BOJ CUTS (amount of bonds its buying as Yen stays weak…)) and China SELLS ($139bb bonds to use proceeds to fund recovery …) and USTs prices are UP a touch within their downtrend …

… visual inspired BY NEWSQUAWK morning notes / thoughts (below) and with so little in mind i’ll quit while I’m behind … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly bull-steepening on 65-70% 30d volume after a sideways session in Tokyo (which saw reduced 5-10y Rinban purchases). Some light real$ selling was seen in the long-end into London, while late-morning flow included some bank demand in intermediates. APAC equity performance was modestly negative (NKY -0.1%, SHCOMP -0.2%, KOSPI unch’d). Energy prices have seen a small bounce (CL +0.4%, XB +0.6%) and USD-majors are close to unchanged (JPY -0.1%). S&P futures are showing +6pts here at 7am, with US 2y reals leading the nominal steepening -3bps…

… Friday’s update from the U-Mich Survey saw stagflationary-lite concerns persist, the switch to web-based data collection likely playing some modest role in the top-line & sub-component deterioration as inflation expectations saw a renewed rise in the 12m ahead time-series (3.5% in May, from 3.2% prior). While gasoline prices in the last few weeks likely played a factor, what was more surprising to us was the sub-component for Real Household Income Expectations (next 1-2yrs), which fell -10pts and has dropped -21pts in the last two months to lows last seen in 2012. The only other 10pt drops were seen in June 2008, July 2012 and NOV 2021, and never have we seen it fall so dramatically back-to-back months. Employment anxieties were also at the forefront, with nearly 40% of respondents expecting the UR to rise in the year ahead, up from 32% in the final April print. This matches the NY Fed consumer survey trend of rising expectations of job loss probability (attached), which will be updated for April data today.

… Ruh Roh… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Tentative trade across markets with DXY flat & modest gains in US equity futures; NY Fed SCE due … Bonds are incrementally firmer, though within contained ranges … USTs are a touch firmer but near unchanged overall as the benchmark takes a slight breather from Friday's marked bearish action but remain within a couple of ticks of the 108-21+ trough from Friday with last week's 108-19+ base below.

We anticipate lower yields and a weaker USD should US CPI print in line with expectations.

With EM inflation consistently surprising to the downside, we like being received EM rates and long EM carry.

Equities are pricing in subdued volatility over CPI. We like owning short-dated SPX topside.

… In markets, we see risks as slightly skewed toward lower yields this week. While there will be significant volatility in either a CPI beat or a miss, we think that the market buys bonds on an in-line number for two reasons. First, an in-line core print of 0.3% m/m would be a welcome relief after consistent beats year to date (Figure 2) have likely kept investors cautious on owning duration into the risk event. Second, we think an in-line print would likely translate to 0.2% m/m on core PCE, which would be very desirable progress for the Fed.

… Recapping last week now. On Friday we had a weak reading for the University of Michigan’s preliminary consumer sentiment index for May. The headline sentiment index dropped well below expectations, falling from 77.2 to 67.4 (vs 76.2 expected), the lowest level since November. Respondents’ view of current conditions also deteriorated in May, falling from 79.0 to 68.8 (vs 79.0 expected). Notably, the year-ahead inflation expectations rose from 3.2% last month to 3.5% (vs 3.2% expected), erasing all the index’s decline earlier this year. The 5-10yr expectation also rose from 3.0% to 3.1% (vs 3.0% expected).

The University of Michigan release helped pare back some of the week’s upbeat tone. The upside in inflation expectations saw the number of Fed rate cuts expected by December decline by -5.1bps on Friday (-4.9bps over the week), erasing mid week optimism that monetary policy was heading to a less restrictive stance. Over in Europe it was a similar story, with the amount of ECB cuts priced by December coming down -3.2bps on Friday (and -5.0bps over the week) to 69bps.

Off the back of this, US Treasuries sold off. The 2yr yield rose +5.1bps on Friday, and +4.9bps on the week. Similarly, 10yr yields rose +4.3bps on Friday, although this failed to fully wipe out the decline in yields earlier in the week, as yields ended the week down -1.3bps at 4.50%. Meanwhile in Europe, yields on 10yr bunds were up +2.2bps (+2.2bps on Friday).

DBDaily: Michigan miss, Canada employment beats (visual context of UoMISSagain)

We expect a 0.28% increase in April core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.61% (vs. 3.6% consensus). We expect a 0.37% increase in April headline CPI (vs. 0.4% consensus), which corresponds to a year-over-year rate of 3.42% (vs. 3.4% consensus). Our forecast is consistent with a 0.19% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.22% increase in core PCE in April. We will update our core PCE forecast after the CPI is released and again after the PPI is released.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect a 1.6% increase in car insurance prices as prices continue catching up to costs. Second, we expect the health insurance component to remain flat starting this month as the BLS incorporates new source data on insurance premiums. Third, we expect rent inflation to slow to 0.37% as the gap between rents for new and continuing leases continues to close but for OER inflation to remain strong at 0.45%, reflecting stronger new-tenant rent growth and a larger gap between new- and existing-tenant rents among single-family detached units.

Going forward, we expect monthly core CPI inflation to remain in the 0.25-0.30% range for the next few months before slowing to around 0.2% by end-2024. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect offsets from continued catch-up inflation in healthcare, car insurance, and housing. We forecast year-over-year core CPI inflation of 3.5% and core PCE inflation of 2.7% in December 2024.

MSSunday Start | What's Next in Global Macro: Inflation's Signals

All around the world, Wednesday at 8:30am New York time, market participants will be staring at their screens, waiting for the CPI release. Chair Powell and the Fed made it clear that only inflation is keeping them from cutting rates. This year, the market has gone from pricing almost seven 25bp cuts, starting as early as March, to now pricing just under two cuts, with the start pushed to September.

While Wednesday’s report will be critical for the timing of the first cut, regardless of the print, we remain confident that inflation will trend lower over the year, making the question when, not if, the Fed will cut. If our forecast is right, the April print on Wednesday will not represent a sea change. We expect core CPI to be 0.29%M with a glacial decline in rent inflation, core goods prices falling a touch, and mild reversion of the upside surprise in services inflation. If we are wrong, the market will likely adjust the implied timing of the first cut earlier or later, but we do not think that the path for the year is likely to change much. Where the signal is greatest, it points to disinflation. And where the data suggest upside risk, they are the noisiest…

… A final technical point is that our US team recently documented that the seasonal adjustment has likely overstated inflation in the first quarter of the year, suggesting some arithmetic payback later. Taking all these factors together, inflation should fall over the year … and when it does, the Fed will start to cut rates.

MS: The Weekly Worldview: Divergent, convergent...it's about time

We expect the Fed to start easing in September, ahead of the ECB and the BoE. Growth and inflation paths justify this divergence.

Is a September initiation to the cutting cycle off the table because it is too close to the US elections? Is the appearance of political bias a meaningful impediment for the Fed? In a note with Matt Hornbach, we argue strongly that the timing does not matter. My experience at the Fed for the 2000, 2004, 2008, and 2012 is consistent with that view. In that piece, we document from Fed transcripts that elections have not changed policy decisions. Then, we show in the data that decisions on policy are the same in years with or without elections…

UBS: Time to tax (so, then … a rate CUT will be warranted?)

More details are emerging about US President Biden’s imminent US consumer tax increases. Some of the tax changes are sizable, with suggestions that consumers of electric vehicles from China could be set at over 100%. Steel and aluminum consumers will also pay more to the US Treasury. However, the economic impact is likely to be muted. US President Trump’s taxes on intermediate goods generally squeezed US corporate profits more than they raised consumer prices, and the US is not a big consumer of electric vehicles from China.

Taxes on trade can be justified by a desire to protect a developing domestic industry, or if the exporting country is unfairly subsidizing its exporters. All too often such taxes come under the heading of economic nationalism. As structural change brings increased economic uncertainty and insecurity, blaming foreigners is always a convenient scapegoat.

China’s April price data was not especially exciting. Higher energy prices helped keep consumer price inflation just above 0% year over year. Producer price deflation persists, albeit slightly less than it has been. Neither price measure has any direct relevance outside of China’s borders.

The New York Federal Reserve’s survey of consumer inflation expectations is due. It is as unreliable as similar surveys, correlating to current food and fuel prices.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Cooling Core Inflation Will Offer Minimal Relief to the Fed

Underlying gauge of US inflation probably moderated in April

China, Japan release key economic data; UK wage numbers due

Bloomberg: Bond Traders Wait for CPI to Fuel — or Doom — the Market’s Rally

Treasuries rebounded this month on signs of job-market cooling

But inflation has been sticky, triggering selloffs on CPI days

Bloomberg: A Doomsday Recession Mentality is Keeping the S&P 500 Strong (make this make sense. i’ll wait)

Companies are ready for a recession that never seems to come

Earnings surprises are on pace for their best level since 2022

Bloomberg: This Round of Inflation Data Will Matter Greatly (Authers’ OpED)

After three successive negative surprises, economists are confident that the core US Consumer Price Index will be down. Also, Sweden takes a big risk on rates and James Simons’ legacy…

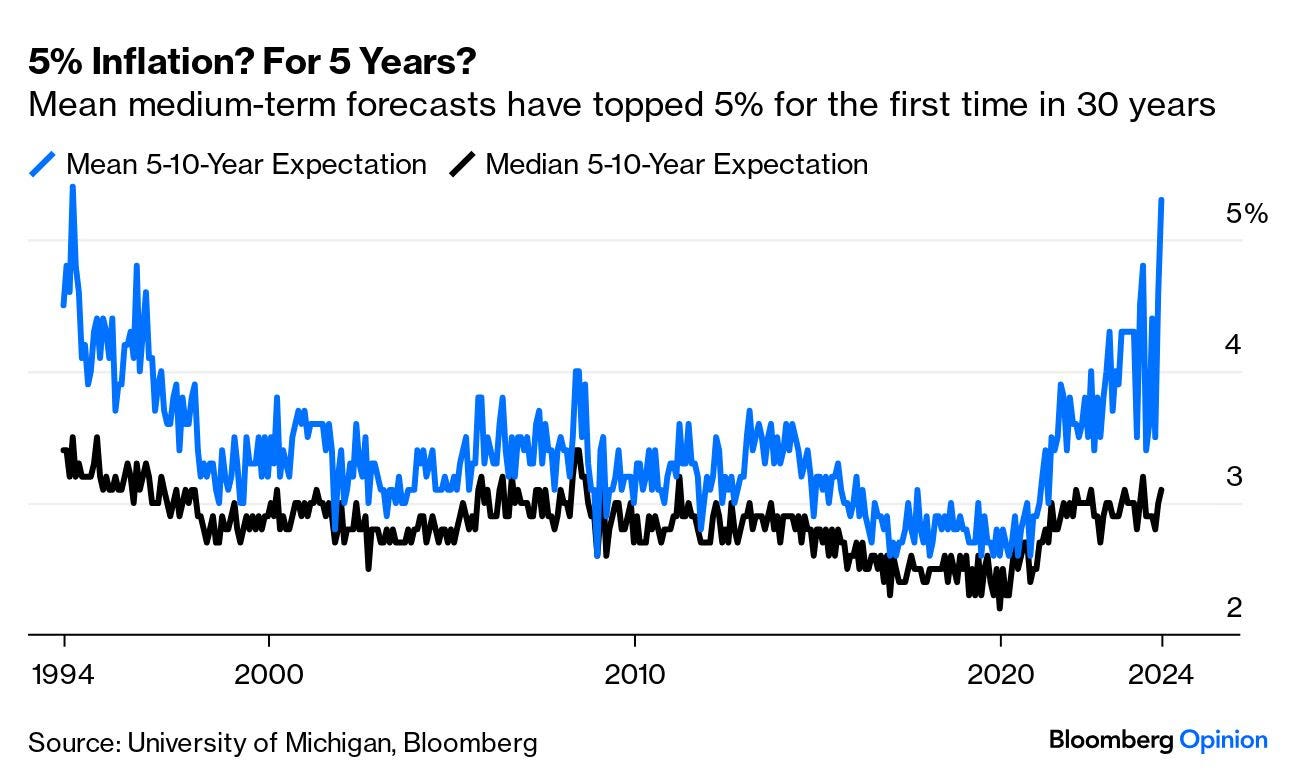

… Then there are the extraordinary results when Michigan asked for forecasts of average inflation over the next five to 10 years. The university publishes both a mean and a median number, and the latter is more widely followed. Given that very few people ever expect prices to go down, outlying high inflation expectations will inevitably skew the mean upward. It’s also true that consumers have long been too negative, and the median has never dropped to the 2% target in the last three years.

All that said, it’s quite something that mean longer-term inflation expectations are now above 5% for the first time in three decades.

There’s a significant mass of people who are convinced that inflation rates are going to rise a lot from here. They probably think so in large part because of their ideological framing, but that doesn’t make their expectations any less real. Long-run expectations have been well anchored for a long time, and it’s strange to see them loosen now, rather than when inflation peaked two years ago. This number is probably a fluke, but until we can say that for sure it does make it harder for the Fed to ease monetary policy.

All of this leaves the situation in fine balance as we await Wednesday’s Consumer Price Index.

Sam Ro from TKer: The state of the stock market in 18 charts (big fan of charts and student of the visual narratives created ‘out there’)

… Higher rates don’t spell doom for stocks 🤔 From Ritholtz Wealth Management’s Ben Carlson: “The relationship between interest rates and stock market performance is murky at best… It’s certainly not a one-to-one correlation where higher rates lead to lower returns. The lowest returns have come in the 3-4% and 7-8% ranges. The best returns have come when rates are 2% or less, which makes sense when you consider rates were only that low during two of the biggest crises this century (the GFC and Covid). Look at the 4% to 6% range, which is where we are now. The returns have been pretty good. Maybe one of the reasons for this is because the average 10 year yield since 1950 is 5.4% (the median is 4.7%). Rates like this occur during normal times (if such a thing exists).“

ZH: Goldman Asks: "Might This Be A Monetary Juncture Akin To 1995 Or 2011" (noting this one for the pre CPI thoughts … for the ‘pro subs’)

… Ahead of next week's April CPI print, we outlined to pro-subs on Friday that traders should expect a "downside surprise" as the lagging OER "crashes" and catches up with real-time metrics.

However, we'll leave you with this from Dohmen Capital Research: "The Fed is being forced to step on the accelerator to enable the financing of the record deficits at the US Treasury. They know that is inflationary, but they have no alternative."

… Finally, in the case you missed economic funDUHmental calendars (YESTERDAY),

The week ahead is jampacked with economic indicator releases. The big ones are for inflation, retail sales, and production. They may be somewhat stagflationary on balance, showing inflation remains too high while economic growth is slowing. Nevertheless, we still expect to see inflation moderate with solid economic growth over the rest of this year. Here are a few observations on this week's key indicators:

(1) CPI. The Cleveland Fed's Inflation Nowcasting model shows headline and core CPI rose 0.41% and 0.31% m/m (3.50% and 3.65% y/y) last month (chart). Those numbers might spook the markets when released on Wednesday because they suggest that inflation remains stuck above the Fed's 2.0% target. The headline rate was boosted by a jump in gasoline prices (chart).

On the other hand, falling used car prices weighed on the core CPI last month…

https://twitter.com/i/status/1789772209247969412

A couple people showed up..........

Corporate Media doesn't want you to see this..............