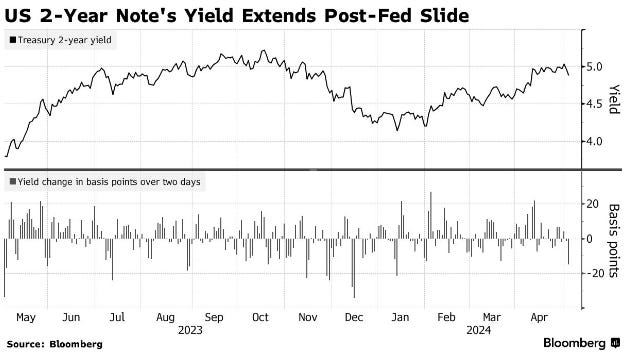

Good morning … Watchin’ 2s for clues with 2yy at what seems to be an important inflection point … awaiting further narrative updates post NFP.

What follows is an abbreviated PRE NFP comment as we all know that Global Wall narrative creation machine will crank back up at about 835a and those who can / will digest ‘news’ quickest, will writeup a weekly note and then look longingly TO Hamptons Hedge and weekend activities …

IS the 2yy sending a message …

2yy: watching 4.865%

… Will 2024 UPtrend come to an end? Dunno and will be watching daily CLOSE as well as weekly … For now … an interesting ZH hit reflecting on labor costs and not unlike ECI from the other day …

ZH: Unit Labor Costs Soar In Q1 As 'AI Productivity Boom' Fails To Show Up

… Will have somewhat more over the weekend and for now, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly bull-flattening on 85% 30d volumes ahead of NFP (Citi 215k, Consensus 240k), perhaps a bit higher than expected given the Japan/China holidays. Our London desk noted an early bid to intermediates with a steepening bias, now reversed in the past hour or so. Fast$ interest was seen in 2s/3s steepeners, while banks have been buying in the long-end. The DXY is a tad softer (-0.1%) with USDJPY lower (-0.3%) as well on light engagement overnight given the Japan outage. APAC equities were mixed (KOSPI -0.3%, HSI +1.5%), the DAX showing +0.4% amid some positivity in US equity futures (S&Ps +0.3%). Crude is a smidge higher at 79.15, and copper has bounced (+1.1%) alongside AUDUSD (+0.4%).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: AAPL climbs post-earnings, NFP & Fed speak ahead … Bonds are mixed but remain rangebound ahead of today’s key events … USTs are flat/incrementally softer with the curve flattening on the margin as the post-FOMC steepening settles into NFP and Fed speak. Currently within a busy 114'25-155'04 range.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

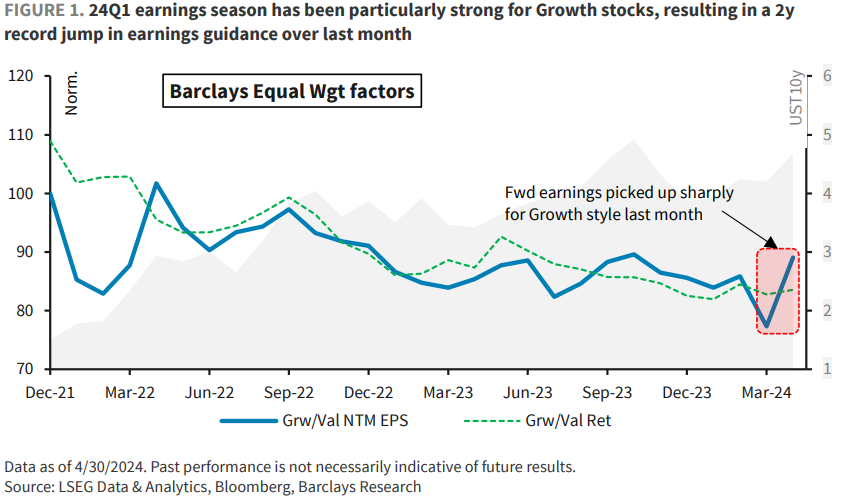

BARCAP Equities Food for Thought: Earnings poised to lift Growth higher

Value's outperformance over Growth from March to mid-April has reversed course over the last two weeks and we expect this to sustain. We think the sharp uptick in earnings guidance for Growth stocks, and the Fed willing to look through recent firming of inflation should favor Growth over Value going forward.

At the latest FOMC, Powell signalled that the Fed has an asymmetric reaction function when it comes to the labor market. Sudden weakness in employment could push the Fed to cut rates, whereas policy is already largely calibrated for continued labor market strength, and would be less responsive to more upside surprises. The market's reaction function should mirror the Fed's asymmetric policy reaction, leaving assets more responsive to weaker-than-expected data than to an upside surprise.

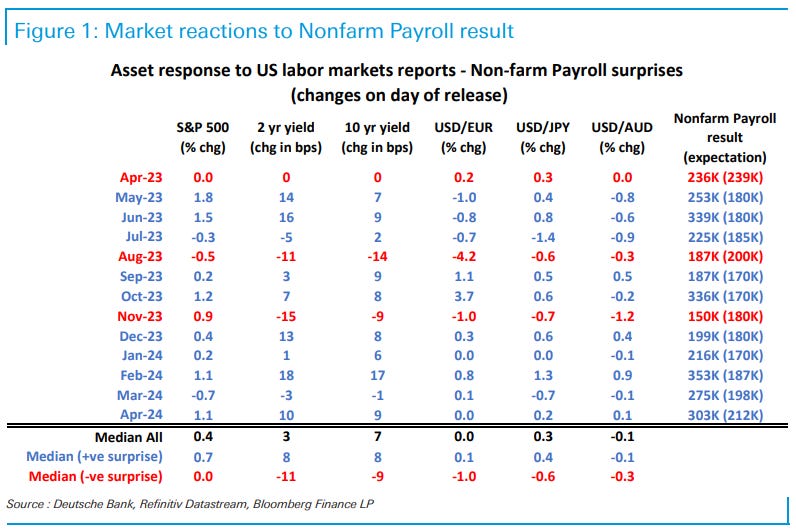

…. As per Bloomberg, a full 75% of surveyed forecasts for both average hourly earning and the U3 unemployment rate are at the medians of 0.3% and 3.8% respectively. Even payrolls has a relatively narrow 120K to 240K range of forecasts…

DB Data DBrief: Let it churn (or not): Fading dynamism of the US labor market

For most of the past four years, the post-pandemic US labor market has been characterized by its remarkable dynamism, including consistent robust employment gains alongside record workers quitting their jobs and a surge in labor supply. However, recent data suggest this dynamism has faded, with the extent of churn in the labor market – movements between different labor market states – declining quickly. Evidence of this is found in low levels of hires, quits, and layoffs.

We show that a summary measure of labor market churn is now at its lowest since 2016 (excluding the pandemic), a level that would typically be consistent with a much higher unemployment rate. We then discuss a few factors that could allow for a tight and resilient labor market to coincide with low churn.

We estimate nonfarm payrolls rose by 275k in April—somewhat above consensus of +241k. Our forecast reflects a favorable evolution in the April seasonal factors and a continued boost from above-normal immigration. Big Data measures generally indicate solid job gains—albeit not as strong as consensus—and our layoff tracker indicates that the pace of layoffs remains low.

We estimate that the unemployment rate edged down but was unchanged on a rounded basis at 3.8%—in line with consensus—reflecting a rise in household employment and flat-to-up labor force participation (at 62.7%). Foreign-born unemployment already fell sharply in March, limiting scope for declines in the April jobless rate. We estimate average hourly earnings rose 0.25% (mom sa), which would lower the year-on-year rate from 4.14% to 4.00%—compared to consensus of 0.3% mom and 4.0% yoy. Our forecast reflects waning wage pressures and a nearly 10bp drag from calendar effects (mom sa). However, we now also assume a 5bp boost from minimum wage hikes for California fast food workers.

Goldilocks: Rising Uncertainty and Term Premium Risks

Consecutive inflation surprises have raised the bar for Fed easing and boosted the odds of higher-for-longer policy rates, and markets have widened the range of potential outcomes for rates accordingly. Front-end and belly rates have been most responsive to these shifting risks thus far, but rising uncertainty around the policy rate outlook also has the potential to transmit through long-end yields via repricing of the term premium.

Empirically, we find that term premia respond strongly to macro uncertainty, which declined sharply following the earlier progress on disinflation and the FOMC’s dovish pivot late last year. Our estimates suggest this dynamic accounted for most of the ~50bp decline in term premium since October last year, and if policy rate uncertainty is to return to its previous cycle peak this could see 10y yields reach back above 5%.

However, we would view this as the upper end of the plausible range for yields rather than the modal case. The strong pushback against rate hikes by Chair Powell should cap the right tail risks for now and limit the distribution of outcomes, while a less uncertain outlook for debt supply—even if at a high level—also paints a friendlier picture for risk premium than last year.

Beyond policy rate uncertainty, two other risks to term premium bear close watching. First, fiscal policy uncertainty will likely pick up in the summer ahead of the election, posing upside risks to term premium of around 10-15bp based on history. Second, heightened policy uncertainty boosts risk premia not only for bonds but also for risk assets including equities. This induces a positive correlation between stock and bond returns and argues for greater compensation for holding duration risk all else equal, and could act as a near-term floor for term premium.

Goldilocks: Productivity Growth Slightly Below Expectations; Trade Deficit Flat; Jobless Claims Hold at Low Levels

BOTTOM LINE: Nonfarm productivity increased 0.3% in the first quarter (qoq ar), slightly below expectations, and the year-on-year rate increased 0.2pp to +2.9%. Unit labor costs increased 4.7%, above expectations. The trade deficit was roughly flat in March and was revised wider for February. Both initial and continuing jobless claims were unchanged at low levels. The March international trade report did not have significant implications for our Q4 or Q1 GDP tracking estimates. We will update these after the mid-morning data.

Goldilocks: Factory Orders in Line but Core Capex Shipments Revised Down; Lowering Q2 GDP Tracking to +3.3% (again see whatever you wanna see … LOWERING or still robust 3.3%)

BOTTOM LINE: Factory orders increased by 1.6% in March, in line with expectations, while growth in February was revised down slightly. We lowered our Q2 GDP tracking estimate by 0.1pp to +3.3% (qoq ar) and our domestic final sales estimate by the same amount to +2.7% (qoq ar). We left our past-quarter GDP tracking estimate unchanged at +1.6%, in line with the advance reading.

We update our rates forecasts alongside a revised Fed call. NatWest Economics now expects the Fed to start cutting in December (from September) in 25bps increments from there – once per meeting. We still expect 225bps of total cuts but we think the Fed will now not reach neutral (3.00%-3.25% in our view) until the end of 2025. Given this, we update our rates forecast to now see a longer period for yields at a higher rate range, before slowing rallying and steepening into and over the course of the Fed cycle.

For the refunding, there were few surprises but given the Fed's minor surprise on QT, we shift our near-term expectations on bill issuance slightly. As guided towards by Treasury, we now see bill issuance rising by $5bn over the next two 4w and 8w issues, before these increases are unwound in mid-June into tax receipts. Short-dated bills should again rise in July and reach the peaks of Feb ’24. Meanwhile, we also expect CMB’s to be utilized regularly as they transition to become a regular “benchmark” issuance – CMBs should increase in May, slow in June, and then increase again in August with occasional step ups / step downs through the end of the year.

US employment report Friday looms. Around 119,000 companies will be asked about their employees. Around 67,000 companies will not bother to reply. Markets will obsess about the data anyway. The expectation is for slower job creation (as measured by payrolls), with a stable monthly change in average earnings (which are not the same thing as wages).

Uncertainty about immigration clouds US employment data. The household survey may be less likely to pick up on illegal immigrant employment than the payrolls survey. Increased immigration may improve trend rates of growth—directly by increasing the labor force and productivity, and indirectly by easing labor force bottlenecks that hinder other job creation.

The possibility of a higher trend rate of growth matters to the economics of Federal Reserve policy, implying more spare capacity and a reason to cut rates. However, the politics of a labor market that is not unambiguously weakening is likely to limit expectations for an imminent rate…

Wells Fargo: Q1 Productivity: Ignore the Quarterly Chop—Trend Favorable for Inflation

Summary The latest productivity report is not as discouraging as viewing the quarterly prints in isolation would suggest. Slower growth in Q1 paired with a pickup in hiring and hours worked led productivity growth to nearly stall in Q1 (+0.3% annualized), while unit labor costs (ULCs) strengthened to a 4.7% annualized rate. However, the unfavorable outturns for both productivity and ULCs are reminiscent of the first quarter of 2022 and 2023, hinting at some difficulty in fully accounting for seasonality in the data.

When measured over the past year, nonfarm productivity growth is up 2.9%, the strongest gain in three years. Unit labor cost growth, which can be viewed as the productivity-adjusted cost of labor, increased just 1.8% over the past year. The downward trend in ULCs points to inflationary pressure from the jobs market continuing to subside and is supportive of inflation resuming its downward trend later this year.

A long-term outlook for the US 30-Year Treasury Yield $TYX

Where are rates heading?

Bloomberg: Traders Pull Forward First Full Fed Rate Cut to November Ahead of Jobs

Repricing comes after FOMC decision, ahead of key jobs report

But two-day bond rally leaves little room for further advance

… The market took flight after Fed Chair Jerome Powell struck a less hawkish tone than feared, signaling a rate hike was unlikely and that cuts can be expected once economic data provides clear evidence that inflation is moving downward. Market-friendly data may come as soon as Friday with the April jobs report — although Treasuries’ capacity for further gains may be limited given the recent advance.

Treasury yields have experienced large swings in response to jobs data over the past year, and “I expect that historic volatility to hold if there’s a large surprise,” said Angelo Manolatos, an interest-rate strategist at Wells Fargo Securities LLC. “But in order to get a sustained rally, we need inflation data to start coming in on the softer side.”

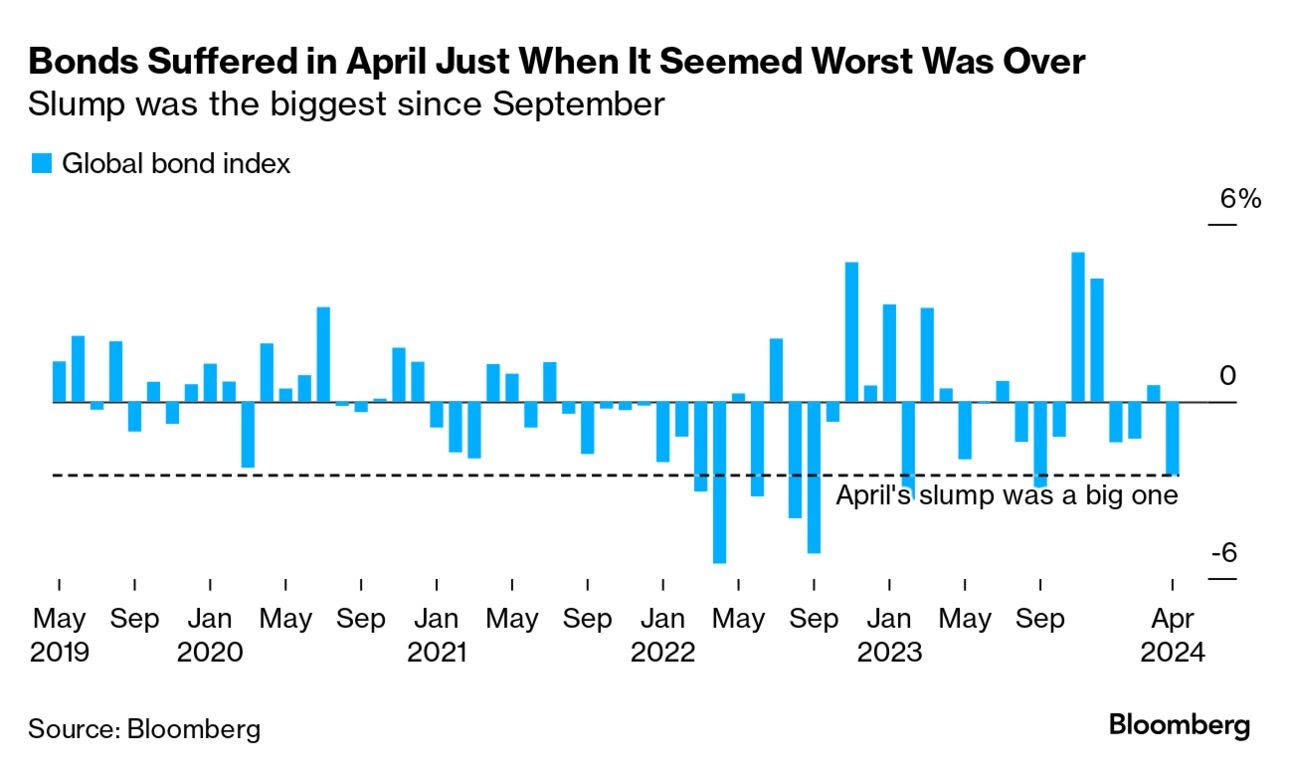

Unusual Cruelty April was a particularly brutal month for bonds as strong inflation and economic data in the US, and elsewhere, stunned investors. Rates traders further wound in bets on interest-rate cuts from the Federal Reserve, with some options action eyeing the potential for a hike. Other markets saw similar trends: Australian traders even switched to seeing rate increases as more likely than easings this year.

The policy path whiplash delivered the worst month for global bonds since last September’s meltdown, with Bloomberg’s gauge of worldwide debt securities sliding 2.5%. The pain was perhaps intensified by the fact that April has traditionally been among the more pleasant months for the index, posting only 11 declines over the past 30 years.

Despite many saying yields are now high enough to bolster the long-term outlook, Bill Gross for one doesn't agree. The total return strategy he pioneered in the late 1980s is now “dead,” Gross wrote, arguing there’s just not the same room for price appreciation. “Don’t let them sell you a bond fund.”

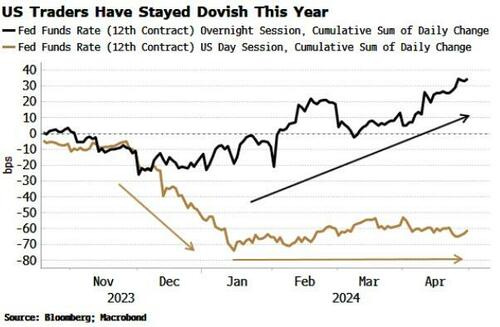

Bloomberg(via ZH): US Traders Took Powell's Pivot More Seriously Than Foreigners

… Here we can see US-based trading drove the proliferation of rate cuts expected at the end of 2023. Since then, US-based traders have not changed their dovish view.

Almost all of the hawkish tilt this year - eradicating most of the cuts expected - came in trading during non-US hours.

It looks like mainly US-based traders took Powell’s pivot in December more seriously than those predominately based abroad. Either way, risk-reward now favors siding with the domestic team for a more dovish rate outcome than is currently priced.

Discipline Funds Chart of the Week: The Softening Labor Market (either gonna be heroic and less than optimally timed …)

… As the following chart shows the quit rate tends to lead hourly earnings. The basic logic is that quits are indicative of how much negotiating power workers have. When they are quitting they’re exercising their power to leave one job for another without worry. This tends to lead wage data because those workers are quitting in an environment where labor favors capital in terms of negotiating power. And while the quit rate will be recorded in real-time the labor market contracts reflected by those negotiations should have more of a lagging reflection in actual data. And the data confirms this logic as earnings tend to lag the quit rate…

… Finally, with all THAT said and in mind AND as narratives about to be shape shifted again by time 831a rolls ‘round, having absolutely NOTHING to do with ANYthing …

… THAT is all for now. More over the weekend but for now … Off to the day job…

Did we just get an accurate number from the BLS, finally ???

Defending the Republic

Good News Friday edition

https://substack.com/app-link/post?publication_id=726749&post_id=144253046&utm_source=post-email-title&utm_campaign=email-post-title&isFreemail=true&r=1ecjk0&token=eyJ1c2VyX2lkIjo4NDU2NjAxNiwicG9zdF9pZCI6MTQ0MjUzMDQ2LCJpYXQiOjE3MTQ3MzcwNjYsImV4cCI6MTcxNzMyOTA2NiwiaXNzIjoicHViLTcyNjc0OSIsInN1YiI6InBvc3QtcmVhY3Rpb24ifQ.DWo4ho0cRxC4orSTFBMVuGwz53o_0WB3FGyRjVNxT9w