HIMCO quarterly report remains to be seen and so, I’ll continue to kill time and attempt to fill the void ahead of it and this afternoons $39bb 10s.

First, a look back …

ZH: Ugly, Tailing 3Y Auction Sees Record Directs As Foreign Demand Slides

... Perhaps it will be different this time with regards to 10s and so, ahead of this afternoons $39bb 10s …

10yy: 4.50% support and 4.33% (200dMA, TLINE) resistance …

… concession ALWAYS welcome and a with momentum (stochastics, bottom panel) overSOLD on DAILY basis, a slight push higher may very well be just what the ‘supply doctor’ ordered … MAYBE …?

… this lack of a firm view stems from a fear of commitment — to wrong answers — and comes in addition TO what was laid out / put forth (HERE) where it STILL seems that 10s are HOME ON (in) THE < Rosie > RANGE … despite the marginal / short-term TLINE break noted above …

I’ll quit while I’m behind because it just is that I’ve not much to add here / now. But first, here is a snapshot OF USTs as of 715a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: EU-US trade deal said to be close, seven letters expected today … A modest upward bias for benchmarks after a few sessions of relatively marked pressure … Strength comes despite the constructive risk tone. But, the magnitude of today's move is limited in nature with Bunds for instance still lower by over 60 ticks WTD, and the move more a function of Bunds retracing some of Tuesday’s supply-induced pressure (primarily from EU debt) than a pronounced move higher … USTs a similar story with specifics light into supply and FOMC Minutes. Thus far, confined to a 110-24 to 110-29+ band, within Tuesday’s slightly more expansive 110-21+ to 111-01+ parameters, and by extension shy of Monday’s 111-12+ WTD peak.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … You’ll find more than a few commentaries dedicated to GLOBAL fiscal follies and fears …

Fiscal follies fears … not just a US thing. France on Japan …

09 JUL 2025 BNP: JPY rates: Third wave in super-long JGBs – fear than fact

Concerns about a fiscal spending boost after upcoming upper house elections have dominated the super-long sell-off this week. Fears are not facts, of course, but we appreciate it as an important consideration at such times.

We keep IRS 10y10y long and long 30y swap spread. We also like to take risk outside the super-long sector as risk diversification.

New trade: IRS 2s5s flattener. Target entry 20bp. target profit 15bp. Stop out 24bp. DV01 30k.

A fan fav German stratEgerist commenting on fiscal follies and fears … it must be a thing, then, eh??

… Equity markets have treaded water over the last 24 hours, even with the latest tariff developments and some renewed jitters in global bond markets around fiscal sustainability. That meant yields rose in pretty much every major economy, with 10yr Treasury yields (+2.0bps) by no means the worst hit but still rising for a 5th consecutive session, before rising another +1.4bps this morning. Meanwhile, the S&P 500 (-0.07%) edged back for a second day as Trump said there’ll be no further tariff extensions beyond August 1st, with futures down another -0.12% overnight. And it was also a record day for US copper futures after Trump said copper would face 50% tariffs, with the biggest daily jump (+13.25%) in available data back to the late-1980s.

In terms of how the day unfolded, that bond selloff initially began in Japan, where there was a big spike in long-end bond yields that pushed the 30yr yield up +9.0bps, and back above 3%. That’s coming ahead of the upper house election there on July 20, where the major parties are advocating further spending or tax cuts, so that’s adding to concerns at a time when the Bank of Japan are already scaling back their bond purchases. And as we just managed to sneak into yesterday’s edition, the Reserve Bank of Australia voted to keep rates on hold, even though a cut was widely expected, so that helped to push yields higher in Australia too…

…Coincidentally, the OBR fiscal watchdog published their “Fiscal risks and sustainability” report yesterday, which concluded that demographic pressures would help push debt-to-GDP above 270% of GDP by the early 2070s, at least on current policy. Admittedly, it’s a similar situation if you look at the CBO’s long-term reports for the US, but it demonstrates how this problem isn’t going away on the current trajectory.

These concerns were clear on both sides of the Atlantic, and 30yr Treasury yields earlier got close to 5% again, closing up +0.9bps at 4.92% after having reached 4.97% in early NY trading. Bear in mind we’ve got a 10yr Treasury auction today and a 30yr auction tomorrow, so those will be in the spotlight to see how much demand there is. Meanwhile in Europe, 10yr bund yields were up +4.4bps to 2.69%, whilst the 30yr yield (+5.4bps) hit 3.17%, which is just shy of its post-Euro crisis peak of 3.21% from late-2023…

…Otherwise, trade and tariffs were the main focus yesterday, and the big development was Trump saying that “No extensions will be granted” to the August 1 deadline on the reciprocal tariffs. That’s a shift in tone from Trump’s own comments on Monday evening, as Trump had said that the August 1 date was “not 100% firm”, and investors had been hopeful that ongoing negotiations and trade deals could avoid that. So it’s a clear hardening up of the rhetoric. During a cabinet meeting yesterday, the President took a hard line against the BRICS countries again, saying the group was “set up to hurt us…I can play that game too so anybody that’s in BRICS is getting a 10%” tariff addition. This comes even though he had previously noted that he was close to a deal with India. In addition, the President took a more hawkish tone, indicating that some countries would be seeing a 60% or 70% tariff rate and that sectoral tariffs are coming. While pharma, autos, and steel have been well flagged, the President proposed a 50% rate on copper products and said that some drug levies could reach as high as 200%, although the President stated that the pharma tariffs would only come after a “year or year and half ”. Copper first month futures on the NY exchange hit an all-time high in response, as prices rose 13.25% (17% intraday), which was the largest daily move since on record going back to 1988.

A chart of the day from Germany, for our review … stocks vs bonds, who you got …

8 July 2025 DB CoTD: Do near record low US dividends matter?

One WOW chart in the pack—on page 56—shows that S&P 500 dividend yields are now within just 20 basis points of their all-time low, last reached during the tech bubble in 2000. In today’s CoTD, we add another dimension: 10-year U.S. Treasury yields.

Prior to 1958, dividend yields were consistently higher than government bond yields. Equities were seen as inherently risky—lacking diversification, regulatory oversight, or corporate transparency. Investors demanded a high dividend yield as compensation. On top of that, dividends often enjoyed more favourable tax treatment than today, reinforcing the view that income was the most reliable path to long-term returns.

That all began to change in the post-war boom, when the market’s perception of equity risk shifted. From the late 1950s onward, dividend yields fell below bond yields —a dynamic that would persist for more than half a century. Rising corporate earnings, improving investor access to diversification (via mutual funds and pensions), and growing inflationary pressure on bond returns made equities more appealing, even with lower income yields.

This shift gained further momentum in the early 1980s, when capital gains taxes were reduced and a new era of share buybacks began. The trend exploded in the 1990s tech boom, as high-growth companies (many in tech) retained earnings to reinvest, rather than distribute them as dividends. This mindset—growth over income—has returned with force over the past decade, once again led by mega-cap tech.

It’s worth spotlighting buybacks specifically. Prior to 1982, SEC rules discouraged buybacks due to concerns over market manipulation. But regulatory changes that year effectively legalised them under clear guidelines. The result: a major shift in corporate capital return behaviour. By the mid-2000s, buybacks overtook dividends as the primary way U.S. companies returned capital to shareholders—and have remained dominant ever since…

…And with dividend yields now approaching all-time lows, there’s a case to be made that valuations and investor expectations have become stretched. In a crisis, the lack of durable income from dividends may matter more than markets currently appreciate…

… Same shop with an economically rhetorically inspired question …

08 July 2025 DB: How high is the tariff rate? Updating our tracker to reflect Trump's letters

On July 7, the Trump administration began sending out letters to other heads of state notifying them that imports from their countries will begin to face higher tariff rates beginning on August 1st if they fail to reach a trade agreement. Trump and other officials mentioned that more letters will be sent out this week.

In this piece, we update our tariff tracker to account for these higher rates, should they end up going into effect. We find that the rates announced thus far would raise the average tariff rate (using 2024 import weights) by about 1.7 percentage points to 18.7%. This increase could add up to 15bps to inflation.

Should the April 2nd tariff rates on other countries go into effect, the average rate would increase another 3.7 percentage points to 22.4% and could add another three-tenths to inflation.

I’m not alone in thinking / fearing the fiscal …

8 July 2025 ING Rates Spark: Fiscal fears everywhere

Fiscal concerns in Japan are pushing up global 30Y rates and since structural forces are not in favour of longer-dated bonds, we find it difficult to see offsetting factors. Tuesday's US 3yr auction was not great, but tolerably fine. Wednesday's 10yr auction will be more telling, as that's where the long end rising rates pressure really begins

US 3yr was okay, but the 10yr and 30yr will likely prove to be a more telling story

It’s never easy to predict what’s coming. But especially now. Not only is there policy uncertainty to contend with, but the policies themselves are hugely impactful. Two of the biggest ones have come in the guise of 'Liberation Day' and the 'Big Beautiful Bill'. The former has left us with an average tariff rate of 13%, and rising, as letters get sent to those on the naughty list, while the latter brings a clear tax-cutting tint to fiscal policy, and leaves the US with a large ongoing structural fiscal deficit, with supply pressure to boot. Tariff revenues help to finance the tax cuts, but likely push US inflation up towards 4% in the coming months.

While Treasury Secretary Scott Bessent has no immediate plans to push issuance pressure out to longer tenors, that does not mean that issuance pressure goes away. To begin with, it is heavily bills-focused, and we’ll feel this now that the debt ceiling has been raised (done in conjunction with the passing of the Big Beautiful Bill). The US Treasury will issue big, as they need to replenish cash balances that have been spent down in an effort to stay within the debt ceiling to date. This will also act to take reserves out of the system, tightening conditions generally. This, alongside the tariff-induced spike in inflation, could well be a problem for long rates.

Tuesday's 3yr auction was not great, but tolerably fine. Wednesday's 10yr auction will be more telling, as that's where the rising rates pressure really is. Thursday's 30yr auction arguably is even more telling, as that's where the pain point has been in the UK and Japan recently.

Structural forces not in favour of longer-dated bonds

Long-end bonds felt particularly heavy at the start of this week with 30y Bund yields already up by 8bp this week. This is in part a spillover from Japanese 30y bond yields having risen 20bp over the same time span on the back of fiscal concerns. That is a theme of course also on the mind of many investors in German Bunds given the government's spending plans, but certainly also in US Treasuries and Gilts – the latter 30y now up by 12bp since the start of the week.

We find it difficult to find factors that would bring a halt to the strong upward momentum in 30Y global rates from a structural perspective. The fiscal concerns are broad-based, with also the US and UK worrying investors. Then we have quantitative tightening continuing in the background, adding interest rate risk to absorb for the market. More niche stories like the Dutch pension reforms are not helping either and reduce demand for longer-dated swaps and bonds…

The Treasury curve continued to bear steepen today with long-end yields initially rising in sympathy with other DM government bond markets, before partially retracing the move late in the session

Tomorrow Treasury will auction $39bn reopened 10-year notes at 1pm, unchanged in size from the last reopening auction. Given modestly rich valuations and a mixed technicals picture, we believe the auction is likely to require some concession in order to be digested smoothly

The 30-year bond backup approaches the 4.99-5.025% support layer. We suspect the long end will find buying interest in that area

…Ten-year yields are roughly unchanged from the last auction and are roughly in the middle of their year-to-date range, though they are 20bp above their local lows reached at the end of June. Intermediate yields appear fairly valued, once adjusting for marketbased growth, Fed, and inflation expectations, as well as the size of the Fed’s balance sheet relative to the size of the economy and a dummy variable to capture policy uncertainty. Along the curve, the sector has underperformed versus the wings on an outright basis over the past week, but remains slightly rich after adjusting for the level of yields and slope of the curve. Indeed, we have noted previously that the intermediate section appears rich on a multi-year basis and that the wings of the Treasury curve offer more value than the belly (see Treasuries, US Fixed Income Markets Weekly, 6/6/25). From a technicals perspective, volatility in the sector has subsided, while market depth has improved to its highest levels since February. Positioning has become longer in recent weeks, though it has not reached the stretched levels seen prior to April. Overall, given less attractive valuations and a mixed technicals picture, we believe the auction is likely to require some concession in order to be digested smoothly.

…Technical Analysis The DM bear steepening pressure sees the US 30-year bond backup approach support at the 4.99% May 22 61.8% retrace and 5.005-5.02% Jan/Apr yield highs (Figure 3The 30-yarbond ckuparohes t4.9-502% suportlaye. Wsupcthe longdwi fbuyngiters nhate.). We suspect the market will find buying interest near that support zone and help cap yields over the near-term. The weekly momentum divergence buy signals we focused on in our mid-year outlook bolster that view, as analysis of the price action after those signals in recent decades shows a clear bias for the market to mean revert to lower yields during the subsequent two month period (65% hit-rate). Those signals were triggered as the May yield high tested the 5.18% Oct 2023 cycle cheap. Beyond those yield levels, longer-term support comes in at the 5.32-5.36% Apr-May equal swings objective and Sep 2024 channel trend line. To lower yields, tactical resistance rests at the 4.875% 50- day moving average and nearby tactical pattern breakdown. the 4.73% Jul 1 yield low stalled just shy of the 4.72-4.725% cluster of Fibonacci retracement levels connected to the Apr yield lows. The next cluster of resistance rests at the 4.60-4.65% 200-day moving average, Apr 61.8% retrace, and Apr 30 yield low. We see the Sep-Apr channel trend line as a medium-term resistance level that will likely contain a bond rally in the months ahead. That line sits at 4.50%.

… a few words on weight on longer-end of global yield curves …

July 8, 2025 MS: Global Macro Commentary: July 8: Long-End Headwinds

Fiscal and tariff uncertainties weigh on long-end duration; JGB sell-off spills over to bunds, gilts, USTs; RBA unexpectedly holds rates; Copper prices surge after tariff announcement; President Trump reaffirms Aug. 1 tariff deadline; DXY at 97.53 (+0.0%); US 10y at 4.399% (+2.0bp).

…Global fiscal concerns alongside ongoing tariff and political uncertainty provide headwinds to long-end rates.

Super-long JGBs extend cheapening amid renewed tariff pressures after President Trump announces 25% tariffs on goods from Japan, and amid heightened domestic fiscal concerns ahead of the election. JGB curve bear-steepens with 30y yields 10bp higher on a simple yield basis, and JPY underperforms (USD/JPY: +0.3%).

Australia rates bear-flatten (2y: +11bp) and AUD outperforms G10 pairs (AUD/NZD: +0.5%) after the RBA keeps rates on hold at its July meeting, against expectations for a 25bp cut. Our economists revert to a slower RBA policy path forecast.

The JGB sell-off spills over to broader markets with European duration bear-steepening in sympathy (30y Bund: +5bp). Tepid demand at a 5y Bund auction also weighs on the curve.

USTs open cheaper on the back of the rising fiscal concerns in Japan, and maintain some losses into NY close (10y: +2bp). A 0.5bp tail in the 3y UST auction has limited impact on price action; the below-average bid-to-cover ratio and indirect allotment are offset by record-high direct participation.

The economic calendar and schedule of Fed appearances (see schedule below) are light this week. On Wednesday at 2pm ET, the release of the FOMC minutes from the June 17-18 meeting are due to be released. A lot of information has been communicated from the Fed in recent weeks, via Powell’s post-FOMC press conference/congressional testimony, and a slew of Fed speeches and media interviews. Thus, we do not expect the FOMC minutes to contain too much new information.

Meanwhile, the June employment report was stronger than expected (see our recap here), with 147,000 jobs added on the month and a 0.127pt drop (to 4.117%) in the unemployment rate—below the Fed's SEP estimate of the long-run rate (4.2%) and their (and our) 4.5% projection for the Q4 average. In turn, the report seems to have sealed the deal for no action from the FOMC on July 29-30 and lessens the probability of a cut at the September meeting too (market participants now anticipate less than 5% probability of a July cut versus ~25% a day before the employment report; and September now shows expectations of a 25bp cut at ~64% versus 91% prior to the jobs report).

As for inflation, we expect the CPI (due next Tuesday, July 15) to pick up a little this month…

…Against that backdrop, we continue to expect that the Fed will hold off from any action until after Chair Powell’s term expires (May 15, 2026).

Switzerland notes everyone everywhere lookin’ to place blame … DJT = inflation = no rate cuts ever? Interesting, for sure but … what IF Paul, here’s wrong … and tariffs aren’t inflationary …

Scapegoat economics creates a story that incorrectly blames a group for everything that is going wrong. Prejudice politics promises to reduce that group’s influence. Because scapegoats are not the problem, new scapegoats continually need to be found when prejudice fails to solve the problems.

US President Trump created a new scapegoat yesterday. Announcing a 50% tax on copper has dramatic effect (50% sounds impressive), but directly such a tax adds about 0.03 percentage points to consumer price inflation. Very simplistically, because the US imports about half its copper, US prices should settle 20-25% above global prices. Less would signal expectations of another Trump retreat.

Threatening a future 200% tax on pharmaceutical imports creates another scapegoat. The US has one of the highest cost healthcare systems delivering one of the lowest life expectancies in the developed world, so tariff retreats are expected. The erratic policy announcements still generate risk, and the general process suggests new scapegoats will be targeted in the future.

Trump is expected to announce more US consumer taxes today. The minutes of the last Federal Reserve meeting are likely to articulate a collective shrug of the shoulders. ECB Chief Economist Lane is speaking—any currency-related comments might ignite a flicker of interest.

Covered wagon folks on small biz and trying to keep tabs on tariffs …

July 8, 2025 Wells Fargo: Small Business Confidence Edges Lower in June Policy Changes Remain a Headwind for Small Firms

Summary Sentiment Mostly Steady, Though Headwinds Mounting The NFIB Small Business Optimism Index fell to 98.6 in June from 98.8 the month prior. The small decline in business sentiment reflects ongoing concerns about the economic ramifications of shifting trade and immigration policies. On net, more firms raised selling prices, reduced capital spending, reported difficulties filling open positions and lowered expectations for economic growth.

…Inflation Creeping Back The net share of firms that raised average selling prices rose by four points in June. Plans to raise prices also increased, though by just one point. Over the past few months, both measures of small firm pricing have climbed modestly higher, suggesting businesses are responding to prospects for higher input costs.

July 8, 2025 Wells Fargo: Keeping Tabs: Tariff Tracker Update

Summary In the latest pause on tariff implementation, the window for deal-making is extended, but so too is the uncertainty that complicates capital spending decisions. This report unveils our latest tariff tracker featuring increased visibility into our process.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

The consensus economic forecast is that growth will slow down over the coming quarters as higher tariffs weigh on earnings, capex spending, and consumer spending.

The consensus equity analyst forecast is that earnings will accelerate over the coming quarters, see chart below.

This is not consistent. Either the MBA forecasters are wrong about corporate earnings, or the PhD economists are wrong about tariffs slowing down growth.

The second-quarter earnings season will start next week and reveal who is right. If earnings continue to be strong, the adverse effects of tariffs, as expected by economists, will prove to be incorrect.

In other words, either the equity analysts are too optimistic, or the economists are too pessimistic.

Positions. Lives. Matter. None better detail them than EBB …

July 8, 2025 at 8:30 PM UTC Bloomberg: Treasury Bulls Unwind Big Bets as Strong Data Pushes Yields Up By Edward Bolingbroke

Futures traders have been unwinding some large bullish bets on Treasury bonds, adding to the recent upward pressure on US yields after a surprisingly strong jobs report last week.

Traders had built up substantial long positions in Treasury markets ahead of Thursday’s payrolls data, anticipating that a weak reading would bolster the case for lower rates.

But since those expectations were quickly confounded, the amount of risk held by futures traders — the open interest — has fallen rapidly over the past couple of sessions. The de-leveraging is putting a profit squeeze on Treasury bulls, with changes concentrated in futures tied to 5- and 10-year notes.

On Thursday, approximately $5 million per basis point of risk was liquidated on contracts tied to the 10-year note. This is roughly equivalent to traders offloading $7 billion of the 10-year Treasuries.

The market came under pressure again Tuesday, as demand for long-term sovereign debt across the globe waned amid concerns that governments are becoming overly reliant on long-dated bonds.

“The strong NFP print drove the market to cut expectations of a July rate cut to zero with cheapening driven by long liquidation as recent longs came under pressure,” Citi strategist David Bieber wrote in a note.

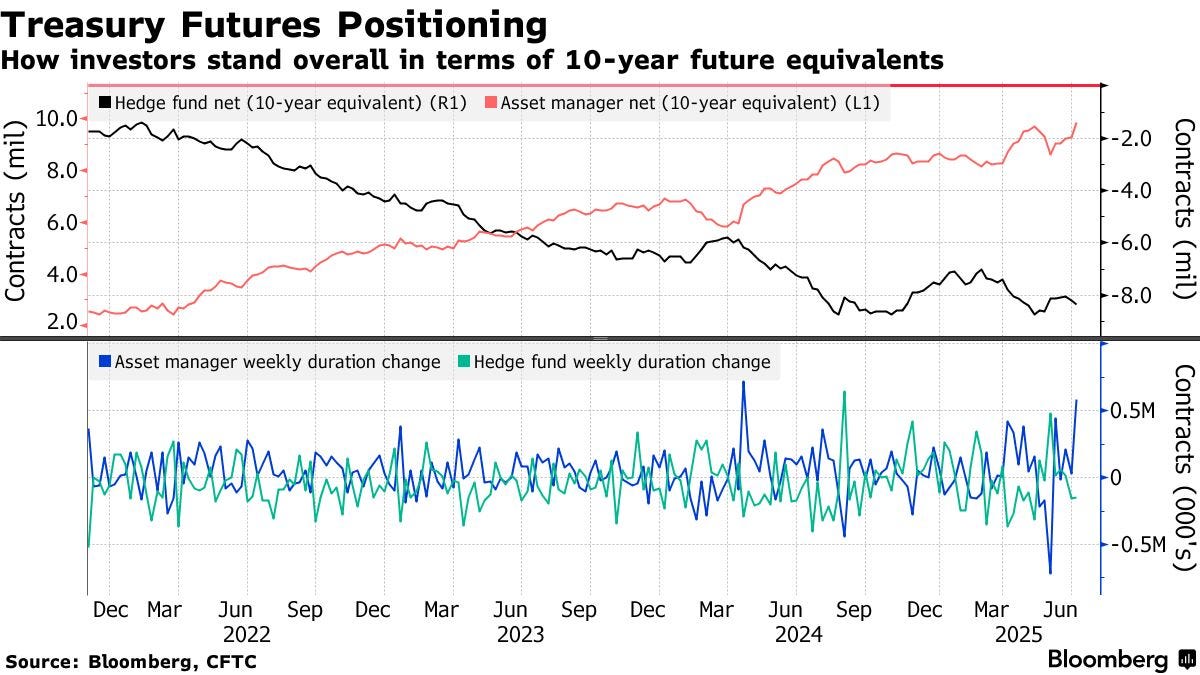

He added, though, that tactical positioning in Treasuries “still remains extended long” with recent bullish bets now in the red. Data released Monday by the Commodity Futures Trading Commission showed a big jump in bullish positioning among asset managers in both 5- and 10-year note futures, which now sit at record-long levels.

The upcoming sales of $39 billion in 10-year notes and $22 billion of 30-year bonds on Wednesday and Thursday have the potential to further squeeze Treasury bulls concentrated in long-duration bets, especially if there are any signs of weak demand. Tuesday’s $58 billion 3-year note sale saw a solid reception…

…CFTC Futures Positioning In the build-up to last week’s payrolls report, asset managers had aggressively ramped-up long positions in Treasury futures, notably in both 5- and 10-year note contracts which hit a record net long amount, along with the ultra 10-year note futures. On the week, shown by CFTC data up to July 1, asset managers extended net duration long by about 582,000 10-year note futures equivalents, the biggest weekly long extension since April 2024. On the flip-side hedge funds added around 148,000 10-year note futures equivalents to net duration short.

… With all the ‘palace intrigue’ of who will take over, a reminder from EBB …

July 9, 2025 at 10:00 AM UTC Bloomberg: Powell’s Successor May Struggle to Deliver the Rate Cuts Trump Wants

Close Federal Reserve watchers have a message for anyone who thinks the next leader of the US central bank will deliver lower borrowing costs on a silver platter: Don’t count on it.

While it’s an unlikely outcome, some investors have staked out positions in futures markets that will profit if interest rates drop immediately after Jerome Powell’s term as chair ends in May 2026. The trade has been fueled by President Donald Trump’s pledge to nominate “somebody that wants to cut rates.”

Those investors have targeted futures contracts linked to the Secured Overnight Financing Rate, or SOFR, which closely tracks the benchmark federal funds rate. They’ve sold off contracts that expire prior to Powell’s exit and piled into contracts that expire just after the expected arrival of a Trump-appointed chair.

It’s a trade that takes a chance on Trump getting his way, shrugging off how the central bank goes about setting rates.

A chair “can’t act like a dictator,” said Mark Gertler, an economics professor at New York University who has co-authored papers with former Fed Chair Ben Bernanke and former Vice Chair Richard Clarida. “He can’t call in the Marines or anything like that.”

Adjusting rates, Gertler pointed out, requires the support of a majority on the Federal Open Market Committee. Nineteen policymakers participate in FOMC meetings and 12 vote. In other words, the new chair will have to win over their colleagues with a reasonable case for cutting.

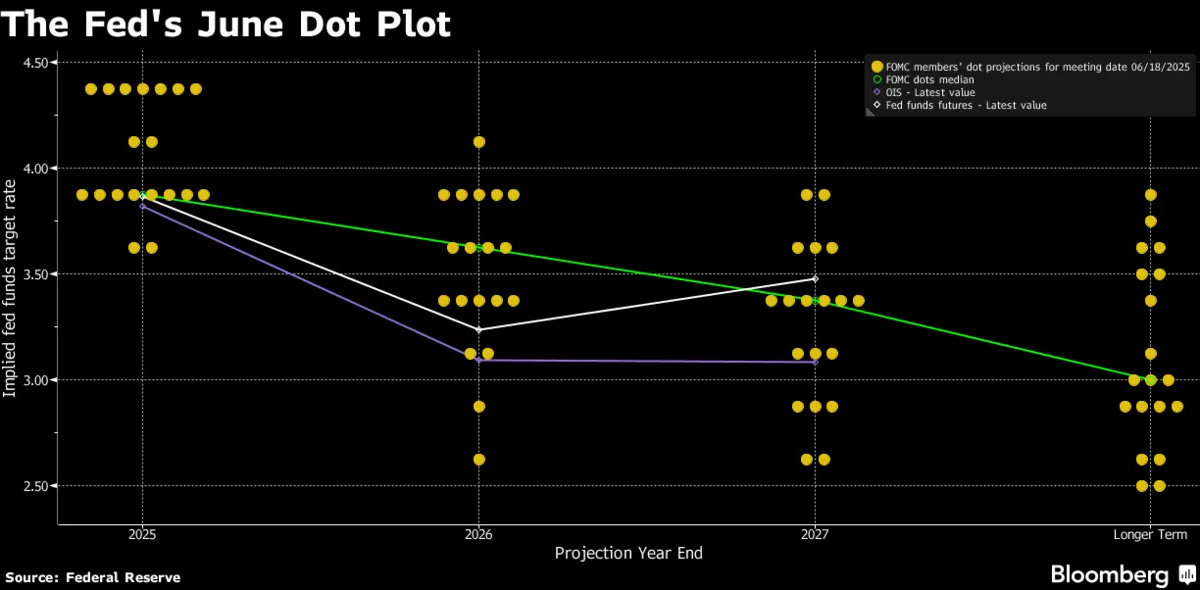

So far this year, Fed officials have agreed to hold borrowing costs steady in a range of 4.25% to 4.5%. But, as rate projections reveal, policymakers appear split over the outlook for cuts over the rest of the year, largely over differing views on how Trump’s tariffs might affect inflation.

Ten policymakers — those more inclined to see the impact of tariffs on prices as temporary — expect two or three cuts by year’s end. Two others see just one cut as appropriate and seven expect the benchmark rate to stay where it is. For next year, the range widens, with the upper boundary of the federal funds rate projected to finish 2026 anywhere from 2.75% to 4.25%.

The projections, being anonymous, can’t be linked with certainty to individual policymakers.

“It’s obviously a concern that the Fed will be less independent, certainly,” said Michael Feroli, chief US economist at JPMorgan Chase & Co. “Whether one person, even if that’s the chair, can immediately get the committee to agree to a big change in policy, I think that might be more difficult.”

Lining Up Votes

Trump’s pick to replace Powell won’t be the only person inclined to support his call for cuts. Fed Governor Michelle Bowman — whom Trump placed on the board in 2018 and promoted to the central bank’s top regulatory job last month — has so far this year supported holding rates steady, but recently said it might be appropriate to cut later this month. So, too, has Governor Christopher Waller, another Trump appointee.

The president may use the vacancy created in January when Fed Governor Adriana Kugler’s term expires to place his pick for chair on the Board of Governors. He’ll then get one more opening to fill if Powell resigns from his underlying post as a governor. That’s what outgoing chairs typically do, but Powell has declined to say whether he’ll exit altogether.

But even if Powell departs, that doesn’t add up to enough votes to make additional cuts. Whether others go along with lowering rates will depend more on what actually happens in the economy. And it could be difficult to peel away other policymakers one-by-one.

Dissents aren’t especially rare, but in an institution that values broad-based agreement, especially when policy shifts, votes are rarely deeply split.

“At the end of the day it’s a committee decision, and whoever the next chair is, he is going to have to build a consensus,” said Brett Ryan, US senior economist at Deutsche Bank Securities.

A view from The Terminal (noting updated S&P targets) …

July 9, 2025 at 4:16 AM UTC Bloomberg: New Trump tariff threats should be a big deal. They're not The risk is that too much ho-hum in the markets could be inflating the Trump Put.

…The Only Way Is Up (for S&P 500 Estimates)

The stock market has been prospering, and strategists are following it upward. A week of apparently market-unfriendly trade news has been accompanied by upgrades from influential Wall Street firms.

It’s easy to poke fun at analysts when they adjust their predictions. In a sense, they’re admitting they were wrong before. But it’s only reasonable to respond to new information, and if the stock market starts higher, that increases the chances for a stronger close. So it is that this week Bank of America’s Savita Subramanian has raised her end-year forecast from 5,600 to 6,300, while Goldman Sachs’ David Kostin moved his to 6,600, from 6,100:

What was their reasoning? For Kostin, the move is justified by shifting the projected forward earnings multiple up by 8%, from 20.4 to 22 times next year’s earnings. This is largely a play on likely lower rates:

Earlier and deeper Fed easing and lower bond yields than we previously expected, continued fundamental strength of the largest stocks, and investors’ willingness to look through likely near-term earnings weakness support our revised S&P 500 forward P/E forecast.

This is an expression of the view that tariffs won’t push up inflation and also won’t, against previous expectation, force the Fed to be more hawkish for longer. So the call is reasonable, but vulnerable to a rise in inflation in the coming months.

If the market is right and inflation continues to be supine, current market levels are justified and further gains are likely. If not, not. Unfortunately, much continues to ride on trade policy and its effects.

Specs bearish stocks …

LizAnnSonders

Large speculators/hedge funds keep pressing their bearish bets … net positioning for S&P 500 futures most negative since March 2024