while WE slept: USTs marginally lower/flat ahead of PCE and month-end; tariffs sharing centre COURT w/month-end, some bond techs, NFP pre-caps and more...

Good morning and my apologies for the radio silence YESTERDAY … woke up 430a as we do every mornin’ nowadays and found out we were without internet — was like time traveling back to 1994 only with worse buffering … MOST didn’t mind (as they were leaving) while couple of us having to work from home, well, it was less funTERtaining.

What did I miss … a picture to begin …

30yy DAILY: 5.20%, 4.93, 4.85 …

… with those levels noted and in mind in to and ahead of today’s 4p month-end extension / duration grab, I’d note momentum (stochastics) are becoming overBOUGHT but not yet at previously overBOUGHT levels which, in hindsight, was a good level to ‘put some hay in the barn’ … perhaps another few days?

… Wait, no, don’t answer that … tariffs ON, tariffs off, then back ON again … throw in some weak data and a bond bid, right …

In less than a week we've had a 1-week forward 50% tariff imposed on the EU, the same tariff delayed by 5 weeks, the US Court of International Trade rule that a large swathe of the US Administration's tariffs are illegal, the Court of Appeal yesterday granting a temporary stay that leaves the tariffs in force while it considers the case, as well as news that the Administration will turn to alternative powers if they lose their court appeal. It really is hard to keep up. Trading and analysing this market successfully requires a lot of luck. Unless of course I get it right and then its skill…

… AND …

ZH: Bonds & Bullion Bid As Tech, Tariffs, & Troubling-Data Spark Pump'n'Dump In Stocks & The Dollar

… sure … of course I missed all the fun … what ELSE could possibly happen … wait, no, don’t tell me … DJT and JPOW hugged it out …

ZH: For First Time Since 2019, Trump Invites Powell To White House To Discuss Economy

… oh come ON already!!

Well … what can I do. I missed it all and I had many great plans and whitty insights to pass along yesterday.

Nah, just kiddin’ … I had nuthin’ — same ‘ole same ‘ole and just get over it and move along.

I’ll edit / update Global Wall (below) with date stamps as needed … for now, I’ll jump in and ask if you happened to … #Got7s …

ZH: Stellar 7Y Auction Sees Highest Stop Through Since 2022, Record Low Dealers

… stellar? Man, what a day and auction which DID in fact go as well as 5yr …

ZH: Record Foreign Demand For Blowout 5Y Treasury Auction

… are we good now with regards to questioning WHERE foreign buyers went? See below for more from one shop who says …

NatWEST: Foreign demand for Treasuries: Still in place …

… in other words, FUNDING SECURED!

… ok fine, but … note to self, those folks had to bid on 5s 1hr before the FOMC minutes came out …

ZH: FOMC Minutes Show Fearful Fed Taking "Cautious Approach" Before Plunge In Uncertainty

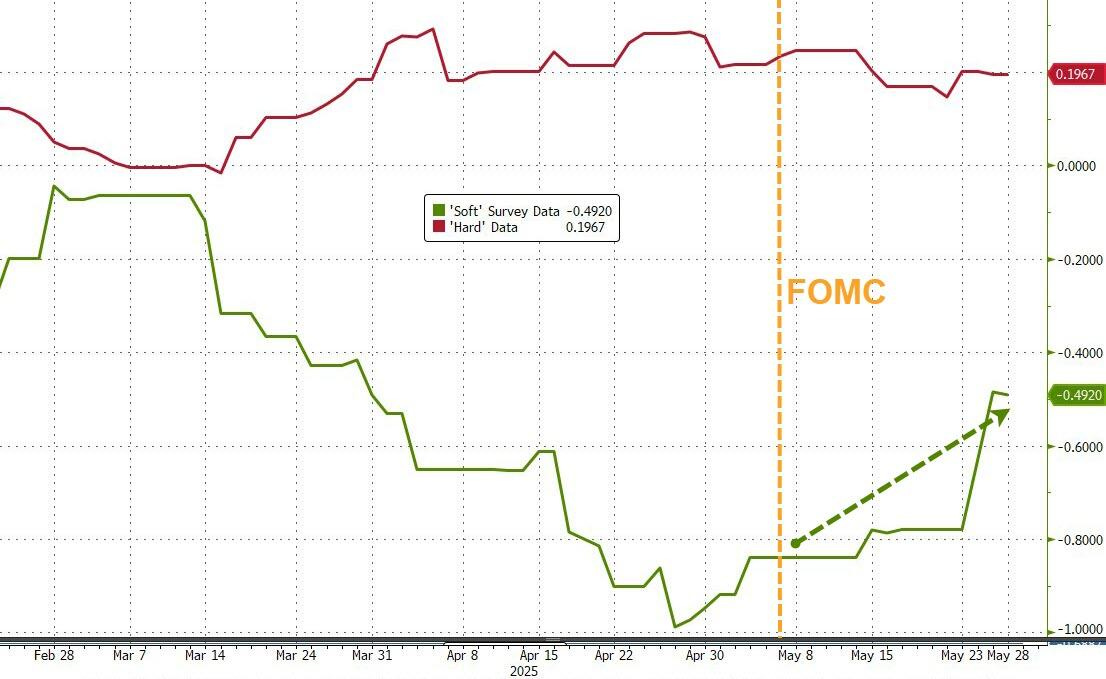

… Hard data continues to be steady and growing while 'soft' survey data has surged in the three weeks since the last Fed meeting...

Source: Bloomberg

Which has pushed rate-cut expectations lower overall (with cuts shifting from 2025 to 2026)...

… and from the buying panic of the other day, to …

ZH: China Chip Ban & 'Soft' Data Surge Sparks 'Sell All The Things' Day

… here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures in the red & USD gains ahead of PCE and Fed speak … USTs marginally lower/flat, two-way EGB action on prelim. inflation prints ahead of Germany's figure and US PCE … USTs are contained. Newsflow this morning has been virtually non-existent for USTs as we continue to digest the court-related trade updates and confirmation that Liberation Day measures will remain in place during the appeals process; timeline remains unknown. In a 110-19 to 110-25 band. A marginal new high for the week with USTs holding onto the gains that began mid-day on Thursday and then continued into the evening as the initial court-related pressure abated with the administration sticking to its plans. Focus now turns to US PCE (Apr).

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … (date stamped best I can with stuff I may have missed) …

Courts vs DJT (again …), a look at global MACRO and at the FOMC minutes …

29 May 2025 Barclays: Court vacates IEEPA tariffs, but the President still has cards to play

The US Court for International Trade vacated the fentanyl and reciprocal tariffs. Sectoral tariffs on steel, aluminum, and autos are not affected. The DOJ plans to appeal. The Supreme Court may ultimately have the final say. President Trump has other legal authorities for tariffs at his disposal.

What now, after the Manhattan trade court struck down both reciprocal and fentanyl tariffs? We provide a few immediate thoughts, some of which might change as more details of the ruling become clear…

As expected, May's minutes reiterated that the FOMC is in no rush to adjust rates as it awaits clarity about government policies and their effects. Adverse risks to both sides of the mandate underscore the lack of urgency. Initial framework discussions seem to signal FAIT's demise.

The minutes of the May FOMC meeting reaffirm that participants are in no rush to adjust policy rates amid elevated uncertainty about policies put in the place by the Trump administration and how they will affect the path of the inflation and the labor market .

Participants continued to view the current monetary policy as moderately restrictive and the economy as growing at a solid pace, with labor market conditions broadly balanced and inflation somewhat elevated. However, they viewed uncertainty as high, with intensified downside risks to employment and economic growth, and upside risks to inflation.

The minutes, which refer to the meeting timed in the week prior to the recent deescalation of US-China trade tensions, prominently highlighted the policy dilemma perceived by the FOMC. On one hand, participants were concerned about fallout on activity and employment from the unexpectedly high tariffs could portend a economic weakness. On the other, they went out of their way to highlight the potential for more persistent inflationary pressures through various channels.

As part of the ongoing monetary policy framework review, participants discussed the merits of flexible average inflation targeting (FAIT), according to which the FOMC seeks to make up for spells of persistently below-target inflation to achieve an average of 2%. The discussion concluded that, even though FAIT was suited to the pre-pandemic environment, it had "diminished benefits" in face of substantial risks of large inflationary shocks or when risks of hitting the effective lower bound are less prominent. The minutes suggest that the FAIT strategy is likely to be discarded in favor of the prior flexible inflation targeting (FIT) strategy, in which the committee no longer seeks to make up for past deviations from the target. As we noted in March, language that directs the FOMC to focus asymmetrically upon "shortfalls" — rather than "deviations" —from maximum employment is also on the deathwatch.

We retain our baseline call of one 25bp rate cuts this year, in December, in the face of tariff-led slowing in economic growth, slightly higher unemployment rate and rising inflation. We then expect the FOMC to cut rates three times in 2026, placing the policy rate at what it regards as a slightly restrictive level by year-end. We view the rate path as unusually uncertain, amid elevated uncertainty about other policies…

The revised GDP growth estimate was little changed from the advance release, showing a 0.2% q/q saar decline. Although we remain skeptical that GDP declined in Q1, details highlight slowing, including sizeable downward revisions to consumer spending and a weak incoming GDI estimate.

Available indicators suggest that nonfarm payroll employment will continue to post solid gains in May, with the headline moderating from +177k to +150k. We think that the unemployment rate likely held steady at 4.2% and that hourly earnings will post a trend-like increase of 0.2% m/m.

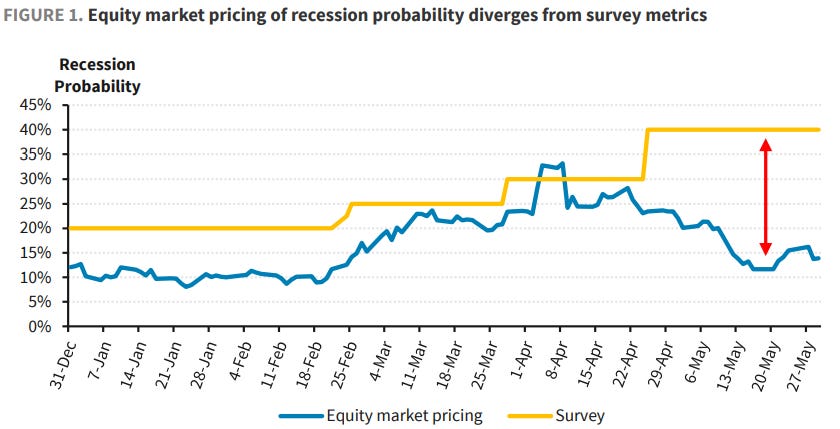

Equity market pricing of a recession has diminished greatly even as survey forecasts continue to rise. Equities could be getting complacent at these valuations considering EPS estimate cuts, high rates, rising jobless claims, and ongoing tariff uncertainties.

Falling rates volatility and AI earnings strength have brought calm back to the equity market. But fatigue is evident, with Trump's tariffs in limbo. Proposed Section 899 on unfair foreign taxes adds a layer of uncertainty for EU exporters to US, and could also impact capital flows.

… Best in show on weak data, UST BID and as day settled out …

May 29, 2025 BMO: Q1 Personal Consumption Revised Down to 1.2%; IJC Jump to 240k; UST Rally

Q1 GDP was revised up to -0.2% vs. -0.3% expected and -0.3% prior (for context, this is the second Q1 estimate from the BEA). While headline growth was a touch better than previously assumed, the economy still contracted in Q1 for the first time since the beginning of 2022. More relevant to the trajectory of aggregate demand and path of Fed policy, Personal Consumption was revised down by 0.6 ppt to 1.2% compared to expectations for a 0.1 ppt downward revision to 1.7%. This is the lowest since 2Q23. The GDP Price Index was unchanged at 3.7%, as-expected. Q1 Core PCE was unexpectedly revised down to 3.4% versus the 3.5% consensus. On the employment side, Initial Jobless Claims jumped to a four-week high 240k in the week of May 24, exceeding all estimates in the Bloomberg survey and topping the 230k consensus by 10k. The prior week’s 227k was revised to 226k. Continuing Claims climbed to 1919k vs. 1893k anticipated and 1893k prior (revised from 1903k). This is the highest print since November 2021.

Shortly before the data, the bulk of the overnight selloff had been erased and 10-year yields headed into 8:30am EST at 4.49%…

The Treasury market rallied on Thursday as the Court of International Trade ruled against the legality of the President’s Liberation Day ‘reciprocal’ tariffs. The ruling also shot down the 20% levies on Canada, China, and Mexico related to the US fentanyl crisis. Later in the day, a federal appeals court temporarily paused the initial block imposed by Wednesday’s ruling, while it considers a longer-lasting stay. The Administration has already signaled it has other ways of applying the tariffs from a legal perspective. In the event that Trump attempts to find an alternative path to applying tariffs, the obvious question then becomes if it will face the same legal challenges and fail. We’ve long maintained that there is a key divergence in the pace of Trump’s policy changes and how quickly the legal system can respond. Trump is moving at the speed of social media while the courts are moving at… well, court speed. Until this ruling, the market had nothing concrete to point toward that suggested Trump had overreached the authority of his office.

The most relevant takeaway is that trade war uncertainty will be a key facet in the US rates market for the foreseeable future. This uncertainty is unfortunate for business leaders as it muddies the outlook all the more and does nothing to answer the questions of when to build? Where to build? Who to hire? Who to fire? In short, while the shifting policy landscape might, eventually, revert back to a rough approximation of what was previously in place, it will take even longer for the dust to settle. It’s notable that there was a separate ruling against Trump’s tariffs on Thursday related to small businesses – although the market response was muted as the tone had already been set.

We’re onboard with the rally and anticipate lower yields as the weekend approaches …

France on Japan AND global TACTICAL asset allocation, jobs and … things …

29 May 2025 BNP: Global Tactical Asset Allocation Chartbook

Our updated tactical asset allocation reflects our view that though policy uncertainty is easing, global scarring will persist via weakened confidence and supply chain frictions. The US economy is slowing but will likely avoid a recession.

We see fiscal spending supporting the eurozone recovery into 2026, despite tariff challenges. Strong momentum and relaxed valuations leave us overweight European assets, with the EUR set to benefit from capital repatriation.

Our selective duration strategy favours dips in US and UK duration while perceiving downside risk for German Bunds as eurozone swap curves steepen.

Elevated positioning, rich valuations and slowing growth suggest USD weakness. We like the BRL for FX carry trades.

Oil faces downside risks, while we remain constructive on gas and gold over industrial metals and copper in particular.

We estimate a 125k increase in nonfarm payrolls and a steady unemployment rate in May.

Household views of the US job market have been softening, but we put more emphasis on the hard data and business confidence in gauging risks.

We see a high bar to the print altering Fed officials’ policy views as substantial uncertainty remains about how court challenges to tariffs play out, as well as the still-evolving contours of a tax bill.

28 May 2025 BNP: Japan: Answers to FAQs on long-end JGBs

As the JGB curve bear-steepened after the big tailed 20y auction last week, we received many inquiries about the long end of the curve. Here are our answers to frequently asked questions on long-end JGBs.

What has happening to long-end JGBs this week? On Tuesday, some media reported that the Ministry of Finance distributed a questionnaire to market participants, asking for their views on issuance and the current market situation. This raised expectations for a reduction in the issuance of 10y+ bonds, leading to significant bull-flattening. Although there was a weak 40y auction result on Wednesday and yields rose, the market reaction was not as large as that following the 20y auction last week (see Sunday Tea with BNPP: Fiscal comes first, dated 25 May 2025) . While we anticipate some volatility in the 10y and longer sectors, the movement is unlikely to be one way, in our view. We have initiated long 10y10y trade idea as a tactical trade (see JPY rates: Flattener crash – outright better risk than curve, dated 22 May 2025)…

…Will the Japanese investors rotate out of FX-hedged foreign bonds back to JGBs? This could happen in theory. However, lifers’ investment plans suggest a reduction in JGB holdings (see Japan: Lifers investment plan in FY2025, dated 28 April 2025). The holdings of FX-hedged foreign sovereign bonds are smaller compared to the past. In 2022, there were significant sales of foreign bonds, according to the MoF’s international transaction data (Fig. 5). This is because an accounting rule affecting lifers’ core profits and losses has changed since FY2023. Lifers used to include the coupon income from FX-hedged foreign bonds to the core profit while charging FX-hedging costs to other profit and loss category before FY2023, but from FY2023 they need to include FX-hedging costs in their core profits. Hence, holdings of FX-hedged foreign bonds were significantly reduced. Recently, lifers’ FX-hedged foreign bonds investments have focused on credit bonds. The yield of FX-hedged USD BBB credit bonds is about 100bp higher than that of the 20y JGBs (Fig. 6).

Interrupting regularly scheduled programming here / now for some techs from one of, if not THE very best in the technicals biz …

We have posted 'outside reversal' candlesticks in daily US treasury yield charts, which suggest we could see a short term move lower. The medium term picture, however, suggests we could stay at these high levels after markets broke past key levels last week.

US 2y yields US 2y yields have posted a clear 'outside day' candlestick on Thursday off resistance at 4.07-4.08% (Dec 2024 low, March 2025 high). This points to short term downside for US 2y yields.

Resistance for US 2y yields remains very strong as well, adding to the building blocks. Above the 4.07-4.08% range, we see 55w MA at 4.16% as well. On the other hand, we see short term support at 3.89% (55d MA), and no strong support after that till the 200w MA at 3.60%.

Overall, we expect the bias for 2y yields to remain for a move lower.

…US 30y yields Similarly, the break above the key 5% level in US 30y yields represents a significant break of levels, with a 'higher high' set. We see the next resistance only at 5.18% (2023 high), which held in the move last week.

Even though we posted an outside day candlestick, we don't expect significant downside, with support at 4.76% (55d MA). We think 30y yields will hold in this 4.78-5.18% range in the interim, and wait for further technical building blocks to add to the picture.

Germany wishin’ upon the stars (for some clarity) … and a couple / few other items of interest …

28 May 2025 DB: Star light, star bright, which u-star will the Fed see tonight?

The anticipated adverse tariff supply shock is expected to create tension between the Fed’s dual-mandate objectives of stable prices and maximum sustainable employment. When its mandates are in tension, the Fed considers the distance from targets and the time horizons over which those gaps are likely to persist when determining which side needs more attention. While the Fed’s 2% PCE inflation target is clear, its full employment target is less well defined.

In this piece, we update analysis deriving estimates of u-star from a variety of labor market slack indicators. While our alternative estimates vary widely, from roughly 3.5% to about 6%, the distribution is currently centered on 4.6%, somewhat higher than the Fed’s median long-run unemployment forecast of 4.2%.

A higher u-star would suggest that the Fed should accept some weakening in the labor market before needing to cut rates, particularly in the presence of elevated inflation. This supports our view that the first cut will come only at the December meeting. That being said, the speed of the deterioration matters given the labor market’s non-linear dynamics (e.g., the Sahm rule). A faster-than-expected deterioration would likely warrant a faster dovish pivot.

29 May 2025 DB: Separating the wheat from the chaff

The long end of bond curves has come under pressure in most G10 countries, with the US and Japan being notable underperformers. However, there are important differences between these two markets.

Today's charts present evidence that there are greater dislocations in JGBs than in USTs, especially at the long end of the curve. This suggests that the long-end JGB sell-off is more likely to be technically driven.

On the other hand, the long-end UST sell-off is more likely to be fundamentally driven. Indeed, as we have documented in our work on twin deficits, the external position tends to be a better predictor of sovereign risk than the fiscal position. While Japan has a very high government debt-to-GDP ratio, its external position is very robust. In contrast, the US has a lower debt-to-GDP ratio but a very weak external position, which is unlikely to improve absent a material fiscal tightening. Thus, the pressure on the long end of the UST curve is likely fundamentally driven, as current policies are eroding the USD's "exorbitant privilege" and leading non-domestic investors to require a higher risk premium to hold US assets.

Different drivers require different remedies. A "technical" solution could reduce the pressure on long-dated JGBs, but a more "fundamental" solution (i.e., a reduction in fiscal deficits) is likely to be necessary to materially reduce the pressure on long-dated USTs.

29 May 2025 DB: Liberation from Liberation Day tariffs?

Overnight, the US Court of International Trade (CIT) struck down tariffs implemented by the Trump administration under the International Emergency Economic Powers Act of 1977 (IEEPA). In this short note, we discuss what happened, what comes next, and initial views on what impact it could have on the economic outlook.

Netherlands on … Courts vs DJT (again …)

29 May 2025 ING: How Trump might bypass US courts to continue his tariff agenda

A US court ruled that President Donald Trump exceeded his authority using the 1977 International Emergency Economic Powers Act (IEEPA) to impose tariffs. Directly affected by this ruling are the 10-30% tariffs on China, Canada, Mexico, and the rest of the world. The sectoral tariffs on steel, aluminium, and automotive, however, remain

Tracking immigration …

May 30, 2025 MSU.S. Economics: Immigration tracker: Low immigration makes it hard to push the unemployment rate higher

We update our tracking estimates for immigration based on data through April. We revise lower our outlook for immigration, population growth, the size of the labor force, the breakeven employment rate, and potential growth. Low immigration makes it hard to push the unemployment rate higher.

Key takeaways

We revise lower our outlook for immigration this year to 800,000, down from 1mn previously. We retain our forecast for immigration inflows of 500,000 next year.

We revise our breakeven employment rate lower to 90,000 and 80,000 this year and next. The labor market can stay tight even as employment growth slows.

Less immigration slows hours worked. We estimate potential growth fell from 2.5-2.7% in 2022-23 to 2.1% currently. We expect it to fall to 1.5% in 2026.

Firming inflation and tight labor market underpin our view the Fed does not cut until March 2026. Fed cuts should be backloaded.

Our terminal rate of 2.50-2.75% in 2026 is based on: 1) a Fed that cuts late cuts more, and 2) lower potential growth pulls the neutral rate down.

A(nother) recap of recent FOMC meeting minutes from across the pond AND couple other items equally as funTERtaining …

29 May 2025 NatWEST: Foreign demand for Treasuries: Still in place

One of the main narratives in markets post-Liberation Day has been that foreign and international investors are migrating away from US assets due to the negative growth / inflation implications of US trade policy, coupled with the deficit impact of currently proposed fiscal policy. This idea has translated to rumblings of a “Sell America” theme, whereby shaken investor confidence in US Treasuries and the dollar as haven assets may be prompting a shift to alternatives.

We do subscribe to parts of this narrative, albeit selectively and likely over a longer time horizon. In the immediate term, we think that domestic and foreign investors are demanding higher yields on longer dated Treasuries to compensate for increased issuance with higher odds of a “soft default” (debt not repaid in real terms) – this risk is underpinned by higher expected inflation due to tariffs and a Fed that is deemed to be biased to their growth mandate above their inflation mandate. These factors have pushed up the Treasury term premium and have pressured the curve to bear steepen.

However, the idea that foreign investors are shunning US assets, and especially US Treasuries, is not yet supported by the data. Indeed, global sovereign debt curves are bear steepening elsewhere, one sign that duration needs are not simply being moved to another market as other regions face their own set of challenges.

In this piece we share charts of the limited hard data expressing foreign demand as well as shifts in domestic demand. For now, both look to be in place, with the latter more impacted by volatility, dealer balance sheet constraints, and asset class rebalancing. We expect any structural shifts will be drawn out over time and thus will be monitoring these indicators through the year…

29 May 2025 NatWEST: Trump Tariff Ruling - Quick Take

The US international trade court ruled that Trump tariffs justified under the IEEPA overreach the President’s authority under the law. This ruling temporarily invalidates the reciprocal tariff regime, the 10% universal minimum tariff, and Trump’s border security tariffs on Canada, Mexico and China. The administration will appeal and could earn a stay that would allow tariffs to remain in place.

This is an important ruling, but one markets shouldn’t overstate as the end of global trade disputes. Trump’s trade policy toolkit has several other options, some tested and others untested, to assert tariff authority. Those other options often include more bureaucratic legwork that take time to implement. If this ruling holds, one practical implication could be that Trump’s ability to rapidly adjust tariffs in many cases would be curtailed, at least in the near-term.

For markets, this if this ruling stands it could force Trump trade policy into a more methodical, predictable stance, which could further push back US recession tail risk and reduce questions around US economic and USD exceptionalism. But there’s only so far that optimism should go – this ruling doesn’t eliminate trade policy risk entirely and won’t immediately bring back policy certainty. Trump has plenty of other options to enact tariffs.

As a side consequence of this ruling, the Trump tax bill rapidly working its way through Congress may face new challenges. Republicans are relying on tariff revenue to help offset the cost of extending and expanding tax cuts, so the prospect of tariffs being rescinded or removed could deepen internal Republican strife over deficit expansion.

28 May 2025 NatWEST: US: Recap of minutes from May 6-7 FOMC meeting

This afternoon’s minutes from the May 6-7 FOMC meeting underscored the committee’s “wait-and-see” stance on monetary policy. The minutes noted that “In considering the outlook for monetary policy, participants agreed that with economic growth and the labor market still solid and current monetary policy moderately restrictive, the Committee was well positioned to wait for more clarity on the outlooks for inflation and economic activity. Participants agreed that uncertainty about the economic outlook had increased further, making it appropriate to take a cautious approach until the net economic effects of the array of changes to government policies become clearer."

The tone of the minutes matched that of chair Powell at his May 7th press conference when he said, “I don’t think we can say, you know, which way this will shake out. I think there’s a great deal of uncertainty about, for example, where tariff policies are going to, to settle out and also, when they do settle out, what will be the implications for the economy for growth and for employment. I think it’s too early to know that. So, I mean, ultimately, we think our policy rate is in—is in a good place to stay as we await further clarity on tariffs and, ultimately, their implications for the economy.” Moreover, recent rhetoric from almost all FOMC members since after the meeting has also been in lock step with most members willing to “wait-and-see” the impact of recent trade policies in the data.

The minutes highlighted greater risks to each of the Fed’s dual mandates, which if realized could lead to a challenge for the Fed as “Overall, participants judged that downside risks to employment and economic activity and upside risks to inflation had risen, primarily reflecting the potential effects of tariff increases. Participants noted that the Committee might face difficult tradeoffs if inflation proves to be more persistent while the outlooks for growth and employment weaken."

Here’s a headline grabber but am not sure this one here checks out with things like vix, MOVE or uncertainty indices …

30 May 2025 UBS: More uncertainty in an uncertain world

There is yet more uncertainty in the US economy. US President Trump appealed the ruling that their trade taxes were illegal. While this is decided, the taxes stay. There are thus three layers of uncertainty. Will the taxes survive? If they are illegal, will US companies and consumers get refunds? And are trade taxes today actually being collected? There is also uncertainty around how US companies will react to this uncertainty, especially with pricing.

The US April personal consumer expenditure deflator is due today. It is too early to see the direct effects of trade taxes. The consumption data may start to show some payback after Democrat-leaning states front-loaded purchases of some consumer goods earlier in the year. Final May Michigan consumer sentiment data says little of itself. However, comparisons to the preliminary data suggest the evolution of partisan bias as Trump retreated from trade taxes…

Covered wagons offered …

May 29, 2025 Wells Fargo: Weaker Spending, Slipping Profits & Court Order on Tariffs Underlying Growth is Slowing as Profits Shrink

Summary A 0.2% contraction compared to a first estimate of 0.3% may appear mild, but the underlying details are not encouraging. Corporate profits fell 3% and a key yardstick of underlying private demand slowed from 3.0% to 2.5%. We also unpack the overnight court ruling that puts tariffs on ice.

May 29, 2025 Wells Fargo: Don’t Get Taken by Supplies How Deliveries Might Overstate Activity in ISMs

Summary We are raising the warning flag now that trade-war dynamics have scope to influence supplier deliveries in such a way that it may be a less-than-perfect way to measure activity in both manufacturing and the service sector, at least for a time.

To be clear, once and for all, NVDA is NOT, repeat NOT Cisco, our government with checks and balances AND we love, love LOVE when Global Wall PhDs tell us they told us so, amIright?

The US is a federal republic. It isn't a democracy, where the majority always rules. The constitutional system was designed by the Founding Fathers, who were mostly lawyers, to provide checks and balances to avert the concentration of political power and to protect the rights of minority parties against abuses by the majority as well as by those in power. The three branches of government were designed to frustrate the ambitions of the powerful on a regular basis.

In other words, "gridlock" is a feature, rather than a bug, of the American constitutional system. Gridlock has generally been viewed as bullish by stock and bond investors. The companies they invest in tend to do best when government is the least meddlesome in their businesses…

…The federal funds rate futures market is currently anticipating three 25bps rate cuts over the next 12 months (chart). We remain in the none-and-done camp through the end of this year.

The Fed is in no rush to lower interest rates because the economy remains resilient. The Bureau of Economic Analysis revised its estimate of Q1's real GDP to show the economy shrank at an annual rate of 0.2% (saar), compared with the previously reported 0.3% drop. However, that contraction was attributable to a 42.6% spike in imports—driven largely by companies racing to get ahead of Trump's tariffs..

May 28, 2025 Yardeni: From Trump's Tariff-Postpone-Repeat to Court's Cease-and-Desist

In imposing his tariffs in early April, President Donald Trump called the trade deficit a national emergency that justified his doing so. This evening, the Manhattan-based Court of International Trade said the US Constitution gives Congress exclusive authority to regulate commerce with other countries that is not overridden by the president's emergency powers to safeguard the US economy. "The court does not pass upon the wisdom or likely effectiveness of the President's use of tariffs as leverage. That use is impermissible not because it is unwise or ineffective, but because [federal law] does not allow it," a three-judge panel said in the decision. The Trump administration minutes later filed a notice of appeal.

Stock futures surged on the court's ruling as well as on Nvidia's strong earnings report after the market closed. The 10-year US Treasury yield remained around 4.50% this evening. The Dollar Index (DXY) firmed and the price of gold slipped.

Two days after Trump's April 2 "Liberation Day," we anticipated the court ruling in our April 4 QuickTakes:

The federal laws governing tariffs give the President very broad authority over trade policy generally, and specifically over tariff rates. However, Trump's tariffs are likely to be challenged in courts. In his executive order announcing the latest round of tariffs, Trump claims the power to do so under a wide range of federal laws, including the International Emergency Economic Powers Act and the Trade Act of 1974. The plaintiffs are likely to ask the courts to deny that the President was justified in declaring a national emergency.

We concluded "that the negative impact of Trump's tariffs will be over by mid-year ... If so, then the current stock market selloff is a buying opportunity."

Five days after Liberation Day, we wrote in our April 7 Morning Briefing:

Trump's Liberation Day last Wednesday triggered Annihilation Days on Thursday and Friday, with the Stock Market Vigilantes giving a costly thumbs-down to Trump's Reign of Tariffs. Trump officials say they aim to make Main Street wealthy again even if that's bad for Wall Street. The problem is that Main Street owns lots of equities traded on Wall Street, so the two streets prosper and suffer together. Congress can't do much to stop Trump given his veto power, but he might get the message that hurting Main Street's stock portfolios can cause a recession and jeopardize the GOP majority in Congress. If so, he might postpone the reciprocal tariffs, giving trade negotiations time to work. Also, the courts might block Trump's tariffs. An early end to Trump's tariff nightmare would result in a V-shaped stock-market bottom. We're counting on that; the alternative is just plain ugly.

Our April 8 QuickTakes was titled, "Is Something About To Blow Up In The Credit Markets?" We warned:

The Stock and Bond Vigilantes are signaling that the Trump administration may be playing with liquid nitro. Something may be about to blow up in the capital markets as a result of the stress created by the administration's trade war.

Indeed, the 10-year the US Treasury yield jumped from 4.01% on April 1 to 4.50% on April 11 (chart). That spooked Trump and his advisors, which is why they chose to postpone Liberation Day on April 9. The S&P 500's correction, which started on February 19 ended on April 8, one day before Trump postponed Liberation Day by 90 days.

As Nvidia's stock price soared during 2024, the naysayers compared its ascent to Cisco's roundtrip performance during the Tech Bubble of the late 1990s, which was followed by the Tech Wreck of 2000 and 2001 (chart). Cisco was the tech darling of the dawning Internet Age. Nvidia is leading the way in the AI Age. Cisco crashed when the Dot.Com Bubble burst.

When DeepSeek was introduced on January 24, 2025, it was widely feared that Nvidia stock might crash if the current datacenter boom is a bubble bound to burst (chart). Instead, the company today reported a blockbuster fiscal Q1 (ended April), with revenues in its datacenter business (which makes chips and other components used in AI computing systems) surging 73% y/y to $39.1 billion. US technology giants Microsoft, Amazon, Google, and Meta all affirmed plans to boost capital spending on AI infrastructure this year in their latest earnings reports. Analysts expect combined spending by those four alone to top $345 billion this year, up 41% from last year.

We've observed that demand for more datacenter capacity is actually driven by robust demand for more cloud computing. AI is certainly contributing to that demand, but the main driver is the Digital Revolution that started in the mid-1960s. The revolution is all about processing more data, more rapidly, and more cheaply. This process feeds on itself…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Credit Default Swaps …

May 30, 2025 Apollo: US Sovereign CDS Spread at BBB Levels

The US sovereign CDS spread is currently trading at levels similar to countries that are rated BBB+, such as Italy and Greece, see chart below. For solutions to the US fiscal challenges see here and here.

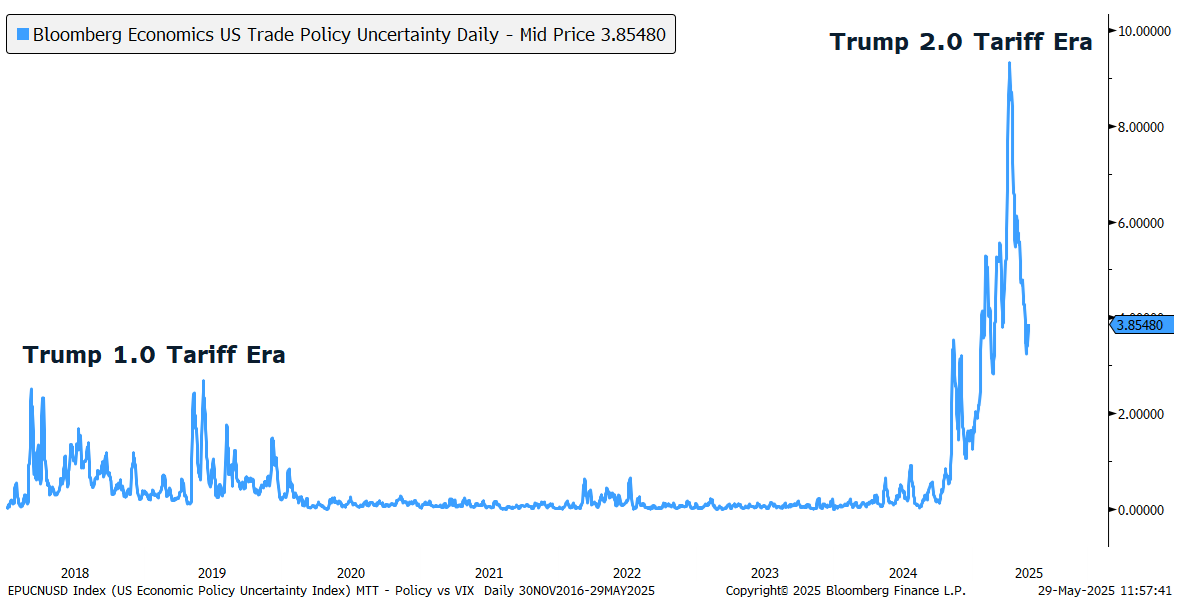

…And while trade policy uncertainty has dropped significantly since the reciprocal tariffs were announced on April 2, it still remains relatively high. The Bloomberg Economics U.S. Trade Policy Uncertainty Index — compiled by analyzing the proportion of news stories that include words related to trade policy, such as tariffs, alongside language that expresses uncertainty, within the total number of articles searched — remains well above pre-Election Day levels or readings registered throughout the Trump 1.0 tariff era. As investors, we know the market hates uncertainty, and it is no coincidence that the trade uncertainty index peaked as the market bottomed last month. Importantly, high levels of trade policy uncertainty tend to correlate with high implied volatility, suggesting investors should expect a bumpier path for stocks until there is more clarity on trade.

U.S. Trade Policy Catches Another Curveball

…Summary The recent CIT summary judgment adds more complexity to an already messy trade outlook. While the blockage of most tariffs enacted under the IEEPA has the potential to significantly reduce the average effective tariff rate in the U.S., it will not mark the end of President Trump’s trade strategy. The administration has already appealed the ruling (which is likely headed to the Supreme Court) and could implement a range of legal countermeasures against the blocked tariffs. Furthermore, the CIT ruling is likely to weaken the U.S.'s hand in current trade negotiations and could further exacerbate deficit concerns. Higher trade policy uncertainty also tends to coincide with increased implied volatility, so investors should expect elevated turbulence until there is greater clarity on trade.

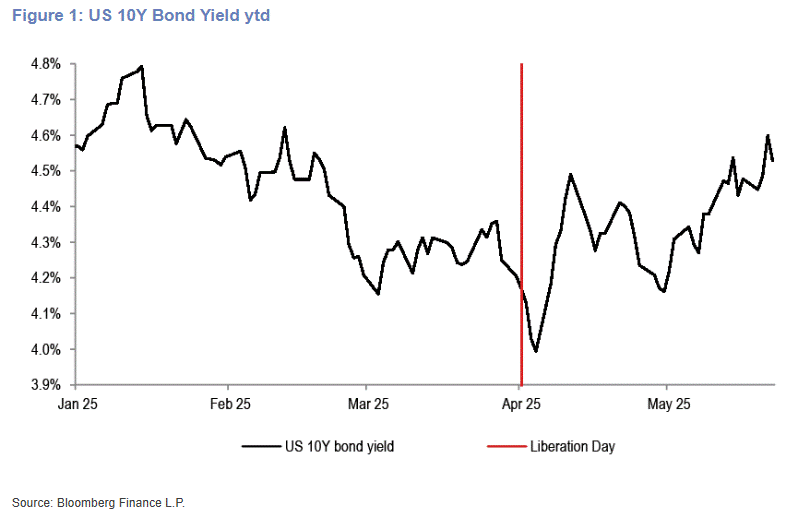

The selloff in bond markets over the last month has been notable, with 10-year U.S. Treasuries (IEI) down ~3% and 30-year U.S. Treasuries (TLT) down ~8%.

Bond yields are moving higher for the wrong reasons – a combination of tariff-driven inflation pickup, rising fiscal deficit concerns, scorching high debt service costs, the big beautiful bill from the House, and a recent Moody's downgrade of the U.S. government's credit rating.

Taken together, a somewhat punitive cocktail and one the bond vigilantes drink hand over fist.

Then, last week’s auction of 20-year U.S. Treasury bonds was the cherry on top.

The typically run-of-the-mill, non-event in which Treasury auctions off new debt to finance the whole party, showed surprisingly soft demand from investors. This lead the long-dated 30-year U.S. Treasury to touch 5.13%, eclipsing the October 2023 cycle highs and reaching the highest level in yield since 2007 – when the Fed Funds Rate was 100 bps higher than it is right now.

What’s more, the carnage in rates is really a bigger, global phenomenon if we zoom out. Investors are demanding higher rates around the world.

Take Japan whose 30-year sovereign bond climbed to a 20+ year high, while their newer 40-year sovereign bond yield printed an all-time record.

Call it the fiscal yips.

Revisiting cycle highs amid easier monetary policy is consistent with rising term premiums and rapid supply outstripping demand in this environment.

Joe Brusuelas, chief economist at RSM, recently wrote in a note to clients: “This rise has taken place not for virtuous reasons around faster growth but rather because of risks around higher inflation and the need for higher interest rates to compensate for holding long-dated dollar-denominated assets.”

It’s hard to find a fan of bonds these days.

Although trend components remain negative and the fiscal side remains an ongoing decades-long mess, it’s important to take note of certain elements that are bullish for bonds.

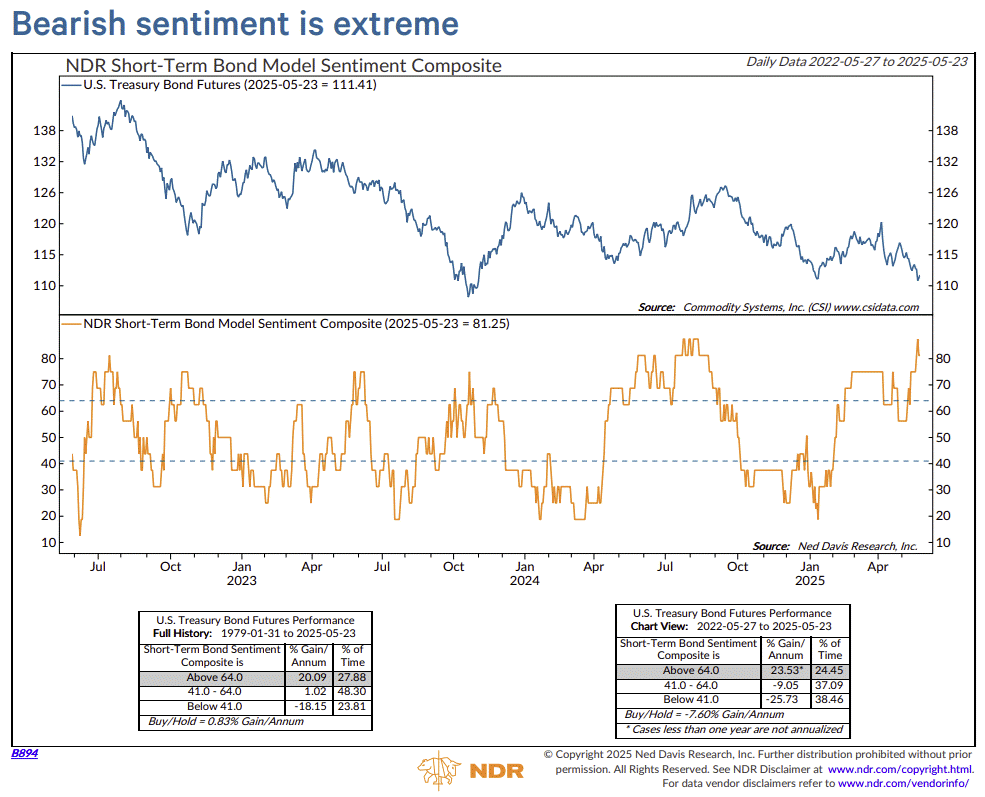

As we know, it’s important for investors to beware of the crowd at extremes. Per Ned Davis Research’s proprietary sentiment index, bond sentiment is about as pessimistic as it gets. See the orange line in the bottom pane below.

The bond market has gotten oversold, as measured by Relative Strength Index (RSI). Similarly, the put/call ratio of options on Treasury bond futures have hit important levels, indicating excessive hedging.

Oil prices have been under pressure all year, which means inflation expectations must remain anchored. This keeps a lid on yields.

The Senate needs to pass its version of the big beautiful bill before it can be reconciled against last week’s House version. This leads to a likely outcome the final bill will be less onerous than current reporting and is reprieve for a possible rally in bonds.

Tariff revenue, in its earliest stages of collection, is showing promise as an offset, although falling far short of the initial promises of $2B per day from the White House. In March, the Treasury Department collected $9.6B. In April, it was up to $17.4B. In May, with a few days remaining, the total is up to $22.3B. For the year, $92B has been received. For context, U.S. government receipts were $80B in all of 2023.

I was searching for you, yesterday...

Internet Outage.......I know the feeling.....hate when that happens

Glad you're back...