

Deregulation: Rule re-writing continues to be a slow-moving process with more sectoral than macro impacts, though deregulation in the financials sector could eventually have ripple effects.

Global growth steps down by a percentage point from 2024. US trade policy and the uncertainty it engenders are the main drivers. Central banks have to confront the slowing, but the Fed must wait until inflation ebbs.

The broad imposition of tariffs by the US is a structural shock to the global trading order…

In our baseline outlook, we forecast a slowdown in global growth from 3.5% 4Q/4Q in 2024 to 2.5% in 2025…

\US President Trump urged Congress to pass the “big, beautiful” budget. An International Monetary Fund (IMF) official urged the US to consider its unsustainable debt level, which this budget will likely make worse. The redistribution effects of the tariffs, spending cuts, and tax cuts does have long term implications. In the short term, the deficit’s size is likely the focus.

Countries are not like casinos or hotel resorts—declaring bankruptcy is not really a thing. The US also has record amounts of wealth that could be mobilized to fund the debt. Fiscal concerns need to be considered within these constraints. The current angst may reinforce the position of fiscal conservatives in budget negotiations…

Covered wagon folks on DC shenanigans … and asking IF it will have a real impact …

May 21, 2025 Wells Fargo: Will Tariffs Spur a Resurgence of U.S. Manufacturing Jobs?

Summary The goals of the administration's trade regime changes are varied, but a resurgence of American manufacturing jobs is certainly a priority. By raising the cost of imported goods, tariffs encourage the consumption and production of domestically produced goods. Could higher trade barriers spur a rebound in U.S. manufacturing employment?

Status Quo: Interest in bolstering manufacturing employment is not new. The sector is associated with lifting droves of American workers into the middle class following WWII, but employment in the industry peaked in 1979 at just under 20 million workers.

Manufacturing employment totals 12.8 million today, or 6.7 million fewer jobs than its 1979 peak. The share of workers employed in the sector has subsequently shrunk to 8% from 22%.

While payrolls are down from their 1970s heyday, anemic labor productivity growth in the manufacturing sector has underpinned a rise in employment recently. Today, there are 1.2 million more manufacturing jobs than there were 2010.

Near Term: An aim of tariffs is to spur a durable rebound in U.S. manufacturing employment. However, a meaningful increase in factory jobs does not appear likely in the foreseeable future, in our view. Higher prices and policy uncertainty may weigh on firms' ability and willingness to expand payrolls.

As downstream industries face higher costs, they must decide whether to absorb them and accept lower margins, pass them onto customers via higher selling prices or a combination of the two. Neither avenue is supportive of employment growth.

Medium to Long Term: A meaningful increase in the share of factory jobs, while possible, would likely unfold over many years and come at high cost.

U.S. labor costs are a hurdle. Labor cost differentials with the rest of the world require U.S. manufacturing firms to be highly capital intensive to compete in a global marketplace. Thus, an expansion in manufacturing employment would require significant capital investment.

In order for manufacturing employment to return to its historic peak, we estimate at a minimum $2.9 trillion in net new capital investment is required. While sizable, we view this estimate as a lower-bound. The build out of new of capacity would likely unfold over multiple years, with further increases in capital intensity and inflation requiring a higher amount.

Assuming businesses are willing and able to invest such ample sums, questions over staffing remain. An already tight labor market for production workers coincides with slower labor force growth more broadly as lower fertility rates and, more recently, a reduction in immigration weigh on working-age population growth.

Increased take up of manufacturing-specific training programs will go a long way toward filling existing vacancies, but these training programs must keep up with the evolving nature of manufacturing. New jobs will require different skills than those previously lost.

May 20, 2025 Wells Fargo: The Fiscal Handbook: A Reconciliation Bill Is Born

Summary

The House of Representatives is weighing a Republican-backed plan to make sweeping changes to U.S. fiscal policy. In short, the bill extends the expiring portions of the 2017 tax cut bill and provides a shot of near-term fiscal stimulus in the form of additional, temporary individual and business income tax cuts, such as no tax on tips or overtime income. The bill also includes some new spending on certain Trump administration priorities, such as more funding for the military and border security.

These tax cuts and spending increases are partially offset by some tax increases and spending cuts for Medicaid, food assistance for lower income individuals, student loans and green energy tax credits, among other budget offsets.

On a current law baseline (i.e. assuming the 2017 tax cuts expire as scheduled), the bill increases the federal budget deficit by very roughly $2.3 trillion over the next 10 years. However, since the 2017 tax cuts extension costs a bit less than $4 trillion over that time period, the new tax and spend changes are deficit-reducing over the next decade relative to current policy.

However, there is a catch. Many of the tax cuts and spending increases are temporary and slated to expire after a few years, while many of the tax increases and spending cuts are phased-in slowly over time. Thus, the fiscal accommodation in the bill is generally front-loaded, while the fiscal tightening is generally back-loaded.

In the near term, the bill would generate new fiscal stimulus and increase the federal budget deficit by 0.5-1.0 percentage point of GDP per year over the next few years. Over the medium to longer term, the deficit impact is highly conditional on the decisions made by future policymakers.

If we include a 15% average effective tariff rate in this analysis, higher tariffs generate roughly 0.8% of GDP in new tax revenue per year, largely nullifying the near-term fiscal impulse from the reconciliation bill. That said, there is an important timing mismatch, with fiscal tightening from higher tariffs occurring today in real-time, and the peak fiscal easing from tax cuts still a year away.

Pulling it all together, we are forecasting neither a fiscal blowout nor a fiscal consolidation in the near term. Our base case forecast for the federal budget deficit as a share of GDP is in the 6.0%-6.5% range over the next few years, more or less in line with the current status quo but still well in excess of the 3% that the U.S. averaged over the half century preceding the pandemic.

The tailwinds from tax cuts and headwinds from tariffs are already largely baked into our U.S. economic forecast. On the margin, the House bill generates modest upside risk to our forecasts for U.S. economic growth, inflation and interest rates in 2026.

It is important to note that even if the House of Representatives passes this bill, the process is not complete. The Senate has yet to weigh in, and we expect alterations are coming from the upper chamber of Congress. That said, we think this bill lays the foundation for the final product.

Our sense is that August 1 is a key date by which the White House and Republican Congressional leaders aim to have the entire process completed. The bill includes an increase in the debt ceiling, and passing it by August 1 would ensure Treasury can meet its borrowing needs during the month-long recess Congress has scheduled for August.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Student loans an issue …

May 21, 2025 Apollo: Significant Headwinds to Consumer Spending

The Covid-motivated pause on reporting delinquent federal student loans has now ended. As a result, starting in May 2025, up to 10% of US households may face a steep decline in their credit score, see chart below. This means they will no longer be able to get a loan to buy a car, a house, or new furniture. Combined with tariffs and high uncertainty, this is a significant headwind to consumer spending over the coming months. See here for more discussion from the New York Fed.

You say ‘global bond crisis’ and clearly you’ve got MY attention …

Japan’s Bond market may prove the dead canary in the coal mine warning of an imminent systemic global bond crisis. Although US stocks have staged a “Terminal Lucidity” recovery – it may prove unsustainable as the shocks start to mount, and Japanese liquidity melts away.

Have you come across the term Terminal Lucidity? It describes the sudden apparent recovery of terminally ill patients just before they resume the downward slope towards death. I’m idly wondering if that’s what we’ve seen in the recent stock market rally…

Markets shook yesterday as the unstable tectonics of the Japanese Government Bond market rocked global bonds.

Yesterday Japan 40-year long-bond yields spiked to 3.6% – staggering for a nation that has had sub 1% yields for the past 35 years of ultra-low rates and proto-QE. The fact the Bank of Japan is now “tapering” its holding of 46% of the total JGB (Japan Government Bond) market, diminishing confidence in the wobbly government of Prime Minister Shigeru Ishiba, a p*ss-poor bond auction, rising concerns about the slowing economy, ongoing structural rigidities, and concerns Japan won’t placate Trump over tariffs (they have dared to argue back – refusing a trade deal unless it immediately undoes the 25% auto tariff), collectively have caused long bond yields to spiral upwards.

It’s a wake-up and smell the coffee moment for other sovereigns in the global bond markets…..

Positions. Lives. Matter. Traders gonna trade and haters gonna hate…

Updated on May 21, 2025 at 1:38 AM UTC Bloomberg: Traders Brace for Treasury 10-Year Yield at 5% as Mood Sours By Edward Bolingbroke

Traders are piling into bets that long-term Treasury yields will surge on concerns over the US government’s swelling debt and deficits, a situation made more precarious by President Donald Trump’s tax-cut bill.

The murky economic outlook is fueling hedging activity in Treasury options, with investors targeting higher rates on longer-dated bonds by the end of the year. The latest spurt of downside wagers echoes sentiment on Wall Street where strategists from Goldman Sachs Group Inc. to JPMorgan Chase & Co. are lifting their forecasts for yields.

Plays favoring the 10-year yield testing 5% are among some of the bigger positions. Monday’s CME open interest data confirmed a large wager on 10-year yields rising toward 5% in the coming weeks, indicating new risk for a heavy premium of $11 million. Over the past week, a trend of options flows hedging a move higher in yields has emerged, reflected in the so-called options skew, which shows rising premiums to reflect a bond market selloff.

“Given trade and monetary policy uncertainty amid a structural shift in the demand landscape, the risks are skewed toward bearish steepening over the near term,” JPMorgan strategists including Jay Barry and Jason Hunter wrote in a note.

On Monday, the 30-year yield briefly eclipsed 5% to reach its highest level since November 2023 before paring the move, during a selloff sparked by Moody’s Ratings cutting the US credit score to Aa1 from Aaa. The downgrade drove yields of all maturities higher in early trading Monday before wiping out increases.

“The bond market is going to have the final say on what happens fiscally,” Garda Capital Partners’ Tim Magnusson said in an interview at the firm’s New York office. Lawmakers “are going to get tested more — 5% is not the final line in the sand.”

Premiums to protect against bigger losses on the long-end of the Treasury curve are now at their highest level since April, when markets were shaken by the potential economic fallout from Trump’s aggressive trade policies. The current move in options skew means that traders are driving up the price of puts that hedge against the risk of a yield spike, relative to call options that would profit from the opposite.

Tuesday’s JPMorgan Treasury client survey also highlights the expectation for higher bond yields, with outright short positions climbing to the highest since Feb. 10. With investor positioning more neutral than in early April however, the JPMorgan strategists expect “significantly smaller moves than experienced last month.”

JPMorgan Treasury Client Survey

In the week up to May 19, investor outright short and long positions both rose by 2 percentage points, with neutrals dropping 4 percentage points. The shift took the outright short positions to the highest level since Feb. 10.

… and in light of CNN news and geopolitical tension noted above supplying a bid to ‘Earl, this next view is, well, timely and topical …

May 21, 2025 at 5:00 AM UTC Bloomberg: Macho Pessimists Say Inflation’ll Be Back Tariffs will bring it with an unblinking certitude; the only question is when.

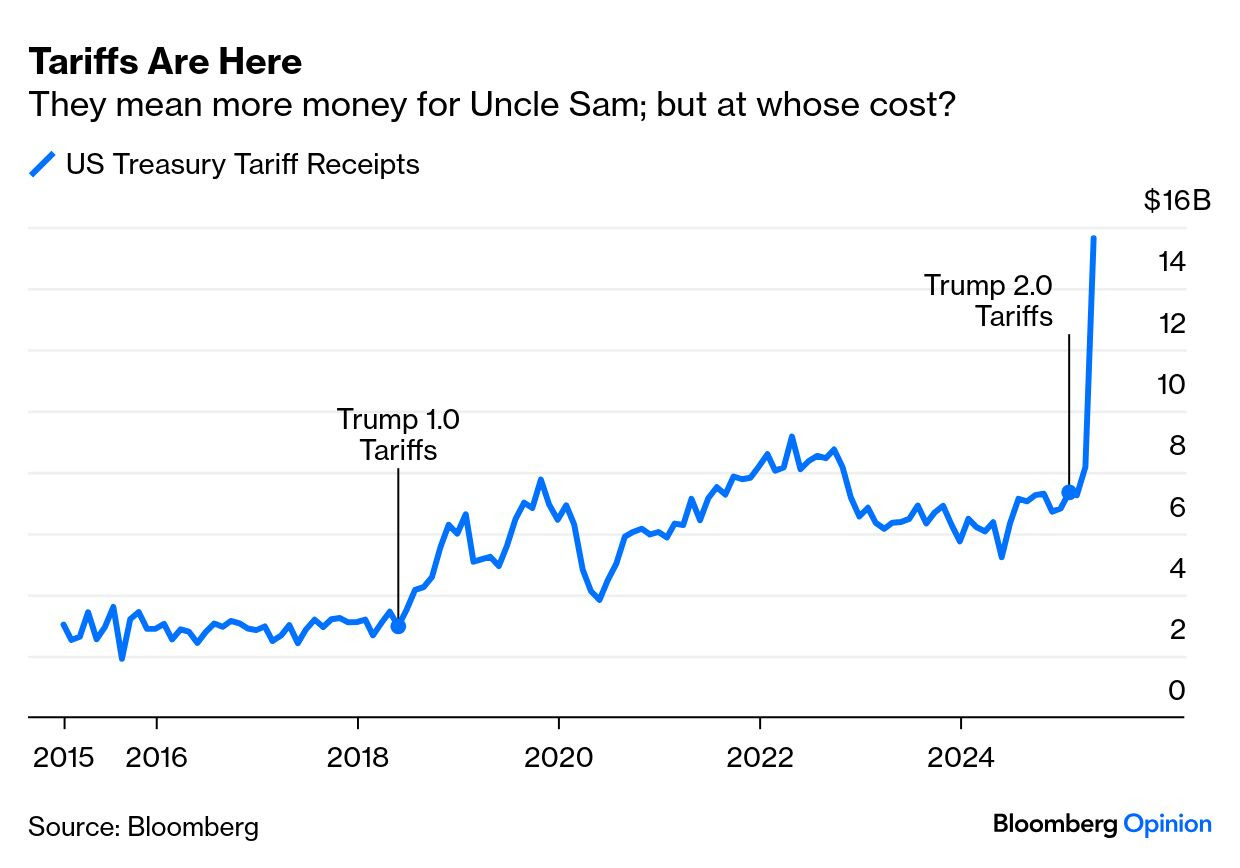

Tariffs and Prices

Where is the tariff inflation? A growing number of macho-pessimists are convinced, much like Arnold Schwarzenegger’s “Terminator,” that rising prices will soon be back. The US has been slapping tariffs on a range of imports for a few months, and that’s already shown up in a sharp increase in the money being paid in import duty:

That is real money for Uncle Sam, and it has been paid by someone. But who, ultimately, will bear the price? President Donald Trump’s weekend outburst against Walmart Inc. suggests that the issue is already politicized:

Between Walmart and China they should, as is said, “EAT THE TARIFFS,” and not charge valued customers ANYTHING. I’ll be watching, and so will your customers!!!

Those with long memories might recall Kamala Harris calling to ban price-gouging during the presidential campaign — retailers have enemies across the political spectrum. Walmart knows that, and also understands that its most crucial constituency is its customers (as Andrea Felsted points out). As a whole, companies have been using earnings conferences to prepare shareholders for tariffs to have a negative impact on profits, so they aren’t expecting to pass them all on to customers.

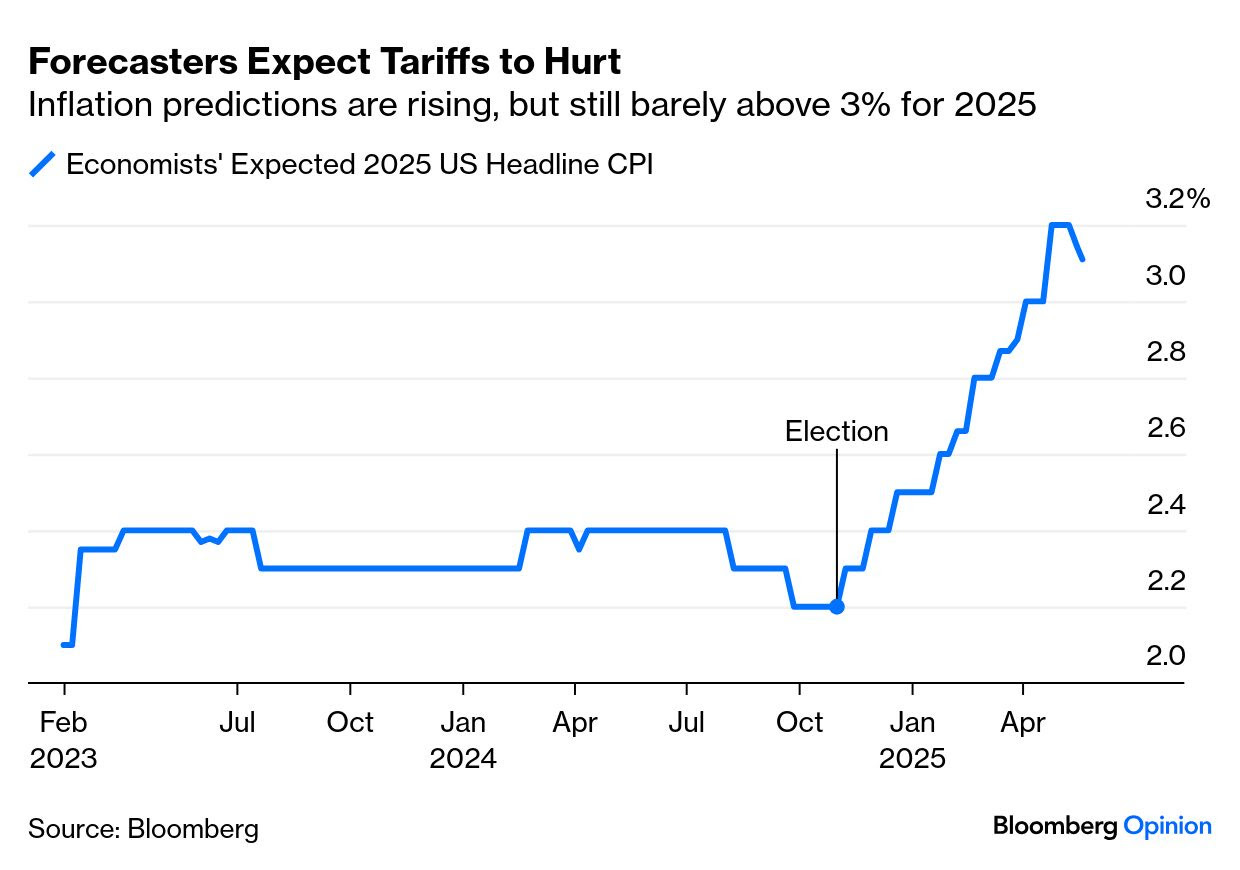

But there are limits to how much shareholders can eat. Economists seem convinced that customers won’t escape without paying “ANYTHING.” Bloomberg’s survey of professional forecasters shows CPI estimates ticking up ever since the election. They’re only a little above 3%, so this isn’t extreme, but the shift is clear:

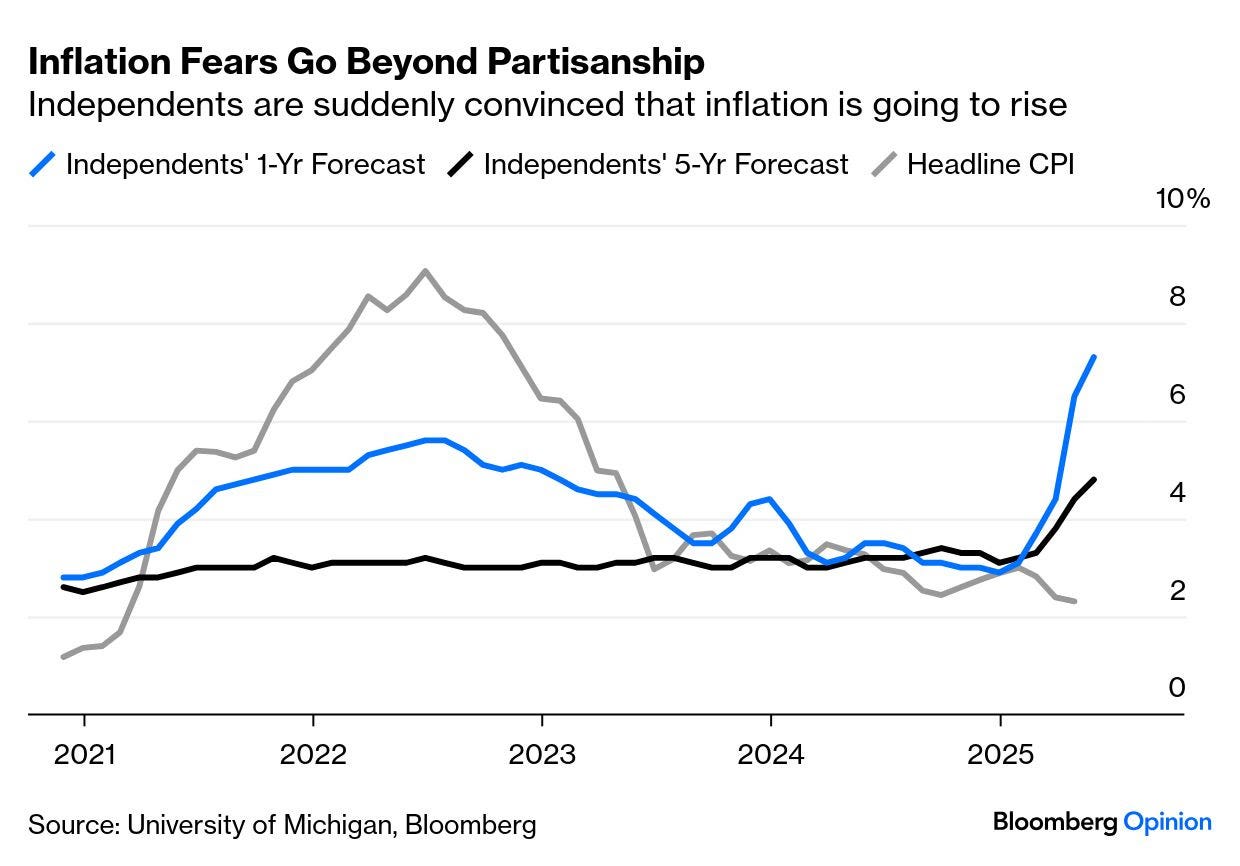

More alarming, for all concerned, is a form of inflationary machismo that has taken hold of the population…

…The depth ofdivision is disquieting. But Michigan also polls independents, who suggest something more worrying for the administration. Their forecasts have shot up since the election, even as actual inflation has fallen. Reasonable people, then, expect tariffs to cause inflation:

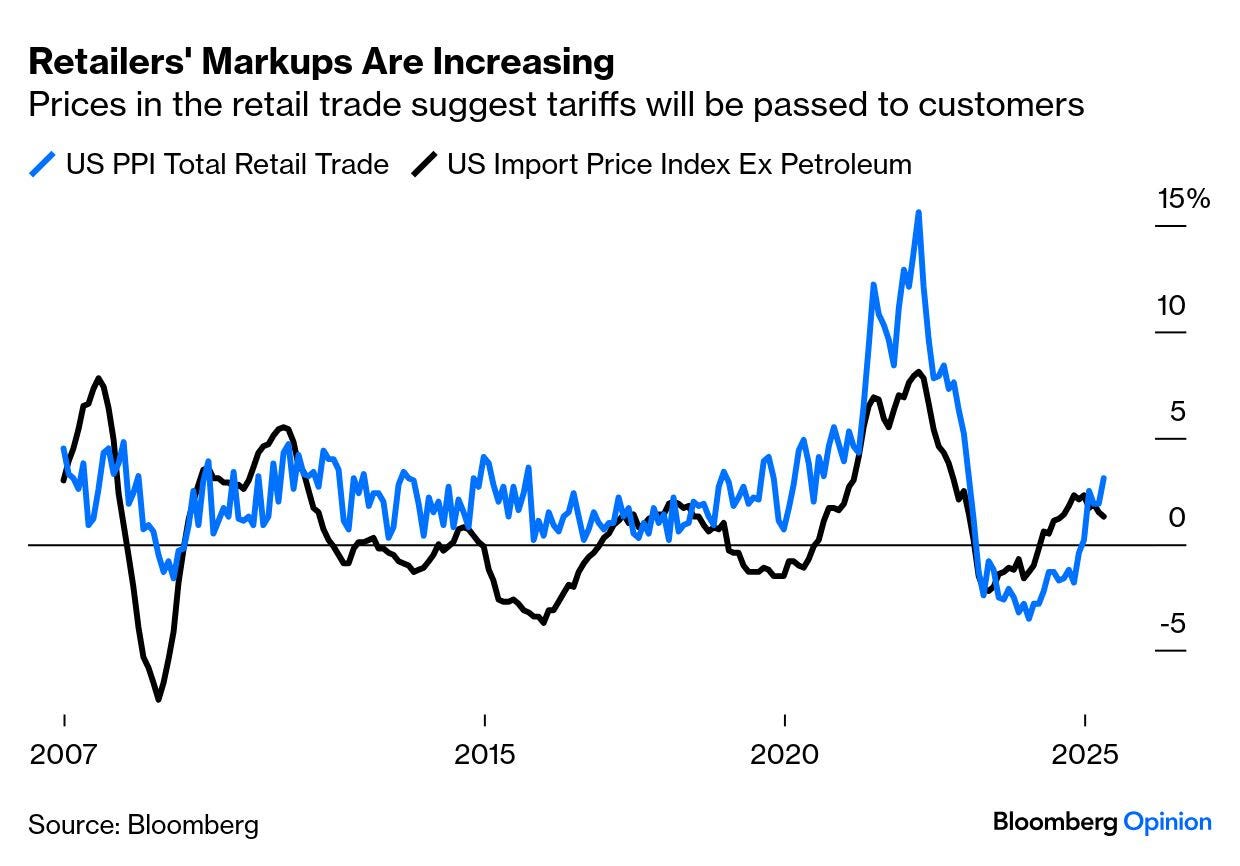

With tariff revenue already shooting upward, how then is inflation still falling? It does take a while for products to move along the supply chain. And there are now signs that retailers are beginning to increase markups to account for duties. Omair Sharif of Inflation Perspectives LLC offers this handy explanation:

Since the item sold to the consumer is typically a finished good (i.e. it does not undergo any transformation), the [Bureau of Labor Statistics] considers a retailer as a supplier of services. Thus the output of a retailer is measured by the difference between the sale price of the item and its acquisition cost. So, retail trade services indexes reflect a retailers’ margins.

With this in mind, the rise in retail trade producer prices measured this way is discomfiting — the highest since early 2023, with the bulk of the tariff shock still in the future:

What looks more encouraging on this chart is that import price inflation has declined slightly. Unfortunately, this doesn’t mean that tariffs won’t hit consumers, because US import prices exclude tariffs. Dario Perkins of TS Lombard in London says: “If Chinese exporters were absorbing them, US import prices would be falling much more sharply. Stability in these metrics means China ISN’T paying.” Apparently calm figures are a reason to expect the tariffs to show up in inflation soon…

… ever wonder WHY we’ve constantly run a trade deficit? if so, today’s yer lucky day…

One possible reason why the United States runs a trade deficit is that the imbalance reflects a macroeconomic phenomenon. Using national accounting, the author shows that deficits could be due to a persistent shortfall in domestic saving that requires funds from abroad to finance domestic investment spending. Therefore, reducing the trade imbalance would require both more exports relative to imports and a narrowing of the gap between saving and investment spending.

…Debating Trade Deficits An argument against running a trade deficit is that it requires U.S. assets that would otherwise have been held domestically to be sold to foreign investors. As a consequence, income generated by these assets flows out of the country instead of going to domestic investors.

The saving gap perspective tells a contrary story. Investment spending would have been lower if not for the United States being able to borrow from the rest of the world. One can argue that this funding raised the economy’s productive capacity from what it would have been otherwise.

Finally, achieving the goal of a smaller trade deficit will likely be painful, since it requires a recalibration of domestic savings and investment. Studieshave found that episodes of substantial reductions in trade deficits were typically facilitated initially by lower investment spending and subsequently through higher saving, as was the case with the improvement in the U.S. current account during the 2008 recession and its aftermath.

…and … NORM!! RIP to a rather large part of my childhood, esp having grown up in / around Boston …