Good morning … First up some Chinese data overnight …

ZH: Yuan Weakens After 'Unbalanced' Chinese Economy Sees GDP Beat In Q1 But Domestic Consumption, Production Disappoint

… Notably, that this is the first time the market compares two periods of economic growth without China'z Zero-COVID policy's impact, and overall, as we detail below, economic activity data in March overall missed expectations.

Industrial production rose 4.5% in March from a year earlier (below economists’ forecast of 6%).

Industrial output rose 6.1% for the first quarter (below the 7.0% in February).

Retail sales climbed 3.1%, also disappointing (versus an expected 4.8% gain) - domestic consumption is still weak amid deflation pressure and after imports shrank during the month.

Investment flows were mixed with Property investment continuing to slide (down 9.5%, worst since December, and considerably worse than the 9.2% expected)...

...but broad-based fixed-asset investment expanded 4.5% in the first three months (better than the 4% increase projected by economists).

Finally, the surveyed jobless rate in March declined to 5.2% from 5.3% in February…

… With that ‘development’ overnight there is some commentary below from Global Walls cognoscenti, as you’d expect. Wasting time on what is likely a highly manufactured set of data ALWAYS seems to me to be a waste of time — yours, mine and frankly, theirs and so I’ll serve up a quick look at 10s…

10yy: remaining in a bearish trend / channel with what looks to ME to be oversold momentum (stochastics, bottom panel) which reminds me then that markets can remain oversold/bought longer than my opinion can remain relevant …

… 4.35% — bottom of the channel — also noteworthy as it marked peak back in October of last year … WATCHING if / when a rally were to develop …

… for somewhat more competent review, have at this mornings notes / thoughts from Citi. Meanwhile, about this time YESTERDAY, FRBNY Williams was speaking …

Bloomberg: Fed’s Williams Still Expects Rate Cuts to Begin This Year

New York Fed chief says monetary policy is in a good place

If inflation gradually eases, it will be appropriate to cut

… “We will need to start a process at some point to bring interest rates back to more normal levels, and my own view is that process will likely start this year,” Williams said Monday in an interview with Bloomberg Television’s Michael McKee …

… AS ReSale Tales was crossing the wires …

CNBC: Retail sales jumped 0.7% in March, much higher than expected

Reuters: US retail sales beat expectations, boost first-quarter growth estimates

… Economists polled by Reuters had forecast retail sales, which are mostly goods and are not adjusted for inflation, would rise 0.3% in March. Sales jumped 4.0% on a year-on-year basis in March.

Reuters Graphics

Despite higher inflation and borrowing costs, spending is continuing to hold up, confounding predictions of distress among lower-income households, thanks to the resilient labor market…

ZH: Nominal Retail Sales Soared In March As Gas Prices Spiked

… The crucial core-control group - used in GDP calculation - ripped higher by 1.1% MoM - its biggest beat since Feb 2023...

Finally, bear in mind that these data are all nominal - not adjusted for the surge in prices of everything, especially gasoline - so are Americans spending more... for less.

…. and I’ll just leave this one be but certainly does feel as though they are destined to CUT rates despite or because of the ‘facts’ as they interpret them.

JPOW speaks later on today and as we know, all opinions are created equally and some are simply more equal than others and so … here is a snapshot OF USTs as of 701a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower this morning with intermediates leading the way south ahead of Powell's 'fireside chat' at 1:30pm this afternoon. Bunds have outperformed this morning with the US-German 10yr differential testing near +220bp again, widest since the very end of 2019. DXY is little change while front WTI futures are a hair lower (-0.25%). Asian stocks fell sharply after the same in NY trading yesterday, EU and UK share markets are all lower (SX5E -1.35%) while ES futures are showing -0.1% here at 6:45am. Our overnight US rates flows saw muted flows during Asian hours with block curve trades (TU-US and TU-UXY) a main focus there. During London's AM hours, Treasuries took a sharp leg lower after the crossover without any observable catalyst. Real$ added paper on the dip (5's to 7's), a consistent theme of late. Overnight Treasury volume was ~90% of average with 10's (136%) seeing some relatively out-sized turnover this morning…

… Our first attachment this morning shows that Treasury 2yrs have recently respected support (4.98% area) derived by their late November high yield print at the level. 2's remain locally oversold (no surprise, see lower panel) but the price action over the last week may be tracing out some form of a bearish continuation pattern. That is, last Wednesday's spasm to higher rates and 4.98% support has only been modestly corrected since. This could be an evolving Bear Flag; we'll know if 4.98% support is taken out with a close. If it is, major support near 5.20% might be the next target for 2yrs.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Negative risk sentiment with equities softer, AUD hampered by mixed Chinese data … Bonds are pressured, and Bunds more-so after German ZEW while Gilts gapped lower on wage numbers … USTs are contained in a narrow nine tick band that is entirely within Monday's 107-18 to 108-22 parameters. Newsflow limited thus far as we await Israel's response to Iran, though the docket ahead is filled with several Fed speakers.

Retail sales registered a robust March increase, with the control group rebounding from soft prints in the prior two months. This month's increase comes alongside continued strong gains in payroll income, consistent with an ongoing virtuous cycle dynamic that has been supercharged by immigration.

BARCAP China: Strong official Q1 GDP marks underlying weakness

The upside surprise in Q1 GDP growth may not be fully capturing underlying developments in the economy. The Q1 rebound is unlikely to be sustained through the rest of year given already slowing March activity and credit data, and no signs of improvement in economic fundamentals. We raise our 2024 GDP outlook.

… On a q/q saar basis, we expect the GDP growth pattern to exhibit a similar pattern to 2023. Following a temporary surge in Q1 (2023: 12.7%), we look for a sharp slowdown to only 0.2% q/q saar in Q2 (versus high Q1 GDP comparison), before returning to an average of 3.5% growth in H2.

On a y/y basis, we expect GDP growth to remain at 5.3% in Q2 thanks to low year-ago basebefore slowing to 4.8% on average in H2. Reflecting the adjustment in the quarterly path (largely due to big upside surprise in Q1 GDP), we revise up our 2024 full-year GDP growth forecast to 5.0% from 4.4%, but keep our 2025 growth forecast unchanged at 4.0%.

We use our models to find trade ideas that provide exposure to rising geopolitical risks but are not dependent on it. We enter long WTI oil, long USDILS and receive USD 5y.

Oil appears cheap according to ComFA, while US yields appear too high according to MarFA™.

Market moves have been broadly in line with BERT’s ‘expansion’ market regime. We maintain exposures to this regime by remaining long USDCLP and USDPEN

… Initiating long US duration: After upside surprises to US inflation and activity data and subsequent repricing of Fed’s cutting path expectations, US rates generally look oversold according to the MarFA™ macro model.

Currently, USD 5y and 10y look 3.2 and 2.3 z-scores too high, respectively, while US 5y and 10y treasuries look 3.1 and 1.6 z-scores too high, respectively.

Geopolitical risks in the Middle East this week, allied with a lack of data releases over the week ahead, could result in lower US yields, in our view. This would particularly be the case if the market was to revert to the ‘Buying assets’ BERT regime (i.e. a decline of real yields on dovish Fed speak). Therefore, we initiate a 5y USD receiver trade, targeting 4.11.

… I continue to believe that it’s going to be incredibly difficult to smoothly land this US economic cycle given we’ve moved from the biggest increase in money supply since WWII to the biggest contraction since the 1930. All with the associated lags. The least likely scenario was always likely to be US growth and inflation moving to trend with anything close to the 6.7 Fed cuts priced in at one point in January. Last year I believed the recession was the most likely outcome but as I said at the start of this year when we changed our view, I think I underestimated the true scale of the stock of stimulus/money still in the system even when the flow turned negative with the tightening of policy. Looser financial conditions since October have exaggerated this and contributed to a boost in activity, inflation and markets this year.

So it's possible that stimulus/liquidity is still working its way through the system and you can see that with Peter Sidorov’s recent work on credit conditions here and here. Peter’s work suggests that the US has benefited from more muted transmission of rate hikes but that there could still be an air pocket of US liquidity later in the year when we return nearer to the long-term money supply trend and finally remove the excesses created. If that’s correct then maybe cutting rates in preparation of that is actually the correct thing to do. However faced with inflation that is currently accelerating that would be very very difficult for the Fed to communicate and be comfortable doing. The lag of policy is incredibly difficult to assess in real time. So the most likely scenario is that rate cuts are delayed (DB only have one cut in December for 2024 now. See here for more) but that in itself creates risks that rates will be left restrictive at the point where the boost from the earlier liquidity overhang runs out.

So a textbook perfect soft landing will still be very difficult to achieve in my opinion. Obviously a no landing but with decent economic growth could be fine for equities while it lasts so the above isn't meant to sound near-term negative but simply to outline the uncertainties that I still think are very large…

Goldilocks: Retail Sales Above Expectations; Empire Manufacturing Below Expectations; Boosting GDP Tracking to 3.1%

BOTTOM LINE: Core retail sales rose 1.1% in March, above expectations. Headline spending also increased by more than expected. The Empire manufacturing index increased by less than expected in April. The composition of the report was weak, with the shipments, new orders, and employment remaining in contractionary territory. The Empire survey has been particularly volatile since 2022, swinging by at least 20 points in over half of instances. We boosted our Q1 GDP tracking estimate by 0.6pp to +3.1% (qoq ar). We boosted our Q1 domestic final sales forecast by 0.7pp to +3.3% (qoq ar).

… To estimate the causal effects, we model state-level economic outcomes—such as job growth or inflation—in a panel regression that exploits the variation in manufacturing GDP shares across states and across time. We also control for the state-level unemployment rate and for the trend in US manufacturing activity. Given the 10% GDP share of manufacturing in the US currently, we estimate that a “typical” rebound in global manufacturing activity would boost 2024 US GDP growth by 0.4pp (Q4/Q4 basis), boost nonfarm payroll growth by at least 30k per month, and would lower the unemployment rate by 0.15-0.3pp by year-end, other things equal. While such an acceleration abroad remains a risk rather than a baseline, these findings increase our conviction in our above-consensus GDP forecast for the year (+2.5% Q4/Q4 basis, vs. consensus +1.4%).

We estimate a more modest impact on 2024 wage growth, at +0.2pp under our preferred specification. The inflation effects are less straightforward, with an estimate range of zero to +0.3pp for year-end core CPI inflation (yoy). The mixed evidence on the inflation effects may reflect the tendency for periods of industrial strength to also exhibit above-average growth in manufacturing capacity. And for 2024 in particular, the continued labor supply tailwind from elevated immigration argues for a smaller-than-normal risk from wage growth or inflation spillovers.

Goldilocks China: Q1 GDP beat expectations amid mixed March activity data

Bottom line: China's Q1 GDP growth came in stronger than our above-consensus forecast, while March activity data delivered a mixed bag. Industrial production growth slowed meaningfully in March and missed expectations, led mainly by slower output growth in computer & other electronics industries. Year-on-year growth in retail sales and services industry output both slowed in March, but the latter held up relatively better. Fixed asset investment growth accelerated in March and beat expectations, thanks to faster manufacturing and infrastructure investment growth. China's sequential growth momentum was robust in Q1 on manufacturing strength and consumption resilience, and the impact of policy easing is gradually kicking in, although property weakness is likely to be prolonged. We maintain our sequential GDP growth forecasts for the coming quarters. Onboarding the Q1 GDP outturn and NBS revisions to 2023 sequential growth estimates, our 2024-25 full-year GDP growth forecasts remain intact at 5.0% and 4.2%, respectively. On the policy front, although the "around 5%" growth target this year is on track, we believe continued policy easing is still necessary, especially on the demand side (e.g., fiscal, housing and consumption), to counteract long-term structural challenges.

1Q real GDP came in strong, driven by export volume and manufacturing capex. However, divergence between real GDP and prices widened in 1Q, and overcapacity worsened. We expect QoQ real GDP growth to moderate from 2Q amid continued debt-deflation risks.

China’s official first quarter GDP data reported surprising strength. Unsurprisingly, this surprise will make the official 2024 growth target easier to achieve. March economic data was less supportive, with weakness evident in production and retail sales figures. The industrial data may reflect the ongoing pivot away from goods by global consumers. Amidst the general hedonism of yesterday’s US retail sales data, the trend away from spending on durables and in favor of spending on services was evident.

US industrial production data is of less global significance than that of China, but it is still important. The localization of supply chains is a trend that will take several years to unfold, and it is futile to look for evidence of that in monthly production figures…

Wells Fargo: In Like a Lion, Out Like a Lion for March Retail Sales

March retail sales handily exceeded expectations with various measures of core spending rising the most in a year or more despite sharp upward revisions. This is not the sort of spending associated with falling prices and brings upside risk to our 2.3% forecast for Q1 consumer spending.

The US economy refuses to land. After March's strong retail sales report was released today, the Atlanta Fed GDPNow tracking model showed Q1's real GDP rising 2.8% (saar), an upward revision from 2.4% as real consumer spending was revised up from 2.9% to 3.4%. That's neither a hard nor a soft landing. The US economy is still flying high. That's because consumers didn't get the recession memo. They keep spending because real disposable income is rising, more Americans are retiring and have the means to do so comfortably, and six million or more "newcomers" are consuming here rather than south of the border.

Today's better-than-expected retail sales report showed a 0.7% m/m gain. Excluding autos, it rose 1.1%, as did the control group which is used to calculate consumer spending in GDP. The latter rose to a new post-pandemic high on an inflation-adjusted basis (chart).

…The yields on Treasury securities have been rising since early this year as stronger- than-expected economic growth, hotter-than-expected CPI inflation, and rising oil prices have convinced more and more investors that the federal funds rate might not get cut after all this year (chart).

Rising yields are starting to weigh on the stock market…

… And from Global Wall Street inbox TO the WWW,

Atlanta FED: First-Quarter GDP Growth Estimate Increased - April 15, 2024

…The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2024 is 2.8 percent on April 15, up from 2.4 percent on April 10. After recent releases from the US Department of the Treasury's Bureau of the Fiscal Service, the US Bureau of Labor Statistics, and the US Census Bureau, increases in nowcasts of first-quarter real personal consumption expenditures growth and first-quarter real gross private domestic investment growth from 2.9 percent and 2.9 percent, respectively, to 3.4 percent and 3.4 percent, were slightly offset by a decrease in the nowcast of first-quarter real government spending growth from 2.6 percent to 2.3 percent, while the nowcast of the contribution of the change in real net exports to first-quarter real GDP growth increased from -0.24 percentage points to -0.15 percentage points…

Bloomberg: Remember 'There Is No Alternative?' Now there is (Authers’ OpED)

Rates rising to a level not seen in a generation undercut the easy allocation to shares. Alan Greenspan’s Fed Model is reappearing.

… If we look at the level of straightforward cash payments, higher rates are more of a problem for share valuations than at any time this millennium. Comparing the dividend yield of the S&P 500 with the two-year Treasury yield, there has been a sudden return to the old status quo, in which short-term bonds yielded more than stocks. As the government must offer an attractive rate to fund its deficits, this is unlikely to change for a while. The TINA (There Is No Alternative) support that low bond yields offered share valuations for a decade after the Global Financial Crisis is now what Ian Harnett of Absolute Strategy Research in London dubs TINY — There Is No Yield on stocks:

Taking a less crude measure, back in the 1990s people used the so-called “Fed Model,” because the central bank’s chairman Alan Greenspan appeared to rely on it in congressional testimony. This held that higher yields on bonds would require a higher earnings yield (the inverse of the price/equity multiple) from stocks. Charting the two measures against each other since 1990 shows why this model was once taken very seriously, and also why it’s dropped out of use in the last two decades:

Now we appear to be back to the status quo ante, with long Treasuries once again yielding more than stocks. This used to be the norm, and was thought to be necessary to compensate investors for bonds’ lack of ability to grow. There’s nothing necessarily alarming about it. But for a generation that had grown accustomed to a stock market that yielded more than bonds, making asset allocation decisions much easier, this development makes life much harder.

It also growsmore difficult to explain just why stocks have rallied the way they have.

In this Chart of the Week, we're going to focus on corporate profit margins.

Corporate profit margins are considered a Leading Indicator of the Business Cycle.

As the chart shows, corporate profit margins tend to peak and decline several quarters before the onset of a Business Cycle recession.

Like most Leading Indicators, the lead time can be highly variable.

To be clear, this chart shows pre-tax corporate profit margins, so the changing effective corporate tax rate does not impact the results.

When corporations notice profit margins starting to decline, they take preemptive steps to protect them, such as scaling back on capital expenditures, reducing the hours of existing employees, and freezing new hiring plans.

All these pre-emptive steps are captured in Leading Indicators of Employment because they foreshadow the final step that businesses take when profit margins continue to decline even after these steps are taken, which is layoffs.

Profit margins have remained highly elevated after the 2020 recession as most of the pandemic windfall landed on corporate balance sheets.

Currently, we see Leading Indicators of Employment moderating as businesses have reduced employee hours, shifted to part-time labor, and reduced hiring intentions, but there has been a huge lag in making the next big step of layoffs because profit margins have provided an extra cushion.

The chart on the right shows how recessions, on average, begin with profit margins around 8% or 9%, and today, margins are at 12%, which allows businesses to wait and delay some of these more binding layoff actions.

Many Leading Indicators of the Business Cycle have been declining and highly negative since the rate hiking cycle began in 2022, but profit margins have been one indicator that has remained elevated and provided a buffer between slowing business conditions and the recessionary step of layoffs.

Fred: Rates related to monetary policy: The fed funds rate stays between the discount rate and the reverse repo rate

Remarkably strong retail sales numbers for March contradict somewhat weaker survey and credit card spending evidence, but with jobs, inflation and activity all beating expectations the Federal Reserve is in no position to carry through with interest rate cuts anytime soon

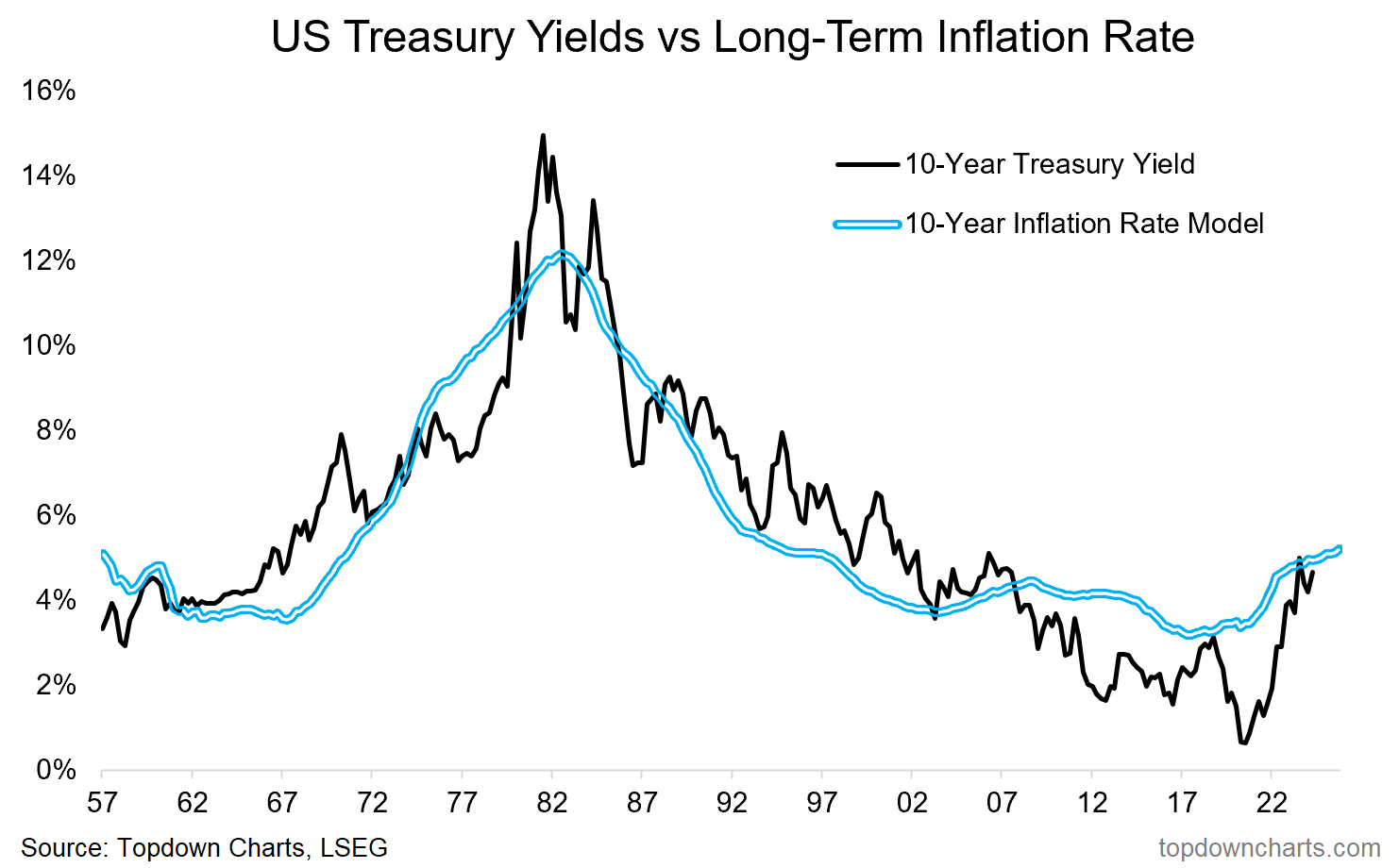

Higher for longer risk is becoming reality for US Treasury Yields..

… So while I want to be bullish bonds because of cheap valuations, and a handful of macro/market models that still point to the potential for lower yields (and an outside, but arguably current lower risk of recession), for now the technicals and fundamentals suggest the path of least resistance is for bond yields to head higher, or at the very least just make themselves right at home in this new higher range.

Key point: A higher long-term rate of inflation = higher for longer level of bond yields…

WolfST: Our Drunken Sailors Binge despite Higher Interest Rates, and the Fed Watches them Nervously

Retail sales by major segment: huge winners (on top: ecommerce and general merchandise retailers), and some big losers.

ZH: 'Hope' Hammered As Empire Fed Plunged In April - Below All Estimates

10's & 30's be blowing out bud; ok not quite soo much now, and Lowe & behold who's on CNBC but none other than Miss Skeletor herself, Lagarde. Interesting symmetries!

Now I sees Mad Maxine, supreme Hoover of SBF campaign CASH herself on CNBC, I guess any leftwing loon can gets on there?! But then Peter Schiff & a BTC pumper-lass were on w/Charles Payne yesterday. Didn't see Alt-Fin YT'ers of 2019 getting on cable in 2024.

{kind=link}

Rate-Cut HOPES spring eternal eh?!

10's & 30's be blowing out bud; ok not quite soo much now, and Lowe & behold who's on CNBC but none other than Miss Skeletor herself, Lagarde. Interesting symmetries!

Now I sees Mad Maxine, supreme Hoover of SBF campaign CASH herself on CNBC, I guess any leftwing loon can gets on there?! But then Peter Schiff & a BTC pumper-lass were on w/Charles Payne yesterday. Didn't see Alt-Fin YT'ers of 2019 getting on cable in 2024.