while WE slept: USTs mixed, 'hair' steeper on strong volumes; some (2y, 10y) levels to watch; reasons for econ resilience w/higher rates; could Fed HIKE?

Good morning … Meta vs Tesla. Tale of two behemoths and markets are being tested to see whatever they want to see. Not a stock jockey and I’ll leave that ‘debate’ to those far smarter than I but will offer it seems similar to the debate of whether or not good news is bad (or bad is good or good is good? no, wait, bad is bad?)

If pushed for a view of the facts we’ve received, well … you’ll have to see the very end of this mornings note. For now I’ll stick to things I know for sure I don’t know.

Global macro economics and bonds … to do this I’ll lean once again on ZH — sorry, not sorry — which noted …

… so, bad news then is GOOD (for Team Rate CUT) but then, rates didn’t go down … Perhaps we needed concession for 5s after all? Know what they say … ‘supply creates its own demand’ …

ZH: Subpar Record 5Y Auction Tails, Pushes Yields To Session Highs

… welp, throw THAT idea out the window, I suppose. Rates UP stocks down but all moves were in what I’d call a relatively calm fashion especially given some of the headlines rec’d earlier in the session

BN 04/24 12:50 Israel Said It Struck Around 40 Hezbollah Sites in South Lebanon BN 04/24 12:37 *ISRAEL STRIKES 40 HEZBOLLAH SITES IN SOUTH LEBANON

Israel Says Strikes 40 Hezbollah Sites in Southern Lebanon 2024-04-24 12:48:16.924 GMT By Alisa Odenheimer (Bloomberg) -- Israeli fighter jets and artillery struck about 40 Hezbollah sites in southern Lebanon, including storage facilities, weaponry and infrastructure used by the organization, the Israeli military says. * NOTE: Hezbollah is designated as a terrorist group by the US

To contact the reporter on this story: Alisa Odenheimer in Jerusalem at aodenheimer@bloomberg.net To contact the editors responsible for this story: Dana Khraiche at dkhraiche@bloomberg.net Sylvia Westall

… not sure I understand the NOTE … do we really need that explanation? Is someone, somewhere there with a Terminal worried ‘bout covering their behinds?? Think … HOPE … we all get the joke and know Hezbollah for whatever they are.

In any case, here is a look at 7yy to consider ahead of this afternoons liquidity event …

7yy DAILY: not gonna labor here too much other than to note 2024 UPtrend remains well defined and IN PLACE and this as momentum (stochastics) are overSOLD … could rates decline a bit … SURE. A test of the uptrend would be down nearer 4.40% …

… here is a snapshot OF USTs as of 736a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting a hair steeper around a little-changed intermediate sector. DXY is lower (-0.25%) while front WTI futures are little changed. Asian stocks saw strong moves lower in Japan and South Korea, Eu and UK share markets are mostly lower (SX5E -0.65%) while ES futures are showing -0.63% here at 6:45am. Our overnight US rates flows saw modest selling of intermediates from fast$ names in an otherwise sleepy session. During London's AM hours, activity was muted amid ranges with clients nosing around in search of cheap expressions to be long intermediates on 'fly. Our dip-buying in cash has dialed down of late with the desk thinking that supply has been satisfying that demand this week. Overnight Treasury volume was decent at ~120% of average with 5's (180%) and 30yrs (150%) seeing some relatively elevated average turnover overnight…

… Our next attachment zooms out to the monthly chart of 30yrs to show how the ~4.80% local support level was also roughly the range highs for bonds back in 2008-2011. Above that, we'd spot next major support near 5.29% should 4.80% give way Friday, or any other time.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: NQ dragged lower by Meta (-13%) post-earnings, DXY softer & Antipodeans benefit from metals prices … Bonds are rangebound awaiting impetus from Tier 1 data later today … USTs are in consolidation mode below the 108 mark as traders brace for today and tomorrow's tier 1 US data. For today's quarterly PCE data, ING notes that a 0.4% MoM reading tomorrow could see Fed easing expectations cut back to just 25bp. Currently USTs remain contained within yesterday's 107.20-108.02.

Strength in April tax revenues may see Treasury lower borrowing estimates over the next two quarters, requiring less T-bill issuance in the near-term.

The first regular buyback operation will be announced at the May refunding, with separate liquidity support and cash management components.

We expect Treasury to pause nominal coupon and FRN auction size increases at the May refunding, but do not rule out further increases over the medium-term. We anticipate another gradual TIPS increase.

Amidst a week of light data calendars and easing geopolitical risk we have positioned for a potential reversion of US equities and USD to fair values by adding tactical long S&P 500 and long GBPUSD. See Quant Trades of the Week: long SPX, GBPUSD and EURCNH, short US airlines, dated 22 April.

Our models indicate that fair values of both the S&P 500 and GBPUSD have risen, suggesting there could be further room for further increases. Both trade ideas are in the money and we are raising our targets. For long S&P 500 we raise target to 5184.9. For long GBPUSD we raise it to 1.2552.

We also tighten the stop-losses close to entry. We are revising our stop loss levels to 4990 for long S&P 500 and at entry (1.2338) for long GBPUSD. We also raise stop loss for our long EURCNH trade to slightly above entry (7.722) given that it has also moved towards its MarFA™ fair value.

CitiFX: US yields: Treading water (best in biz right here…imo)

US 2y yields We retain our slight bias for a break higher in 2y yields:

We have seen multiple tests of 4.99-5.00% resistance (76.4% Fibonacci, psychological level).

No signs of a turn yet in momentum (weekly slow stochastics)

We are biased for a break higher in 2y yields, though we think we will find strong resistance at 5.08% (November 2023 highs)

There is no strong support till the 4.77% level (December 2023 high)

US 10y yields While we expect slightly higher yields from here (and a re-test of the resistance), the key difference is that we expect the strong resistance at 4.69%-4.73% to hold.

4.69%-4.73% (76.4% Fibonacci, November 13 high, psychological level) is the key resistance band, which we tested in mid April.

No signs of a turn yet in momentum (weekly slow stochastics).

Near term support at 4.49% (April 19 low).

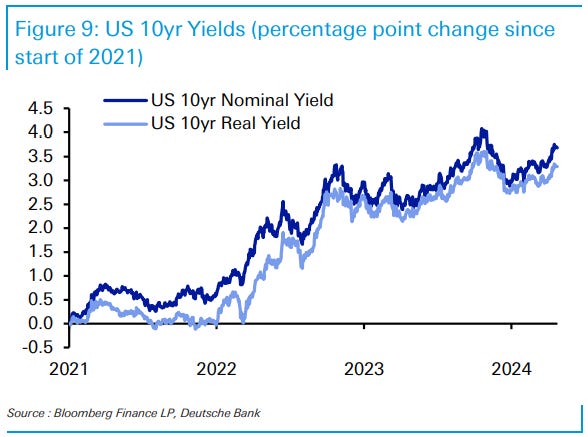

DB: 5 reasons for the economy's resilience to higher rates

Over the last couple of years, we’ve seen one of the most aggressive series of rate hikes since the early 1980s. The Fed hiked rates by 525bps, the ECB hiked by 450bps, and the Bank of Japan ended its negative interest rate policy.

But despite many fears, the global economy held up remarkably well in the circumstances, particularly given the concern that even modest hikes would have a significant impact. It’s true there have been episodes of turmoil, particularly around SVB’s collapse last year. But those have proven contained so far.

This economic resilience has led to suggestions that higher rates could even be stimulating the economy, and that the traditional channels no longer apply. For instance, savers are earning significantly more interest income that they’re now able to spend. But we don’t think that’s the case overall. Instead, a few unique features of this cycle have dampened the usual impact of rate hikes, such as supportive fiscal policy, as well as the strong supply-side recovery after the pandemic.

… 1. Although rate hikes have worked to reduce demand, the supply-side of the economy recovered strongly at the same time.

2. With lots of fixed-rate debt, the effects of tighter monetary policy are taking time to work through the economy.

3. Although monetary policy has been tightening, fiscal policy has become more supportive.

4. Investors have repeatedly expected rate cuts to occur soon, which has meant long-end yields have not risen as significantly.

5. The rise in real yields has been more subdued than the rise in nominal yields.

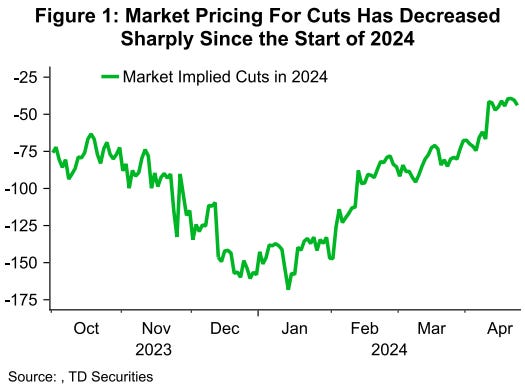

Recent strength in US inflation and growth data has sharply lowered the market's pricing for cuts this year, with investors now penciling in just 44bp of cuts in 2024 compared with 160bp at the start of the year (Fig 1).

Worries of sticky inflation have also fanned worries of a potential rate hike as investors question the Fed's ability to slow inflation. Options market pricing currently puts the odds of one or more hikes this year at 12% — up from 4% just before the March CPI report but down from a peak of 20% (Fig 2). Note that open interest in tail risk options tends to be thin, possibly skewing the pricing for hikes.

We see a greater probability that the Fed keeps rates on hold in the event that inflation and growth surprise to the upside. In fact, it would likely take a fullblown re-acceleration in inflation data and the risk of inflation expectations becoming unanchored for the Fed to tighten again. This is far from our base case expectation for two cuts this year, starting in September.

Market pricing has largely followed recent upside surprises in economic data, which have moved higher across the board (Fig 3). This leaves markets vulnerable to a correction lower in rates if data begins to miss these heightened expectations. We also believe market pricing for the terminal funds rate is much too high at 4%, leaving Treasuries looking attractive (Fig 4).

The US releases its first guess at first quarter GDP (a generally accurate number should be available sometime around 2029 or 2030). The rapid pace of structural change means that increasing amounts of economic activity are likely being missed in this sort of data. Overall, there should be some signs of a slowdown, but middle-income consumers will still provide resilience.

There are two practical considerations with the US GDP numbers. In an election year, it is important to remember that normal people do not care about abstract concepts like GDP. National economic wellbeing is judged (or misjudged) through a biased perspective of personal economic circumstances. There is also uncertainty about the trend rate of growth of the US—the Federal Reserve’s 1.8% guess is probably too low. Immigration and productivity gains from things like flexible working have likely raised the sustainable growth rate.

Wells Fargo: Durable Goods Orders Continue to Reflect Hesitant Demand

Summary There was little surprise in the March durables release. Aircraft-related volatility boosted orders, and the underlying details suggest a continued hesitancy in demand. Shipments data remained weak and present some downside to Q1 real GDP growth—out tomorrow.

Wells Fargo: Worst of Both Worlds: Are the Risks of Stagflation Elevated?

Part II: A Brief Review of Past Episodes of Stagflation Summary

In the first installment of this series, we presented a simple framework to characterize stagflation and identified 13 instances in the United States since 1950.

Episodes vary in severity, but each posed unique challenges to monetary policymakers. In this second report, we briefly review historical instances of stagflation and their accompanying monetary policy decisions.

Six of the 13 episodes of stagflation occurred in the 1970s as oil price shocks, imbalanced fiscal and monetary policy and robust labor cost growth placed upward pressure on prices and weighed on output growth.

The episodes outside the 1970s have ranged from mild to moderate, with the exception of the post-COVID pandemic occurrence, a topic that we will turn to in the final installment of this three-report series.

Over time, historical instances of stagflation have often been met with accommodative monetary policy to support employment, despite elevated price growth.

The degree to which the accommodative policy stance exacerbated stagflation depends on the drivers of the inflationary bouts themselves and whether the economy's structure would help entrench or dilute price momentum.

External factors, such as oil price shocks, were associated with severe episodes of stagflation, but expansionary fiscal policy enacted amid a tight labor market also played a role. Those dynamics mirror the current environment, as the unemployment rate is at a decades' low and the fiscal deficit is swelling. Will the economy suffer from stagflation in the near term?

… And from Global Wall Street inbox TO the WWW,

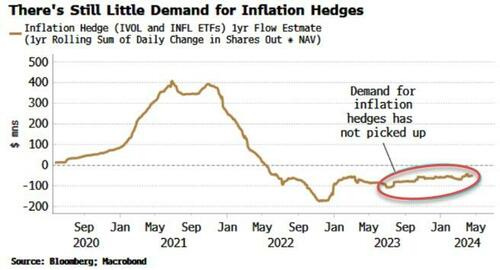

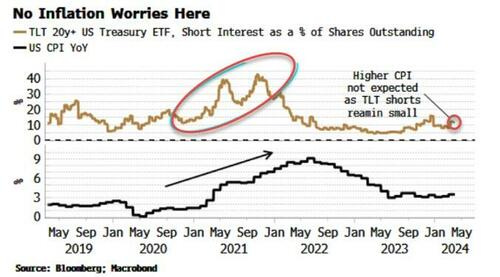

Bloomberg(via ZH): Market Is Splendidly Indifferent To Rising Inflation Risks

… Yields have been rising, and so have gold and silver, but there is a distinct lack of the inflation urgency seen in 2021 and early 2022, when CPI was hitting decade highs and the Federal Reserve had not yet responded with interest rate hikes.

As one sign of the relative complacency, take two ETFs that are designed to hedge inflation, INFL and IVOL.

These saw marked inflows in 2021, but the flows have been muted since the Fed started raising rates in 2022 and have remained so.

There have also been no marked pick-up in flows to ETFs of inflation-linked bonds, such as the TIP ETF.

Similarly shorting interest in Treasuries continues to be minimal. JPMorgan’s Client Treasury Survey is registering a near series-low of outright shorts, while short interest in the TLT long-term UST ETF is low and has barely risen.

There are no inflation alarms ringing. But that could prove to be misguided as inflation shows clear signs of resurfacing.

This is even more so as the structural backdrop, with increasingly coordinated fiscal and monetary policy, is conducive to a secular rise in price growth.

Biden's 44.6 Percent Capital Gains Tax a 100-Year High

https://www.newsmax.com/politics/biden-capital-gains-taxes/2024/04/24/id/1162315/