Good morning … I simply cannot now and never have been able to compete with the likes of ‘Roaring Kitty’ who’s apparently ‘resurfaced’ … I will defer to those far more professionally capable than I to comment and only ask someone let me know when said Kitty is involved in the US Rates space … until then, well …

Good morning … unless yer were surveyed by FRBNY recently and / or are a card carrying member of Team Rate Cut …

ZH: Household Finance Fears Worst Since COVID As Inflation Expectations Surged In April, NY Fed Survey Finds

… good thing these are only surveys and, as always, one is cautioned to watch / listen to what they say AND even more so to whatever they DO … SAME applies to rates and while having a view and trying to ‘skate to where YOU think the puck is gonna be’ is all well and good, here’s a check-in on the 7yy just because it appears to ME we’re at yet another pivotal moment in 2024 …

… as it appears to be the calm before the storm about to end with today’s PPI followed by JPOW at 1030a … More questions than answers and there’s great hope that by weeks END that imbalance will be resolved AND we’ll have more answer than questions but for now … here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly bull-steepening after another somnambulant session in Tokyo that featured a 2-tick range and ~50% 30d volumes. Desk flows there saw FM interest in flatteners and RM buyers in intermediates. Into London hours, some FM paying was seen in 2s5s10s to clean up their received positions, marginal steepener interest as well. Intermediates are struggling a bit on the curve, cheapening about 0.5bps vs the wings on some profit taking from FM, with volumes improving slightly to ~80% into the US crossover. FX & energy markets aren’t making waves, close to unchanged (save for gasoline futures -0.5%), while Gilts are slightly outperforming here after the BoE’s Pill noted ‘it’s not unreasonable to consider’ Summer easing after mixed UK labor data. Equity futures are close to home here at 6:45am, the DAX -0.2%, S&P e-minis UNCH’d, after minimal changes to APAC bourses overnight (NKY +0.5%, SHCOMP -0.1%, KOSPI +0.1%).

… In the debate over whether US inflation is in the riffles (Q1 residual seasonality, lagged shelter impact) or rapids (renewed surge, unmooring expectations), we remain largely in the former camp. While yesterday’s NY Fed SCE survey showed an unusual climb in consumer inflation expectations (3.3% from 3% in recent months) as well as home price growth (fastest since Summer 2022), we see the data as more of a response to lagged energy prices and realized inflation in Q1. That said, looking at the long-term chart of the Citi Inflation surprise Index, the US price data does seem to be negotiating the top end of a ‘band of tolerable surprises’ as we enter the Q2 reporting period…perhaps raising the stakes and consequences of errors for the Fed. The NY Fed’s data on the labor market, which showed a three year low in confidence in “the ability to find a new job if they lost one”, also speaks to the recent loosening in labor/soft data, which was reflected in yesterday’s online job-posting release (IndeedPostings) as well as in this morning’s NFIB release: a net 12% of owners reported planning to create new jobs in the next three months, up one point from March’s lowest level since May 2020, while a net 26% planned price hikes in April, down seven points and the lowest reading since April of last year (NFIB).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities trade tentatively ahead of US PPI & Fed Chair Powell; GBP softer post-Pill … Bonds are firmer, taking a further leg higher after BoE’s Pill before paring on ZEW … USTs are incrementally firmer but with magnitudes much more contained than EGBs as we await US PPI ahead of Wednesday's CPI print. USTs at the top-end of 108-24 to 108-29 bounds which are contained by Monday's 108-23 to 109-00 parameters.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BAML Flow Show: Bonds are Back (just now stumbling upon last weeks ‘show’)

… The Biggest Picture: corporate bonds en fuego…since Mar’20 biggest outperformance vs govt bonds in 100 years (Chart 2 – US government spending +40% over period to $6.2tn), IG bond inflows on course for record $440bn in '24, IG spreads (88bps) at levels seen during boom/extreme QE (Chart 5); credit like stocks loving macro ambiguity & Fed asymmetry…but once govvies start outperforming credit, risk assets get toppy …

Goldilocks: DM Rate Divergence Is Unlikely to Constrain Policy

Since the start of this year, the prospect of a more hawkish Fed at the same time that other major DM central banks are pivoting toward rate cuts has raised the possibility that policy rates could diverge across economies. Although our baseline forecasts assume only modest policy divergence, some investors and central bank officials have speculated that diverging policy rates could eventually constrain policy options for other DM central banks.

The main economic effect of policy divergence in non-US DMs would likely come from higher import prices and inflation due to currency depreciation, but so far this channel appears set to have only modest inflation impacts. Currency depreciations since the January US CPI report—the first hotter US inflation print that escalated concerns of policy rate divergence—imply no more than 0.2pp of upside core inflation risk across G10 economies, although the larger FX move in Japan since a year ago could imply up to 0.6pp of upward pressure. We therefore do not see current levels of expected policy divergence as constraining policy options, but the prospect of higher inflation in Japan supports our view that the BOJ will ultimately hike to 1.5% this cycle.

We also do not expect that reasonable levels of policy divergence will constrain DM central bank policy over the medium run. After developing rules of thumb that relate policy divergence to inflation, we estimate that each 100bp in rate cuts in excess of the Fed adds 0.1-0.2pp of upward pressure to core inflation in most DMs, with larger effects of 0.3pp in Canada and Japan. These estimates generally suggest that policy rates in DM central banks would need to diverge from the Fed by over 100bp more than we currently forecast for inflation to rise to uncomfortable levels, although inflation could increase more quickly if any single DM central bank cuts more aggressively than its peers (in addition to the Fed) and its currency therefore depreciates relative to a broader set of trade partners.

More dovish policy abroad should slow growth and inflation in the US, and we estimate that each 100bp of policy rate divergence (relative to the broad group of other DMs) lowers US core inflation by 0.1-0.2pp. Given that small changes in the inflation outlook could meaningfully affect Fed cuts, these patterns add to our confidence that the Fed will ultimately cut rates by more than markets expect.

Our analysis suggests that a hawkish Fed is generally unlikely to limit policy options in non-US DMs, but that Canada and Japan are most likely to face higher inflation if they diverge too far. We therefore maintain our forecasts that the ECB, BoE, and BoC will cut three times in 2024, and that the BoJ will embark on a gradual rate hike cycle even though we expect that the Fed will only cut twice.

UBS: Inflation numbers of limited interest (conspiracy theory or not …?)

… US April producer price inflation is expected to be benign, with a slight slowing in the core rate. The problem is that this tells us less and less about consumer price inflation. Market-based prices at a consumer level are generally in disinflation, and durable goods prices have been falling for months and months. It is the made-up prices calculated by a mysterious statistical alchemy in the depths of the Bureau of Labor Statistics that are propping up consumer price inflation, and producer prices have no influence over those…

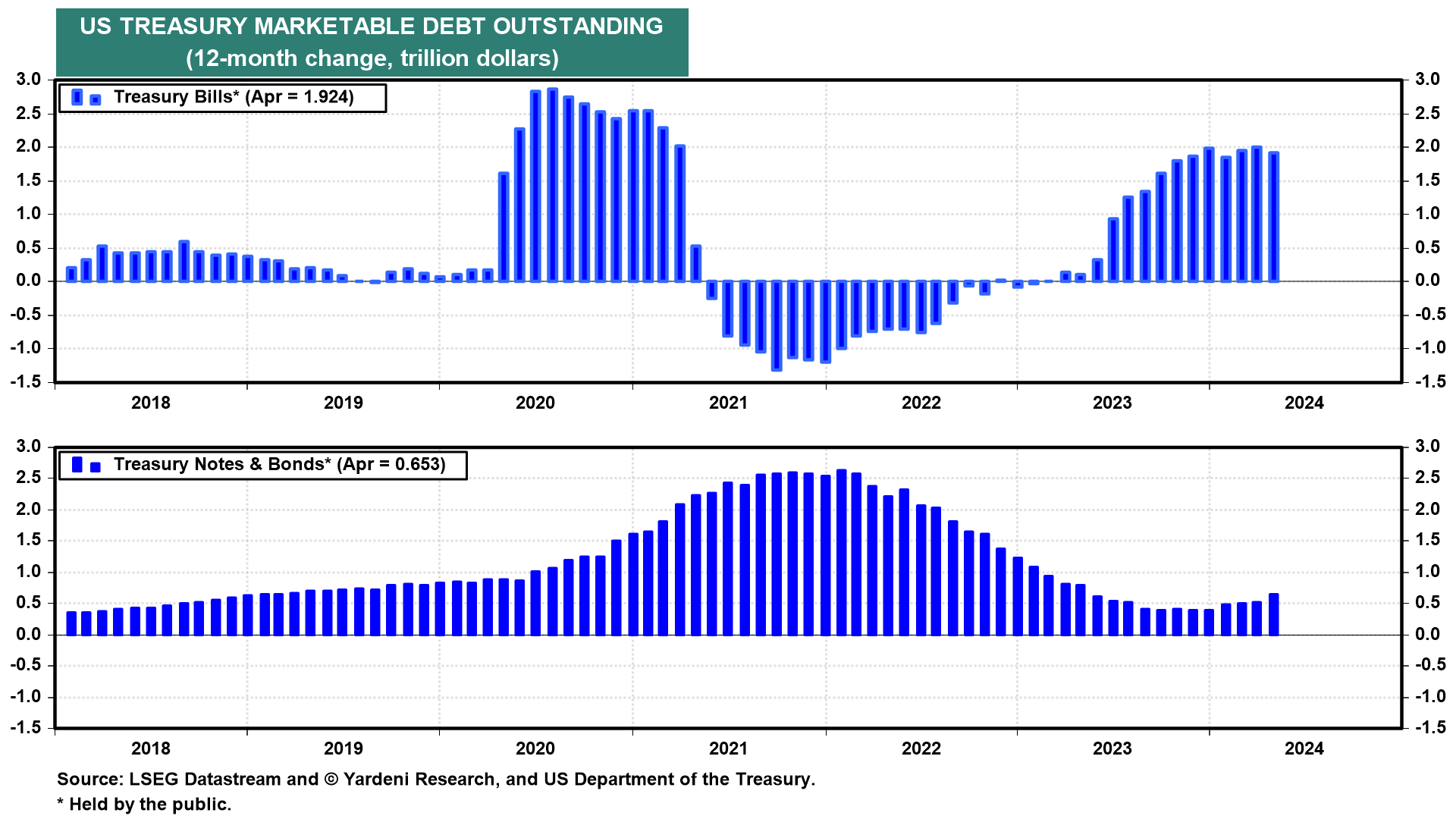

Yardeni: The Blob Keeps Growing. So Why Aren't Bond Yields Soaring? (because if you build it — CONCESSION — they keep coming … to the front end in form of money markets mutual funds…?)

…Why aren't bond yields soaring on all this supply of Treasury securities? The Treasury has been funding most of its needs over the past 12 months through April with Treasury bills ($1.92 trillion) compared to $653 billion in notes and bonds (chart).

Last year, money market mutual funds purchased $1.21 trillion of Treasury bills (chart).

… And from Global Wall Street inbox TO the WWW,

Bloomberg: GameStop Mania Won’t Pack a Punch Like in 2021 (forge the meme’s head TO the ‘flation stuff…)

But irrational trading can still do some damage.

… What to Expect When You’re Expecting (Inflation Edition)

Are US consumers bracing for higher inflation, and does it matter? The latest survey last week from the University of Michigan showed a disquieting rise in the inflation consumers said they were expecting, with a growing contingent anticipating extreme rises. The New York Federal Reserve’s Survey of Consumer Expectations, produced on Monday, shed some more light on this, again showing slight increases in expected inflation over the short term.

However, there may be some relief after the mean expectation recorded by Michigan (in which the most bearish outliers are fully represented) showed an average of above 5% for the next three years. That was the highest in three decades. But the New York Fed survey wasn’t so extreme. It provides the predictions by the 25th and 75th percentile of its respondents (in other words, the 25% who thought inflation would be lowest, and the 25% who expected the highest price rises). If those in the 75th percentile are right, we are in for a tough few years. But they don’t expect inflation to be any worse than they did 11 years ago, when price rises were well under control:

The New York Fed also has a breakout on what is expected for the prices of certain vital services, which strengthens the impression that people tend to be habitually over-negative. Since the beginning of the survey, predictions for the next year’s inflation in medical fees, college tuition and rents have been persistently way too high:

That said, market-based expectations aren’t so much better. The purest expression of expected inflation for the next year is the one-year breakeven — the difference in the yield between fixed and inflation-linked one-year bonds. This is the level of inflation at which the return on the two bonds would be the same, so it is the implicit inflation forecast. Comparing one-year breakevens with actual inflation a year later is instructive. They were broadly accurate during the long post-crisis spell when inflation was under control. But they totally failed to predict the major spikes in inflation. That’s a shame because it’s on precisely these occasions that a good prediction would be useful:

So, how much do inflation expectations matter, when they’re so wildly inaccurate?

FirstTrust: Monday Morning Outlook - Would Trump Reignite Inflation?

… Again, we are not saying inflation won’t be a problem in the years ahead; it likely will be. But it’s likely to be a problem no matter who wins this November.

Cost pressures remain the top issue for small business owners, including historically high levels of owners raising compensation to keep and attract employees,” said Bill Dunkelberg, NFIB Chief Economist. “Overall, small business owners remain historically very pessimistic as they continue to navigate these challenges. Owners are dealing with a rising level of uncertainty but will continue to do what they do best – serve their customers.

Key findings include:

The net percent of owners who expect real sales to be higher rose six points from March to a net negative 12% (seasonally adjusted).

A seasonally adjusted net 12% of owners reported planning to create new jobs in the next three months, up one point from March’s lowest level since May 2020.

A net 26% (seasonally adjusted) of owners plan price hikes in April, down seven points and the lowest reading since April of last year.

Forty percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, up three points from March, which was the lowest reading since January 2021.

The net percent of owners raising average selling prices fell three points from March to a net 25% seasonally adjusted.

ZH: With "Exceptionalism" Like This, Who Needs Enemies?

**UPDATE** there will be NO regular spammation tomorrow — Wednesday, May 15 — as I’m travelling for work and so, if you require a refund please reach out and arrangements will be … oh, wait, you are getting what you pay for … carry on, back to biz on Thursday and … THAT is all for now. Off to the day job…