while WE slept: USTs 'modestly bear-steepening after yesterday's Waller induced bull-steepening'; "Less is more"; #2025 dart-throwing (UBS, lower rates)

Good morning … as I walked dog earlier today I heard that 10yy were about 4.25% and so, upon further review …

10yy: middle of (5.00 - 3.60) range is just about 4.30 and so …

… middle range and bearish leaning momentum … what could possibly go wrong?

AND I’ll move along …first, a quick look at the day ahead …

CalculatedRisk: Wednesday: ADP Employment, ISM Services, Fed Chair Powell Discussion, Beige Book

… and a quick review

ZH: Job Opening Unexpectedly Surge With Biggest Increase in 14 Months; Quits Also Soar

… so this is good news OR is good news bad news, I forget … ZH notes it was so good it was, um, well … you know (bad) as ZH notes. Importantly, whatever you think you think and are to infer from the data, please be careful as it’s ALL a complete GUESS … as ZH continues

… Finally, no matter what the "data" shows, let's not forget that it is all just estimated, and it is safe to say that the real number of job openings remains still far lower since half of it - or some 70% to be specific - is guesswork. As the BLS itself admits, while the response rate to most of its various labor (and other) surveys has collapsed in recent years, nothing is as bad as the JOLTS report where the actual response rate remains near a record low 33% …

In other words, more than two thirds, or 67% of the final number of job openings, is made up!

… here is a snapshot OF USTs as of 700a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US futures tilt higher ahead of Powell & European paper awaits French no confidence vote … The US curve is modestly bear-steepening after yesterday's Waller induced bull-steepening. Commentary from Fed officials since from the likes of Daly has done little to talk up the odds of a pause later this month. Today sees US ADP, ISM Services ahead of Chair Powell at 18:45 GMT. Mar'25 UST has broken below Tuesday's low and is eyeing the WTD trough at 110.23.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… here’s an adult recap of the JOLTS data from across the pond …

BARCAP: October JOLTS: Signs of stable labor demand

Job openings rebounded in October following September's decline, with the updated trajectory now looking fairly stable since early summer. Although the hiring rate fell amid hurricane-related disruptions, we see little in today's estimates that would move the needle for the FOMC.

… and same shop thinkin’ bout tariffs and stocks …

BARCAP U.S. Equity Strategy: Food for Thought: Another Salvo of Tariff Threats

Trump's latest expanded tariff threats against Canada, Mexico, and China could amount to a -2.8% drag on SPX EPS if fully enacted, with Materials and Discretionary most at risk. However, we view these threats as more likely to be a a negotiating tactic, with low likelihood of implementation.

… me too. The fella DID write a book, “The Art of the Deal”

… in this next note, one of Global Walls fan fav statEgerists sounds off on a couple things I could ‘buy into’ (ditchin’ NEUTRAL concept and stop with the forward guidance — essentially DOGE the Open MOUTH committee) …

Over the last few days both Governor Waller at the Fed and Board member Schnabel at the ECB have spoken out on monetary policy. Their approach is in our view at best unhelpful and at worst counter-productive and does not acknowledge the huge level of uncertainty ahead.

Please ditch the neutral rate. Many at the Fed and ECB continue to frame the policy debate in terms of the neutral policy setting. But it is nearly impossible to know where this is. In the US, model estimates are nearly 200bps wide and historical revisions can be very large too. Imminent large structural shocks from the US and Europe could push neutral rates materially higher or lower. And imminent large cyclical shocks could well force policy below or above neutral anyway. In this context, talking about neutral rates is akin to piloting a plane in a storm with a view to the weather forecast next year. Better focus on the storm.

Please ditch forward guidance. In her latest interview, Isabel Schnabel stressed policymakers should not tie their hands with forward guidance; yet subsequently warned against the ECB moving into accommodative territory. Christopher Waller expressed confidence that the direction of monetary policy over the medium term is clear: downward, all at the same time accepting that inflation visibility is low. How is it possible to be so confident in such forward looking statements when we don't know if the French fiscal stance is about to sharply contract, if a major trade war is about to unfold, or if the US labour market is about to materially tighten via a reduction in immigration? Admittedly, it may be difficult for central bankers to comment on political developments. It might be better to avoid commenting on future policy all together…

In a stunning political event overnight, South Korea's president declared martial law for the first time since 1979. Later, the National Assembly voted to block the decree and the cabinet agreed to rescind the order. We see the uncertainty surrounding the economy and politics remaining high and likely to dampen sentiment if the situation persists

… same shop on overseas / geopolitical developments …

ING: FX Daily: Geopolitics just another reason to hold dollars

If US exceptionalism and the potential for a second Trump administration weren’t enough to hold dollars, geopolitics and events in South Korea yesterday only add to the argument. Expect the market to keep one eye on Korea today, but also take note of central bank speakers and US data. In the CEE, we see the risk of continuing strength in CZK and PLN

USD: Rates, liquidity and geopolitics keep dollar supported

… unsure if I’ve seen / passed along this next 2025 outlook and so …

… In our base case, we believe that central banks are poised to cut interest rates further in the year ahead and that returns on cash will fall. As such, we believe investors should position for lower rates by putting cash to work in investment grade bonds, diversified fixed income strategies, and equity income strategies to sustain portfolio income …

…Portfolio income strategies can offer attractive yields Yields across fixed income and equities, including a high dividend + call overwriting strategy

… We think there is more to go in equities. With markets powered by falling interest rates, solid economic growth, and transformational innovations, we expect the S&P 500 to reach 6,600 by the end of 2025—around a 10% price return from current levels. Tariffs and geopolitical uncertainty are likely to contribute to volatility for European and Chinese markets in the year ahead …

…Rate cuts support US equities without recession S&P 500 average performance (indexed to 100) following first Fed rate cut

…Asset class expectations

Cash Recent years have been dismal for real returns on cash, with higher interest rates not sufficient to offset the surge in inflation. Since the start of the decade, the real purchasing power of cash has fallen by 8% in US dollars, 13% in euros, and 6% in Swiss francs.

We expect cash to remain among the worst-performing major asset classes. A rate-cutting cycle is underway, eroding future returns on cash. Meanwhile, secular trends such as deglobalization, decarbonization, higher debt, and an aging population may put periodic upward pressure on inflation, eroding cash’s after-inflation returns.

We advise investors to shift excess cash deposits and money market funds into assets that provide higher and more durable sources of income.

Government bonds Government bonds have had one of the worst fiveyear periods in modern history, with the Bloomberg US Aggregate Government bond index delivering a nominal negative return of 2.8%.

Conditions for government bonds have improved lately, with yields now higher and lower inflation and central bank rate cuts ahead.

That said, because of strains on public finances, investors may increasingly demand higher risk premia for government bonds. And while central banks may use their balance sheets to smooth financial market functioning, investors may need to prepare for greater volatility on longer-dated debt.

We believe investors should therefore supplement core government bond holdings with alternative sources of income, including investment grade credit, fixed income hedge fund strategies, or private credit funds.

… AND those in the covered wagons thinking outloud ‘bout the flation …

Wells Fargo: Inflation: Universally Hated, but Unevenly Shouldered

Summary

Prices are still rising faster than the pace consistent with the Fed's inflation target, making it difficult for consumers to feel like they are getting any meaningful relief. What's more, inflation continues to affect some consumer groups disproportionately. The Consumer Price Index (CPI) calculates the average change in prices across the average consumption basket. Yet, spending patterns vary widely, leading to significantly different inflation experiences. To determine which groups inflation is weighing on the most, we dust off our earlier work constructing unique CPIs based on the Consumer Expenditure Survey (CES). Across three demographic groupings, we find:

Income: Lower-income households have faced the strongest inflation not just over the past year, but over the past four years following outsized increases in the cost of essentials like housing, electricity and food at home. Because lower-income consumers devote a larger share of their spend to necessities, the continued elevated rate of inflation in essentials has weighed most on them.

Race/Ethnicity: Asian households have faced the highest rate of inflation over the past year, although on a cumulative basis have seen the least-egregious rise in living costs this cycle. In contrast, inflation has been lowest for Hispanic & Latino households the past year, even as it has been—along with Black households—the steepest over the entire past four-year period.

Age: Rising healthcare costs have led to seniors facing the highest rate of inflation this past year. Meanwhile, Gen-X households have experienced some of the least-severe inflation over the past year and over the cycle as a whole as they tend to devote a relatively high portion of outlays to items that have seen a less-dizzying rate of price increases.

Of course, the difference in the recent rate of inflation and the cumulative rise in living costs across consumer groups does not fully capture the different experiences with price increases. Consumers with less take-home pay—who are more likely to be Hispanic or Latino, Black and/or young—are more constrained in their ability to adjust to higher prices. Real income is also an important factor. The lowest-income households have seen the largest gain in inflation-adjusted incomes over the past four years, but the improvement in real income came in the first two years of the pandemic. Gains have eroded more recently due to not only weaker growth in nominal income, but the stronger rate of inflation lower-income households are facing than those higher up the income spectrum.

… and a final word on jobs from Dr Bond Vigilante …

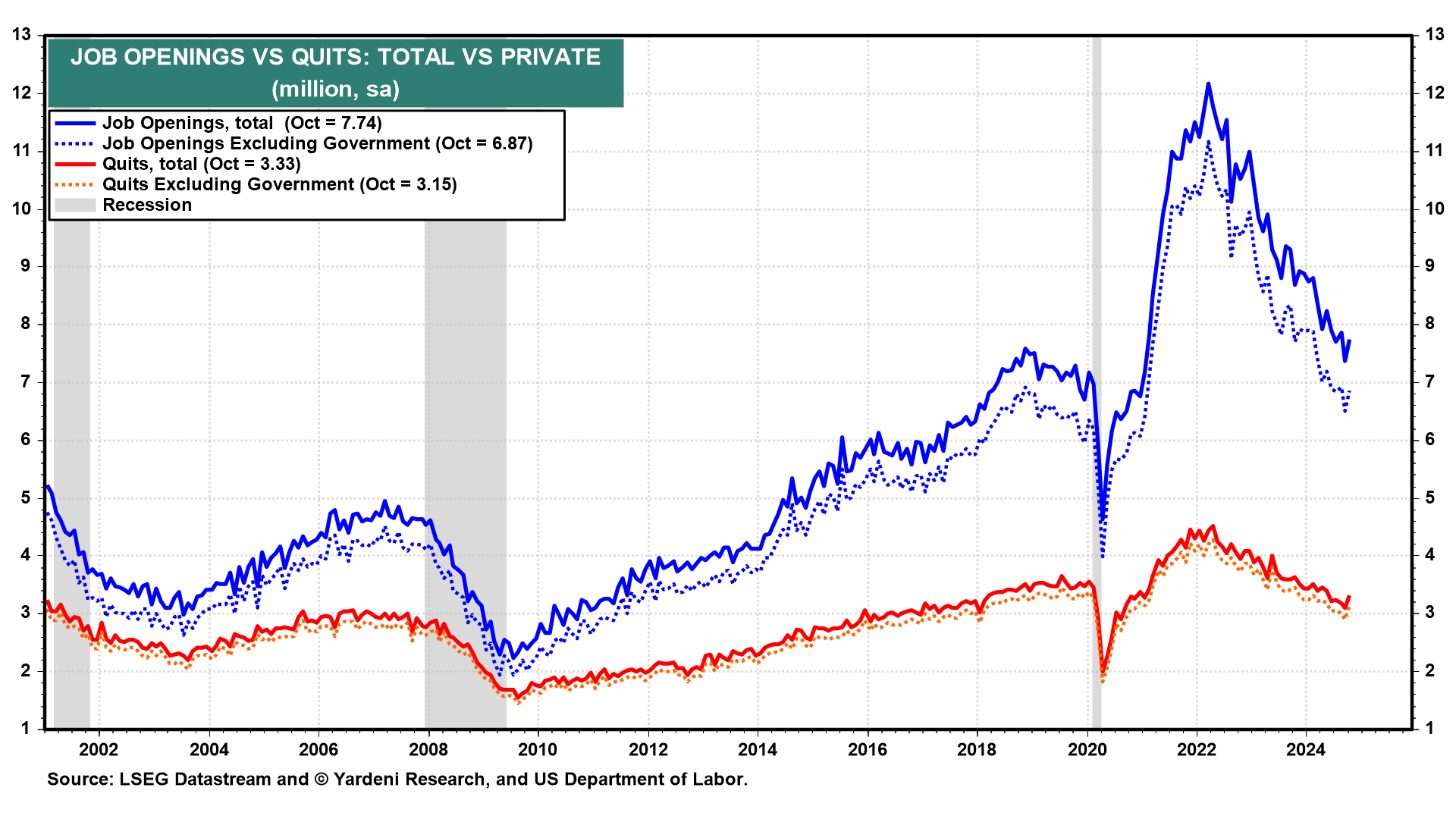

We've contended all year that the labor market was normalizing from the unsustainable pace of hiring during the pandemic. We disagreed with the view that it was weakening. Now we are turning more upbeat about the outlook for employment. Our bet is that the animal spirits unleased by Trump 2.0 will soon be reflected in more job openings and a faster pace of hiring. Today's JOLTS report about labor market conditions was for October, just before Election Day. The results were mixed but encouraging on balance:

(1) October's job openings rose 372,000 to 7.74 million (chart). While hires fell by 269,000, layoffs decreased 169,000 and quits increased by 228,000. Bad weather, labor strikes, and uncertainty regarding the US elections probably depressed hiring in October. Still, the labor market's broad resilience in the face of those pressures is significant. More workers quitting their jobs suggests they are confident about their ability to earn higher wages elsewhere. The animal spirits unleashed by Trump 2.0 should boost hiring during the final three months of this year and well into next year, in our opinion.

… so, more upbeat = Santa PAUSE? Somehow I’m not sure as I get sense no matter WHAT happens, balance of Global Wall will find way to say ‘I told ya so’ …

… And from Global Wall Street inbox TO the WWW …

… and, ‘bout that next CUT (or Santa Pause) AND don’t look now, but EARLs on the move … a view …

Bloomberg OpED: Korea's crisis is just a small part of the picture

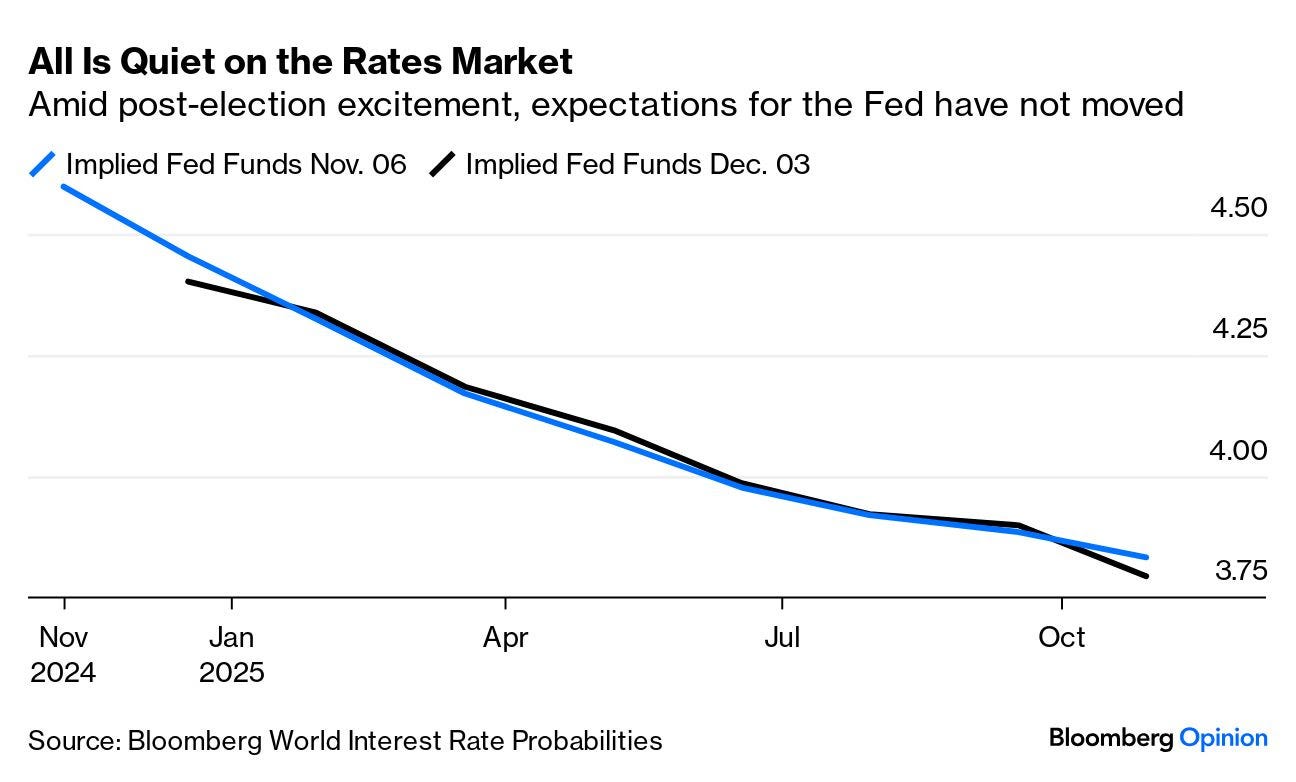

…Another Cut

A further cut of 25 basis points to the Federal Reserve’s policy rate later this month looks ever more likely. Ahead of the non-farm payrolls data for November, due on Friday, which could still slip things up, the Fed seems plainly to be moving in that direction. They also seem highly unlikely to cut any further at their first meeting of next year. Amid all the excitement in the month since the Federal Open Market Committee last met, only hours after the US election, expectations for the central bank have been remarkably calm. Overnight index swaps suggest that rates will continue to come down, but only steadily, over the next year:

One data point to support the doves came from manufacturing supply manager data, which has unduly bearishly signalled for a year that the industrial sector is in recession. In 2021, its numbers proved to be a good leading indicator that price rises were coming unanchored. Surprisingly, the latest reading has dropped right back to the 50 level that suggests prices are in balance. That makes it far easier for the Fed to cut:

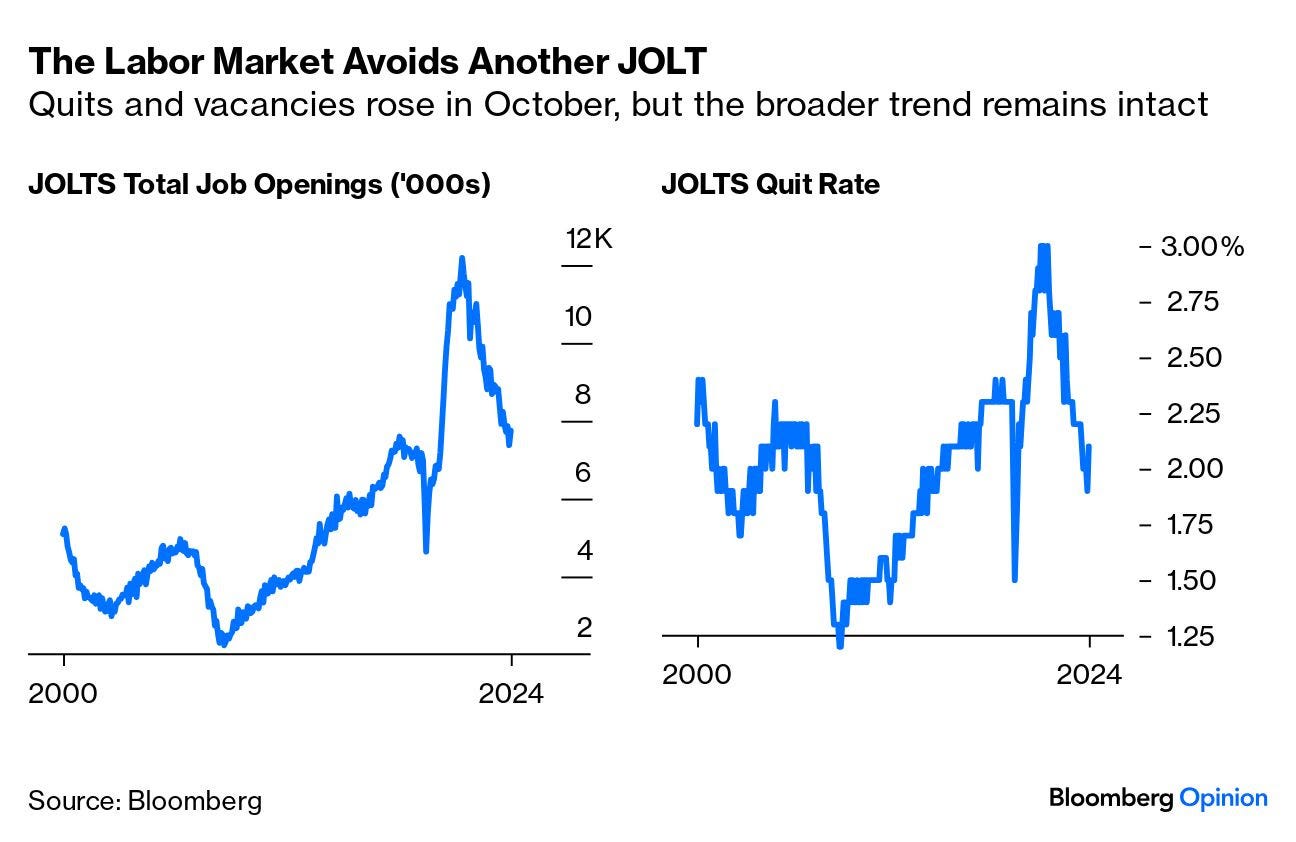

The Job Openings and Labor Turnover Survey (JOLTS), which comes out with a month’s lag, suggested that the numbers of people quitting their jobs rose in October, as did the total number of openings — not the direction that would reassure the Fed that it can relax its inflation guard:

However, closer examination shows little in the JOLTS that would put off the Fed from making at least one more cut. The numbers are volatile, and Samuel Tombs, chief US economist at Pantheon Macroeconomics, suggests that the latest report actually bolsters the case for a December cut. Comparing the official data with the new job postings index kept by the internet job search company Indeed, he shows that they’re consistent with a continuing gradual downward trend.

Meanwhile, the quits rate is a great leading indicator for private sector wage growth, a critical measure for the Fed. Even with the latest slight pickup in voluntary deparatures, it points to continuing deceleration in pay rises.

Fed speakers have been out in force. While none will promise a cut this month, and stress that there’s more data coming in the next two weeks, they leave little doubt that the most likely path involves a cut at the Dec. 17-18 meeting, and then a pause. Governor Christopher Waller gave the clearest steer at a conference on Monday:

At present, I lean toward supporting a cut to the policy rate at our December meeting. But that decision will depend on whether data that we will receive before then surprises to the upside and alters my forecast for the path of inflation.

The most important factor, which Fed voices cannot address directly, is politics. The Trump agenda could reignite inflation, while the Fed might come under pressure to make further cuts. With a new chair due to be nominated in about a year, and the incoming administration batting around possible changes to the central bank’s independence, they need to be as unobtrusive as possible for now, and retain optionsfor whatever 2025 might bring.

Trump nominates Jerome Powell as Fed chair in 2017. Source: Bloomberg

Having cut by a full percentage point to end the year, the Fed also then has greater credibility in the opening months of Trump 2.0, when its credentials could be tested. Absent a shockingly strong employment report later this week, it’s best to pencil in a December cut, and then leave the paper completely blank for 2025.

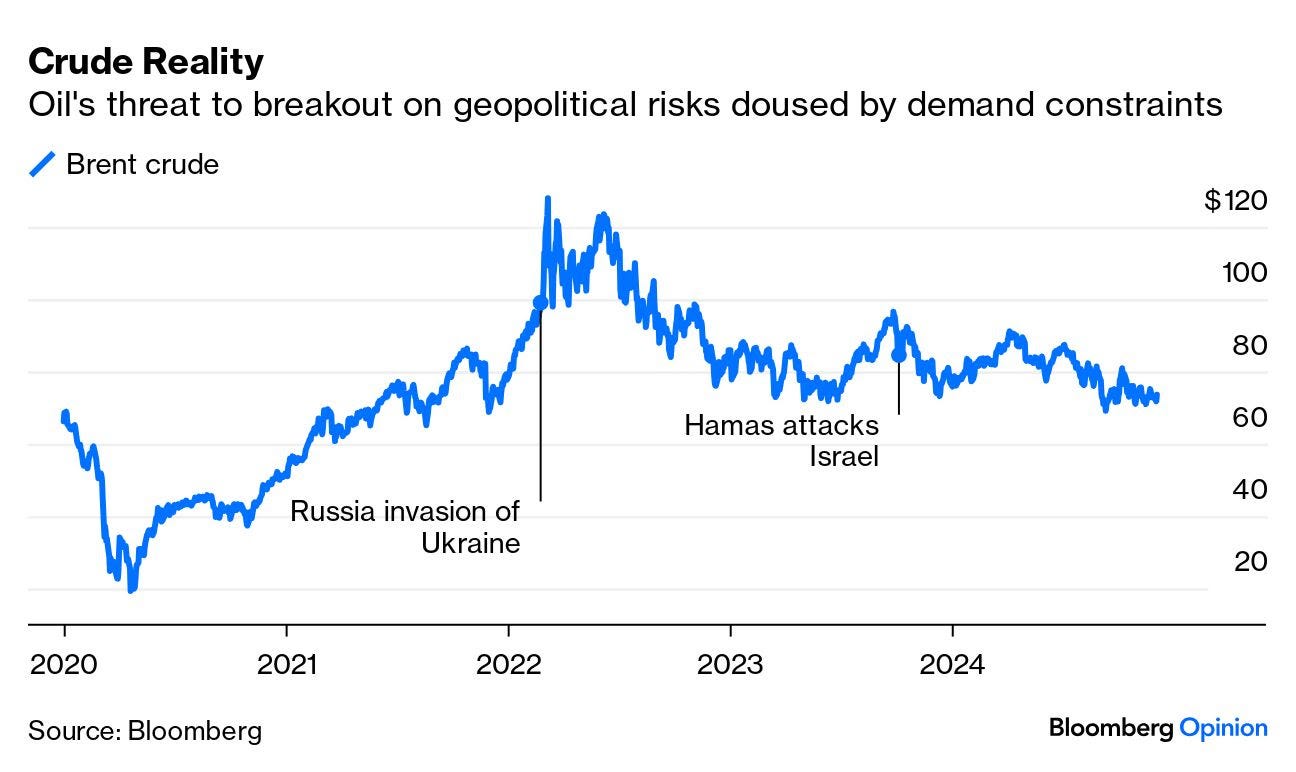

Crude Reality

Oil is on the move, rising by more than 2% to its highest point in about two weeks after the US announced sanctions targeting Iranian oil thatcould potentially limit supply. But despite geopolitical risks like this, a glut has kept prices in check for the last two years. Indeed, it’s trading more than 4% lower for the year, despite escalation in the Middle East and nuclear fears in the conflict between Russia and Ukraine. Through wars and a pandemic, oil has climbed less than 9% since 2020.

The Organization of Petroleum Exporting Countries’ plans to limit supply partly explain oil’s upward movement. The cartel, meeting later this week, hopes to delay increasing production — due to commence with an initial hike of 180,000 barrels a day in January — by another three months. But trying to limit the glut coexists with limited demand. Trump 2.0 could act as a further drag. How so? Bank of America’s commodity team argues that if the global economy is poised for a soft landing, an abrupt shift in US policy would increase the short-run risks to global growth and therefore the entire commodity complex. The BofA team led by Francisco Blanch argues that with non-OPEC supply poised to increase meaningfully in 2025 and demand growth likely to remain steady (or drop materially if Trump tariffs come into play), incremental supply could outpace the projected demand increase:

Oil markets have already been trending lower for some time, only gaining occasional support from geopolitical tensions in the Middle East. As prices slip lower, energy exploration and production private companies could cut back on well completions and, ultimately, crude oil production growth, eventually allowing for some price support.

With prices hovering around $73 per barrel, there’s some incentive for producers to ramp up output,or “drill, baby, drill,” as Trump would put it. Recent surveys from the Federal Reserve banks of Kansas and Dallas estimate producers’ breakeven price at about $64 per barrel. While the price has stayed above this floor post-pandemic, its impact on companies’ margins is profound. Respondents in the Kansas survey suggest $89 per barrel (30% above current levels) is needed for a “substantial increase” in drilling to occur.

Without a dramatic price increase, Trump’s energy policy faces severe constraints. Harry Colvin of Longview Economics adds that Energy secretary-nominee Chris Wright’s planned attempt to boost production would meanless regulation and more permits. It’s unlikely to make any meaningful difference. Overall, weak demand is keeping a lid on the oil price, and neither OPEC+ nor the frightening geopolitical risks of the moment can lift it. The key development that could change that would be economic revival, particularly in China.

… here are a few choice words and visuals from one of the brighter spots out there in the Global Wall landscape and one who reminds ME of a very young, skillful Lacy Hunt …

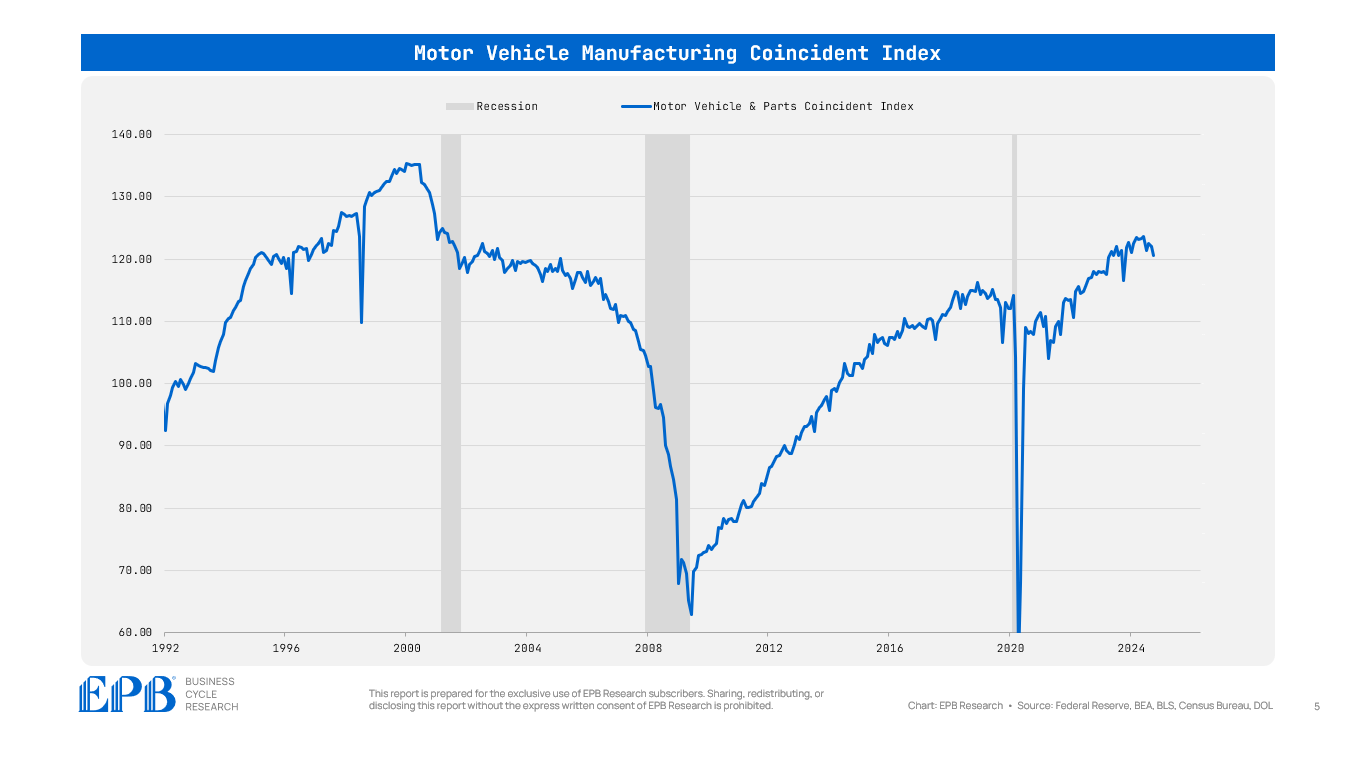

EPB Research: The State of US Manufacturing Analyzing the depth & duration of the contraction in US manufacturing production and employment.

Next to residential construction, the manufacturing sector is the most influential determinant of the Business Cycle.

It’s often suggested that the manufacturing sector’s shrinking relative size has lessened the influence in determining the fate of the Business Cycle, but that declaration is incorrect.

Moreover, it’s been postulated that the US economy has remained resilient in spite of a multi-year contraction in US manufacturing activity. That, too, is incorrect.

The US economy has remained resilient due to a lack of contraction in manufacturing activity…

… In 2021 and 2022, new orders exceeded production by such a large amount, that multiple years worth of backlogs were created that allowed production and employment to continue without a continued flow of new orders.

This phenomenon is evident perhaps most strongly in the motor vehicle manufacturing sector, which saw a major increase in coincident activity in 2023 and 2024, feeding off production backlogs accumulated in 2021 and 2022.

Most leading measures of manufacturing activity remain weak, and production backlogs are wearing thin in most sub-categories, which is why the Coincident Indexes, particularly the durables index, are starting to contract after an unusually long lag time.

The economy has not remained resilient in spite of a contraction in manufacturing; the economy has remained resilient because of a lack of contraction in manufacturing.

It’s far from coincidence that the Federal Reserve shifted from rate hikes to a long pause to rate cuts as actual manufacturing activity moved from expansion to the beginning of a contraction.

… and somewhat MORE ON DECEMBER (than offered HERE) … and a bit of a cautionary tale as far as what may be ahead …

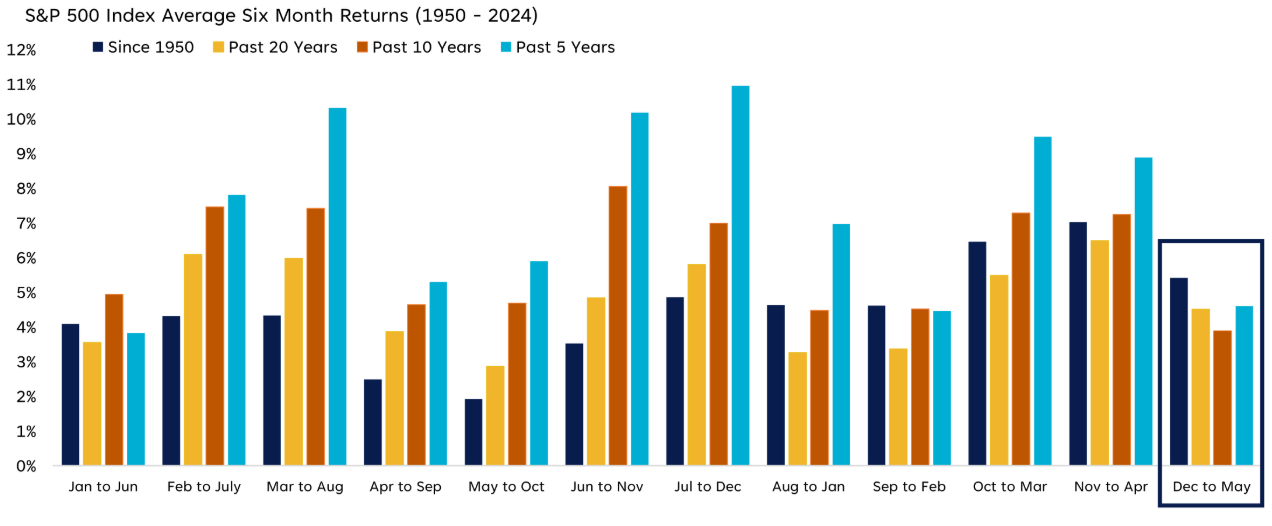

LPL: Is the Santa Claus Rally Still Coming to Town?

…The Santa Claus Rally Has Driven Solid December Gains Historically

…December to May Is One of the Weakest Six-Month Periods in Recent Years

…In summary, after a strong November, overall stock market seasonals are still supportive for stocks through year-end, but somewhat mixed after this period. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equity markets, with a preference for the U.S., a slight tilt toward large growth, and benchmark-like exposure across the rest of the market capitalization spectrum. We don’t rule out the possibility of short-term weakness, especially as geopolitical threats in Europe and the Middle East have the potential to escalate. Equities may also need to readjust to what may be a slower and shallower Federal Reserve rate-cutting cycle than markets are currently pricing in.

… finally, a few more words on JOLTS …

WolfST: Underlying Job Market Dynamics Begin to Retighten. The Fed Is Already Backpedaling on the Pace and Depth of Rate Cuts

Job openings and voluntary quits jumped by the most in over a year, layoffs and discharges plunged.