30yy DAILY: trend yet to bend (aka CONCESSION for supply?) and momentum crossing BEARISHLY …

… sometimes this stuff works / makes sense. Moving along before it starts to sound like a Global Wall victory lap (it isn’t), here is a snapshot OF USTs as of 656a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly cheaper and steeper alongside the hawkish BoJ Summary of opinions and onslaught of US primary issuance (up to ~53bn after yday). The move has been quieter than expected this morning, according to our London desk, the long end under pressure on ~85-90% volumes. Better selling has been seen from both discretionary fast$ and systematic accounts out the curve, while there was a 4k TY block sale near the London session lows that has the move ahead of the BoE and 25bn 30y UST auction. Bunds are leading the core underperformance, with peripherals slightly wider to core as well (10y BTPs +4.5bps). Risk-assets are modestly on the back-foot (VG -0.2%, S&Ps -0.2%) after a mixed session in APAC (NKY -0.3%, KOSPI -1.2%, SCHOMP +0.8%). The DXY is modestly higher (+0.1%) with USDJPY +0.3% to 155.90, and AUDJPY -0.2%. Crude and Gasoline futures are both up +1%, with 30y real rates leading the UST steepening.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures lower, Gilts pressured ahead of the BoE and USD/JPY nears 156 … Bonds pressured in a continuation of recent action; Gilts underperform slightly ahead of the BoE … USTs are softer, in a continuation of the general bearish tone that was in place yesterday and one that appears to be driven by a pause-for-breath from the post-NFP move, lack of geopolitical escalation, relatively average 10yr before today's 30yr and an increase in corporate issuance activity.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

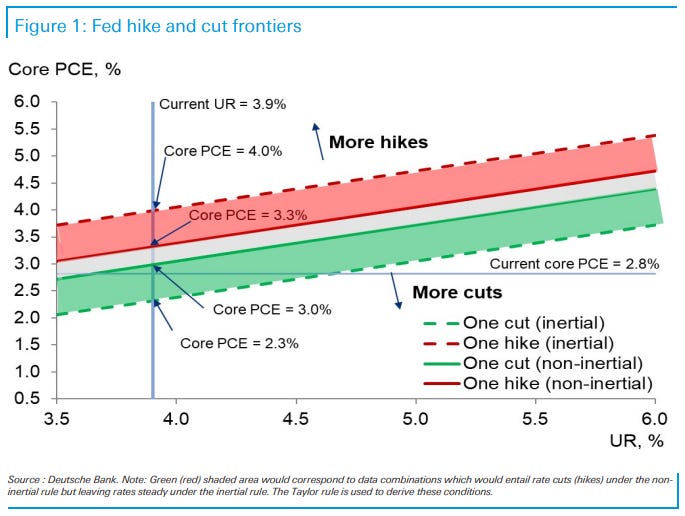

DB: The next (and final?) frontier: Mapping conditions for cuts and hikes

At the May FOMC meeting, Chair Powell ditched calendar-based guidance and embraced data dependence (see "Hold the line, cuts aren't always on time"). In doing so, he detailed the Fed’s broad reaction function to various economic outcomes. In this piece, we conduct a scenario analysis around conditions for cutting and hiking rates based on a rate cut frontier we first published in our recent monthly chartbook (see slide 43 here: "The waiting is the hardest part").

Our analysis identifies conditions for the unemployment rate and inflation that would be consistent with rate cuts and hikes this year depending on if the Fed is acting inertially or non-inertially. Taken together, the framework is consistent with current signals from the Fed, namely: rates are likely at the peak; the next move is more likely to be a rate cut than a rate increase; but that further progress on inflation is needed to gain confidence in disinflation and trigger a reduction.

Policy twist reduces risk of disorderly rate moves as the labor market eases further

The recent bond market sell off has been quite orderly compared with last fall’s term premium “shock”. The main goal for policymakers – the Fed and Treasury - is to avoid a repeat of last year, as we approach the election. So far they’ve done a good job, helped but more signs of labor market slowing. Investors might still worry about sticky inflation but as we argue below it’s all about understanding the drivers of inflation at a disaggregated level. Faster drivers normalize more quickly, leaving slower drivers behind so that the average pace of inflation normalization slows. The Fed can afford to be patient but only so long as the labor market can hang together and further hiking is unwarranted, in our view …

… The attribution tables show the importance of net supply historically – for example QT and the deterioration in net supply overall itself contributed 86 bps to higher 10y yields of which +115bps came through term premium. The projection through to June 2025 is that even with a deficit of around $2 trillion, net supply can contribute to slightly less term premium -0.14 bps, reflecting the taper. Overall if the Fed forwards are realized we project 10s down 85 bps by mid 2025 largely driven by the realization of current Fed expectations in the 1y1y space.

SocGEN: Global Strategy Weekly (Albert Edwards speaks we lean in and listen…)

I remain on a mission to counterbalance bullish investment groupthink

Long-time readers will know that they get an unadulterated view on these pages. That view may sometimes be wrong, or ‘early’ as I prefer to call it, but no reader can ever accuse me of falling victim to the optimism bias that the sell-side usually suffers from.

… The most recent collective failure to think differently was western central banks’ (and the economics industry generally) inability to predict that monetising huge fiscal deficits during the (supply constrained) pandemic would cause a surge in consumer price inflation.

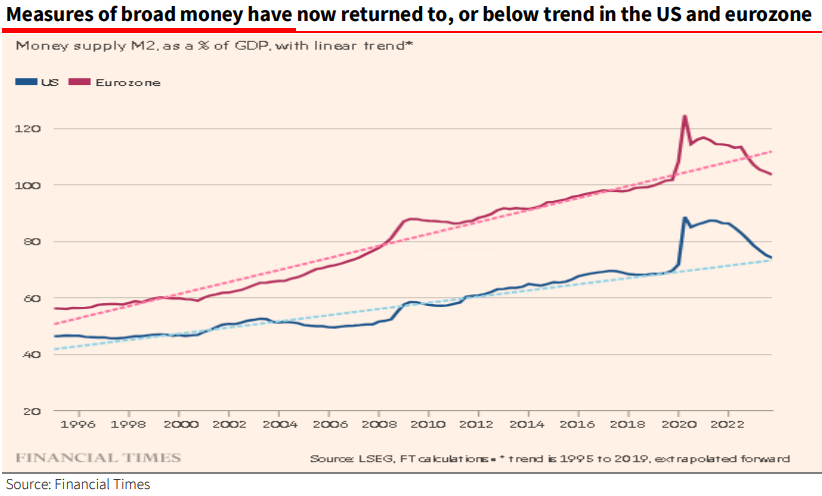

In that context the former Bank of England Governor (and chief economist) Mervyn King was making headlines last week. King criticised “groupthink” and the lack of dissenting voices at central banks for fuelling the inflation crisis. In particular he said it was “foolish” for central banks to rely on forecasting models that ignored the role of money – link and link.

With that last point in mind, I noted the FT’s venerable Martin Wolf pointed out that the explosive expansion in broad money relative to GDP had now fully unwound. Indeed, broad money growth has been the weakest since the 1930s. Wolf writes, “These numbers show a huge monetary boom and bust. In future, disinflationary pressure might prove excessive” – link.

Summary A string of uncomfortably-hot inflation readings in the first quarter leaves a narrow window for inflation to downshift before a late summer rate cut by the Federal Open Market Committee (FOMC) is no longer on the table. We expect the April CPI report to demonstrate that while inflation is not as sticky as the Q1 pace indicated, the journey back to 2% remains slow-going.

Headline CPI likely rose by 0.4% for a third consecutive month in April, which would leave overall prices running at nearly a 5% three-month annualized rate. Progress in lowering core inflation, however, likely resumed. Excluding food and energy, we estimate prices rose 0.3%, which would break the streak of 0.4% gains since January and push the year-over-year rate down to 3.6%, a three-year low. Ongoing deflation in the goods sector is expected to help keep a lid on core inflation in April, but services are likely to be the bigger driver of the softer print. We look for shelter inflation to have eased a bit further in April, and we anticipate a bigger step-down in core services ex-housing (+0.4% following a 0.6% rise in March).

While inflation has been stubborn in recent months, we do not believe the underlying trend is re-accelerating. Supply chain pressures are not easing as rapidly as a year or two ago, but they are not building either. Shelter inflation looks set to moderate further this year, while services ex-housing inflation should benefit from tamer growth in goods-related input costs and gradual loosening in the labor market. We expect to see monthly inflation prints trend lower over the remainder of the year as a result, with the core CPI subsiding to a 2.8% annualized rate in Q4 and the core PCE easing to a 2.1% annualized rate in Q4…

… However, with core CPI and core PCE in March picking up to three-month annualized rates of 4.5% and 4.4%, respectively, the sufficient confidence has yet to be built (Figure 1) …

Wells Fargo: Like There’s No Tomorrow: Unpacking Consumer Credit

Summary The recent run-up in revolving debt combined with the much higher financing costs raises doubts about the ability of credit to continue to make up for the shortfall between modest real income growth and aspirational spending. Is there a way to feel better about the consumer credit situation?

… Signs of Struggle Be wary of reassurances from those bearing charts of broad household debt-to-income measures or financing costs, like that shown in Figure 6. The fact that aggregate household debt remains near the low end of a 15-year range says more about mortgages, which comprise a 70% share of household debt, much of which has a fixed rate structure and therefore are unimpacted by Fed rate hikes, than it does about households serviceability burdens.

So are there any indications that households are struggling with debt today? The share of debt that is delinquent is the best way to gauge household stress. The delinquency rate on all household debt stands at just 1.7% as of the fourth quarter, which is below pre-pandemic levels and just a stone's throw away from the all-time low of 1.4% hit in late 2022. But here too a sound mortgage portfolio is impacting the data as delinquency trends differ across loan-products (Figure 7). Delinquency rates remain near the low end of the range for the past decade for mortgages and student loans. Yet if we look at delinquency rates for auto loans and credit cards we find that both measures are as high as they have been since 2011 when they were coming down from financial crisis era highs.

The increased transition into delinquency on credit card and autos loans is clearly not a favorable development and suggests continued reliance on credit cards will grow more challenging. But when we think of it from the broad macro perspective, the notable offset from mortgages cannot be ignored as it offers a bit more cushion for delinquencies to rise elsewhere without a credit crunch in the broad household sector.

Consumers keep spending, and they're pulling out all the stops to do so. Credit reliance has been a key factor in helping support the consumer this cycle, but with the smallest increase in revolving credit since April 2021 in March, this source of purchasing power may be fading. Interest rates are perched at 30-year highs leading to serviceability challenges as delinquencies are ticking higher. While we're not yet worried of a full-blown credit crunch in the household sector, the recent run-up in credit card borrowing doesn't look sustainable. It's no wonder households are growing a bit more choosy in spending behavior.

Wells Fargo: Inventories Are Quiet...A Little Too Quiet

Summary The economy is in the midst of an unusually calm stretch with respect to inventory investment. It is like the point in the scary movie when someone points out that all the forest creatures have gotten quiet. It is a classic set-up for a jump scare and thus warrants an extra measure of vigilance.

… And from Global Wall Street inbox TO the WWW,

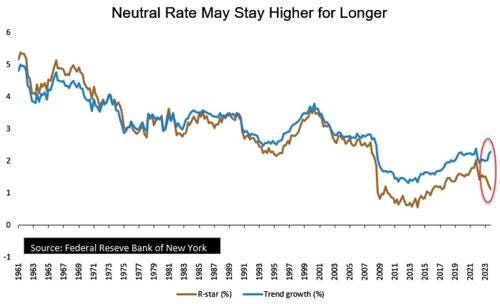

Bloomberg: Treasury Yields To Stay Sticky As Neutral-Rate Fears Loom Large(contrary to what I’m told is more common — RATES COMING DOWN — wisdom 'out there’, a recap / reflection of Ka$hkari commentary)

… For good measure, he has also penciled in a higher short-run neutral rate.

The neutral rate, where an economy is at full employment and inflation steady, is still elevated at 1.12%, based on the latest update of the Laubach-Williams model:

That compares with the Fed’s implicit assumption of a 60-basis point real neutral rate, based on its March summary of economic projections.

If core PCE were to bob around 3%, as Kashkari fears, and assuming the Laubach-Williams model provides a more realistic reading of the real neutral rate, the implied nominal policy rate would be north of 4% - making the current rate less restrictive.

This is why Kashkari remarked that there is the prospect of interest rates having to go higher, although he added that it isn’t the most likely scenario (note also that he doesn’t vote on monetary policy this year).

However marginal that prospect may look now, market pricing must reflect the possibility of such a scenario.

And at around 4.47%, Treasury 10-year yields are doing just that.

With so many factors sapping sentiment, longer-dated Treasuries will find it hard to rally just yet.

FRBNY: Balance Sheet Reduction: Progress to Date and a Look Ahead

…Conclusion Where does that leave us? As I noted at the outset, the past two years of balance sheet runoff have proceeded smoothly. That is, of course, good news for central bankers. But we cannot take this performance for granted. We therefore continue to manage risks and carefully monitor money market conditions.

Slowing the pace of runoff is one effective way to manage those risks. Doing so allows money markets and the banking system to adapt to progressively lower levels of reserves. It also provides more time for us to collect data and assess the level and evolution of reserve demand. That careful and gradual approach is consistent with the plans laid out by the FOMC prior to the start of our balance sheet reduction program. In that sense, the Committee’s recent announcement is simply the execution of that existing plan.

We are also continuing to monitor money markets for any sign of strains. Econometric analysis can tell us how responsive money market rates are to changes in reserves. That gives us a reasonably clear sense of whether reserve supply is currently abundant or ample. Other measures can be deployed to get a complementary or more forward-looking view. As I just mentioned, those include, but are certainly not limited to, domestic bank activity in federal funds, the timing of interbank payments, the aggregate amount of daylight overdrafts, and granular data on repo market activity. And I would be remiss if I did not highlight the incredibly valuable money market intelligence we get from market participants, including primary dealers.

We also have new tools at our disposal to deal with any unexpected turbulence. The SRF supplies additional cash to repo markets at an administered rate, which the FOMC has set at the top of the target range, against Treasury and agency collateral. The SRF is available every day; it can provide a strong defense against the kind of disruption we saw in 2019, and we would expect our counterparties to use it if market rates make it economically convenient to do so. And the same goes for the discount window, which of course is not a new tool but is also available every day, and through which the Federal Reserve can lend to depository institutions against a wider range of collateral.

Taken together, the indicators and tools at our disposal constitute a powerful set of instruments, and they support my confidence that the balance sheet reduction process can continue smoothly….

ZH: Someone Is Lying: Atlanta Fed Claims US GDP Is 4.2% While DOE Reports Lowest Gasoline, Diesel Demand Since Covid

Israel Security Minister: Hamas loves Biden

https://youtube.com/shorts/94bYxLH78iU?si=S4jCaefTLctBEBOm

Try a Little Honesty About Israel

Here are ten of their most common untruths about October 7 and the war that followed.

By Victor Davis Hanson

http://trk.amgreatness.org/c/7/eyJhaSI6OTkyNjA2OTcsImUiOiJ2YW5oZXluaW5nZW5AeWFob28uY29tIiwicmkiOiIxMzc1NTM2OTQwIiwicnEiOiIwMi1iMjQxMzAtZmFkMWZmZmNiM2JkNDZkODgyZjFlYWVjMTFjMWNiYTkiLCJwaCI6bnVsbCwibSI6ZmFsc2UsInVpIjoiIiwidW4iOiIiLCJ1IjoiaHR0cHM6Ly9hbWdyZWF0bmVzcy5jb20vMjAyNC8wNS8wOS90cnktYS1saXR0bGUtaG9uZXN0eS1hYm91dC1pc3JhZWwvP3V0bV9tZWRpdW09ZW1haWwmdXRtX3NvdXJjZT1hY3RfZW5nJnNleWlkPTEzNDg2NCJ9/gdEE-ney8MRbyR1HrWKtzg