Good morning … a slow news day and charts are simply not inspiring me at the moment and so a shorter than normal note. First, how the day, yesterday started …

ZH: Trump Victory Sparks Renewed Optimism In Manufacturing Surveys

… clearly following along the data, well, there are Santa PAUSE implications … BUT this good news then was followed up by the ‘all-important’ and omnipotent comments from Gov Waller …

… All of that information will help me decide whether to cut or skip. As of today, I am leaning toward continuing the work we have started in returning monetary policy to a more neutral setting. Policy is still restrictive enough that an additional cut at our next meeting will not dramatically change the stance of monetary policy and allow ample scope to later slow the pace of rate cuts, if needed, to maintain progress toward our inflation target. That said, if the data we receive between today and the next meeting surprise in a way that suggests our forecasts of slowing inflation and a moderating but still-solid economy are wrong, then I will be supportive of holding the policy rate constant. I will be watching the incoming data closely over the next couple weeks to help me make my decision as to what path to take.

…

… But wait, there was more and this, from FRBNY Williams …

The target range for the federal funds rate currently stands at 4-1/2 to 4-3/4 percent. Monetary policy remains in restrictive territory to support the sustainable return of inflation to our 2 percent goal. I expect it will be appropriate to continue to move to a more neutral policy setting over time.

The path for policy will depend on the data. If we’ve learned anything over the past five years, it’s that the outlook remains highly uncertain. Our decisions on future policy actions will continue to be made on a meeting-by-meeting basis. And they will be based on the totality of the data, the evolution of the economic outlook, and the risks to achieving our dual mandate goals.

From what we know today, I expect real GDP growth to come in at about 2-1/2 percent for this year—or maybe a bit higher—reflecting solid supply-side growth. I anticipate the unemployment rate will run between 4 and 4-1/4 percent over coming months. And I expect inflation to be around 2-1/4 percent for the year as a whole. Looking ahead, I expect inflation to gradually come down to our 2 percent objective, although progress may be uneven at times.

…Treasury yields were mixed today with the short-end notably underperforming (2Y +5bps, 30Y unch). However, it was a very choppy day in bond-land with the PMIs marking the yield highs of the day (after French bond risk contagion spread)...

We note that late in the day, Fed's Waller said some marginally dovish shit which was utterly meaningless (we'll cut if data supports it... which we all know it doesn't) and 2Y yields tumbled...

… Finally finally, RIP Art Cashin (83)...

...you will be missed.

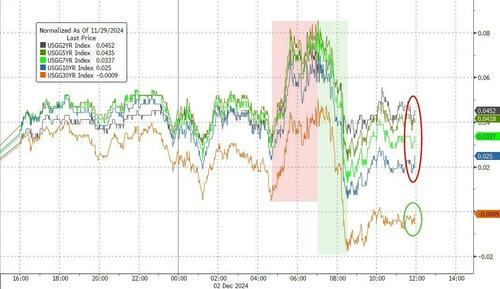

Indeed he will … one of those generational talents who defined many a career on Global Wall and while I never had the pleasure of meeting him in person, well, we’ll all join in celebrating his life, marinating a few ice cubes and raising a glass TO the man, the myth, the legend … RIP, indeed … here is a snapshot OF USTs as of 656a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US yield curve steepens and Dollar is broadly softer ahead of JOLTS and Fed speak, OATs await Wednesday's confidence vote … US yield curve steepens ahead of JOLTS, OATs await Wednesday's confidence vote … USTs are softer, weighed on by recent strong data which is lifting yields from the belly out. However, short-end debt is bid in the wake of Fed speak overnight with yields at the short-end pressured. Overnight, Waller said he is leaning towards a December cut, though noted one could argue the case for skipping and will be watching the data closely. USTs at the low-end of a 110-31+ to 111-06 band with the curve steeper.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … first up on some of the data points here in the USofA yesterday …

BARCAP: ISM manufacturing: Telltale signs of post-hurricane payback

The manufacturing ISM rose 1.9pts in November, returning to the upper-end of the range that has prevailed since late 2022. Details point to an unwinding of storm-related disruptions, which bodes well for payback in Friday's payroll report.

FirstTRUST: The ISM Manufacturing Index Increased to 48.4 in November

The ISM Manufacturing Index increased to 48.4 in November, beating the consensus expected 47.5. (Levels higher than 50 signal expansion; levels below 50 signal contraction.)

The major measures of activity were mostly higher in November. The new orders index increased to 50.4 from 47.1, while the production index rose to 46.8 from 46.2. The employment index increased to 48.1 from 44.4 in November, while the supplier deliveries index declined to 48.7 from 52.0.

The prices paid index declined to 50.3 in November from 54.8 in October.

… While the Fed believes they have room to continue cutting rates at the meetings ahead, there are serious risks that an overly aggressive path of cuts could bring with them a pickup in the M2 measure of money, and with it a return of inflation. In other news this morning, construction spending rose 0.4% in October, as a large increase in homebuilding was only partially offset by drops for commercial construction and highway & street projects.

ING: US manufacturing continues to struggle with tariff uncertainty

The US ISM manufacturing index improved in November, but remains in contraction territory. Election clarity probably saw some delayed orders getting pushed through, but the potential for tariffs and the associated risk of supply chain disruption and reciprocal tariffs placed on US exports means further gains will be limited until we have clarity

US and Chinese manufacturing purchasing managers' indices

Wells Fargo: Upside Surprise Still Leaves ISM Below 50

Summary A better-than-expected print for the ISM index still leaves manufacturing stuck in a rut, even if orders did crest above 50 for the first time since March. We revisit the ups and downs of Trump's first term to get a sense of the potential impact of coming tariffs.

Summary Inventory management is a trying job at the best of times, but rising tariffs make it even harder. Stocking up on whatever you need sounds easy, but at a time when inventory financing remains dear, that’s an expensive fix. The choice of the purchasing manager has big implications for GDP.

Yardeni: Manufacturing Indicators May Be Rebounding in US and China

After languishing for the past couple years, manufacturing gauges in both the US and China improved in November. Could this be the start of a rolling recovery for both countries' goods producers? We think so, though a tariff war would spoil the party quickly.

A revival in US goods production would likely boost bond yields as growth expectations increase. The 10-year Treasury yield could breach 4.5% by year-end in that scenario while the inflation-adjusted TIPS yield climbs above 2.0%, similar to where they traded before the Great Financial Crisis (chart).

… and on THE spread global asset managers are watching …

DB: OAT/Bund spread heading into uncharted territory

… Today's daily widening move in isolation, filtered through the beta (1yr regression up until EU elections) of OAT/Bund to average EGB spread ex OAT, was the biggest daily cheapening of OATs relative to its peers (Figure 2) this year, bigger than the daily moves seen last June. Of course, the reverse interpretation of this is that other EGBs are more resilient to the OAT move than they were last June/July, ie. less contagion (which is another point we made in last week's publication)…

… Outside of Europe, markets actually put in a decent performance yesterday, with the S&P 500 (+0.24%) moving up to yet another record high. One supportive factor was an upside surprise in the ISM manufacturing for November, which came in at 48.4 (vs. 47.5 expected). So even though it was still in contractionary territory, it was the strongest since June, and the new orders subcomponent (50.4) was in expansionary territory for the first time since March. That’s lifted up other growth estimates as well, with the Atlanta Fed’s GDPNow tracker for Q4 pointing to an annualised pace of +3.2%, which is its highest level to date.

That equity rally was led by further strength among big tech stocks, and the NASDAQ (+0.97%) and Magnificent 7 (+1.41%) moved up to record highs of their own. So it was a fairly narrow rally over the last 24 hours, and the equal-weighted S&P 500 actually saw a decent fall of -0.27%, moving off the all-time high it achieved last Friday.

In the meantime, US Treasury yields inched higher, with the 2yr yield up +2.9bps to 4.18%, whilst the 10yr yield rose +2.1bps to 4.19% (4.21% this morning). So that just about pushed the 2s10s curve back into inversion territory. The weakness on the 2yr might be pointing to a higher terminal rate, but investors yesterday priced in a greater chance of a rate cut this month. The chance of a cut closed at 76%, up 10pp from Friday, and the highest we have observed since US CPI data was released over 2 weeks ago. The uptick came after Fed Governor Waller spoke at the American Institute for Economic Research (AIER) Monetary Conference in Washington, D.C. last night. He said that “I am leaning toward continuing the work we have started in returning monetary policy to a more neutral setting,” signaling further cuts ahead, while adding that “an additional cut at our next meeting will not dramatically change the stance of monetary policy and allow ample scope to later slow the pace of rate cuts, if needed.” On the path of inflation he noted, “I believe the evidence is strong that policy continues to be significantly restrictive and that cutting again will only mean that we aren't pressing on the brake pedal quite as hard.” …

DB: Outlook in charts: Trump II: Growth too fast, inflation too furious for Fed cuts

…Trade policy uncertainty is once again on the rise

… a weekly observation worth a click …

FirstTrust: Monday Morning Outlook Inflation Distractions

It’s hard to keep track of all the theories about inflation. Remember policymakers and analysts blaming the surge in inflation in 2021-22 on supply-chain disruptions, too much government spending, and Putin invading Ukraine? Now some are saying that tariffs and deportations are going to cause a second surge in inflation…

…Immigration has surged since early 2021 and yet inflation has averaged 5.0% per year, the most in decades. If we can have high immigration and high inflation, we think the Fed can get to low inflation with low immigration, as well.

None of this is to argue that inflation hasn’t been a problem or won’t continue to be a problem in the years ahead. We think the bipartisan low inflation consensus that prevailed prior to the Great Recession and Financial Crisis of 2008-09 is dead and expect inflation will average 2.5% or more in the decade to come. But that’s because we think the Fed will conduct a looser monetary policy, not because of tariffs, government spending, deportations, supply-chains, or Putin.

…We expect the Fed to cut interest rates at the December and January meetings. Recent US PCE data was in line with expectations, and we view the increase in specific inflation subcomponents as noise, not signal. We continue to expect softer PCE inflation prints in November and December. The expected inflation deceleration reinforces our call for sequential Fed cuts. Meanwhile, growth remains robust: real GDP grew at 2.8% (quarterly, a.r.) in 3Q24, with solid real consumption spending growth at 3.5%…

The French government faces a vote of confidence tomorrow, with both the far right and the left pledging to vote against Prime Minister Barnier over the budget. A likely scenario would be Barnier continuing as a caretaker prime minister, and the 2024 budget being rolled over.

The euro weakened a little. As a current account surplus bloc, the euro’s value is determined by Eurozone investors’ willingness to invest overseas (the US dollar’s value is determined by foreign investors’ willingness to buy). Domestic investors understand political risk better than foreigners, so the euro should react but not overreact to politics. France is not Greece circa 2008; it is a wealthy country that can fund its deficit. France is not the US circa 2024; over the medium term, political structures make budget control easier.

US JOLTS data, recording externally advertised job vacancies, is due. The survey response rate is so low the numbers would not be published elsewhere. Recent variations in vacancies represented shifts between internal and external advertised positions. Vacancies may be in focus if US President-elect Trump pursues deportations that create labor market bottlenecks…

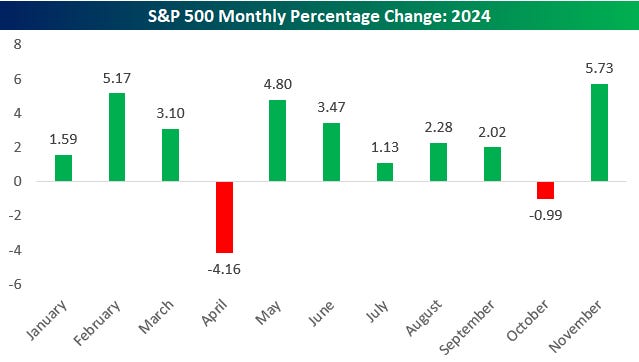

… The S&P 500 ended November with gains on eight of the final nine trading days of the month. The 5.73% gain for the S&P in November marked the best month of 2024 so far:

Moving on to December, below is the table we publish at the start of each month summarizing average monthly returns for the Dow Jones Industrial Average over the last 100, 50, and 20 years. While not the absolute best month of the year from a seasonal perspective, December is one of four months along with April, July, and November which has seen an average gain of more than 1% over all three time frames.

Today's Chart of the Day sent to subscribers includes the chart and table above plus a much more in-depth look at November market performance and December seasonality. One of the most interesting stats revolves around December performance when November and year-to-date returns have been very strong already during Election years.

… Bloomberg on those evil short-sellers of stocks …

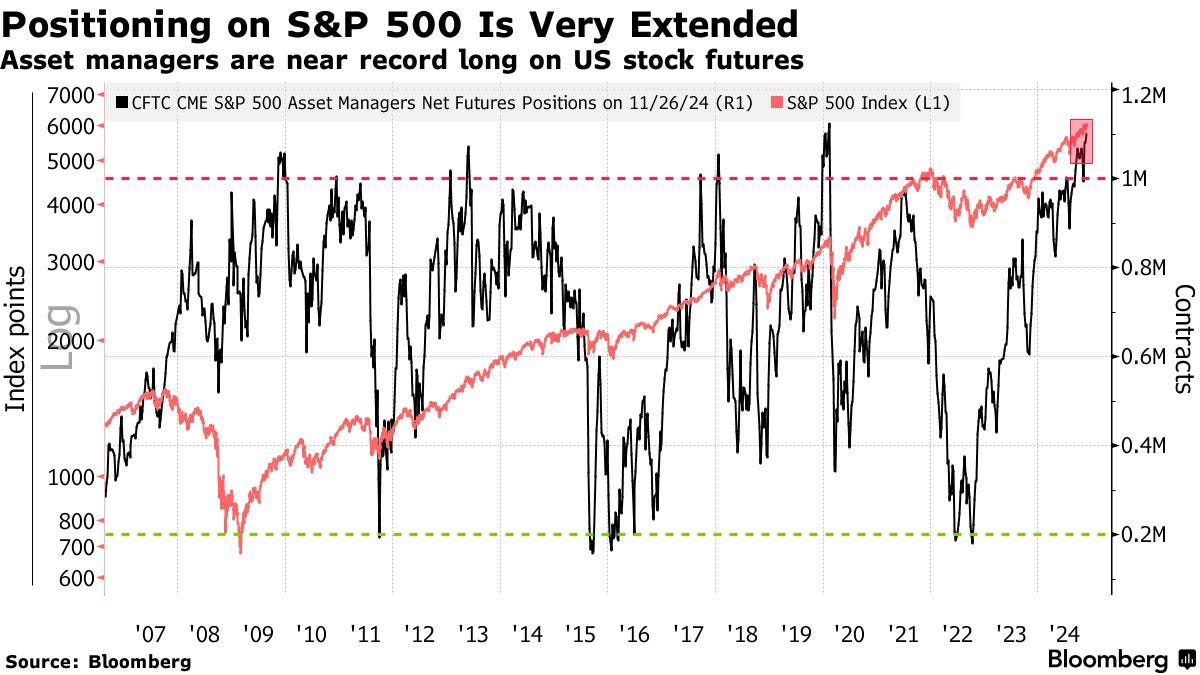

Bloomberg: Wall Street Short Sellers Throwing In the Towel, Citigroup Says

S&P 500 futures positioning ‘completely one-sided’: Citi

Gap widens with Europe, where sentiment remains bearish

… Investor positioning in S&P 500 futures is “completely one-sided,” the strategists led by Chris Montagu wrote in a note. It’s “setting new highs for a fourth consecutive week and increasingly the hold-out shorts are capitulating,” they said.

Appetite for US equities has shown no sign of abating this year. The S&P 500 made multiple record highs, surging 27%, powered by technology shares and a broad preference for US assets. The rally extended after the election of Donald Trump raised hopes of tax cuts and deregulation…

…AND for a MACRO perspective …

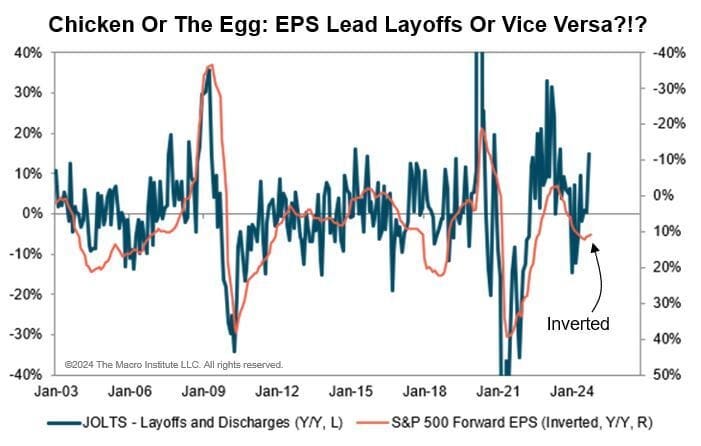

The Macro Institute: Macro Monday: Earnings Slowdown Setting Stage For Layoffs?

This is our favorite data week of the month with plenty of interesting releases. Monday brings the national Manufacturing PMIs (Markit and ISM), and the Services PMIs will be released Wednesday. The headline figures are always interesting, but in the current context, we will be most focused on the employment component. This is especially true since we get the December payrolls report on Friday. The report should have a "feel good" aspect given the weak (and distorted) numbers in October thanks to hurricanes and the dock workers' strike, so expect revisions to be substantial. At the end of the day, the headline numbers get all the attention, but they subsequently get revised, so they are hard to use on a real-time basis. Still, we are concerned about the recent slowdown in earnings, as it often brings about a fresh wave of layoffs, as the chart here illustrates. Keep a close eye on overtime hours, part-time vs full-time employment, and the number of jobs coming from government hires. All three of these data points will help explain what is really going with labor markets.