First order of biz from a guy who used to have more of a front row seat to the institutional FI world … ok, maybe in my eyes it was front row but in reality … was more like this:

…. in any case, today requires I start with …

Bloomberg: US Lifts Quarterly Borrowing Above Forecasts to $243 Billion

Treasury cites weaker cash receipts for bigger borrowing

Department estimates $847 billion net borrowing next quarter

The US Treasury ramped up its estimate for federal borrowing for the current quarter to $243 billion, more than most dealers had anticipated, in a move that largely reflected weaker cash receipts than officials had expected…

ZH: Here's What The Treasury Will Announce In Its Borrowing Estimate At 3pm Today

ZH: Treasury Estimates Borrowing Needs For Q3 Which Sneak Below The Median Estimate

… Bottom line: amid some ridiculous speculation and even conspiracy theories that the BOJ intervened today because it was expecting a surge in funding needs, the Treasury reported numbers that came in in line with expectations for Q2, and actually below the estimate for Q3, which is precisely what we said, because the number is driven not so much by financial but by political considerations.

The real question should be not what the Treasury projects for Q2 and Q3, but Q4, which is after the election, and when all the lipstick on this pig will finally wash off.

… an interesting ZH hit just AFTER equity markets opened up …

ZH: Bitcoin, Bullion, & Breakevens Soar As Markets Lose Faith In 'Inflation-Fighting' Fed

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the belly of the curve giving back some of yesterday's gains (5's still look locally too cheap on curve, technically) after the Eurozone escaped recession in Q1 on the back of topside beats in French, Spanish, Italian and German growth numbers. DXY is modestly higher (+0.1%) while front WTI futures are too (+0.3%). Asian stocks were mixed though Japan's Nikkei (+1.24%) saw a rally, EU and UK share markets were mostly lower while ES futures are showing -0.13% here at 6:40am. Our overnight US rates flows saw modest selling in intermediates with much of the screen volume going through in 5yrs then. During London's AM hours, Treasuries drifted lower despite the looming month-end extensions. The desk saw selling from systematic names around the 10y point while fast$ names sold 3's on curve. Overnight Treasury volume was decent at ~130% of average all across the curve.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities modestly lower, Bunds hampered by EZ data & DXY is flat; US ECI & AMZN due … Bonds are lower, dragged down by French/German and finally EZ figures … USTs are moving in tandem with EGBs which leaves the benchmark a touch softer but some way from Monday's 107-18+ base. Specifics light thus far into Wednesday's FOMC and Quarterly Refunding.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … I’ll be pouring over / through the latest Equity Gilt Study from Barclays and offer a highlight or two tomorrow (see BBG writeup below for preview…)

ABNAmro China: April PMIs point to imbalances and supply-side dominance | Insights newsletter

China Macro: Both manufacturing PMIs remain in expansion territory. Official non-manufacturing PMI drops back by almost two points.

BARCAP China: April PMIs: prepare for the slowdown

While exports acted as an offset, we think more signs of weaker domestic demand suggest growth momentum will fade quickly in Q2. We think the April PMI data reveal a more gloomier picture of developments on the domestic front, ranging from falling industrial profits to a deteriorating labour market.

DB The long and the short of it: How the Fed drives long-term yields

With the May FOMC meeting this week, we conduct a deep dive into a fascinating empirical peculiarity – recent academic work has found that all of the net decline in long-term yields over the past three-and-a-half decades has occurred during relatively small windows around FOMC meetings (see Hillenbrand (2023) ).

In this piece, we update this academic work to incorporate data for the period since 2021. This episode coincided with an aggressive rate hiking cycle and a sharp rise in yields across the curve, in contrast to the trends of the past several decades when the relationship between long-end yields and FOMC meetings was uncovered. Notably, this FOMC puzzle persists with recent data.

We then discuss how the new data can help identify the cause of this relationship. In particular, we provide evidence that is consistent with a variety of other pieces of research suggesting that these moves in long-term yields could be driven by a dynamic whereby monetary policy surprises at the front-end propagate out the curve, driving term premia down in a non-permanent way. This stands in contrast to the explanation in Hillenbrand, that the underlying driver has been the Fed signaling private information on the neutral rate, prompting revisions to market expectations.

Recent months have seen an increasingly positive outlook for markets and the global economy. Fears of a hard landing have receded, and risk assets have posted a significant advance since late-October. Our own House View forecast was significantly upgraded in January for the US, with our economists now forecasting US growth of +2.6% for 2024. They now only expect one rate cut this year as well (see here).”

But there’s still a lot of uncertainty right now, and several things in this cycle that are yet to be resolved. In this chartbook, we run through the issues that keep us awake at night and are worth paying attention to.

As we were thinking about this, 7 different issues came to mind:

The effects of the pandemic stimulus are still present in the US (e.g. excess savings) but are likely to run out by YE ’24. So is the lag of monetary policy just delayed?

Inflation is still above target, meaning rates could stay in restrictive territory for longer. That would raise the chance of a market accident.

Remember that core CPI is still historically high, and apart from the post-Covid inflation, the last three months have seen the highest core inflation since the early 1990s

Several leading indicators (e.g. yield curves) are still pointing in a negative direction.

Some data points suggest the economy isn’t as strong as it seems.

Valuations are pretty stretched by traditional metrics.

National debt burdens remain high (and rising in many cases).

The geopolitical situation remains tense.

This chartbook runs through each of these themes. For now growth and the performance of risk assets are overpowering such concerns. However, given the repeated surprises of the last 4 years, it’s worth keeping these on your radar over the months ahead

We were constructive on earnings coming into the Q1 season, expecting growth to remain robust at around 10% yoy (Q1 Earnings Preview: Looking For Rotation In Growth, Apr 2 2024). In the event, halfway through the season, earnings have surpassed even our constructive expectations. Beats are running at 9.2% in aggregate, a near three-year high and almost double the historical average of 4.9%. If these beats hold through to the end of the season, earnings growth is on track to accelerate into the double digits to 11.8%, driven by a combination of steady mid-single digit sales growth and margins rising to the highest in nearly 2 years.

Across sectors, mega-cap-growth (MCG) and Tech saw earnings growth remain very strong at 38% yoy again despite the boost from base effects diminishing this quarter. Moreover, unlike last quarter, other sectors also stepped up, with growth of 3.2% after four straight quarters of negative growth. Absent a large drag from Energy and Materials, their growth would have been even stronger at nearly 8%.

Considering strong Q1 earnings, and in line with DB’s upgraded house macro forecasts, we raise our 2024 EPS base case forecast from $250 to $258, implying 13% growth over 2023. Alternatively, if macro growth remains above-trend, we continue to see 2024 EPS higher at $271.

Earnings growth is on track to accelerate into the double digits to 11.8%

Goldilocks China: April PMIs – mixed news on manufacturing, slower services growth

Bottom line: The NBS manufacturing PMI fell to 50.4 in April from 50.8 in March. The Caixin manufacturing PMI rose to 51.4 in April from 51.1 in March. Both manufacturing PMIs were better than market expectations. The NBS non-manufacturing PMI decreased to 51.2 in April from 53.0 in March, moderately below market expectations and entirely driven by weakness in real estate and financial services.

MS The Problem with Steepeners | US Rates Strategy

Curve steepeners are popular among all investor types. Yet, the possibility of "insurance cuts", improving fiscal and historical trends, and consensus positioning means there is an under-appreciated path to bull flattening. Duration longs offer better risk/reward than steepeners. Add 3m30y receivers.

Investors think steepeners work in many scenarios: Curve steepeners are immensely popular among investors of all stripes – albeit for different reasons, varying from traditional Fed cuts-driven bull steepening to term premium expansion in the long end.

Investors under-appreciate bull-flattening risk: Investors think curves can both bull steepen and bear steepen, but under-appreciate the bull-flattening risk. We think bull steepening and bull flattening are both viable scenarios, and thus see bullish duration as a better option than curve steepeners. We look at the key arguments cited in favor of steepeners.

Argument 1: The curve can bull steepen in a Fed cutting cycle; counter argument – the curve can bull flatten instead if markets see cuts as "insurance" like in mid-2019.

Argument 2: 2023 suggests steepeners can keep doing well; counter argument – history suggests that bear steepenings are mean reverted by bull flattenings.

Argument 3: Perceived fiscal deterioration and a supply/demand mismatch can expand term premiums, driving bear steepening; counter argument – the near-term fiscal picture is improving, supporting demand for longer-duration Treasuries.

Argument 4: A Trump election scenario is linked to a dovish Fed and fiscal expansion – supporting twist steepening; counter argument – many hurdles and checks lie between an expansionary fiscal policy or a dovish Fed post-elections.

Argument 5: Investors will add more steepeners; counter argument – curve steepeners positioning is pretty consensus.

Long 3m30y receivers: We add long 3m30y receivers to play for the idea that duration longs are better than curve steepeners.

We estimate total nonfarm payrolls rose 250k (200k private) in April vs. 276k average in the last 3 months. AHE rises 0.3%, slowing year/year to 4.0% - the slowest pace since early in the pandemic. The unemployment and participation rates likely stalled at 3.8% and 62.7%.

UBS (Donovan): Another day, another set of inflation data (over there …)

Employment Trends in the Establishment and Household Surveys

Summary The establishment and household measures of employment have painted different pictures of the labor market's resilience in recent months. According to the payroll survey, U.S. employment continues to grow at a robust pace year-over-year. Meanwhile, annual employment growth as measured by the household survey has nearly stalled, with the 0.4% rise through March the smallest increase outside the pandemic since October 2013. In this report, we discuss key differences in the objectives and methodologies of the surveys, potential explanations for the current divergence in trends and what it means for expected strength in hiring ahead.

The household survey and the establishment survey of payrolls are designed to provide separate views of the labor market. The household survey is a demographic survey offering insight into the labor force status of segments of the population. The payroll survey measures employment and earnings from an industry perspective.

The surveys define employment differently. The household survey measures the count of employed persons while the establishment survey measures jobs in the U.S. economy. The scope of payrolls is less comprehensive and excludes agricultural workers, workers in private households (e.g., housekeepers), the unincorporated self-employed and workers on unpaid leave (e.g., on strike). However, even after reconciling the surveys' scopes, the present gap in employment growth remains large.

The birth-death factor is still providing a historically large lift to monthly payroll gains, but this is not a major contributor. Over the past year, the birth-death model has boosted payrolls employment by 26K more per month than its pre-pandemic lift, but given the household survey is a survey of persons and not businesses, it neither requires nor receives such an adjustment.

The household survey could be underestimating the population, and therefore employment, if the recent surge in immigration is not yet reflected in the survey's population controls. The Census net immigration estimates rely on lagged data and currently sit below other approximations. Meantime, the establishment survey's count of jobs does not rely on population estimates and is likely to be faster to include an influx of foreign workers.

The household measure of employment is more volatile and difficult to compare across periods given its smaller sample size and revision methodology. Household employment tends to oscillate around the more stable payroll trend, and a steeper plunge in response rates post-pandemic may be exacerbating the volatility.

We do not believe the downturn in household employment is a harbinger of an imminent collapse in nonfarm payrolls. The household survey has a poor track record of foreshadowing downturns in payrolls. The employment trend divergence is also somewhat cyclical, so it is not unusual for the gap to be increasing over an expansion. Both surveys' primary outputs—payroll growth and the unemployment rate—point to a still-strong jobs market. We will thus continue to keep our eyes on payrolls to gauge the strength of hiring and not fret over the near-stalling in household employment growth over the past year.

… Because the surveys differ in their samples and objectives, they also track distinct definitions of employment. "Employment” in the household survey is a count of employed persons, while the establishment survey estimates the number of nonfarm jobs in the U.S. economy. The household survey's measure of employment is also wider in scope, as it includes individuals working in agriculture, a family business without pay, private households (e.g., housekeepers or nannies) or those who are self-employed or taking a temporary leave of absence (e.g., workers on strike). Meantime, the establishment survey only counts jobs that show up on a company’s payroll during the reference period (the pay period including the 12th day of the month). This excludes agricultural workers, the unincorporated self-employed and workers on unpaid leave. Finally, people working multiple jobs are counted as employed once in the household survey, whereas they are counted in the establishment survey for each position held.

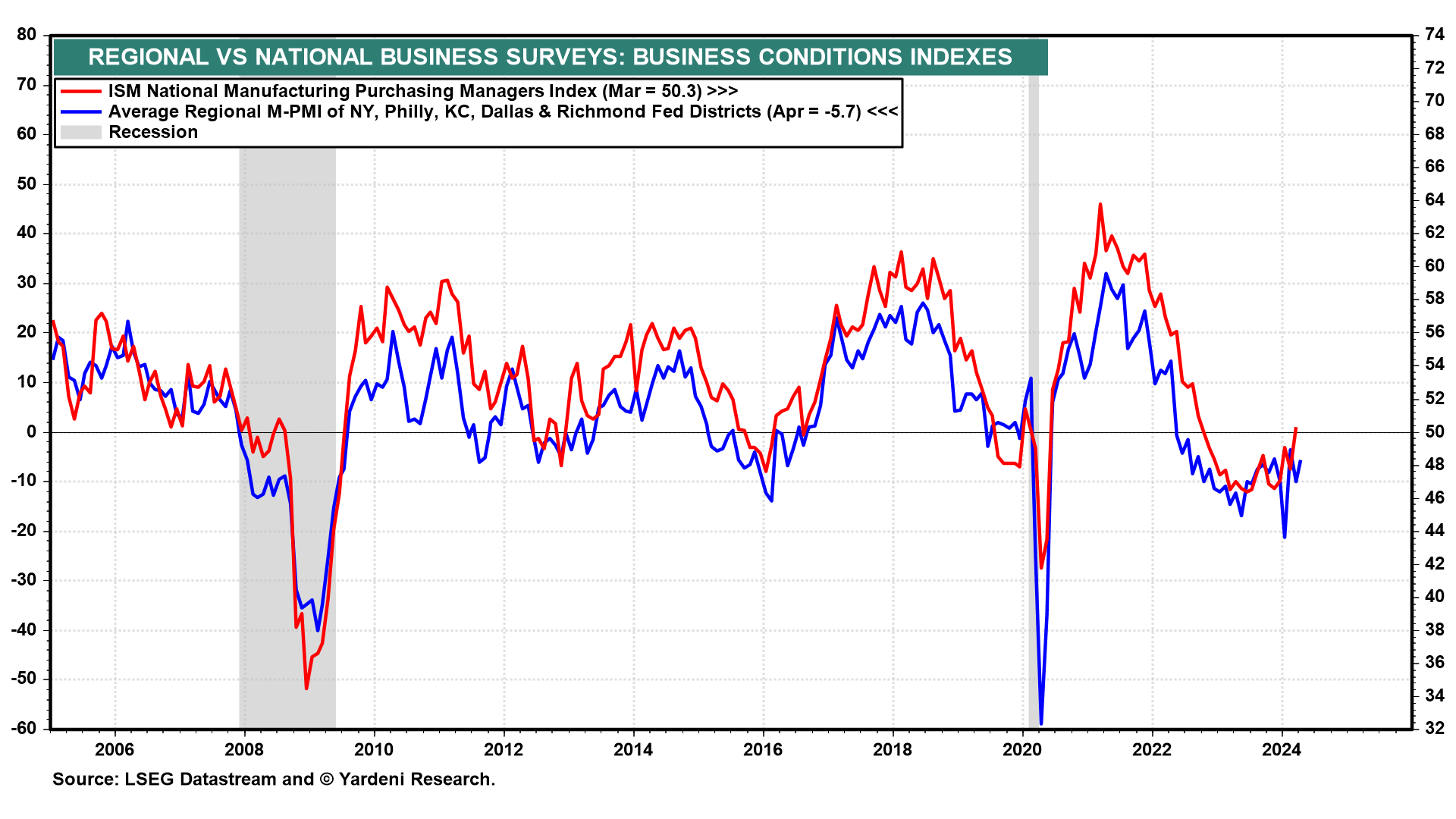

Yardeni: Lackluster Fed Regional Business Surveys (looks like it’s moving in the right direction, though …?)

We now have the regional business surveys conducted by five of the Federal Reserve district banks. The average of their general business conditions indexes closely tracks the national manufacturing purchasing managers index (M-PMI), which rose slightly above 50.0 during March following 16 consecutive monthly readings below this level (chart). The regional average index was still negative in April. So it has yet to confirm that the rolling recession in the manufacturing sector is over.

The averages of the regional prices-paid and prices-received indexes have been relatively stable around 20.0 and 10.0, respectively, over the past 12 months or so (chart). These are both relatively normal readings and well below their highs during 2021 and 2022, when pandemic-related supply chain disruptions were most severe. By the way, the PPI final demand inflation rate closely tracks the prices-paid index, which suggests that the former should be around 2.0% y/y. It was 2.1% in March.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Treasury Yields to Stay Elevated on Supply Deluge, Barclays Says

Changing composition of Treasury buyers to also impact yields

Higher US yields pose risks to other global bond markets

A glut of Treasury issuance will outweigh any Federal Reserve policy pivot to keep long-term yields elevated and pressure global bonds, according to Barclays Plc.

“Long-term yields in the US are likely to remain high, even if the Fed cuts rates,” the bank’s strategists Jeffrey Meli and Ajay Rajadhyaksha wrote in a note. “Studies suggest that a one percentage-point increase in the projected deficit-GDP ratio pushes up the 10-year Treasury yield by 20 basis points.”

The benchmark 10-year Treasury yield jumped to a six-month high in April as resilient US economic data prompted traders to pare back on their expectations for Fed rate cuts this year. Concern over heavy debt supply has the potential to further hurt demand for US debt.

Bloomberg: The Fed’s Quantitative Easing Program Cost Too Much (Duds OpED…)

The total bill could exceed $500 billion. A proper evaluation should make the next one less expensive.

… It is worth considering how the 10-year Treasury yield moved historically with inflation and the state of the economy. There were quite a few deviations and they contribute to some interesting findings. For the 1960s and 1970s, the predominant theme was a continuous underestimation of rising inflation, with occasional exceptions. From 1965 to 1969, the inflation rate increased to around 5%, which provided the backdrop for a decade of high inflation. In the 1970s, the money supply expansion, along with the oil crisis, sent inflation into the double digits. This was the decade of “stagflation” with low growth, high unemployment, weaker personal consumption yet higher inflation. After inflation peaked in the early 1980s, 10-year yields showed some inertia. The period 1982 to 1993 marks a decade of continuous disinflation in which inflation expectations did not come down as fast as the actual inflation rate, while the economy in the 1980s grew relatively well. The key is bond yields lagged nominal growth in PCE both on the way up and again on the way down. In order words, to the extent that bond yields are tied to nominal growth in PCE, they tended to become anchored to past rates of growth rather than correctly anticipating faster or slower nominal growth in the future. They are reactive and not anticipatory.

Figure 1: 10-year Treasury Yield and PCE Growth, 1962-1992

ZH: Weaker Growth And Higher Inflation... Why Consensus Was Wrong

Why Biased NYC Trial Judge is Setting Donald Trump Up for a Conviction, with Andy McCarthy

https://youtu.be/U7vI9Fv5U6k?si=LZyWGz6bZJ5FqVHY

That muti-job indicator sure appears to be Recessionary....