CNBC: China strikes back with 125% tariffs on U.S. goods as trade war intensifies

China has retaliated against the U.S. President Donald Trump’s reciprocal tariffs by raising its levies on U.S. goods to 125% from 84%, the finance ministry said.

Trump administration confirmed to CNBC on Thursday that the U.S. tariff rate on Chinese imports now effectively totals 145%.

… AND meet the markets new boss … same as the old boss?

After being outta pocket YESTERDAY little bit of catchin’ up to do on THIS side … so, with stonks down yesterday, that get ‘47 off the hook for insider trading charges OR are we still crowin’ about that? CPI was what, that tree that fell in the forest and nobody there to hear IF it made a sound?

I’ll jump right in with a look at long bonds on heels of the auction …

30yy WEEKLY (w/daily inset): 5.00% back on the map …

… weekly momentum moved from overBOUGHT to somewhat less so while DAILY overSOLD levels coincide nicely with timing of 5.00% yield … shorter-term RENTAL longer term neutral?

… unsure if there’ll be an update over the weekend (passover) and sorry for that. Will try BUT no promises …

A few things which have caught MY eyes and likely more than already incorporated into the price action …

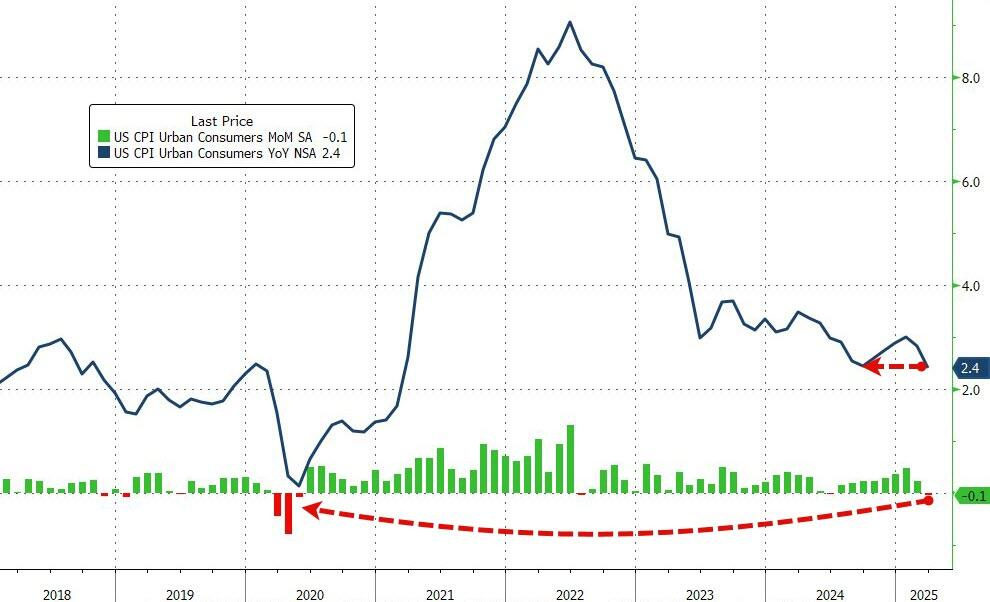

…Headline CPI FELL 0.1% MoM (vs +0.1% exp), which dragged the YoY CPI to +2.4%, matching the September lows...

ZH: Stellar 30Y Auction: 2nd Highest Direct Award, 3rd Biggest Stop-Through On Record

ZH: Stellar 10Y Auction Prices At 2nd Highest Stop Through On Record Despite Plunge In Directs

ZH: FOMC Minutes Confirm Fed Members Fear Trade Policy "Uncertainty", Support QT Taper

ZH: "Absolutely Spectacular Meltdown": The Basis Trade Is Blowing Up, Sparking Multi-Trillion Liquidation Panic

… at the end of the day (Wednesday), maybe the funniest thing I came across and which was directed at all us muppets …

ZH: Goldman Calls "US Recession" At 12:57pm; 73 Minutes Later Rescinds Recession Call

… simply cannot make this stuff up. Wondering if after Thursday's move back down, have we heard from Goldilocks? Recession back ON again? Someone like to arrange wellness check 200 West St

Need any more proof that narratives follow price?

I’ll quit while I’m behind as the situation REMAINS fluid and there’s lots below from Global WALL and the intertubes \… here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: DXY slumps & havens lifted after China raises tariffs on US goods to 125% … Bonds lifted by China's latest retaliation but remain on track to end the week with significant losses … A softer start to the day but one that leaves USTs just off the overnight 110-01+ trough, a low which printed as the benchmark faded initial strength on Thursday despite a strong 30yr tap. Action occurred as the risk tone stateside began to lift and as the yield curve steepened further. Only a modest uptick in USTs to the latest additional Chinese tariffs, keeping them within the existing 110-01+ to 110-15 band.

Yield Hunting Daily Note | April 9, 2025 | The Rollercoaster Continues, Starting To Nibble More, Indiv Munis

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

CPI clouds gathering …

10 April 2025 Barclays: US CPI Inflation Monitor (March CPI): While the storm clouds gather

Core CPI decelerated to 0.06% m/m (2.8% y/y) in March, helped by core goods and services prices. We think the inflation trajectory moves up from here amid tariffs. Our year-end core CPI forecast for 2025 is unchanged, at 4.1% y/y, but we mark our 2026 core CPI forecast lower, to 2.7% y/y.

10 April 2025 UPDATE: March CPI: Good, but likely short-lived

Core CPI slowed further, to 0.06% m/m (2.8% y/y), amid deceleration in both core goods and services prices. Headline inflation also benefited from a drag from energy prices, and declined 0.05% m/m (2.4% y/y). Our core PCE translation stands at 0.17% m/m (2.6% y/y).

AND a look at FOMC mins …

9 April 2025 Barclays: Federal Reserve Commentary: March FOMC minutes: RIP employment 'shortfall'

The minutes of the March FOMC meeting reaffirm that participants are in no rush to adjust policy rates. Amid the review of its monetary policy framework, the FOMC is seemingly changing its focus from employment "shortfalls" to "deviations" of employment from its maximum level.

Here’s a look at an EQUITY market review … you’ll see why I care with this excerpt …

11 April 2025 Barclays: Equity Market Review Reprieved, but not liberated

The Trump put may provide a floor to equities. But erratic policy/governance likely cap the upside, as an edgy treasury market and weaker dollar undermine confidence. In Europe, progress on German coalition talks supports a positive narrative for domestic plays, but beware of the surging eurusd.

… If the treasury market goes wrong, everything goes wrong. Given the growth damage likely done by the tariffs mess, some investors we speak to are hopeful that the Trump administration will focus on delivering stimulus sooner than later (think tax-cut bill). But fiscal headroom is limited, and our fixed income strategists believe that concerns about inflation hamstringing the Fed, and reassessment of term premium higher due to worries about foreign demand/outright sales will keep pressuring long-end rates (Help wanted, 9 April). In fact, despite a lower than expected CPI release on Thursday (March CPI: Good, but likely short-lived, 10 April), the March FOMC minutes reinforced the message that the Fed is in no hurry to cut rates, given lingering uncertainty clouding the economic outlook (March FOMC minutes: RIP employment ‘shortfall’, 9 Apr). This conundrum curtails bonds' ability to hedge equities, with the rates/stock correlation turning positive since Liberation day. More worrisome, rising US yields and a falling USD is a bad cocktail, which is reminiscent of the UK budget crisis of 2022 and likely prompted the Trump pivot this week. And given how central the treasury market is to financial stability, it was no surprise this week to see investors' focus shifting to credit risk. Our high quality balance sheet basket strongly outperformed the low quality balance sheet basket, as credit spreads widened sharply. With macro uncertainty unlikely to dissipate anytime soon, balance sheet quality is likely to become more discriminant for stock picking, in our view…

… The key caveat to Powell’s wait-and-see approach comes in the form of market functioning and systemic risk – which was much more worrying earlier in the week as positions were liquidated and deleveraging was the theme. The more obvious risk was that Trump’s trade war caused overseas investors to step away from this week’s auctions. The results of 10s and 30s served to significantly ease these concerns. Typically, the market wouldn’t know the magnitude of foreign participation in the auctions until the Treasury Department releases the allotment data (April 23rd in this case) – although attempts to extrapolate participation based on the indirect and direct awards invariably occur. This episode is different because of the Treasury Secretary’s comments at Thursday’s cabinet meeting. Specifically, Bessent said, “The bond auction went well yesterday. We had a lot of foreigners show up… showing that the US is still the best place to invest.” …

From France … A CPI recap, a reminder that it could always be worse AND … a position UPDATE (long closed…)

Although in large part driven by significant declines in airfares and hotel prices, March’s lower-than-expected CPI reflects a US inflation trajectory that was likely headed toward 2% y/y if not for recently announced tariffs.

While we observed fewer tariff-driven price increases than expected, the report still showed some initial signs of this impact.

Our preliminary March forecast for core PCE stands at 0.14% m/m.

10 Apr 2025 BNP US: Things could get worse from here

KEY MESSAGES

Following the Trump administration’s pivot on tariffs, our base case for the US is near-zero growth, elevated inflation and an on-hold FOMC. Achieving this moderate path depends critically on the White House sharply reducing tariffs on China near term.

We assign a 25% probability to a significant recession. The FOMC would likely respond to a material increase in unemployment with rate cuts.

We assign a 15% probability to a stagflationary environment with unanchored inflation expectations. This scenario could result in at least 100bp of rate hikes – something we think is currently an underappreciated risk.

09 Apr 2025 BNP US rates: A self-propagating rise in yields?

KEY MESSAGES

There are many technical and fundamental reasons behind the rise in Treasury yields. We think the biggest issue will be the perception about Treasuries turning out to be a poor hedge against recession risks.

The 10y and 30y auctions in the next two days will be crucial checkpoints to see if yields stabilize or become unhinged – risks of a Liz Truss Moment in Treasuries has gone up

We think the Fed ends QT in June, but an earlier intervention for market function (read QE) may be required if yields rise unabated. A bond vigilant administration can speed up moves towards SLR changes, and guide towards lower Treasury supply.

We closed our long 10y UST, and suggest being neutral on duration and curve.

…Selloff potential driver 4: A pension rebalancing or 60-40 rebalancing. For a 60-40 portfolio, the sharp decline in equities and strong performance of fixed income after Liberation Day may have thrown the portfolios completely out of balance, requiring the need to either add equities or sell duration. It is possible such rebalancing may have led to selling in long-duration Treasuries.

Similarly, for defined benefit pension funds, a fall in equities and an increase in fixed income may have meant a worse net funding ratio. In such cases, pensions can rebalance by adding equities or selling fixed income, which can show up in late-day rebalancing trades.

Calm before the tariff ‘flation storm, they say …

10 April 2025 DB: March CPI recap: Calm before the tariff storm

Both headline (-0.05% vs. +0.22% in February) and core (+0.06% vs. +0.23% CPI came in much softer than our expectations. The year-over-year rate for headline fell four-tenths to 2.4% while core fell by three to 2.8%. Shorter-term trends in core improved, with the three- and six-month annualized change falling six-tenths, both to 3.0%

In terms of the breakdown within the expenditure basket, core goods prices declined by a tenth and showed little evidence of price pressures from the early rounds of tariffs. Nor did there seem to be much of a price effect from the pull forward of demand for vehicles. On the services side, large declines in lodging away and airfares contributed to much of the softness on the services side.

The readthrough into core PCE is not as large. Continued strength in food away inflation will feed through into core PCE while the weakness in CPI airfares will not. As such, the details in tomorrow’s PPI will be heavily scrutinized. We are tracking 0.15% for March core PCE, which would be consistent with 2.6% year-over-year.

With respect to the near-term outlook, the biggest risk remains tariff policy. As of yet, we have not incorporated the recent tariff actions into our forecast. However, should these measures remain in place for a significant period of time, back of the envelope calculations suggest they could shave 1 - 1.5 percentage points from growth this year – meaningfully raising recession risks – while adding a broadly similar amount to core PCE inflation (see "Tools of the trade war could top up inflation while tanking growth").

The textbook response for the Fed to price level effects is to “look through” the shock. However, discerning in real time how much of any price increases are a function of tariffs and how much are organic price pressures will be difficult, especially with some evidence that inflation expectations may not be reliably anchored.

AND a development worth watching, brought forward from a very EARLY morning REID …

… Despite the risk-off tone, we sawa renewed bond market sell-off, with 10yr Treasury yields closing +9.2bps higher at 4.43% and 30yr yields +13.3bps at 4.87% . Higher yields came as the House narrowly passed the Senate-approved budget outline that envisages cutting taxes by up to $5.3 trillion over a decade, in exchange for only minimal spending cuts. The bond sell-off continued during the US afternoon despite a brief rally following a solid 30yr auction that saw $22bn of bonds issued at 4.813%, -2.6bps below the pre-sale yield. 30yr yields are another +2bps higher this morning, and on course for a +48bps weekly increase, which would be their largest since the 1980s. So there is some déjà vu of the bond market moves that Jim highlighted in his “Danger Zone” CoTD on Wednesday morning (link here) and which were followed by President Trump’s pullback on reciprocal tariffs. As a reminder, our head of US rates strategy Matt Raskin discussed the conditions under which the Fed might intervene to preserve market functioning in a note on Wednesday.

Treasuries had actually rallied earlier on yesterday following a very soft US CPI print for March. Headline inflation (-0.1% mom vs +0.1% expected) saw its largest monthly decline since early Covid restrictions in spring 2020, while core inflation (+0.1% vs +0.3%) saw its smallest monthly rise since January 2021 with the data showing little evidence of price pressures from the early rounds of tariffs. Our US economists did note that the read-through into the Fed’s preferred core PCE measure was not as weak as the headline CPI readings and they will be keeping a close eye on today’s PPI print. See their full reaction here.

The weaker inflation data saw investors increase their expectations for rate cuts, with a 25bps Fed cut being again fully priced in by the June meeting. The Fed pricing did reverse slightly as a host of Fed speakers signaled continued patience on future cuts. Boston Fed President Collins said tariff-related inflation could further delay rate cuts, Chicago Fed President Goolsbee noted that the bar for adjusting rates was a “little higher” with the stagflationary shock from tariffs and Kansas Fed President Schmid said he “would be hesitant” to view the effects of tariffs on inflation as temporary. But with a risk-off tone continuing overnight, the amount of Fed cuts priced by year-end is back up to 92bps this morning, from 80bps this time yesterday …

Victory lapping … dunno … doesn’t seem appropriate but then again, maybe it is …

April 10, 2025 First Trust: 5,200 Target Hit but Still Overvalued? A Look at the Cap Profits Model

The past few weeks have been turbulent, to say the least. A wave of newly implemented U.S. tariffs has served as the catalyst for a broad repricing in equities — and there’s a real possibility that stocks could fall further. That said, valuations were stretched even before the tariffs. If it hadn’t been tariffs driving the pullback, it likely would have been something else. This is exactly why we expected 2025 to be a more challenging year for markets. Last Friday, the S&P 500 Index touched our year-end target of 5,200. So, where do we go from here? In today’s “Three on Thursday,” we revisit our Capitalized Profits Model, a framework we use to gauge fair value for the S&P 500 Index. It’s important to note that this is a valuation tool, not a market timing indicator. An overvalued reading doesn’t mean stocks will immediately fall, just as undervaluation doesn’t guarantee a rally. For a deeper dive, see the chart and two tables below.

10s TO 4.50% …

10 April 2025 ING Rates Spark: US yields not for turning, so spreads widen

Our impression from here is the 10yr Treasury yield will have a tendency to head for the 4.5% area, potentially with a view to thinking about 4.75%. In the Netherlands, Dutch pension funds will no longer be required to organise a vote to transition in the latest proposal – important; we explore further...

A better-than-avg recap of Thursday AND some CPI thoughts…

April 10, 2025 MS: Global Macro Commentary: April 10

Optimism following tariff reprieve fades; miss in US CPI supports front-end UST rally; 30y USTs cheapen further; broad based USD weakness; China yields stable despite tariff hike; RBA's Bullock says its too early to determine rate path; DXY at 100.95 (-1.9%); US 10y at 4.425% (+9.3bp)

… Soft US March inflation with Core CPI rising just 0.06% m/m (C: 0.3%) and an unexpected cooling in core services (ex shelter); the CPI miss supports a front-end UST rally (2y: -5bp).

Long-end USTs extend their recent weakness (30y: +13bp) despite a solid 30y auction that comes 2.6bp through, further weighed down by fiscal concerns as the tax bill moves through the legislative process …

April 10, 2025 MS: US Inflation Monitor: March CPI: Temporary weakness

CPI came in below expectations, with core rising by 0.06% m/m (MS: 0.23%) and headline by -0.05%. This leaves core up3.0% and headline up 2.5% y/y. Incorporating inputs from CPI, we now forecast core PCE inflation increased 0.14%m/m in March, bringing the 12-month pace to 2.58% y/y.We will update our forecasts after PPI tomorrow. Despite this soft print, we think inflation will start to accelerate in May/June due to tariffs.

CPI inflation decelerated more than expected from the February print. The downward surprise is mostly explained by: (i) airfares with another very weak consecutive print (-5.3%m/m), (ii) hotels coming down at -3.5% m/m, and (iii) a negative print in car insurance. The weak airfares and hotel plans could be a sign of services consumption weakness, Note, however, that the negative airfares prints might just reflect industry-level issues. Airfares increased more than 10% in 2H24 mostly due to supply issues, and the consumer may be just reacting to higher relative prices…

… There are no clear signs of tariffs pushing prices yet. New cars accelerated but little. Goods with a high share of Chinese imports showed mixed evidence; apparel and appliances decelerated, and furniture and information technology commodities both ticked up.

AND same firm here with a look at the ECONOMIC week ahead …

We retain our outlook for sluggish growth, firming inflation and a Fed on hold in 2025. The outlook received some good news with a delay in reciprocal tariffs, but trade barriers between the US and China have been set at exceptionally high levels. How long can trade volumes hold up?

Key takeaways

The White House delayed reciprocal tariffs for 90-days, opening the door for negotiations to lower tariff rates for non-China trading partners.

That said, this merely extends policy uncertainty and the effective tariff rate of 23% is the highest it has been in a century.

Applying 145% tariffs on imports from China, while they apply an 84% tariff on their imports from the US, risks a sudden stop in trade flows.

… For now, we maintain our baseline outlook for sluggish growth, firming inflation, and a Fed on hold. We expect real GDP growth of 0.6% in 2025 (Q4/Q4) and 0.5% in 2026 on decelerating growth in consumption, nonresidential fixed investment, and net exports. We look for headline and core PCE inflation to firm to 3.5% and 4.0% by year end, with the peak impulse is in Q3 2025. A key component of our Fed-on-hold view is that immigration restrictions slow growth in the labor force and keep the unemployment rate low even as growth decelerates.

In this setting, looking through inflation is easier said than done. Inflation diverges more from the 2% target in our outlook than does employment from maximum employment. As a result, we think the right answer is for the Fed to wait in its current stance for longer. We look for no rate cuts from the Fed in 2025 and only expect a rate cutting cycle to begin in March 2026. We think the Fed will cut gradually – 25bp at every meeting thereafter – to balance a still-low unemployment rate and above-target inflation. We expect a terminal rate of 2.50-2.75% reached in late 2026. That said, we think risks to the outlook for activity remain skewed to the downside. For the Fed, this would imply an earlier onset of policy easing…

Those to the North on OUR ‘flation …

April 10, 2025 RBC: Tariffs could quickly reverse March U.S. CPI downside

The Bottom Line: Today’s U.S. inflation print is stale in the context of tariffs. Yesterday’s 90-day pause on the most severe tariff hikes on regions outside of China provided some immediate relief. But import tariffs are still much higher than a week ago and we are still assuming significant upward pressure on inflation in the coming months. This morning’s print gives us a starting place (or a jumping off point) - and with core at 2.8%, that starting place is much better than we were expecting.

Notwithstanding ‘reciprocal’ tariffs, there are three key themes continuing to play out in the CPI data – we were already losing out on the benefit of goods deflation (in the absence of tariffs, this would have made getting to the Fed’s inflation target harder than before), a surge in auto prices will follow if tariffs on motor vehicles stick. And the downtrend in shelter price growth will end. Add these themes into the mix with tariff-driven core goods inflation, and we expect price growth to accelerate in the coming months.

US President Trump’s administration clarified the 125% tax on imports from China was 145%. This increase will not shift demand patterns (it will cost US consumers more money). For investors, this raises policy competence questions again. A well-planned trade tax would consider costs. Tax rates set seemingly at random question whether costs are properly considered.

US Treasury Secretary Bessent said that they saw nothing unusual in yesterday’s market moves. The 30-year Treasury yield experienced the biggest increase snice 1982, equities are falling, the dollar is falling, and gold hit an all-time high. Economists might consider this pattern not entirely usual.

The US House of Representatives passed a substantial deficit-financed tax cut (Senate reconciliation follows). Bond market vigilantes might not be in the mood for substantial deficit-financed tax cuts. A Supreme Court decision may mean the president could fire members of the Federal Reserve in the future. Bond market vigilantes might not be in the mood for a politically-run central bank…

Covered wagon folks on CPI …

April 10, 2025 Wells Fargo: March CPI: Sunset in the Rearview Mirror

Summary The CPI data were unexpectedly soft in March and give the FOMC a bit of breathing room as policymakers grapple with the appropriate stance of monetary policy amid significant economic uncertainty. Consumer prices declined 0.1% last month, the largest monthly drop since May 2020. A 6.3% decline in gasoline prices helped push headline inflation into negative territory. But, even excluding food and energy, the March inflation data were quite cool. Core CPI rose 0.1% (0.06% unrounded), the smallest increase since January 2021. Big declines in some of the more volatile travel-related components contributed to the slowdown, with deflation for airfares (-5.3%), lodging away from home (-3.5%) and used autos (-0.7%). Our initial read on the pass through to the core PCE deflator, the Fed's preferred inflation metric, suggests a 0.1% print in March when the data are released in a couple of weeks.

Taking a step back, gradual progress on the inflation front has continued in recent months, despite the frustratingly slow pace of improvement and the periodic bumps in the road. The core CPI has risen 2.8% over the past year, a four-year low and 100 bps lower than the rate that prevailed one year ago in March 2024. The question facing FOMC officials is whether inflation will start rising again in the face of a historic increase in the average tariff rate on U.S. imports. Even with President Trump's 90-day pause on reciprocal tariffs, the numerous other tariff increases (10% universal + 125% on China + steel, aluminum, autos, etc.) leaves the average effective tariff rate at the highest rate in a century. As discussed in our April U.S. Economic Outlook, our current working assumption is that the year-over-year rate of core CPI will be back to nearly 4% at the end of the year.

Our expectation is that when push comes to shove, the FOMC will cut the federal funds rate to limit damage to the labor market, even if inflation moves higher in the months ahead. We project the federal funds rate to be 125 bps lower by the end of the year amid a modest rise in the unemployment and economic growth that is near zero for the year.

Dr Bond Vigilante weighing in on … bond vigilantes …

Apr 10, 2025 Yardeni: Bond Vigilantes Remain Unhappy

It was not a happy day in the bond market. Neither was it a happy day in the stock market:

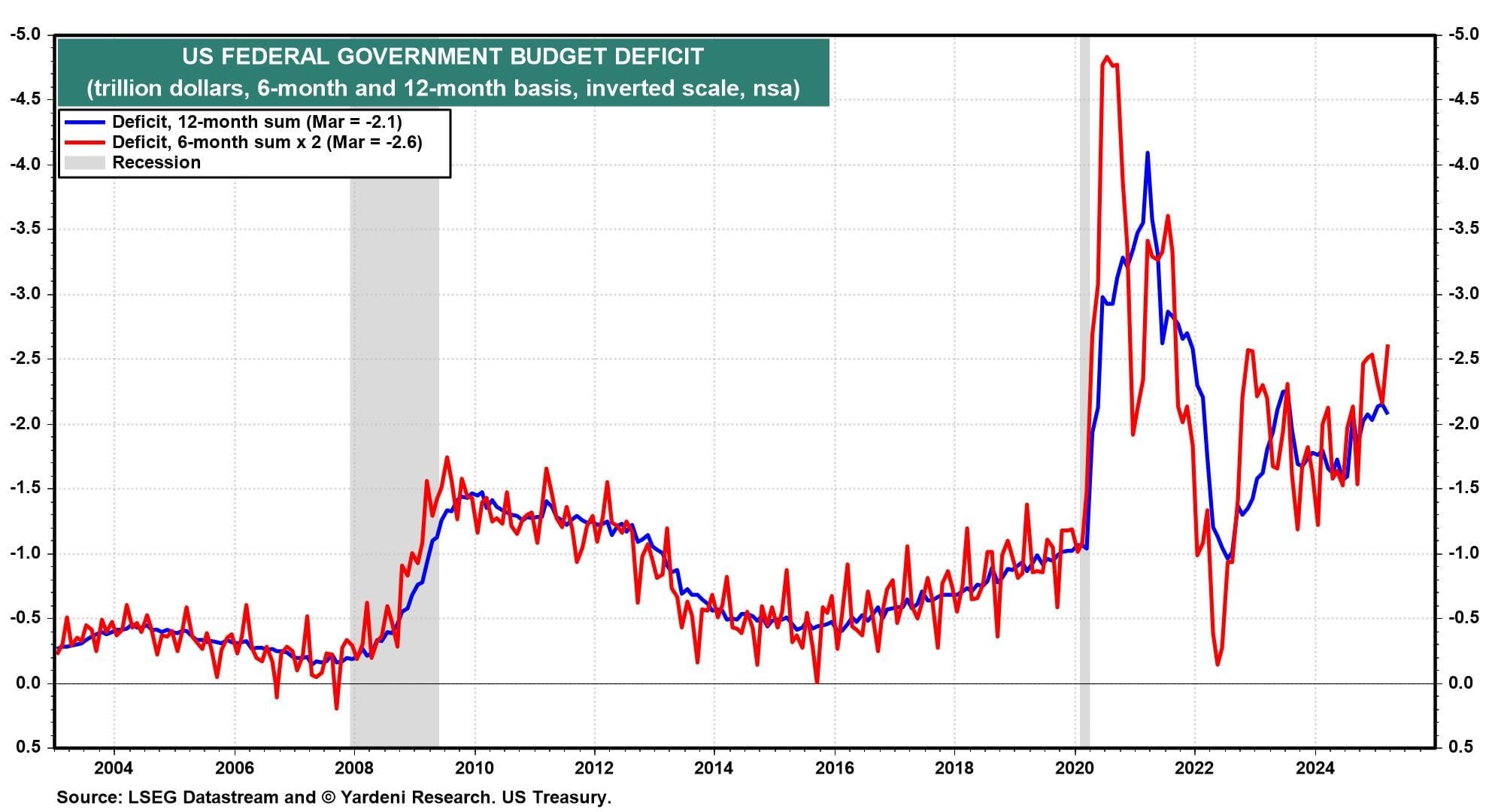

Bond Market. The 10-year Treasury bond yield rose to 4.45% this evening, up from a recent low of 4.01% on April 4, two days after Liberation Day. Yesterday, President Donald Trump partially postponed Liberation Day because the bond market was "tricky." It remained tricky today. Yields rose even though the March CPI inflation rate reported this morning was lower than expected. The Treasury reported today that the federal budget deficit totaled $2.1 trillion over the past 12 months (chart). It was $2.6 trillion over the past six months at an annual rate.

Stock Market. After one of the best one-day performances on record yesterday, the major US stock market price indexes fell more than 4% despite upbeat economic news (chart). Trump Tariff Turmoil (TTT) hasn't been significantly reduced by the President's 90-day postponement of reciprocal tariffs. The now 145% tariff on China will make various imports too expensive and disrupt business operations. Public and private companies will have to find new suppliers, reduce margins, and raise prices. The 25% tariff on auto imports will drive up their prices significantly along with the cost of auto insurance.

Apr 9, 2025 Yardeni: Bond Vigilantes Hit Another Homerun

"Bond investors are the economy's bond vigilantes. ... So if the fiscal and monetary authorities won’t regulate the economy, the bond investors will. The economy will be run by vigilantes in the credit markets.” – Ed Yardeni, 1983

"I used to think that if there was reincarnation, I wanted to come back as the President or the Pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody." – James Carville, 1993

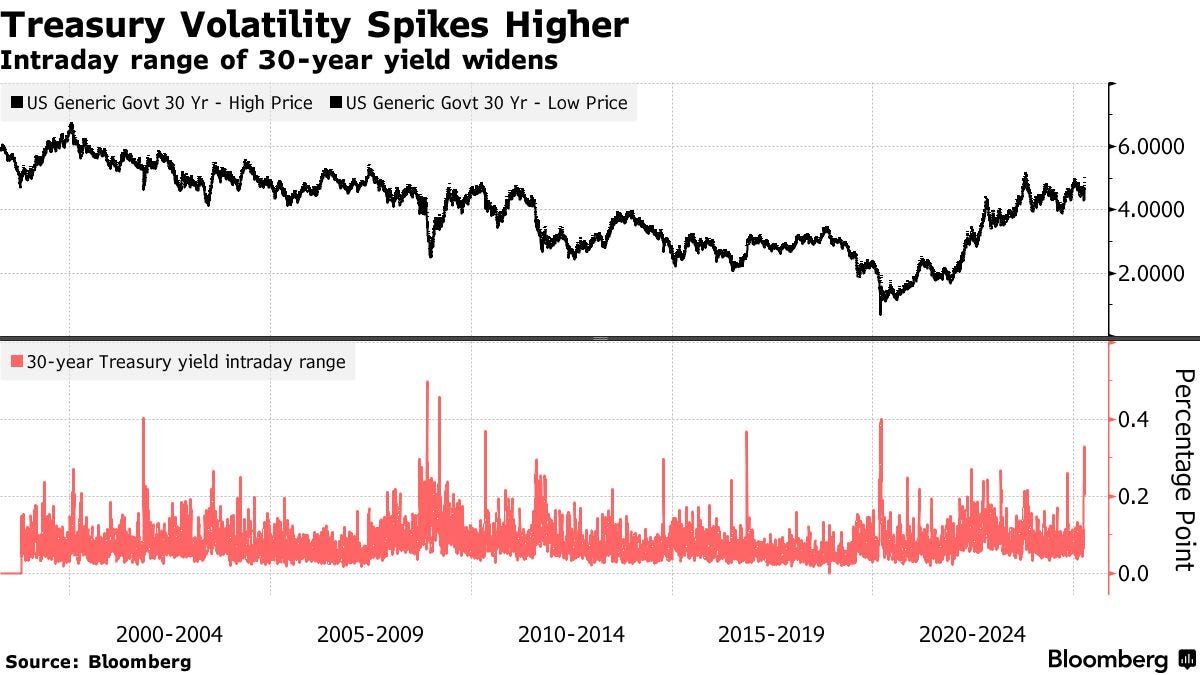

The Bond Vigilantes have struck again. As far as we can tell, at least with respect to US financial markets, they are the only 1.000 hitters in history. Even though the Stock Vigilantes were clearly telling President Donald Trump that his tariff policy was misguided late last week, his advisers touted falling oil prices and bond yields as ultimately helping Main Street America. That changed as the 10-year Treasury yield surged 34 bps from below 4.0% on Friday to nearly 4.34% today (chart).

After ratcheting back all reciprocal tariffs to 10% for at least 90 days (and upping the pressure on China to a greater than 100% tariff), Trump said today: "I was watching the bond market. The bond market is very tricky, I was watching it. But if you look at it now it's beautiful. The bond market right now is beautiful…. I saw last night where people were getting a little queasy." Trump also said he listened to JPMorgan CEO Jamie Dimon's interview this morning with Fox's Maria Bartiromo, where Dimon said a recession was likely and the bond market was sending bad signals about stress in the financial plumbing.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Question on EVERYONES MIND once again identified with some possible answers …

April 11, 2025 Apollo: Why Are US Long-Term Interest Rates Moving Higher?

The textbook would be saying that when the stock market is going down, long-term interest rates should also be going down.

But this is not what is happening at the moment, see chart below.

What could be the reasons why long-term interest rates are moving higher when the stock market is moving lower?

1) With the yen, euro, and Canadian dollar strengthening at the same time, this could be foreigners selling US Treasuries.

2) With the VIX at elevated levels around 50, there is a lot of hedging activity going on, and it could, therefore, be risk reduction among large asset managers managing rates, credit, and equities.

3) With almost $1 trillion in the basis trade, it could be an unwinding of the basis trade among levered hedge funds.

The answer is likely some combination of these three forces.

Want excitement of trading stocks without trading stocks? How about trading BONDS then …

April 11, 2025 at 2:50 AM UTC Bloomberg: Treasuries Suddenly Trade Like Risky Assets in Warning to Trump

Billed on Wall Street as so rock-solid safe they’re risk-free, US Treasury bonds have long served as first port of call for investors during times of panic. They rallied during the global financial crisis, on 9/11 and even when America’s own credit rating was cut.

… Yields, especially on longer-term debt, have surged in recent days while the dollar has plunged. Even more disconcerting is the pattern of the recent market moves. Investors have often dumped 10- and 30-year Treasuries — pushing prices down and yields up — at the very same time they frantically sold stocks, crypto and other risky assets. The inverse is also true, with Treasuries rallying in unison with them.

They are trading, in other words, a little like a risky asset themselves. Or, as former Treasury Secretary Lawrence Summers says, like the debt of an emerging-market country. Even if this dynamic was to fade as swings in stocks eventually normalize, as most analysts expect, a message has been delivered to policymakers in Washington: Investor confidence in US bonds can no longer be taken for granted — not after a years-long borrowing binge that swelled its debt load and not with a president in the White House hell-bent on rewriting the rules at home and abroad and antagonizing, in the process, many of the country’s biggest creditors.

This has profound implications for the global financial system. As the world’s ‘risk-free’ asset, Treasuries are used as a benchmark to determine the price of everything from stocks to sovereign bonds to mortgage rates while serving as collateral for trillions of dollars of lending a day.

Treasuries and the dollar get their strength from “the world’s perception of the competence of American fiscal and monetary management and the solidity of American political and financial institutions,” said Jim Grant, founder of Grant’s Interest Rate Observer, a widely followed financial newsletter. “Possibly, the world is reconsidering.”

Stocks, bonds and dollar all tumbled in unison Thursday, adding to concerns that foreign investors are retreating from US assets en masse. Thirty-year Treasury yields surged 13 basis points to 4.87%, while the dollar plunged against the euro and Swiss franc by the most in a decade. The widespread selloff extended on Friday.

“Treasuries are not behaving as a safe haven,” said ING rates strategist Padhraic Garvey. “If we were to slip into recession there is a path there for yields to revert lower. But the here and now is painting Treasuries as a tainted product, and that’s not comfortable territory. Treasuries have proved to be a pain trade too.”..

China behind the move higher in yields?

April 11, 2025 at 3:31 AM EDT Bloomberg: Bond Analysts Debate If China Had Role in Treasuries Swings

(Bloomberg) -- After a week of wild swings in the US bond market, China’s holdings of Treasuries are increasingly under scrutiny from analysts around the world.

Some have gone as far as suggesting — without hard evidence — that sales by Beijing may have helped fuel the biggest surge in 30-year yields since the pandemic and subsequent volatility. Others debate whether China might turn to dumping US debt in the future as a response to the steepest American tariffs in a century.

“China may be selling Treasuries in retaliation,” wrote Ataru Okumura, a senior interest-rate strategist at SMBC Nikko Securities in Tokyo, in a note to clients. Should this be the case, China has an incentive to show “it won’t hesitate to cause turmoil in the global financial market in order to improve its negotiating power against the US.” …

… Holdings have steadily fallen to the lowest since at least 2011, according to the figures from the US Department of the Treasury in January. However, the picture is muddied by the fact that holdings belonging to countries like Belgium are seen as linked to custodian accounts in China and have climbed …

Spreads. At. RISK …

Bloomberg: Credit is *the* market to watch to gauge the market and economic impact of the trade war

Markets have a had a reprieve as a pause in tariffs to most countries was announced, but tariff rates are still set to be higher than they have been since the 1930s

Credit will be central to the real-world impact. Corporate cash flows closely follow the ups and down of global trade, and the almost inevitable decline in global exports we will soon see promises wider spreads

If spreads widen too much, a recession is almost guaranteed prompting further falls in markets

Moreover, declines in credit could prompt bond funds to sell their bond futures, triggering another unwind in the basis trade - as we have seen this week, it leads to significant financial instability

Despite the tariff pause, much damage has already been done to sentiment. Confidence is waning, as can be seen in CEO confidence - as the chart shows, this has typically led to wider credit spreads

Activate to view larger image,

AND … a room with a VIEW …

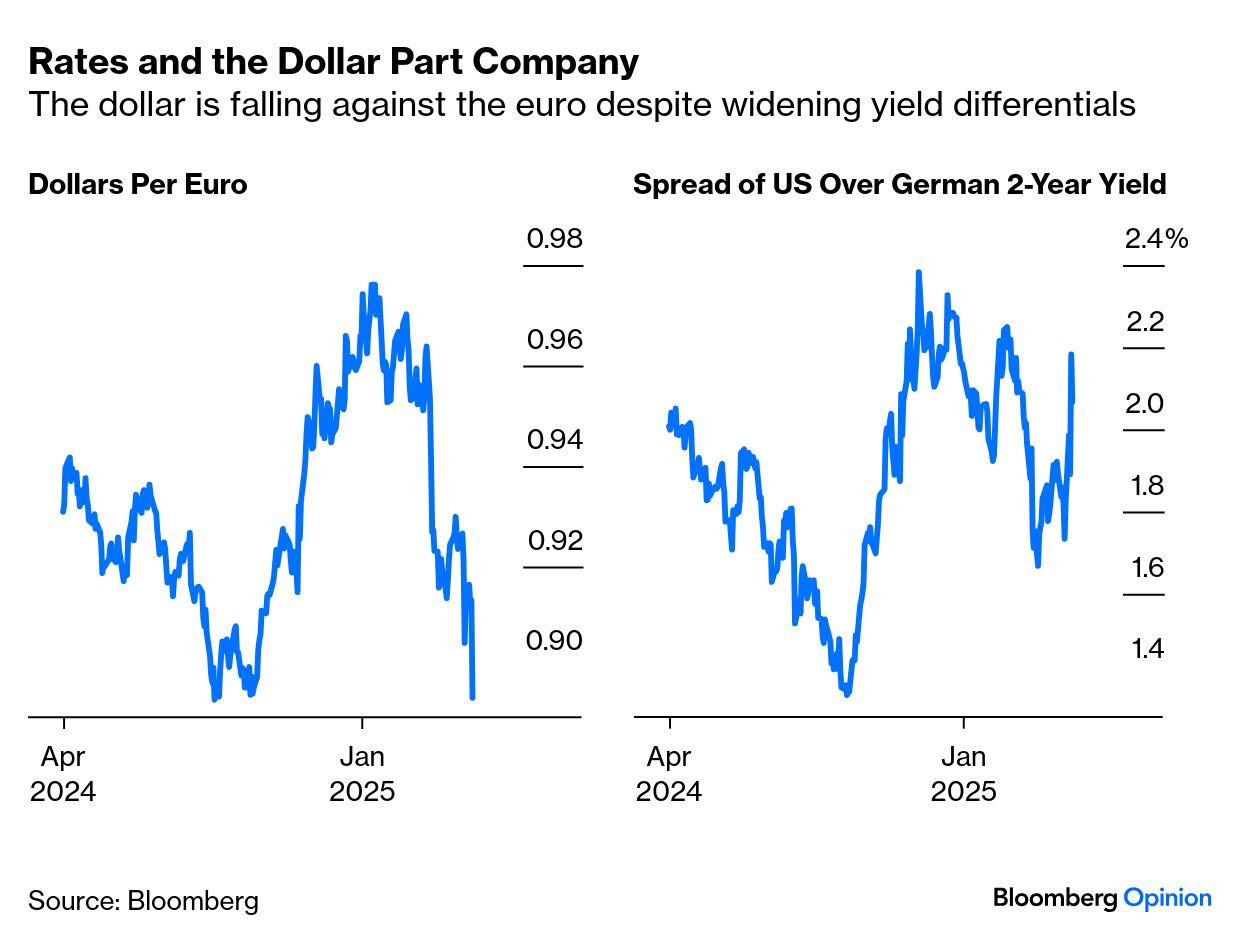

April 11, 2025 at 5:07 AM UTC Bloomberg: Victory over inflation now seems so yesterday Welcome to a whiplash-inducing crisis of confidence in the US.

… One logical explanation for a weakening dollar after strong inflation numbers would center on bond yields. All else equal, lower inflation makes it easier to cut rates, and will bring down short-term yields. The differential between two-year yields has been a key driver of the exchange rate and lower US yields should mean a weaker dollar.

The problem with this theory is that the differential has widened sharply in the US favor of late. The dollar’s slump has come as Treasury yields have risen sharply above German bunds — itself a remarkable occurrence only weeks after Germany committed to its biggest fiscal expansion in generations (largely in response to the Vance speech as it decided it could no longer treat Washington as a reliable ally):

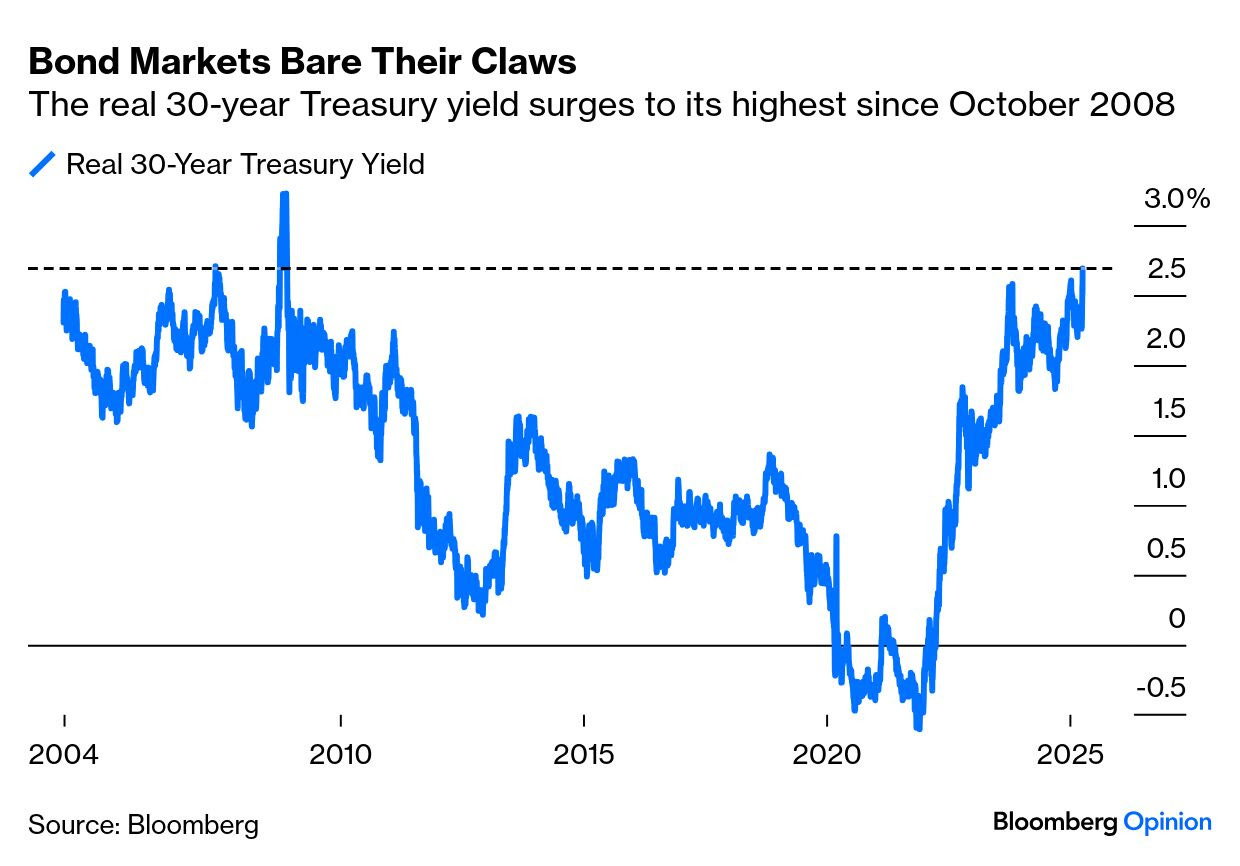

Short-term yields are more important to the currency, but the move in longer bonds has been more startling. The real 30-year yield, as pure a measure of the cost of long-term money as exists, has now reached a high only previously seen during the spasm that followed the Lehman Brothers bankruptcy in 2008:

It’s hard not to write about this in terms that sound apocalyptic.But it’s also hard to cast this as anything other than a significant loss of confidence in the US. It doesn’t have to be terminal. The shock of the debt-ceiling crisis in 2011 turned out to be a major turning point that was followed by a decade of American Exceptionalism.But the moves in the bond and currency markets — to a far greater extent than stocks (which by the way endured a massive selloff Thursday and gave up more than half of Wednesday’s gains)— ram home that a lot is at stake. And the US is currently embarked on what appears to be a wholesale change in foreign policy, not struggling to get things back to normal as Barack Obama tried in 2011…

One of the better technicians out there — Peter Brandt on BONDS …

at PeterLBrandt

Here is a chart that should cause you some alarm. Since 2020 the trend in Bond yields has been up (price down). What is it going to take for buyers to be willing to own US govt debt? Or what fancy "where is the rabbit" trickery will the Fed do? $US30

Apr 10, 2025 WolfST: Beneath the Skin of CPI Inflation: Surging Prices of Food, Housing, Medical Care Meet Plunging Prices of Gasoline & Travel Services

Worst food inflation since 2022. Worst housing inflation in months. But plunging prices for lodging, rental cars, and airfares are interesting.

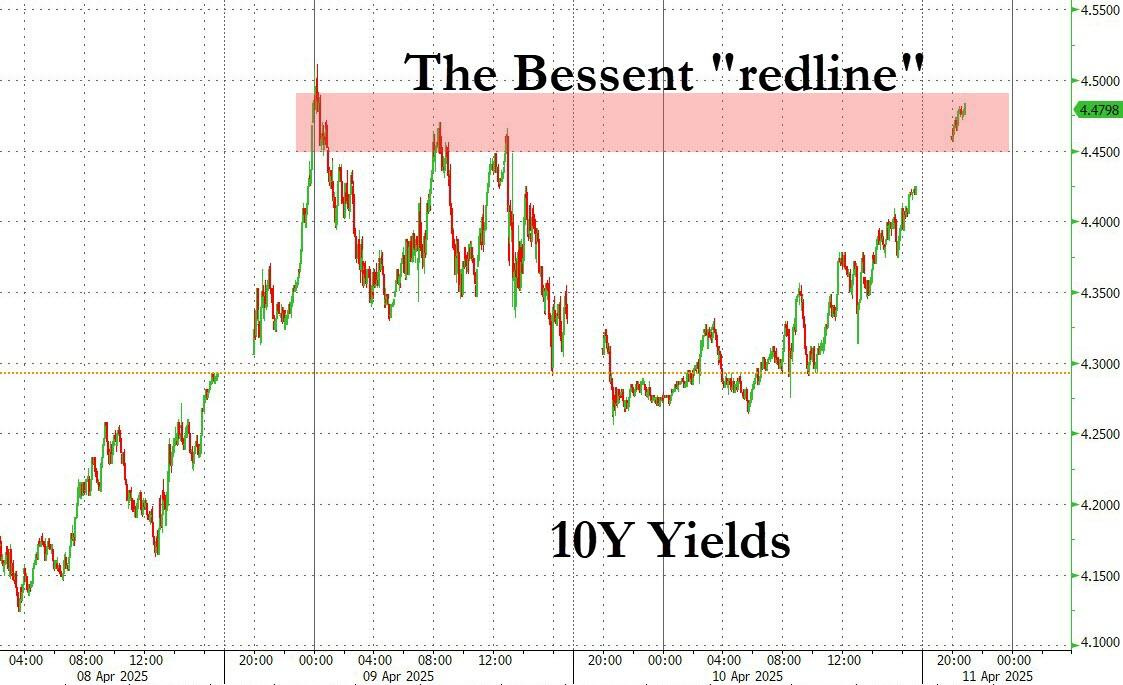

Finally, a red-line crossed?

Friday, Apr 11, 2025 - 01:14 AM ZH: Here We Go Again: Basis Trade Disintegrates Sending Gold, Euro, Yen Soaring, Yields Trip Bessent's "Redline" As Dollar Plummets

... which is again slamming Treasuries and pushing the 10Y yield above the so-called Bessent "red line" above 4.45%, which on Tuesday prompted Trump to pivot on his tariff vows and spark a brief relief rally...

{kind=link}